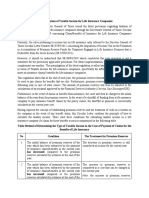

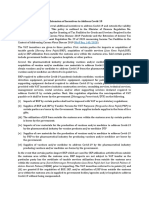

Exemptions of Aid, Donations, and Grants From Objects of Income Tax

Exemptions of Aid, Donations, and Grants From Objects of Income Tax

You might also like

- Newsletter - Agustus I - Part IIIDocument11 pagesNewsletter - Agustus I - Part IIIDaisy Anita SusiloNo ratings yet

- Analysis of Finance Bill 2024 13 May 2024 - 002Document67 pagesAnalysis of Finance Bill 2024 13 May 2024 - 002ondalafrederickNo ratings yet

- Required ReadingDocument11 pagesRequired ReadingJennelyn Asas PagaduanNo ratings yet

- GST On TrustDocument4 pagesGST On TruststeveNo ratings yet

- Assessment of Charitable Trust and InstitutionDocument52 pagesAssessment of Charitable Trust and InstitutionAnonymous JJhHAdY5HzNo ratings yet

- Tax-Free Exchanges That Are Not Subject To Income Tax, Capital Gains Tax, Documentary Stamp Tax And/or Value-Added Tax, As The Case May BeDocument7 pagesTax-Free Exchanges That Are Not Subject To Income Tax, Capital Gains Tax, Documentary Stamp Tax And/or Value-Added Tax, As The Case May BeJouhara ObeñitaNo ratings yet

- Kenya Proposes Tax Changes Under The Finance Bill - 061808Document25 pagesKenya Proposes Tax Changes Under The Finance Bill - 061808lenarokushulNo ratings yet

- GEC Nov 13Document7 pagesGEC Nov 13koreanissueNo ratings yet

- Types of Organizations Revised Corporation CodeDocument11 pagesTypes of Organizations Revised Corporation CodeNadie LrdNo ratings yet

- DT InterviewDocument37 pagesDT Interviewanjali aggarwalNo ratings yet

- Rationale For The Imposition of TaxesDocument5 pagesRationale For The Imposition of TaxesBurnok SupolNo ratings yet

- The TRAIN Law and The Poor Antonio P. Contreras: BY ON JANUARY 30, 201Document7 pagesThe TRAIN Law and The Poor Antonio P. Contreras: BY ON JANUARY 30, 201Jellah Lorezo AbreganaNo ratings yet

- Modelo de Informe en Inglés TRIBUTACIONDocument8 pagesModelo de Informe en Inglés TRIBUTACIONPatrick ArteagaNo ratings yet

- Uae Corporate Tax Law SummaryDocument37 pagesUae Corporate Tax Law SummarypankajNo ratings yet

- Union Budget 2023 For NGOsDocument7 pagesUnion Budget 2023 For NGOsGOODS AND SERVICES TAXNo ratings yet

- Ovw1 1 - ST Ataglance 19may16Document4 pagesOvw1 1 - ST Ataglance 19may16Sanjog DewanNo ratings yet

- Tax Alert (April 2020) FinalDocument30 pagesTax Alert (April 2020) FinalRheneir MoraNo ratings yet

- Public Accounts 2013-14 SaskatchewanDocument270 pagesPublic Accounts 2013-14 SaskatchewanAnishinabeNo ratings yet

- Rmo 20-2013Document7 pagesRmo 20-2013Carlos105No ratings yet

- Chapter 2. EditedDocument9 pagesChapter 2. EditedJellah Lorezo AbreganaNo ratings yet

- Alana - Self-Assessment Module 2Document3 pagesAlana - Self-Assessment Module 2kate trishaNo ratings yet

- GST BILL Highlights of Draft Model GST LawDocument6 pagesGST BILL Highlights of Draft Model GST LawS Sinha RayNo ratings yet

- Taxable Event Under GSTDocument4 pagesTaxable Event Under GSTSuman SharmaNo ratings yet

- BIR 10-2003 Implementing The Tax Incentives Provisions RA 8525 Adopt-A-School Act of 1998Document5 pagesBIR 10-2003 Implementing The Tax Incentives Provisions RA 8525 Adopt-A-School Act of 1998LakanPH100% (1)

- Courage vs. CIRDocument2 pagesCourage vs. CIRMike E Dm33% (3)

- Tax AssessmentsDocument3 pagesTax AssessmentsKing AlduezaNo ratings yet

- Courage Vs CIRDocument8 pagesCourage Vs CIRAna GNo ratings yet

- Law of TaxationDocument3 pagesLaw of TaxationmangalagowrirudrappaNo ratings yet

