Download as pdf or txt

You might also like

- Dave Banking Account StatementDocument2 pagesDave Banking Account Statementdaniel floydNo ratings yet

- 1.1 Assertions and Audit Objectives For CashDocument10 pages1.1 Assertions and Audit Objectives For Cashhey67% (3)

- Auditing Accounts ReceivableDocument5 pagesAuditing Accounts ReceivableVivien NaigNo ratings yet

- Wally's Billboard & Sign Supply The Audit of Cash: Ateneo de Zamboanga UniversityDocument10 pagesWally's Billboard & Sign Supply The Audit of Cash: Ateneo de Zamboanga UniversityAlrac Garcia0% (1)

- Module 8 LIABILITIESDocument5 pagesModule 8 LIABILITIESNiño Mendoza MabatoNo ratings yet

- Partnership Liquidation: Debit CreditDocument7 pagesPartnership Liquidation: Debit CreditWenjun0% (1)

- Bfs Foreclosed Properties Listing As of 2017-04-12 PublicDocument14 pagesBfs Foreclosed Properties Listing As of 2017-04-12 PublicCianPanganibanNo ratings yet

- Audit Cash: Audit Assertions For Cash Existence Completeness Rights and Obligations Valuation or AllocationDocument4 pagesAudit Cash: Audit Assertions For Cash Existence Completeness Rights and Obligations Valuation or AllocationMacmilan Trevor JamuNo ratings yet

- Audit Accounts PayableDocument7 pagesAudit Accounts PayableMacmilan Trevor Jamu0% (1)

- Module 3 - Audit of CashDocument23 pagesModule 3 - Audit of CashIvan Landaos100% (2)

- Audit of Cash 1Document14 pagesAudit of Cash 1Fritz IgnacioNo ratings yet

- ARIBA, Fretzyl Bless A. - Chapter 7 - Substantive Test of Cash - ReflectionDocument4 pagesARIBA, Fretzyl Bless A. - Chapter 7 - Substantive Test of Cash - ReflectionFretzyl JulyNo ratings yet

- Point Audit Week 12Document10 pagesPoint Audit Week 12tolha ramadhaniNo ratings yet

- Chapter 7. Audit of Cash BalanceDocument12 pagesChapter 7. Audit of Cash BalanceGena AlisuuNo ratings yet

- Chapter 18-Auditing Investments and Cash BalancesDocument6 pagesChapter 18-Auditing Investments and Cash BalancesTsunaNo ratings yet

- How To Audit ARDocument4 pagesHow To Audit ARStefanie Jane Royo PabalinasNo ratings yet

- Audit of CashDocument23 pagesAudit of CashmeseleNo ratings yet

- CH16 Ni Nyoman SrinadiDocument19 pagesCH16 Ni Nyoman SrinadiNehemia LuartowoNo ratings yet

- Audit Objectives and Procedures: HapterDocument121 pagesAudit Objectives and Procedures: HapterabdellaNo ratings yet

- Review Questions and Problems Chapter 7Document5 pagesReview Questions and Problems Chapter 7Chelle HullezaNo ratings yet

- Audit Procedures For Cash and Cash Equivalents - WIKIACCOUNTINGDocument13 pagesAudit Procedures For Cash and Cash Equivalents - WIKIACCOUNTINGsninaricaNo ratings yet

- Designing Test of Details of BalancesDocument5 pagesDesigning Test of Details of BalancesPaulina InggitaNo ratings yet

- Chapter 7Document22 pagesChapter 7Genanew AbebeNo ratings yet

- Chapter-2: Audit of Cash and Marketable SecuritiesDocument27 pagesChapter-2: Audit of Cash and Marketable Securitiesbikilahussen100% (1)

- AUD Module 3 - Audit of CashDocument25 pagesAUD Module 3 - Audit of CashChristine CariñoNo ratings yet

- 2024 - For Merge1Document17 pages2024 - For Merge1tigistdesalegn2021No ratings yet

- Limitations To Financial Statement AnalysisDocument4 pagesLimitations To Financial Statement Analysissangya01No ratings yet

- C. Cash Including Bank BalancesDocument17 pagesC. Cash Including Bank BalancesadelmariaracelleNo ratings yet

- Weeks 5 Topic 5Document13 pagesWeeks 5 Topic 5Shalin LataNo ratings yet

- How To AuditDocument34 pagesHow To AuditMaria ZarinaNo ratings yet

- Substantive Tests123Document3 pagesSubstantive Tests123Ryan TamondongNo ratings yet

- C. Cash PSPDocument23 pagesC. Cash PSPamgvicente29No ratings yet

- Audit PracticeDocument161 pagesAudit PracticeKez Max100% (1)

- AP 07 Substantive Audit Tests of LiabilitiesDocument3 pagesAP 07 Substantive Audit Tests of LiabilitiesJobby Jaranilla100% (1)

- Audit of Cash and Financial InstrumentsDocument4 pagesAudit of Cash and Financial Instrumentsmrs leeNo ratings yet

- Zelalem G Audit II CHAP. SIX AUDIT CLDocument7 pagesZelalem G Audit II CHAP. SIX AUDIT CLalemayehuNo ratings yet

