Download as docx, pdf, or txt

You might also like

- Assessing The Car Rental and Leasing Market in The UAE and QatarDocument2 pagesAssessing The Car Rental and Leasing Market in The UAE and QatarShehjar KaulNo ratings yet

- Bain Cover LetterDocument1 pageBain Cover Letter56seven8100% (2)

- DAMRODocument14 pagesDAMRODusha Periyasamy0% (1)

- Modern Methods of Vocational and Industrial TrainingFrom EverandModern Methods of Vocational and Industrial TrainingNo ratings yet

- Week 4 EntrepDocument4 pagesWeek 4 EntrepHubert S. Banting75% (4)

- Conceptual Framework and Accounting Standard SyllabusDocument12 pagesConceptual Framework and Accounting Standard Syllabusrenzelmagbitang222No ratings yet

- Conceptual Framework and Accounting Standard SyllabusDocument11 pagesConceptual Framework and Accounting Standard SyllabusAnas Aloyodan60% (5)

- PDF Conceptual Framework and Accounting Standard Syllabus DDDocument11 pagesPDF Conceptual Framework and Accounting Standard Syllabus DDMariya BhavesNo ratings yet

- College of Business and Entrepreneurial Technology: Rizal Technological UniversityDocument8 pagesCollege of Business and Entrepreneurial Technology: Rizal Technological Universitypraise ferrerNo ratings yet

- University Mission Statement: Fundamentals of Accountancy, Business & Management 2 Abm - Fabm2Document8 pagesUniversity Mission Statement: Fundamentals of Accountancy, Business & Management 2 Abm - Fabm2kieNo ratings yet

- N-ABM 2 - Business Finance - SyllabusDocument9 pagesN-ABM 2 - Business Finance - SyllabusAnne Jere BajariasNo ratings yet

- ACCT 100-Principles of Financial Accounting - Fall 2018-19Document7 pagesACCT 100-Principles of Financial Accounting - Fall 2018-19Qudsia AbbasNo ratings yet

- Detailed Teaching Syllabus (DTS) and Instructor Guide (Ig'S)Document19 pagesDetailed Teaching Syllabus (DTS) and Instructor Guide (Ig'S)Charo Gironella67% (3)

- Detailed Teaching Syllabus (DTS) and Instructor Guide (Ig'S)Document15 pagesDetailed Teaching Syllabus (DTS) and Instructor Guide (Ig'S)Charo Gironella100% (1)

- ACCT 100 POFA Course Outline Fall Semester 2022-23Document6 pagesACCT 100 POFA Course Outline Fall Semester 2022-23MuhammadNo ratings yet

- ACCT 100-Principle of Financial Accounting-Saira RizwanDocument6 pagesACCT 100-Principle of Financial Accounting-Saira Rizwanraziqachaudhry9665No ratings yet

- Detailed Teaching Syllabus (DTS) and Instructor Guide (Ig'S)Document20 pagesDetailed Teaching Syllabus (DTS) and Instructor Guide (Ig'S)Blecemie MonteraNo ratings yet

- ACCT 221-Corporate Financial Reporting-Atifa Arif Dar-Waqar AliDocument7 pagesACCT 221-Corporate Financial Reporting-Atifa Arif Dar-Waqar AliAbdelmonim Awad OsmanNo ratings yet

- Principles of Financial AccountingDocument7 pagesPrinciples of Financial AccountingmfaizanzahidNo ratings yet

- ACCT 220-Corporate Financial Reporting-I-Samia AliDocument9 pagesACCT 220-Corporate Financial Reporting-I-Samia Alinetflix accountNo ratings yet

- ACCT 100-Principles of Financial Accounting - Atifa Dar - Omair HaroonDocument7 pagesACCT 100-Principles of Financial Accounting - Atifa Dar - Omair HaroonAbdelmonim Awad OsmanNo ratings yet

- ACCT 100 POFA Course Outline Fall Semester 2020 - Online - Updated Oct 1 2020 - 1Document7 pagesACCT 100 POFA Course Outline Fall Semester 2020 - Online - Updated Oct 1 2020 - 1Usama KhanNo ratings yet

- Principles of Financial AccountingDocument7 pagesPrinciples of Financial Accountinghnoor94No ratings yet