- An Economic Impact Analysis On Tax Reform For Acceleration and Inclusion or Train BillDocument6 pagesAn Economic Impact Analysis On Tax Reform For Acceleration and Inclusion or Train BillZarina BartolayNo ratings yet

- Negative List of ServicesDocument104 pagesNegative List of ServicesGautam SinghNo ratings yet

- PFA Final Exam October 2022Document4 pagesPFA Final Exam October 2022Jay PugonNo ratings yet

- 2013 Tax-Exemption Guidelines For Non-Stock, Nonprofit Corporations FDM 8.1.13Document2 pages2013 Tax-Exemption Guidelines For Non-Stock, Nonprofit Corporations FDM 8.1.13cyrilNo ratings yet

- Train Law: What Does It Change?: Tax Reform For Acceleration and Inclusion (Train) LawDocument8 pagesTrain Law: What Does It Change?: Tax Reform For Acceleration and Inclusion (Train) LawJoan PaynorNo ratings yet

- TRAIN Law Implementing Rules and Regulations - Facing PH TaxesDocument10 pagesTRAIN Law Implementing Rules and Regulations - Facing PH Taxesreneth davidNo ratings yet

- Tax Guide On The Deduction of Medical, Physical Impairment and Disability Expenses (Issue 3)Document28 pagesTax Guide On The Deduction of Medical, Physical Impairment and Disability Expenses (Issue 3)iadhiaNo ratings yet

- Taxpayers Remedies For FDDADocument2 pagesTaxpayers Remedies For FDDAalmira halasanNo ratings yet

- Train Law-Wps OfficeDocument4 pagesTrain Law-Wps OfficeAdam Ross Toledo BrionesNo ratings yet

- S.G.T College, BallariDocument5 pagesS.G.T College, BallariManish HarlalkaNo ratings yet

- Tax Brief - June 2012Document8 pagesTax Brief - June 2012Rheneir MoraNo ratings yet

- Untitled DocumentDocument3 pagesUntitled DocumentbshivamofficialNo ratings yet

- Debit Note & Credit NoteDocument9 pagesDebit Note & Credit NoteconciliataxesNo ratings yet

- Tax On Compensation - AGP 7.10.14Document3 pagesTax On Compensation - AGP 7.10.14Bryan Paul InocencioNo ratings yet

- Budget Highlights Athena Law-R1Document4 pagesBudget Highlights Athena Law-R1Ashar AkhtarNo ratings yet

- ST TH THDocument23 pagesST TH THgaganNo ratings yet

- No Tax For Filipinos Earning P21,000 or BelowDocument4 pagesNo Tax For Filipinos Earning P21,000 or BelowLielet MatutinoNo ratings yet

- Decoding Form 10 B & 10 BBDocument10 pagesDecoding Form 10 B & 10 BBCA Amresh VashishtNo ratings yet

- (OPINION) Train Law: What Does It Change?: Tax Reform For Acceleration and Inclusion (Train) LawDocument10 pages(OPINION) Train Law: What Does It Change?: Tax Reform For Acceleration and Inclusion (Train) Lawksulaw2018No ratings yet

- April 2010 Tax BriefDocument10 pagesApril 2010 Tax BriefAna MergalNo ratings yet

- Train LawDocument17 pagesTrain LawMaria Sophia Isabel Grajo RosalesNo ratings yet

- Train Law: Rodrigo DuterteDocument5 pagesTrain Law: Rodrigo DuterteSheila Mae AramanNo ratings yet

- Proposed Tax Changes Under The Finance Bill 2023 Snapshot - ALN Kenya Legal AlertDocument20 pagesProposed Tax Changes Under The Finance Bill 2023 Snapshot - ALN Kenya Legal AlertKafonyi JohnNo ratings yet

- Value Added Tax & CustomsDocument17 pagesValue Added Tax & CustomsnibirNo ratings yet

- ELP Tax Alert - Clarification On Services by Government or Local AuthorityDocument4 pagesELP Tax Alert - Clarification On Services by Government or Local AuthorityNITINNo ratings yet

- Transfer Tax Train Law 2Document6 pagesTransfer Tax Train Law 2Mark DasiganNo ratings yet

- Charities CBRDocument24 pagesCharities CBRfecto9920No ratings yet

- Unit:4 GST: By: Simran Jain Assistant Professor GibsDocument46 pagesUnit:4 GST: By: Simran Jain Assistant Professor GibsTushar SrivastavaNo ratings yet

- Recent Changes in ST Law 2013 14Document14 pagesRecent Changes in ST Law 2013 14vb_krishnaNo ratings yet

- 1040 Exam Prep Module XI: Circular 230 and AMTFrom Everand1040 Exam Prep Module XI: Circular 230 and AMTRating: 1 out of 5 stars1/5 (1)