- Chapter 6Document14 pagesChapter 6Genanew AbebeNo ratings yet

- Project IN AuditingDocument9 pagesProject IN AuditingToniNo ratings yet

- Audit of Current AssetsDocument3 pagesAudit of Current AssetsNEstandaNo ratings yet

- Chapter 2Document8 pagesChapter 2Karin NafilaNo ratings yet

- Transaction Cycle and Substantive TestingDocument5 pagesTransaction Cycle and Substantive TestingZaira PangesfanNo ratings yet

- SIM ACP 323 Week 4 5Document32 pagesSIM ACP 323 Week 4 5Helga MatiasNo ratings yet

- AC414 - Audit and Investigations II - Audit of RecievablesDocument14 pagesAC414 - Audit and Investigations II - Audit of RecievablesTsitsi AbigailNo ratings yet

- ARIBA, Fretzyl Bless A. - Chapter 9 - Substantive Test of Receivables and Sales - ReflectionDocument3 pagesARIBA, Fretzyl Bless A. - Chapter 9 - Substantive Test of Receivables and Sales - ReflectionFretzyl JulyNo ratings yet

- Chapter FiveDocument14 pagesChapter Fivemubarek oumerNo ratings yet

- Chapter 5 - Solution ManualDocument25 pagesChapter 5 - Solution ManualKim Ngân100% (4)

- Chapter 14 - Accounts Payables and Other LiabilitisDocument28 pagesChapter 14 - Accounts Payables and Other LiabilitisHamda AbdinasirNo ratings yet

- Auditing and Accounting Auditing Cash & Bank Balances: ObjectiveDocument3 pagesAuditing and Accounting Auditing Cash & Bank Balances: ObjectiveMohit SainiNo ratings yet

- SIM Audit 421 Problem Week 4-5Document33 pagesSIM Audit 421 Problem Week 4-5Kristelle MarieNo ratings yet

- Unit-2 Audit of Cash and Marketable SecuritiesDocument6 pagesUnit-2 Audit of Cash and Marketable SecuritiesKiya AbdiNo ratings yet

- Audit Evidence SummaryDocument14 pagesAudit Evidence SummaryEunice GloriaNo ratings yet

- Accounts Receivable AuditingDocument2 pagesAccounts Receivable AuditingJohnNo ratings yet

- Vouching DefinitionDocument8 pagesVouching DefinitionMariam AfzalNo ratings yet

- How To Conduct A Financial AuditDocument4 pagesHow To Conduct A Financial AuditSherleen GallardoNo ratings yet

- Audit ReportDocument10 pagesAudit Report03fl22bcl033No ratings yet

- Audit II CH 06 AuditDocument4 pagesAudit II CH 06 AuditmissaassefaNo ratings yet

- Reading Report: 1. Prepare A Summary For Each Business Process, NamelyDocument2 pagesReading Report: 1. Prepare A Summary For Each Business Process, NamelyAnita Noah MeloNo ratings yet

- AC414 - Audit and Investigations II - Audit of Cash and Bank BalanceDocument20 pagesAC414 - Audit and Investigations II - Audit of Cash and Bank BalanceTsitsi AbigailNo ratings yet

- Louw 7Document26 pagesLouw 7drobinspaperNo ratings yet

- Reading Report: 1. Prepare A Summary For Each Business Process, NamelyDocument2 pagesReading Report: 1. Prepare A Summary For Each Business Process, NamelyAnita Noah MeloNo ratings yet

- Erros Noah PDFDocument2 pagesErros Noah PDFAnita Noah MeloNo ratings yet

- Textbook of Urgent Care Management: Chapter 13, Financial ManagementFrom EverandTextbook of Urgent Care Management: Chapter 13, Financial ManagementNo ratings yet

- Dollars and Sense: Demystifying Financial Records for Business OwnersFrom EverandDollars and Sense: Demystifying Financial Records for Business OwnersNo ratings yet

- Preparing A Bank Reconciliation - Financial AccountingDocument14 pagesPreparing A Bank Reconciliation - Financial AccountingsninaricaNo ratings yet

- Estate Tax AmnestyDocument10 pagesEstate Tax AmnestysninaricaNo ratings yet

- Philippine Accounting Standards - BusinessMirrorDocument2 pagesPhilippine Accounting Standards - BusinessMirrorsninaricaNo ratings yet

- Then Commit) AndkdksjsjsjsjdDocument4 pagesThen Commit) AndkdksjsjsjsjdsninaricaNo ratings yet

- Auditing Theory RA 9298 Auditing Theory RA 9298Document10 pagesAuditing Theory RA 9298 Auditing Theory RA 9298sninaricaNo ratings yet

- Advanced Accounting NOV 2012 Question Paper PDFDocument11 pagesAdvanced Accounting NOV 2012 Question Paper PDFsninaricaNo ratings yet

- Nike Announces Layoffs After COVID-19 LossesDocument6 pagesNike Announces Layoffs After COVID-19 LossessninaricaNo ratings yet

