Download as pdf or txt

You might also like

- CISSP October Slides - Learner Slides PDFDocument560 pagesCISSP October Slides - Learner Slides PDFVelicia Vera80% (5)

- Financial Management Theory and Practice 13th Edition Brigham Solutions ManualDocument35 pagesFinancial Management Theory and Practice 13th Edition Brigham Solutions Manualrappelpotherueo100% (23)

- Statement of Changes in Equity: Caf 5 - Ias 1Document24 pagesStatement of Changes in Equity: Caf 5 - Ias 1amitsinghslideshare100% (1)

- Note Topic 3Document8 pagesNote Topic 3ModraNo ratings yet

- Note Topic 3.Document4 pagesNote Topic 3.ModraNo ratings yet

- Abm 4 Module 4Document4 pagesAbm 4 Module 4Argene AbellanosaNo ratings yet

- Finance Quick Reference GuideDocument16 pagesFinance Quick Reference GuideNathalia Montoya DiazNo ratings yet

- Statement of Changes in EquityDocument65 pagesStatement of Changes in EquityJhie Anne MayoNo ratings yet

- accounting(分享版)Document7 pagesaccounting(分享版)Siyang QuNo ratings yet

- Income StatementDocument2 pagesIncome StatementJereme PascuaNo ratings yet

- Sme PfrsDocument9 pagesSme PfrsAlmae Joy DieteNo ratings yet

- SAP Financial Planning v1.0Document42 pagesSAP Financial Planning v1.0edoardo.dellaferreraNo ratings yet

- Purpose of Income StatementDocument11 pagesPurpose of Income StatementNhật QuyênNo ratings yet

- Chapter 2 Bus FinDocument19 pagesChapter 2 Bus FinMickaella DukaNo ratings yet

- Ingles Infografia - EE - FF - Samuel ToctoDocument2 pagesIngles Infografia - EE - FF - Samuel Toctosamuel denilson tocto peñaNo ratings yet

- Accounting KPIs LkdInDocument10 pagesAccounting KPIs LkdInGeorge BerberiNo ratings yet

- Financial Management - ResumosDocument10 pagesFinancial Management - ResumosBeatriz BastosNo ratings yet

- Manual of Accounting Policies (MAP) : Shareholders EquityDocument10 pagesManual of Accounting Policies (MAP) : Shareholders EquityMiruna RaduNo ratings yet

- Income Statement - Reading PDFDocument9 pagesIncome Statement - Reading PDFNishant ShrivastavaNo ratings yet

- Intro To Economics Lecture 1 - Elements of FSDocument28 pagesIntro To Economics Lecture 1 - Elements of FSАлихан МажитовNo ratings yet

- Fundamentals of AccountingDocument3 pagesFundamentals of AccountingImma Therese YuNo ratings yet

- Notes To Financial Statement MeaningDocument2 pagesNotes To Financial Statement MeaningChincel G. ANINo ratings yet

- 2018 Quarter 4 Report: Presented by You ExecDocument20 pages2018 Quarter 4 Report: Presented by You ExecLohith t rNo ratings yet

- Chapter 2 Concept 16 To 22Document7 pagesChapter 2 Concept 16 To 22sundaram MishraNo ratings yet

- Group Reporting II: Application of The Acquisition Method Under IFRS 3Document77 pagesGroup Reporting II: Application of The Acquisition Method Under IFRS 3فهد التويجريNo ratings yet

- Business FinanceDocument14 pagesBusiness Financeericamae lavapieNo ratings yet

- EBOOK6131f1fd1229c Unit 5 Company Financial Statements PDFDocument36 pagesEBOOK6131f1fd1229c Unit 5 Company Financial Statements PDFYaw Antwi-AddaeNo ratings yet

- Chapter 17 - Earnings Per Share and Retained Earnings PDFDocument59 pagesChapter 17 - Earnings Per Share and Retained Earnings PDFDaniela MacaveiuNo ratings yet

- Group 6 - Management Control System of Measurement and Control of Managed AssetsDocument25 pagesGroup 6 - Management Control System of Measurement and Control of Managed AssetsHernawatiNo ratings yet

- Forum 5 - 43219010035 - Leonita Mega PratiwiDocument7 pagesForum 5 - 43219010035 - Leonita Mega PratiwiLeonita Mega PratiwiNo ratings yet

- Full Download Corporate Finance A Focused Approach 5th Edition Ehrhardt Solutions ManualDocument36 pagesFull Download Corporate Finance A Focused Approach 5th Edition Ehrhardt Solutions Manualkisslingcicelypro100% (40)