- Basics About Sales, Use, and Other Transactional Taxes: Overview of Transactional Taxes for Consideration When Striving Toward the Maximization of Tax Compliance and Minimization of Tax Costs.From EverandBasics About Sales, Use, and Other Transactional Taxes: Overview of Transactional Taxes for Consideration When Striving Toward the Maximization of Tax Compliance and Minimization of Tax Costs.No ratings yet

- Receipt: No: 10706028/KWT/FIN-GOLD/XII/17Document1 pageReceipt: No: 10706028/KWT/FIN-GOLD/XII/17Daisy Anita SusiloNo ratings yet

- Per Dir Pajak 32 2012Document17 pagesPer Dir Pajak 32 2012Daisy Anita SusiloNo ratings yet

- Nio Daisy Anita: Surabaya - T2 (SUB)Document2 pagesNio Daisy Anita: Surabaya - T2 (SUB)Daisy Anita SusiloNo ratings yet

- Newsletter Maret I - EnglishDocument6 pagesNewsletter Maret I - EnglishDaisy Anita SusiloNo ratings yet

- Business English: No. Title PublisherDocument4 pagesBusiness English: No. Title PublisherDaisy Anita SusiloNo ratings yet

- Taxflash: Tax Indonesia / July 2017 / No.09Document3 pagesTaxflash: Tax Indonesia / July 2017 / No.09Daisy Anita SusiloNo ratings yet

- Ketentuan Angsuran PPH Pasal 25 Untuk WP Kriteria Tertentu - EnglishDocument2 pagesKetentuan Angsuran PPH Pasal 25 Untuk WP Kriteria Tertentu - EnglishDaisy Anita SusiloNo ratings yet

- Nio Daisy Anita: Jakarta (CGK)Document2 pagesNio Daisy Anita: Jakarta (CGK)Daisy Anita SusiloNo ratings yet

- Ketentuan Terbaru Atas Pemotongan PPH BungaDocument2 pagesKetentuan Terbaru Atas Pemotongan PPH BungaDaisy Anita SusiloNo ratings yet

- Indonesia Taxation Quarterly Report 2019 - I: ForewordDocument47 pagesIndonesia Taxation Quarterly Report 2019 - I: ForewordDaisy Anita SusiloNo ratings yet

- Ketentuan Terbaru PBB-P2 JakartaDocument2 pagesKetentuan Terbaru PBB-P2 JakartaDaisy Anita SusiloNo ratings yet

- Receipt PDFDocument1 pageReceipt PDFDaisy Anita SusiloNo ratings yet

- Klaim Asuransi JiwaDocument2 pagesKlaim Asuransi JiwaDaisy Anita SusiloNo ratings yet

- Government Regulates Tax Incentives To Boost Ease of ExportDocument2 pagesGovernment Regulates Tax Incentives To Boost Ease of ExportDaisy Anita SusiloNo ratings yet

- Diymarketingpresentation 190302212312 PDFDocument19 pagesDiymarketingpresentation 190302212312 PDFDaisy Anita SusiloNo ratings yet

- Newsletter - Content - Feb 2019 EnglishDocument7 pagesNewsletter - Content - Feb 2019 EnglishDaisy Anita SusiloNo ratings yet

- Katun TaiwanDocument5 pagesKatun TaiwanDaisy Anita SusiloNo ratings yet

- Tax - Newsletter R&D 10 2019Document6 pagesTax - Newsletter R&D 10 2019Daisy Anita SusiloNo ratings yet

- Newsletter - Okt I - Part 3Document6 pagesNewsletter - Okt I - Part 3Daisy Anita SusiloNo ratings yet

- Compile Newsletter April I 2019 ENGLISH Edit PagiDocument7 pagesCompile Newsletter April I 2019 ENGLISH Edit PagiDaisy Anita SusiloNo ratings yet

- Newsletter - Okt I - Part 4Document3 pagesNewsletter - Okt I - Part 4Daisy Anita SusiloNo ratings yet

- Newsletter - Agustus I - Part IIIDocument11 pagesNewsletter - Agustus I - Part IIIDaisy Anita SusiloNo ratings yet

- Safeguard Import Duty On Fructose Syrup Products: Mof Reg. 126/2020Document3 pagesSafeguard Import Duty On Fructose Syrup Products: Mof Reg. 126/2020Daisy Anita SusiloNo ratings yet

- Kedudukan: DJP Selayang PandangDocument2 pagesKedudukan: DJP Selayang PandangDaisy Anita SusiloNo ratings yet

- Beleid Pajak Untuk ECommerce BatalDocument1 pageBeleid Pajak Untuk ECommerce BatalDaisy Anita SusiloNo ratings yet

