Download as xlsx, pdf, or txt

You might also like

- CH - 02 - Cost Terms, Concepts and Classifications With Mixed Cost AnalysisDocument84 pagesCH - 02 - Cost Terms, Concepts and Classifications With Mixed Cost AnalysisankonmahmudNo ratings yet

- China-The Land That Failed To Fail PDFDocument81 pagesChina-The Land That Failed To Fail PDFeric_stNo ratings yet

- Leo BurnettDocument30 pagesLeo BurnettBindi DharodNo ratings yet

- Case Analysis Hony, CIFA and Zoomlion (Creating Value and Strategic Choices in A Dynamic Market)Document5 pagesCase Analysis Hony, CIFA and Zoomlion (Creating Value and Strategic Choices in A Dynamic Market)abhinav100% (1)

- Cost Concept and ClassificationDocument45 pagesCost Concept and ClassificationMountaha0% (1)

- Chapter 2 Cost Accounting ConceptsDocument22 pagesChapter 2 Cost Accounting ConceptsRosliana RazabNo ratings yet

- MANUFACTURING OPERATIONSDocument2 pagesMANUFACTURING OPERATIONStmiss5461No ratings yet

- Chapter 2-Cost ClassificationDocument66 pagesChapter 2-Cost Classification040404.anniNo ratings yet

- 1a Cost Classification Form Manufacturing PT of View and Predicting Cost Behaviour - 19 - 12 - 2023Document12 pages1a Cost Classification Form Manufacturing PT of View and Predicting Cost Behaviour - 19 - 12 - 2023Md Rashadul IslamNo ratings yet

- CH 02Document40 pagesCH 02lyonanh289No ratings yet

- CH 2Document35 pagesCH 2nigoxiy168No ratings yet

- Cost Terminologies and ClassficationsDocument51 pagesCost Terminologies and ClassficationsLim Jie XiNo ratings yet

- Basic Cost Management ConceptsDocument7 pagesBasic Cost Management ConceptsHeizeruNo ratings yet

- Topic 2 IDocument16 pagesTopic 2 Iami zawaniNo ratings yet

- Chapter 1Document4 pagesChapter 1Tricia Rozl PimentelNo ratings yet

- Managerial Accounting and Cost ConceptsDocument6 pagesManagerial Accounting and Cost ConceptsJUST KINGNo ratings yet

- Managerial Accounting and Cost Concepts: Chapter TwoDocument63 pagesManagerial Accounting and Cost Concepts: Chapter TwoMd Hasibul Karim 1811766630No ratings yet

- Chapter 1 IntroductionDocument46 pagesChapter 1 IntroductionIrzam ZairyNo ratings yet

- Cost Term, Concept and ClassificationsDocument28 pagesCost Term, Concept and ClassificationskumarNo ratings yet

- Chapter 02 - Cost Term and Concepts FinalDocument60 pagesChapter 02 - Cost Term and Concepts FinalAminaMatinNo ratings yet

- CH 2-3-B Concepts & Cost BehaviorDocument31 pagesCH 2-3-B Concepts & Cost BehaviorAdi Prawira ArfanNo ratings yet

- Cost Terms, Concepts, and ClassificationsDocument22 pagesCost Terms, Concepts, and ClassificationsKi xxiNo ratings yet

- Week 2-Basic Cost ManagementDocument21 pagesWeek 2-Basic Cost ManagementRichard Oliver CortezNo ratings yet

- Chapter 2Document25 pagesChapter 2JOSEPH LEE ZE LOONG MoeNo ratings yet

- 10632m Lecture 6 - Full Costing I (Full Version)Document53 pages10632m Lecture 6 - Full Costing I (Full Version)kammiefan215No ratings yet

- Presentation 04 (1slide-Pg)Document33 pagesPresentation 04 (1slide-Pg)araika.maksutNo ratings yet

- Chapter 2 UpdatedDocument58 pagesChapter 2 Updatedbing bongNo ratings yet

- SPPTChap 002Document16 pagesSPPTChap 002saharinshakib7505No ratings yet

- Chapter - 2 - Managerial Accounting and Cost ConceptDocument61 pagesChapter - 2 - Managerial Accounting and Cost ConceptSoka PokaNo ratings yet

- 1 Garrison+Chapter2Document61 pages1 Garrison+Chapter2lubna.attariNo ratings yet

- L1-Manufacturer's CostDocument19 pagesL1-Manufacturer's CostomarNo ratings yet

- Cost AccountingDocument39 pagesCost AccountingMian Abdullah MukhdoomNo ratings yet

- Basic Cost ConceptDocument43 pagesBasic Cost ConceptAaron WidofanNo ratings yet

- Chapter 2 Managerial Accounting and Cost ConceptsDocument49 pagesChapter 2 Managerial Accounting and Cost ConceptsFarihaNo ratings yet