- Lahore University of Management Sciences ACCT 321 Advance Financial ReportingDocument5 pagesLahore University of Management Sciences ACCT 321 Advance Financial ReportingusamaNo ratings yet

- Module 1 TheAcctgProfAndConceptualFrameworkDocument2 pagesModule 1 TheAcctgProfAndConceptualFrameworkMin YoongiNo ratings yet

- Module 1 Packet: College OF CommerceDocument14 pagesModule 1 Packet: College OF CommerceCJ GranadaNo ratings yet

- EIH Spring 2024Document10 pagesEIH Spring 2024arfanajam18No ratings yet

- Detailed Teaching Syllabus (DTS) and Instructor Guide (Ig'S)Document10 pagesDetailed Teaching Syllabus (DTS) and Instructor Guide (Ig'S)Charo Gironella100% (1)

- Tomas Del Rosario College: City of Balanga Curricular Program: AccountancyDocument12 pagesTomas Del Rosario College: City of Balanga Curricular Program: AccountancyVanessa L. VinluanNo ratings yet

- Syllabus in Intro To AcctgDocument9 pagesSyllabus in Intro To AcctgKryzzle Tritz DangelNo ratings yet

- Masbate Polytechnic and Development College, Inc.: VisionDocument7 pagesMasbate Polytechnic and Development College, Inc.: VisionRobelyn Fababier VeranoNo ratings yet

- ACCT 100-Principles of Financial AccountingDocument7 pagesACCT 100-Principles of Financial AccountingZulfeqar HaiderNo ratings yet

- Financial Statement Analysis: Standard Course OutlineDocument6 pagesFinancial Statement Analysis: Standard Course OutlineMahmoud ZizoNo ratings yet

- Xmanac1 Syl IbmDocument12 pagesXmanac1 Syl IbmMark Anthony ManarangNo ratings yet

- ACCT 321-Advance Financial-Atifa Arif DarDocument6 pagesACCT 321-Advance Financial-Atifa Arif DarmonimawadNo ratings yet

- JMC Guidelines and Template For Compendium 2 1Document63 pagesJMC Guidelines and Template For Compendium 2 1kingsters zabateNo ratings yet

- Lahore University of Management Sciences ACCT 100 - Principles of Financial AccountingDocument6 pagesLahore University of Management Sciences ACCT 100 - Principles of Financial AccountingAli Zain ParharNo ratings yet

- MCD4013 Pemasaran Perkhidmatan Kewangan-New SLTDocument5 pagesMCD4013 Pemasaran Perkhidmatan Kewangan-New SLThisyamstarkNo ratings yet

- ACCT220 CFR-1 OutlineDocument6 pagesACCT220 CFR-1 OutlineReward IntakerNo ratings yet

- ACCT 100 - Principles of Financial AccountingDocument7 pagesACCT 100 - Principles of Financial AccountingHaseeb Nasir SheikhNo ratings yet

- AE11Document11 pagesAE11Jinrey AzuriasNo ratings yet

- AC 1103 OBEdized Syllabi FINALDocument19 pagesAC 1103 OBEdized Syllabi FINALEdgar L. AlbiaNo ratings yet

- Ita - Occ - Obe Syllabus Sy 2022-2023Document7 pagesIta - Occ - Obe Syllabus Sy 2022-2023Ruffaidah LantodNo ratings yet

- Financial Accounting and Information Systems: Class MBADocument6 pagesFinancial Accounting and Information Systems: Class MBADaniyal JunaidNo ratings yet

- Dr. Gloria D. Lacson Foundation Colleges, IncDocument5 pagesDr. Gloria D. Lacson Foundation Colleges, IncMa. Liza MagatNo ratings yet

- ACC 12 - Entrepreneurial Accounting Course Study GuideDocument66 pagesACC 12 - Entrepreneurial Accounting Course Study GuideHannah Jean MabunayNo ratings yet

- BusfinDocument6 pagesBusfinEg EgNo ratings yet

- Philippine Countryville College, Inc.: PreliminaryDocument5 pagesPhilippine Countryville College, Inc.: PreliminaryEg Eg100% (1)

- Acco 30013 Accounting For Special Transactions 2019Document8 pagesAcco 30013 Accounting For Special Transactions 2019Azel Ann AlibinNo ratings yet