- PerkenalanDocument1 pagePerkenalanDaisy Anita SusiloNo ratings yet

- Writing Poin 6Document1 pageWriting Poin 6Daisy Anita SusiloNo ratings yet

- Nara - English Course Homework - Circular LetterDocument1 pageNara - English Course Homework - Circular LetterDaisy Anita SusiloNo ratings yet

- CH 4 4-35 SpreadsheetDocument34 pagesCH 4 4-35 Spreadsheetcherishwisdom_997598No ratings yet

- GR 9 Teachers GuideDocument107 pagesGR 9 Teachers GuideAmogelang Katlego MakhalemeleNo ratings yet

- More Solved Examples PDFDocument16 pagesMore Solved Examples PDFrobbsNo ratings yet

- Transport Company Invoice FormatDocument1 pageTransport Company Invoice FormatLokesh RavNo ratings yet

- Quiz 1 20.06.17 Q& ADocument11 pagesQuiz 1 20.06.17 Q& ADeependra NigamNo ratings yet

- SNGPL BIll CalculationDocument1 pageSNGPL BIll CalculationRana Tahir NaveedNo ratings yet

- Answer: D: Statement 2: The Share of A Co-Venturer Corporation in The Net Income of Tax Exempt Joint Venture orDocument3 pagesAnswer: D: Statement 2: The Share of A Co-Venturer Corporation in The Net Income of Tax Exempt Joint Venture orRosemarie CruzNo ratings yet

- ColumbiaDocument2 pagesColumbiaEllie McIntireNo ratings yet

- Oblicon Cases COMPLETEDocument10 pagesOblicon Cases COMPLETEEarl Justine OcuamanNo ratings yet

- Bank of IndiaDocument49 pagesBank of IndiaJasmeet Singh50% (2)

- RCBC V AlfaDocument1 pageRCBC V AlfaJhoel VillafuerteNo ratings yet

- Acharya Shri SudarshanDocument1 pageAcharya Shri SudarshanAditya SinghNo ratings yet

- 10ME71 NotesDocument64 pages10ME71 NotesHarsha VardhanNo ratings yet

- Gaurab CH Shaw ITR3-Ack 2022 - 521946781220922Document1 pageGaurab CH Shaw ITR3-Ack 2022 - 521946781220922Sagar PradhanNo ratings yet

- AIS Chapter 1 Lecture NotesDocument28 pagesAIS Chapter 1 Lecture NotesNhi Ho50% (4)

- Presentation of Banking and Working Capital: Presented By: Ashish Bansal Ashish Kumar Chinky Mittal Vasam BansalDocument24 pagesPresentation of Banking and Working Capital: Presented By: Ashish Bansal Ashish Kumar Chinky Mittal Vasam BansalprernaNo ratings yet

- Chapter Sixteen: Managing Bond PortfoliosDocument16 pagesChapter Sixteen: Managing Bond PortfoliosOona NiallNo ratings yet

- Quiz in Financial Statements Preparation: Adjusted Trial Balance Debit CreditDocument2 pagesQuiz in Financial Statements Preparation: Adjusted Trial Balance Debit CreditEzra Mikah G. CaalimNo ratings yet

- Fadi Ismail CV-4Document2 pagesFadi Ismail CV-4CatyNo ratings yet

- Accounting Concepts & ConventionsDocument2 pagesAccounting Concepts & ConventionsKartik KNo ratings yet

- PCI-Leasing-vs-Trojan-Metal-Industries-digestDocument1 pagePCI-Leasing-vs-Trojan-Metal-Industries-digestKrister VallenteNo ratings yet

- 2021 Vietnam Banking Opportunities and ChallengesDocument3 pages2021 Vietnam Banking Opportunities and ChallengesCường MạnhNo ratings yet

- Quiz No. 1 - Corporate LiquidationDocument15 pagesQuiz No. 1 - Corporate LiquidationJam SurdivillaNo ratings yet

- Multiple Choice Quizes Mcgraw HillDocument26 pagesMultiple Choice Quizes Mcgraw HillMorcy JonesNo ratings yet

- Bank of Kigali Limited: Financially Transforming LivesDocument3 pagesBank of Kigali Limited: Financially Transforming LivesBank of KigaliNo ratings yet

- Profit BandsDocument11 pagesProfit Bandszanzdude50% (2)

- Robo-Signed Assignment of Mortgage Prepared by Nationwide Title ClearingDocument1 pageRobo-Signed Assignment of Mortgage Prepared by Nationwide Title Clearinglarry-612445No ratings yet

- Statement: (Including Pots)Document3 pagesStatement: (Including Pots)13KARATNo ratings yet

- SIC 29 - Disclosure - Service Concession ArrangementsDocument6 pagesSIC 29 - Disclosure - Service Concession ArrangementsJimmyChaoNo ratings yet