- Latest Cost AccountingDocument128 pagesLatest Cost AccountingMian Abdullah MukhdoomNo ratings yet

- Introduction To Managerial Accounting Canadian 5th Edition Brewer Solutions ManualDocument25 pagesIntroduction To Managerial Accounting Canadian 5th Edition Brewer Solutions ManualMaryJohnsonsmni100% (60)

- PDFenDocument68 pagesPDFenby ScribdNo ratings yet

- Lecture 2 - Acc204Document4 pagesLecture 2 - Acc204ALYZA NICOLE CALLEJANo ratings yet

- COST Lesson 2Document4 pagesCOST Lesson 2Christian Clyde Zacal Ching0% (1)

- Cost Concepts Classification BehaviorDocument46 pagesCost Concepts Classification BehaviorrhearomefranciscoNo ratings yet

- Managerial Accounting and Cost ConceptsDocument19 pagesManagerial Accounting and Cost ConceptsFarhan RabbehNo ratings yet

- Managerial Accounting and Cost ConceptsDocument61 pagesManagerial Accounting and Cost ConceptsAmer Wagdy GergesNo ratings yet

- Cost Accounting Concepts: Prof. Dr. Farid MoharamDocument90 pagesCost Accounting Concepts: Prof. Dr. Farid Moharammohamed el kadyNo ratings yet

- Garrison Lecture Chapter 2Document61 pagesGarrison Lecture Chapter 2Ahmad Tawfiq Darabseh100% (2)

- Chapter 2 - Cost Concepts and Design EconomicsDocument21 pagesChapter 2 - Cost Concepts and Design EconomicsChristine ParkNo ratings yet

- Managerial Accounting and Cost ConceptsDocument50 pagesManagerial Accounting and Cost ConceptsGigo Kafare BinoNo ratings yet

- Cost Concepts Chapter 2Document56 pagesCost Concepts Chapter 2cece.11.29.22No ratings yet

- Chapter 2 - Managerial Acc. & Cost ConceptsDocument23 pagesChapter 2 - Managerial Acc. & Cost ConceptsMuhammad Ali KazmiNo ratings yet

- Cost Accounting ReviewerDocument6 pagesCost Accounting ReviewerOlivea Dela TorreNo ratings yet

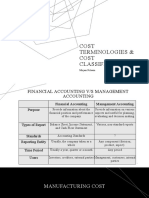

- Cost Terminologies & Cost Classification: Mirjam NilssonDocument13 pagesCost Terminologies & Cost Classification: Mirjam NilssonHitesh JainNo ratings yet

- Managerial Accounting and Cost ConceptsDocument18 pagesManagerial Accounting and Cost ConceptsadamNo ratings yet

- Introduction To Managerial Accounting Canadian 5th Edition Brewer Solutions ManualDocument36 pagesIntroduction To Managerial Accounting Canadian 5th Edition Brewer Solutions Manualfayedavidsonhet0cs100% (24)

- Act 202 Chapter 2Document52 pagesAct 202 Chapter 2Shaon KhanNo ratings yet

- Cost - Pa2 - Ligawad, Melody-Bsa 2CDocument6 pagesCost - Pa2 - Ligawad, Melody-Bsa 2CLIGAWAD, MELODY P.No ratings yet

- 03 - Management AccountingDocument7 pages03 - Management AccountingRigner ArandiaNo ratings yet

- 07 Module 03 AVC PDFDocument12 pages07 Module 03 AVC PDFMarriah Izzabelle Suarez RamadaNo ratings yet

- MA Module 2Document7 pagesMA Module 2BroniNo ratings yet

- Accounting For Decision Making Week 3 Lecture (Seminar 4 - The Nature of Costs)Document51 pagesAccounting For Decision Making Week 3 Lecture (Seminar 4 - The Nature of Costs)nwcbenny337No ratings yet

- Chapter 3 - Virtual - Classroom-M.Document61 pagesChapter 3 - Virtual - Classroom-M.rebeccahf7No ratings yet

- Managerial Accounting and Cost ConceptsDocument18 pagesManagerial Accounting and Cost ConceptsrisaNo ratings yet

- Chapter 2 Reviewer in ManAccDocument2 pagesChapter 2 Reviewer in ManAccChristian AribasNo ratings yet

- Management Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesFrom EverandManagement Accounting Strategy Study Resource for CIMA Students: CIMA Study ResourcesNo ratings yet

- Cost AccountingDocument5 pagesCost Accountingretchiel love calinogNo ratings yet

- Quiz 1 Cost Accounting FDocument5 pagesQuiz 1 Cost Accounting Fretchiel love calinogNo ratings yet

- 5.1 - Gendered Constructions of SexualityDocument45 pages5.1 - Gendered Constructions of Sexualityretchiel love calinogNo ratings yet