- BBDocument9 pagesBBChreann RachelNo ratings yet

- Module 7 Packet: College OF CommerceDocument13 pagesModule 7 Packet: College OF CommerceCJ GranadaNo ratings yet

- Syllabus - Introduction To Financial Accounting - SY 2023 2024Document11 pagesSyllabus - Introduction To Financial Accounting - SY 2023 2024Saila mae SurioNo ratings yet

- RPS Manajemen Keuangan 1 - 2021 - EngDocument13 pagesRPS Manajemen Keuangan 1 - 2021 - EngAisyah RianiNo ratings yet

- ACCT320 CFR-2 Course Outline Spring 2020Document7 pagesACCT320 CFR-2 Course Outline Spring 2020Waris AliNo ratings yet

- Detailed Teaching Syllabus (DTS) and Instructor Guide (Ig'S)Document13 pagesDetailed Teaching Syllabus (DTS) and Instructor Guide (Ig'S)Charo GironellaNo ratings yet

- ADV ACCTG. 2 Syllabus MCUDocument26 pagesADV ACCTG. 2 Syllabus MCUFiona CondeNo ratings yet

- JMC Guidelines and Template For Compendium 2Document63 pagesJMC Guidelines and Template For Compendium 2kingsters zabateNo ratings yet

- Financial Accounting Theory and Reporting IDocument16 pagesFinancial Accounting Theory and Reporting IKendrick PajarinNo ratings yet

- Financial ManagementDocument109 pagesFinancial ManagementAlfe PinongpongNo ratings yet

- Principles of FinanceDocument9 pagesPrinciples of FinanceOmar FarukNo ratings yet

- ACCT 411-Applied Financial Analysis-Atifa Arif DarDocument5 pagesACCT 411-Applied Financial Analysis-Atifa Arif Darnetflix accountNo ratings yet

- L1 BI - FSM0716 Principle of Business ManagementDocument4 pagesL1 BI - FSM0716 Principle of Business ManagementNur Sakinah IdrisNo ratings yet

- A Trainer’S Guide for Preclinical Courses in Medicine: Series I Introduction to MedicineFrom EverandA Trainer’S Guide for Preclinical Courses in Medicine: Series I Introduction to MedicineNo ratings yet

- Input Data Sheet For SHS E-Class Record: Learners' NamesDocument11 pagesInput Data Sheet For SHS E-Class Record: Learners' NamesMariya BhavesNo ratings yet

- Input Data Sheet For SHS E-Class Record: Learners' NamesDocument10 pagesInput Data Sheet For SHS E-Class Record: Learners' NamesMariya BhavesNo ratings yet

- Input Data Sheet For SHS E-Class Record: Learners' NamesDocument10 pagesInput Data Sheet For SHS E-Class Record: Learners' NamesMariya BhavesNo ratings yet

- Input Data Sheet For SHS E-Class Record: Learners' NamesDocument11 pagesInput Data Sheet For SHS E-Class Record: Learners' NamesMariya BhavesNo ratings yet

- Input Data Sheet For SHS E-Class Record: Learners' NamesDocument11 pagesInput Data Sheet For SHS E-Class Record: Learners' NamesMariya BhavesNo ratings yet

- Grading Sheet For FINANCE 2Document1 pageGrading Sheet For FINANCE 2Mariya BhavesNo ratings yet

- Logistic ManagementDocument1 pageLogistic ManagementMariya BhavesNo ratings yet

- Chapter 3Document3 pagesChapter 3Mariya BhavesNo ratings yet

- PDPRDocument1 pagePDPRMariya BhavesNo ratings yet

- Chapter 2-3 Strategic ManagementDocument5 pagesChapter 2-3 Strategic ManagementMariya BhavesNo ratings yet

- SPss Project BeveragesDocument6 pagesSPss Project BeveragesMariya BhavesNo ratings yet

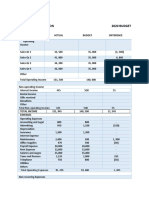

- Twinnies Corporation 2020 BudgetDocument2 pagesTwinnies Corporation 2020 BudgetMariya BhavesNo ratings yet

- Chapter 6-7 Strategic ManagementDocument5 pagesChapter 6-7 Strategic ManagementMariya BhavesNo ratings yet