- Customer Relationship Management (CRM)Document28 pagesCustomer Relationship Management (CRM)Chirag SabhayaNo ratings yet

Download as docx, pdf, or txt

You might also like

- Newsletter - Agustus I - Part IIIDocument11 pagesNewsletter - Agustus I - Part IIIDaisy Anita SusiloNo ratings yet

- Analysis of Finance Bill 2024 13 May 2024 - 002Document67 pagesAnalysis of Finance Bill 2024 13 May 2024 - 002ondalafrederickNo ratings yet

- Required ReadingDocument11 pagesRequired ReadingJennelyn Asas PagaduanNo ratings yet

- GST On TrustDocument4 pagesGST On TruststeveNo ratings yet

- Assessment of Charitable Trust and InstitutionDocument52 pagesAssessment of Charitable Trust and InstitutionAnonymous JJhHAdY5HzNo ratings yet

- Tax-Free Exchanges That Are Not Subject To Income Tax, Capital Gains Tax, Documentary Stamp Tax And/or Value-Added Tax, As The Case May BeDocument7 pagesTax-Free Exchanges That Are Not Subject To Income Tax, Capital Gains Tax, Documentary Stamp Tax And/or Value-Added Tax, As The Case May BeJouhara ObeñitaNo ratings yet

- Kenya Proposes Tax Changes Under The Finance Bill - 061808Document25 pagesKenya Proposes Tax Changes Under The Finance Bill - 061808lenarokushulNo ratings yet

- GEC Nov 13Document7 pagesGEC Nov 13koreanissueNo ratings yet

- Types of Organizations Revised Corporation CodeDocument11 pagesTypes of Organizations Revised Corporation CodeNadie LrdNo ratings yet

- DT InterviewDocument37 pagesDT Interviewanjali aggarwalNo ratings yet

- Rationale For The Imposition of TaxesDocument5 pagesRationale For The Imposition of TaxesBurnok SupolNo ratings yet

- The TRAIN Law and The Poor Antonio P. Contreras: BY ON JANUARY 30, 201Document7 pagesThe TRAIN Law and The Poor Antonio P. Contreras: BY ON JANUARY 30, 201Jellah Lorezo AbreganaNo ratings yet

- Modelo de Informe en Inglés TRIBUTACIONDocument8 pagesModelo de Informe en Inglés TRIBUTACIONPatrick ArteagaNo ratings yet

- Uae Corporate Tax Law SummaryDocument37 pagesUae Corporate Tax Law SummarypankajNo ratings yet

- Union Budget 2023 For NGOsDocument7 pagesUnion Budget 2023 For NGOsGOODS AND SERVICES TAXNo ratings yet

- Ovw1 1 - ST Ataglance 19may16Document4 pagesOvw1 1 - ST Ataglance 19may16Sanjog DewanNo ratings yet

- Tax Alert (April 2020) FinalDocument30 pagesTax Alert (April 2020) FinalRheneir MoraNo ratings yet

- Public Accounts 2013-14 SaskatchewanDocument270 pagesPublic Accounts 2013-14 SaskatchewanAnishinabeNo ratings yet

- Rmo 20-2013Document7 pagesRmo 20-2013Carlos105No ratings yet

- Chapter 2. EditedDocument9 pagesChapter 2. EditedJellah Lorezo AbreganaNo ratings yet

- Alana - Self-Assessment Module 2Document3 pagesAlana - Self-Assessment Module 2kate trishaNo ratings yet

- GST BILL Highlights of Draft Model GST LawDocument6 pagesGST BILL Highlights of Draft Model GST LawS Sinha RayNo ratings yet

- Taxable Event Under GSTDocument4 pagesTaxable Event Under GSTSuman SharmaNo ratings yet

- BIR 10-2003 Implementing The Tax Incentives Provisions RA 8525 Adopt-A-School Act of 1998Document5 pagesBIR 10-2003 Implementing The Tax Incentives Provisions RA 8525 Adopt-A-School Act of 1998LakanPH100% (1)

- Courage vs. CIRDocument2 pagesCourage vs. CIRMike E Dm33% (3)

- Tax AssessmentsDocument3 pagesTax AssessmentsKing AlduezaNo ratings yet

- Courage Vs CIRDocument8 pagesCourage Vs CIRAna GNo ratings yet

- Law of TaxationDocument3 pagesLaw of TaxationmangalagowrirudrappaNo ratings yet

- An Economic Impact Analysis On Tax Reform For Acceleration and Inclusion or Train BillDocument6 pagesAn Economic Impact Analysis On Tax Reform For Acceleration and Inclusion or Train BillZarina BartolayNo ratings yet