- Dwnload Full Corporate Finance A Focused Approach 5th Edition Ehrhardt Solutions Manual PDFDocument36 pagesDwnload Full Corporate Finance A Focused Approach 5th Edition Ehrhardt Solutions Manual PDFmiltongoodwin2490i100% (20)

- Noer Rachmadhani H - 1810523011 - Week 10 AssignmentDocument9 pagesNoer Rachmadhani H - 1810523011 - Week 10 AssignmentSajakul SornNo ratings yet

- 2 - Partnership OperationsDocument14 pages2 - Partnership Operationslou-924No ratings yet

- Tutorial A40 Kis Aktuaria/Materi TGL 15 A40Document40 pagesTutorial A40 Kis Aktuaria/Materi TGL 15 A40nirmalazintaNo ratings yet

- ACCTG 1st Sem Prelim NotesDocument11 pagesACCTG 1st Sem Prelim NoteshjNo ratings yet

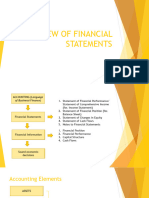

- Chapter 2-Overview of Financial StatementsDocument26 pagesChapter 2-Overview of Financial StatementsTESDA Regional Training Center- TaclobanNo ratings yet

- Module 013 Week005-Statement of Changes in Equity, Accounting Policies, Changes in Accounting Estimates and ErrorsDocument7 pagesModule 013 Week005-Statement of Changes in Equity, Accounting Policies, Changes in Accounting Estimates and Errorsman ibeNo ratings yet

- Ratios and InterpretationDocument6 pagesRatios and Interpretationjohngay1987No ratings yet

- Chapter 17Document16 pagesChapter 17soniadhingra1805No ratings yet

- Dividends Are Payments Made by A: Corporation ShareholderDocument6 pagesDividends Are Payments Made by A: Corporation ShareholderPavan RajeshNo ratings yet

- Functions: DisclosesDocument10 pagesFunctions: Disclosesdownlodemaster1No ratings yet

- Topic: Introduction To Financial Statements K W LDocument3 pagesTopic: Introduction To Financial Statements K W LSabeen KhalidNo ratings yet

- Finman ReviewerDocument8 pagesFinman ReviewerRafael BensigNo ratings yet

- Accounting For Business: Asso. Prof. Dr. Nguyen Thi Phuong HoaDocument37 pagesAccounting For Business: Asso. Prof. Dr. Nguyen Thi Phuong HoaTam DoNo ratings yet

- Changes in OwnerDocument1 pageChanges in OwnertaetaeNo ratings yet

- (VALIX) SCE - Accounting ChangesDocument45 pages(VALIX) SCE - Accounting ChangesMaeNo ratings yet

- Chapter 8 - CorporationDocument7 pagesChapter 8 - CorporationNyah MallariNo ratings yet

- 2018 Quarter 4 Report: Presented by You ExecDocument20 pages2018 Quarter 4 Report: Presented by You ExecLohith t rNo ratings yet

- 2019 Quarter One Report: Presented by You ExecDocument21 pages2019 Quarter One Report: Presented by You ExecdayanaNo ratings yet

- Topic: Introduction To Financial Statements K W LDocument3 pagesTopic: Introduction To Financial Statements K W Lfatima waqar100% (1)

- EDHEC - MSC Fin - FAA - Overview of The Income StatementDocument27 pagesEDHEC - MSC Fin - FAA - Overview of The Income StatementGabriele GabrieliNo ratings yet

- Accounting: Quantitative Information Primarily Financial inDocument19 pagesAccounting: Quantitative Information Primarily Financial inleeeydoNo ratings yet

- Fabm 2Document7 pagesFabm 2Akaashi KeijiNo ratings yet

- Chap7 PDFDocument61 pagesChap7 PDFAshraf Alawneh100% (1)

- Business Finance PDFDocument38 pagesBusiness Finance PDFSamantha OcfemiaNo ratings yet

- Group Reporting II: Application of The Acquisition Method Under IFRS 3Document77 pagesGroup Reporting II: Application of The Acquisition Method Under IFRS 3Hà PhươngNo ratings yet

- Tugas Modul Pertemuan Ke-2: Accounting PeroidDocument4 pagesTugas Modul Pertemuan Ke-2: Accounting PeroidThita NurpitasariNo ratings yet

- Statement of Changes in EquityDocument4 pagesStatement of Changes in Equityfrancis albaracinNo ratings yet