- Chapter 3Document5 pagesChapter 3Mariya BhavesNo ratings yet

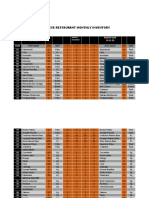

- Japanese Restaurant Monthly InventoryDocument2 pagesJapanese Restaurant Monthly InventoryMariya BhavesNo ratings yet

- Analitycal Ability 02Document20 pagesAnalitycal Ability 02Morium ZafarNo ratings yet

- MSDM 03 Strategic HRM & HR ScorecardDocument12 pagesMSDM 03 Strategic HRM & HR Scorecardakos kosasihNo ratings yet

- Learning Diary Chapter 01 MGT702 1922000303Document4 pagesLearning Diary Chapter 01 MGT702 1922000303Syed Muhammed Sabeehul RehmanNo ratings yet

- Session 2 Teachers GuideDocument10 pagesSession 2 Teachers GuideJoanna ChongNo ratings yet

- Design Thinking and Creativity For InnovationDocument10 pagesDesign Thinking and Creativity For InnovationAnanya DeyNo ratings yet

- Occupational Health, Safety and Wellbeing Strategy 2016-2021Document22 pagesOccupational Health, Safety and Wellbeing Strategy 2016-2021Taufan Arif ZulkarnainNo ratings yet

- Chapter 1BDocument13 pagesChapter 1BShreyaSomvanshiNo ratings yet

- Academedia Annualreport 2122Document111 pagesAcademedia Annualreport 2122Shaun HeelanNo ratings yet

- Negotiation Skills: Free ReportDocument19 pagesNegotiation Skills: Free ReportpadmasunilNo ratings yet

- The Wealth BibleDocument32 pagesThe Wealth BibleJose Luis Garcés MontoyaNo ratings yet

- Bank of The Philippine Islands and Mercury DrugDocument6 pagesBank of The Philippine Islands and Mercury DrugKim TaehyungNo ratings yet

- ECE001 - Engineering EconomyDocument6 pagesECE001 - Engineering EconomyJacob Chico SueroNo ratings yet

- Innovative Greeks Event ReportDocument32 pagesInnovative Greeks Event ReportNikos AnastopoulosNo ratings yet

- CharusankarganeshresumeDocument1 pageCharusankarganeshresumeapi-527241539No ratings yet

- E2 March 2011 QueDocument12 pagesE2 March 2011 QuebunipatNo ratings yet

- Annual Report: Unilever Pakistan Foods LimitedDocument100 pagesAnnual Report: Unilever Pakistan Foods LimitedDanishNo ratings yet

- Formato Curriculum Vitade Hoja de Vida en InglésDocument4 pagesFormato Curriculum Vitade Hoja de Vida en InglésanahyNo ratings yet

- Materiais 9201455476Document95 pagesMateriais 9201455476Nilton Cesar marcelinoNo ratings yet

- Socio Economic FactorsDocument22 pagesSocio Economic Factorslance sibayanNo ratings yet

- Literature Review Wealth ManagementDocument7 pagesLiterature Review Wealth Managementea2pbjqk100% (1)

- Chapter 1 SummaryDocument6 pagesChapter 1 SummarytaxnodestestdemoNo ratings yet

- IIMC APMP Brochure 2020 - 1Document17 pagesIIMC APMP Brochure 2020 - 1vivek punjabiNo ratings yet

- Activity Sheets Environment and Market 2Document3 pagesActivity Sheets Environment and Market 2Marlon Raluto GervacioNo ratings yet

- Samantha Roberts CVDocument2 pagesSamantha Roberts CVSammy RobertsNo ratings yet

- Discussion Questions - 221030 - 141623Document21 pagesDiscussion Questions - 221030 - 141623Heitham OmarNo ratings yet

- (Download PDF) Business Strategy Development Application 3Rd Edition Gary Bissonette Full Chapter PDFDocument69 pages(Download PDF) Business Strategy Development Application 3Rd Edition Gary Bissonette Full Chapter PDFbazziqaim4100% (11)

- Cambridge IGCSE: Design & Technology 0445/12Document4 pagesCambridge IGCSE: Design & Technology 0445/12...No ratings yet