- Negative List of ServicesDocument104 pagesNegative List of ServicesGautam SinghNo ratings yet

- PFA Final Exam October 2022Document4 pagesPFA Final Exam October 2022Jay PugonNo ratings yet

- 2013 Tax-Exemption Guidelines For Non-Stock, Nonprofit Corporations FDM 8.1.13Document2 pages2013 Tax-Exemption Guidelines For Non-Stock, Nonprofit Corporations FDM 8.1.13cyrilNo ratings yet

- Train Law: What Does It Change?: Tax Reform For Acceleration and Inclusion (Train) LawDocument8 pagesTrain Law: What Does It Change?: Tax Reform For Acceleration and Inclusion (Train) LawJoan PaynorNo ratings yet

- TRAIN Law Implementing Rules and Regulations - Facing PH TaxesDocument10 pagesTRAIN Law Implementing Rules and Regulations - Facing PH Taxesreneth davidNo ratings yet

- Tax Guide On The Deduction of Medical, Physical Impairment and Disability Expenses (Issue 3)Document28 pagesTax Guide On The Deduction of Medical, Physical Impairment and Disability Expenses (Issue 3)iadhiaNo ratings yet

- Taxpayers Remedies For FDDADocument2 pagesTaxpayers Remedies For FDDAalmira halasanNo ratings yet

- Train Law-Wps OfficeDocument4 pagesTrain Law-Wps OfficeAdam Ross Toledo BrionesNo ratings yet

- S.G.T College, BallariDocument5 pagesS.G.T College, BallariManish HarlalkaNo ratings yet

- Tax Brief - June 2012Document8 pagesTax Brief - June 2012Rheneir MoraNo ratings yet

- Untitled DocumentDocument3 pagesUntitled DocumentbshivamofficialNo ratings yet

- Debit Note & Credit NoteDocument9 pagesDebit Note & Credit NoteconciliataxesNo ratings yet

- Tax On Compensation - AGP 7.10.14Document3 pagesTax On Compensation - AGP 7.10.14Bryan Paul InocencioNo ratings yet

- Budget Highlights Athena Law-R1Document4 pagesBudget Highlights Athena Law-R1Ashar AkhtarNo ratings yet

- ST TH THDocument23 pagesST TH THgaganNo ratings yet

- No Tax For Filipinos Earning P21,000 or BelowDocument4 pagesNo Tax For Filipinos Earning P21,000 or BelowLielet MatutinoNo ratings yet

- Decoding Form 10 B & 10 BBDocument10 pagesDecoding Form 10 B & 10 BBCA Amresh VashishtNo ratings yet

- (OPINION) Train Law: What Does It Change?: Tax Reform For Acceleration and Inclusion (Train) LawDocument10 pages(OPINION) Train Law: What Does It Change?: Tax Reform For Acceleration and Inclusion (Train) Lawksulaw2018No ratings yet

- April 2010 Tax BriefDocument10 pagesApril 2010 Tax BriefAna MergalNo ratings yet

- Train LawDocument17 pagesTrain LawMaria Sophia Isabel Grajo RosalesNo ratings yet

- Train Law: Rodrigo DuterteDocument5 pagesTrain Law: Rodrigo DuterteSheila Mae AramanNo ratings yet

- Proposed Tax Changes Under The Finance Bill 2023 Snapshot - ALN Kenya Legal AlertDocument20 pagesProposed Tax Changes Under The Finance Bill 2023 Snapshot - ALN Kenya Legal AlertKafonyi JohnNo ratings yet

- Value Added Tax & CustomsDocument17 pagesValue Added Tax & CustomsnibirNo ratings yet

- ELP Tax Alert - Clarification On Services by Government or Local AuthorityDocument4 pagesELP Tax Alert - Clarification On Services by Government or Local AuthorityNITINNo ratings yet

- Transfer Tax Train Law 2Document6 pagesTransfer Tax Train Law 2Mark DasiganNo ratings yet

- Charities CBRDocument24 pagesCharities CBRfecto9920No ratings yet

- Unit:4 GST: By: Simran Jain Assistant Professor GibsDocument46 pagesUnit:4 GST: By: Simran Jain Assistant Professor GibsTushar SrivastavaNo ratings yet

- Recent Changes in ST Law 2013 14Document14 pagesRecent Changes in ST Law 2013 14vb_krishnaNo ratings yet

- 1040 Exam Prep Module XI: Circular 230 and AMTFrom Everand1040 Exam Prep Module XI: Circular 230 and AMTRating: 1 out of 5 stars1/5 (1)

- Basics About Sales, Use, and Other Transactional Taxes: Overview of Transactional Taxes for Consideration When Striving Toward the Maximization of Tax Compliance and Minimization of Tax Costs.From EverandBasics About Sales, Use, and Other Transactional Taxes: Overview of Transactional Taxes for Consideration When Striving Toward the Maximization of Tax Compliance and Minimization of Tax Costs.No ratings yet