- Least Square Regression Method: Cost AccountingDocument11 pagesLeast Square Regression Method: Cost Accountingretchiel love calinogNo ratings yet

- Business Statistics Answers KeyDocument6 pagesBusiness Statistics Answers Keyretchiel love calinog100% (2)

- 6 Psychosocial-DevelopmentDocument30 pages6 Psychosocial-Developmentretchiel love calinogNo ratings yet

- AccountingDocument2 pagesAccountingretchiel love calinogNo ratings yet

- Activity Chapter 1Document5 pagesActivity Chapter 1retchiel love calinogNo ratings yet

- What Do We Mean by Leadership?Document32 pagesWhat Do We Mean by Leadership?retchiel love calinogNo ratings yet

- Inventory Costing and Capacity Analysis: True/FalseDocument56 pagesInventory Costing and Capacity Analysis: True/FalseambiNo ratings yet

- Mark Elliot ZuckerbergDocument11 pagesMark Elliot ZuckerbergPratik MunotNo ratings yet

- Inland Intermodal Terminals and Freight Logistics Hubs PDFDocument29 pagesInland Intermodal Terminals and Freight Logistics Hubs PDFMiloš MilenkovićNo ratings yet

- Objectives: The Objectives of HUDCO IncludeDocument2 pagesObjectives: The Objectives of HUDCO IncludeAditya VermaNo ratings yet

- Sap SD (Sales and Distribution) Online TRAININGDocument20 pagesSap SD (Sales and Distribution) Online TRAININGchandrashekar_ganesanNo ratings yet

- CMJU-Common Fee Structure (W.e.f. 01 March, 2012) : Sl. No. Course University Fee (Per Year)Document3 pagesCMJU-Common Fee Structure (W.e.f. 01 March, 2012) : Sl. No. Course University Fee (Per Year)souvik5000No ratings yet

- Study Material - A. R. Krishnan - 01.3.14Document34 pagesStudy Material - A. R. Krishnan - 01.3.14Aayushi AroraNo ratings yet

- Jaspreet Brar Sop AlgomaDocument4 pagesJaspreet Brar Sop AlgomaJaydeb Das100% (1)

- IBM Analytics - Ladder To AIDocument31 pagesIBM Analytics - Ladder To AIweeliyen5754No ratings yet

- CRM M-16Document1 pageCRM M-16Shrenik Shri Shri MalNo ratings yet

- Case Digest - Week 3 - Mutuum, Cases 1,2,3,4,5,6,7,8,10Document9 pagesCase Digest - Week 3 - Mutuum, Cases 1,2,3,4,5,6,7,8,10Anonymous b4ycWuoIcNo ratings yet

- Pakistan State Oil CompanyDocument43 pagesPakistan State Oil CompanyfarkhundaNo ratings yet

- The Purpose Is Profit Mclaughlin en 26797Document5 pagesThe Purpose Is Profit Mclaughlin en 26797Tej ShahNo ratings yet

- CS Viet NamDocument10 pagesCS Viet NamLập DuyNo ratings yet

- Call Center TerminologiesDocument3 pagesCall Center TerminologiesJoy CelestialNo ratings yet

- Sane Retail Private Limited,: Grand TotalDocument1 pageSane Retail Private Limited,: Grand TotalAnkush ZadeNo ratings yet

- PBIEF (Eng) WebDocument10 pagesPBIEF (Eng) WebFayZ ZabidyNo ratings yet

- Commercial Law NotesDocument81 pagesCommercial Law Notesxh7zf28b2vNo ratings yet

- Accounting (Tally & Peach Tree) : Questions July 2008Document10 pagesAccounting (Tally & Peach Tree) : Questions July 2008bpcbiswanathNo ratings yet

- ECON HelpDocument12 pagesECON HelpYulian IhnatyukNo ratings yet

- Project 4ed - Level 5 - Photocopiable Activities - Unit 5Document8 pagesProject 4ed - Level 5 - Photocopiable Activities - Unit 5Oksana TykhonovaNo ratings yet

- Iso - Iec Fdis 27001 - Redline Iso - Iec Fdis 27001Document2 pagesIso - Iec Fdis 27001 - Redline Iso - Iec Fdis 27001Manish SharmaNo ratings yet

- In The United States Bankruptcy Court Eastern District of Michigan Southern DivisionDocument15 pagesIn The United States Bankruptcy Court Eastern District of Michigan Southern DivisionChapter 11 DocketsNo ratings yet

- BlackstoneDocument2 pagesBlackstoneaidem100% (2)

- IOSA Program ManualDocument148 pagesIOSA Program Manualartamzaimi100% (2)

- 4th FABM 2Document2 pages4th FABM 2Keisha MarieNo ratings yet

- PD 129 SummaryDocument5 pagesPD 129 SummaryFrancis De CastroNo ratings yet