- Materi Kel 1 FATDocument30 pagesMateri Kel 1 FATFawwazNo ratings yet

- Analysis of Credit Risk Measurement UsinDocument6 pagesAnalysis of Credit Risk Measurement UsinDia-wiNo ratings yet

- 4th Chapter Business Government and Institutional BuyingDocument17 pages4th Chapter Business Government and Institutional BuyingChristine Nivera-PilonNo ratings yet

- ED Hiring GuideDocument20 pagesED Hiring Guidechokx008No ratings yet

- Korean Made Easy For Beginners 2nd Edition by Seu 22Document36 pagesKorean Made Easy For Beginners 2nd Edition by Seu 22takoshaloshviliNo ratings yet

- IncotermsDocument39 pagesIncotermsVipin Singh Gautam100% (1)

- Jeopardy SolutionsDocument14 pagesJeopardy SolutionsMirkan OrdeNo ratings yet

- 14-128 MTR Veh Appraisal FormDocument2 pages14-128 MTR Veh Appraisal FormJASONNo ratings yet

- Profiles of For-Profit Education Management Companies: Fifth Annual Report 2002-2003Document115 pagesProfiles of For-Profit Education Management Companies: Fifth Annual Report 2002-2003National Education Policy CenterNo ratings yet

- Annual Report 2020 V3Document179 pagesAnnual Report 2020 V3Uswa KhurramNo ratings yet

- Nnadili v. Chevron U.s.a., Inc.Document10 pagesNnadili v. Chevron U.s.a., Inc.RavenFoxNo ratings yet

- P2mys 2009 Jun ADocument14 pagesP2mys 2009 Jun Aamrita tamangNo ratings yet

- Debate Against UA PDFDocument5 pagesDebate Against UA PDFHermione Shalimar Justice CaspeNo ratings yet

- Alternative Dispute Resolution Syllabus LLMDocument5 pagesAlternative Dispute Resolution Syllabus LLMprernaNo ratings yet

- Retail Banking AdvancesDocument38 pagesRetail Banking AdvancesShruti SrivastavaNo ratings yet

- STUDENT 2021-2022 Academic Calendar (FINAL)Document1 pageSTUDENT 2021-2022 Academic Calendar (FINAL)Babar ImtiazNo ratings yet

- TED Taiye SelasiDocument4 pagesTED Taiye SelasiMinh ThuNo ratings yet

- Gulf Times: HMC Providing State-Of-The-Art Treatment To All Covid-19 PatientsDocument20 pagesGulf Times: HMC Providing State-Of-The-Art Treatment To All Covid-19 PatientsmurphygtNo ratings yet

- Media Release 3665 (English) 14 08 14Document2 pagesMedia Release 3665 (English) 14 08 14ElPaisUyNo ratings yet

- Assignment of MGT 2133 (Section: 08) : Date of Submission: 24 August 2017Document17 pagesAssignment of MGT 2133 (Section: 08) : Date of Submission: 24 August 2017Mahzabeen NahidNo ratings yet

- Lecture 03 - ECO 209 - W2013 PDFDocument69 pagesLecture 03 - ECO 209 - W2013 PDF123No ratings yet

- Best BA Outline-HagueDocument195 pagesBest BA Outline-HagueAsia LemmonNo ratings yet

- SPIL - Geneva ConventionDocument4 pagesSPIL - Geneva ConventionInna LadislaoNo ratings yet

- Asian Paints: Sales Turnover: Sales Turnover of The Asian Paints Is Shows The Remarkable Increase FromDocument3 pagesAsian Paints: Sales Turnover: Sales Turnover of The Asian Paints Is Shows The Remarkable Increase FromHarsh AryaNo ratings yet

- 2 - AC Corporation (ACC) v. CIRDocument20 pages2 - AC Corporation (ACC) v. CIRCarlota VillaromanNo ratings yet

- Aipmt Round 3Document335 pagesAipmt Round 3AnweshaBoseNo ratings yet

- Mayank Mehta EYDocument10 pagesMayank Mehta EYyasmeenfatimak52No ratings yet

- Entrepreneurship Module 8Document7 pagesEntrepreneurship Module 8Jay Mark Dulce HalogNo ratings yet

- Digest Partnership CaseDocument12 pagesDigest Partnership Casejaynard9150% (2)

- Grey Alba Vs Dela CruzDocument4 pagesGrey Alba Vs Dela CruzJamie StevensNo ratings yet