- Receipt: No: 10706028/KWT/FIN-GOLD/XII/17Document1 pageReceipt: No: 10706028/KWT/FIN-GOLD/XII/17Daisy Anita SusiloNo ratings yet

- Per Dir Pajak 32 2012Document17 pagesPer Dir Pajak 32 2012Daisy Anita SusiloNo ratings yet

- Nio Daisy Anita: Surabaya - T2 (SUB)Document2 pagesNio Daisy Anita: Surabaya - T2 (SUB)Daisy Anita SusiloNo ratings yet

- Newsletter Maret I - EnglishDocument6 pagesNewsletter Maret I - EnglishDaisy Anita SusiloNo ratings yet

- Business English: No. Title PublisherDocument4 pagesBusiness English: No. Title PublisherDaisy Anita SusiloNo ratings yet

- Taxflash: Tax Indonesia / July 2017 / No.09Document3 pagesTaxflash: Tax Indonesia / July 2017 / No.09Daisy Anita SusiloNo ratings yet

- Ketentuan Angsuran PPH Pasal 25 Untuk WP Kriteria Tertentu - EnglishDocument2 pagesKetentuan Angsuran PPH Pasal 25 Untuk WP Kriteria Tertentu - EnglishDaisy Anita SusiloNo ratings yet

- Nio Daisy Anita: Jakarta (CGK)Document2 pagesNio Daisy Anita: Jakarta (CGK)Daisy Anita SusiloNo ratings yet

- Ketentuan Terbaru Atas Pemotongan PPH BungaDocument2 pagesKetentuan Terbaru Atas Pemotongan PPH BungaDaisy Anita SusiloNo ratings yet

- Indonesia Taxation Quarterly Report 2019 - I: ForewordDocument47 pagesIndonesia Taxation Quarterly Report 2019 - I: ForewordDaisy Anita SusiloNo ratings yet

- Ketentuan Terbaru PBB-P2 JakartaDocument2 pagesKetentuan Terbaru PBB-P2 JakartaDaisy Anita SusiloNo ratings yet

- Receipt PDFDocument1 pageReceipt PDFDaisy Anita SusiloNo ratings yet

- Klaim Asuransi JiwaDocument2 pagesKlaim Asuransi JiwaDaisy Anita SusiloNo ratings yet

- Government Regulates Tax Incentives To Boost Ease of ExportDocument2 pagesGovernment Regulates Tax Incentives To Boost Ease of ExportDaisy Anita SusiloNo ratings yet

- Diymarketingpresentation 190302212312 PDFDocument19 pagesDiymarketingpresentation 190302212312 PDFDaisy Anita SusiloNo ratings yet

- Newsletter - Content - Feb 2019 EnglishDocument7 pagesNewsletter - Content - Feb 2019 EnglishDaisy Anita SusiloNo ratings yet

- Katun TaiwanDocument5 pagesKatun TaiwanDaisy Anita SusiloNo ratings yet

- Tax - Newsletter R&D 10 2019Document6 pagesTax - Newsletter R&D 10 2019Daisy Anita SusiloNo ratings yet

- Newsletter - Okt I - Part 3Document6 pagesNewsletter - Okt I - Part 3Daisy Anita SusiloNo ratings yet

- Compile Newsletter April I 2019 ENGLISH Edit PagiDocument7 pagesCompile Newsletter April I 2019 ENGLISH Edit PagiDaisy Anita SusiloNo ratings yet

- Newsletter - Okt I - Part 4Document3 pagesNewsletter - Okt I - Part 4Daisy Anita SusiloNo ratings yet

- Newsletter - Agustus I - Part IIIDocument11 pagesNewsletter - Agustus I - Part IIIDaisy Anita SusiloNo ratings yet

- Safeguard Import Duty On Fructose Syrup Products: Mof Reg. 126/2020Document3 pagesSafeguard Import Duty On Fructose Syrup Products: Mof Reg. 126/2020Daisy Anita SusiloNo ratings yet

- Kedudukan: DJP Selayang PandangDocument2 pagesKedudukan: DJP Selayang PandangDaisy Anita SusiloNo ratings yet

- Beleid Pajak Untuk ECommerce BatalDocument1 pageBeleid Pajak Untuk ECommerce BatalDaisy Anita SusiloNo ratings yet

- PerkenalanDocument1 pagePerkenalanDaisy Anita SusiloNo ratings yet

- Writing Poin 6Document1 pageWriting Poin 6Daisy Anita SusiloNo ratings yet

- Nara - English Course Homework - Circular LetterDocument1 pageNara - English Course Homework - Circular LetterDaisy Anita SusiloNo ratings yet

