Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5834)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (350)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (824)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (405)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Profile of A Treatment Plan:: Early Stage Middle Stage Late StageDocument37 pagesProfile of A Treatment Plan:: Early Stage Middle Stage Late StageLea Laura100% (1)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- International TradeDocument5 pagesInternational TradeAsif Nawaz ArishNo ratings yet

- Deliverance QuestionnaireDocument9 pagesDeliverance Questionnaireyoutube_archangel100% (3)

- Business Office Manager Administrator in NYC Resume M Crawford GardnerDocument3 pagesBusiness Office Manager Administrator in NYC Resume M Crawford GardnerMCrawfordGardnerNo ratings yet

- Acumen West Africa One PagerDocument2 pagesAcumen West Africa One PagertobointNo ratings yet

- RMFB5 Schedule of Yuletide Break Updated December 17 2022 BDocument17 pagesRMFB5 Schedule of Yuletide Break Updated December 17 2022 Bjohn paul AbraganNo ratings yet

- HistoryDocument3 pagesHistoryberardmanon12No ratings yet

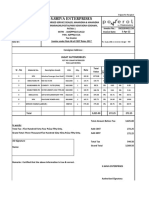

- S.Shiva Enterprises: Jagat AutomobilesDocument2 pagesS.Shiva Enterprises: Jagat AutomobilesS.SHIVA ENTERPRISESNo ratings yet

- Tajweed TerminologyDocument2 pagesTajweed TerminologyJawedsIslamicLibraryNo ratings yet

- Av4 SyllDocument3 pagesAv4 Syllapi-262711797No ratings yet

- CHN ReviewerDocument10 pagesCHN ReviewerAyessa Yvonne PanganibanNo ratings yet

- AccountStatement JUL 2021Document2 pagesAccountStatement JUL 2021Hatem FaroukNo ratings yet

- VPN Owners Unveiled 97 VPN Products Run by Just 23 Companies InfographicDocument1 pageVPN Owners Unveiled 97 VPN Products Run by Just 23 Companies InfographicPeter PanNo ratings yet

- Csec Poa: Page 8 of 24Document1 pageCsec Poa: Page 8 of 24Tori GeeNo ratings yet

- Early Life and Military Career: Milan Nedić (Document10 pagesEarly Life and Military Career: Milan Nedić (Jovan PerićNo ratings yet

- Thesis Topic - 2015-2020 BATCH, MCAPDocument2 pagesThesis Topic - 2015-2020 BATCH, MCAPDestro NNo ratings yet

- Soal Pas Aqidah 7 Ganjil 2021Document50 pagesSoal Pas Aqidah 7 Ganjil 2021SolichudinNo ratings yet

- Bride and PrejudiceDocument5 pagesBride and PrejudiceLaReine_Salma__2189No ratings yet

- Lisacenter WolfempowermentDocument4 pagesLisacenter WolfempowermentVedvyas100% (2)

- Business Intelligence (BI) Frequently Asked Questions (FAQ)Document9 pagesBusiness Intelligence (BI) Frequently Asked Questions (FAQ)Milind ChavareNo ratings yet

- Partnership With Community - 26 Jan 2018Document38 pagesPartnership With Community - 26 Jan 2018farajhiNo ratings yet

- 33 Al Ahzab TranslationDocument18 pages33 Al Ahzab TranslationAbbey IshaqNo ratings yet

- Skylanders Trap Team Characters - Google Search 3Document1 pageSkylanders Trap Team Characters - Google Search 3amkomota3No ratings yet

- English Core 5Document14 pagesEnglish Core 5Tanu Singh100% (1)

- Development of Hot Cells and Their Embedded PartsDocument3 pagesDevelopment of Hot Cells and Their Embedded PartsK. JayarajanNo ratings yet

- Energy Management in An Automated Solar Powered Irrigation SystemDocument6 pagesEnergy Management in An Automated Solar Powered Irrigation Systemdivya1587No ratings yet

- Koustuv AssignmentsDocument5 pagesKoustuv AssignmentsKoustuv PokhrelNo ratings yet

- Business PlanDocument46 pagesBusiness PlanJhon Fernan MadolidNo ratings yet

- CBSE SolutionDocument80 pagesCBSE SolutionMuktara LisaNo ratings yet

- History of Solar Cell DevelopmentDocument12 pagesHistory of Solar Cell DevelopmentFerdous ShamaunNo ratings yet