- CH 4 4-35 SpreadsheetDocument34 pagesCH 4 4-35 Spreadsheetcherishwisdom_997598No ratings yet

- GR 9 Teachers GuideDocument107 pagesGR 9 Teachers GuideAmogelang Katlego MakhalemeleNo ratings yet

- More Solved Examples PDFDocument16 pagesMore Solved Examples PDFrobbsNo ratings yet

- Transport Company Invoice FormatDocument1 pageTransport Company Invoice FormatLokesh RavNo ratings yet

- Quiz 1 20.06.17 Q& ADocument11 pagesQuiz 1 20.06.17 Q& ADeependra NigamNo ratings yet

- SNGPL BIll CalculationDocument1 pageSNGPL BIll CalculationRana Tahir NaveedNo ratings yet

- Answer: D: Statement 2: The Share of A Co-Venturer Corporation in The Net Income of Tax Exempt Joint Venture orDocument3 pagesAnswer: D: Statement 2: The Share of A Co-Venturer Corporation in The Net Income of Tax Exempt Joint Venture orRosemarie CruzNo ratings yet

- ColumbiaDocument2 pagesColumbiaEllie McIntireNo ratings yet

- Oblicon Cases COMPLETEDocument10 pagesOblicon Cases COMPLETEEarl Justine OcuamanNo ratings yet

- Bank of IndiaDocument49 pagesBank of IndiaJasmeet Singh50% (2)

- RCBC V AlfaDocument1 pageRCBC V AlfaJhoel VillafuerteNo ratings yet

- Acharya Shri SudarshanDocument1 pageAcharya Shri SudarshanAditya SinghNo ratings yet

- 10ME71 NotesDocument64 pages10ME71 NotesHarsha VardhanNo ratings yet

- Gaurab CH Shaw ITR3-Ack 2022 - 521946781220922Document1 pageGaurab CH Shaw ITR3-Ack 2022 - 521946781220922Sagar PradhanNo ratings yet

- AIS Chapter 1 Lecture NotesDocument28 pagesAIS Chapter 1 Lecture NotesNhi Ho50% (4)

- Presentation of Banking and Working Capital: Presented By: Ashish Bansal Ashish Kumar Chinky Mittal Vasam BansalDocument24 pagesPresentation of Banking and Working Capital: Presented By: Ashish Bansal Ashish Kumar Chinky Mittal Vasam BansalprernaNo ratings yet

- Chapter Sixteen: Managing Bond PortfoliosDocument16 pagesChapter Sixteen: Managing Bond PortfoliosOona NiallNo ratings yet

- Quiz in Financial Statements Preparation: Adjusted Trial Balance Debit CreditDocument2 pagesQuiz in Financial Statements Preparation: Adjusted Trial Balance Debit CreditEzra Mikah G. CaalimNo ratings yet

- Fadi Ismail CV-4Document2 pagesFadi Ismail CV-4CatyNo ratings yet

- Accounting Concepts & ConventionsDocument2 pagesAccounting Concepts & ConventionsKartik KNo ratings yet

- PCI-Leasing-vs-Trojan-Metal-Industries-digestDocument1 pagePCI-Leasing-vs-Trojan-Metal-Industries-digestKrister VallenteNo ratings yet

- 2021 Vietnam Banking Opportunities and ChallengesDocument3 pages2021 Vietnam Banking Opportunities and ChallengesCường MạnhNo ratings yet

- Quiz No. 1 - Corporate LiquidationDocument15 pagesQuiz No. 1 - Corporate LiquidationJam SurdivillaNo ratings yet

- Multiple Choice Quizes Mcgraw HillDocument26 pagesMultiple Choice Quizes Mcgraw HillMorcy JonesNo ratings yet

- Bank of Kigali Limited: Financially Transforming LivesDocument3 pagesBank of Kigali Limited: Financially Transforming LivesBank of KigaliNo ratings yet

- Profit BandsDocument11 pagesProfit Bandszanzdude50% (2)

- Robo-Signed Assignment of Mortgage Prepared by Nationwide Title ClearingDocument1 pageRobo-Signed Assignment of Mortgage Prepared by Nationwide Title Clearinglarry-612445No ratings yet

- Statement: (Including Pots)Document3 pagesStatement: (Including Pots)13KARATNo ratings yet

- SIC 29 - Disclosure - Service Concession ArrangementsDocument6 pagesSIC 29 - Disclosure - Service Concession ArrangementsJimmyChaoNo ratings yet

- Customer Relationship Management (CRM)Document28 pagesCustomer Relationship Management (CRM)Chirag SabhayaNo ratings yet