- SpookedDocument10 pagesSpookedsninaricaNo ratings yet

- The Restaurateur's Guide To Senior Citizen Benefits - F&B Report MagazineDocument17 pagesThe Restaurateur's Guide To Senior Citizen Benefits - F&B Report MagazinesninaricaNo ratings yet

- Internal Auditing OverviewDocument2 pagesInternal Auditing OverviewsninaricaNo ratings yet

- What Is The Business Transfer Tax For Intangible Assets?Document3 pagesWhat Is The Business Transfer Tax For Intangible Assets?sninaricaNo ratings yet

- Corporate Governance - Overview, Principles, ImportanceDocument5 pagesCorporate Governance - Overview, Principles, ImportancesninaricaNo ratings yet

- Auditing Test BankDocument34 pagesAuditing Test BanksninaricaNo ratings yet

- Philippine CPA Review - Auditing ProblemsDocument2 pagesPhilippine CPA Review - Auditing ProblemssninaricaNo ratings yet

- Module 2. Conceptual Framework of Corporate GovernanceDocument7 pagesModule 2. Conceptual Framework of Corporate GovernancesninaricaNo ratings yet

- Kinds of Donation As To Tax LiabilityDocument6 pagesKinds of Donation As To Tax LiabilitysninaricaNo ratings yet

- San Miguel 2019 FSDocument176 pagesSan Miguel 2019 FSsninaricaNo ratings yet

- Audit Procedures For Cash and Cash Equivalents - WIKIACCOUNTINGDocument13 pagesAudit Procedures For Cash and Cash Equivalents - WIKIACCOUNTINGsninaricaNo ratings yet

- ABC and FifoDocument4 pagesABC and FifosninaricaNo ratings yet

- Fifo Method and Debt Held As MaturityDocument3 pagesFifo Method and Debt Held As MaturitysninaricaNo ratings yet

- Corporate Moral Obligations A Critical ExaminationDocument16 pagesCorporate Moral Obligations A Critical ExaminationsninaricaNo ratings yet

- Income Tax General-PrinciplesDocument10 pagesIncome Tax General-PrinciplessninaricaNo ratings yet

- Tutorial Questions FinDocument16 pagesTutorial Questions FinNhu Nguyen HoangNo ratings yet

- Annual Report For The Year Ended June 2016Document56 pagesAnnual Report For The Year Ended June 2016WELASON CHUNGANo ratings yet

- Buttons: AP/10/723,724, BUTTONS, ANCHAL Anchal GSTIN:32KDFPS7807P1ZPDocument9 pagesButtons: AP/10/723,724, BUTTONS, ANCHAL Anchal GSTIN:32KDFPS7807P1ZPRahul NathNo ratings yet

- Attempt History: Due Mar 16 at 19:45 Available Mar 16 at 17:45 - Mar 16 at 19:45 1 / 1 PtsDocument5 pagesAttempt History: Due Mar 16 at 19:45 Available Mar 16 at 17:45 - Mar 16 at 19:45 1 / 1 PtsmlaNo ratings yet

- Answer Question 6.6Document3 pagesAnswer Question 6.6Lee Li HengNo ratings yet

- Accounting 50 Imp Questions 1642414963Document75 pagesAccounting 50 Imp Questions 1642414963vishal kadamNo ratings yet

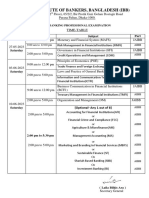

- Exam Routin of 96 Banking Deploma PDFDocument1 pageExam Routin of 96 Banking Deploma PDFMamunur RahmanNo ratings yet

- 1-3B WT Oyo ApDocument3 pages1-3B WT Oyo ApWilliam BrucknerNo ratings yet

- Managerial Accounting Chapter 4Document59 pagesManagerial Accounting Chapter 4jesica.k237No ratings yet

- Merchant BankingDocument17 pagesMerchant BankingRaghavendra.K.A100% (1)

- (Score For Question 1: - of 5 Points) : Math - Graded Assignment - Unit Test, Part 2 - IncomeDocument2 pages(Score For Question 1: - of 5 Points) : Math - Graded Assignment - Unit Test, Part 2 - IncomeGracie CroneNo ratings yet

- Official Payments - Pay Taxes, Utility Bills, Tuition & More OnlineDocument1 pageOfficial Payments - Pay Taxes, Utility Bills, Tuition & More OnlineGuadalupe MarquezNo ratings yet

- Time Value of MoneyDocument2 pagesTime Value of Moneyangelavani_16No ratings yet

- Admission Capital AdjustmentsDocument6 pagesAdmission Capital AdjustmentsHamza MudassirNo ratings yet

- SMDM Project Business Report - Ketan Sawalkar: (Document Title)Document17 pagesSMDM Project Business Report - Ketan Sawalkar: (Document Title)Ketan Sawalkar100% (2)

- Covering LetterDocument2 pagesCovering LetterAishwary SinhaNo ratings yet

- BBA AccountingDocument71 pagesBBA Accountingkhansha ComputersNo ratings yet

- Assignment QuestionDocument3 pagesAssignment QuestionMohd Tajudin DiniNo ratings yet

- Joann Honkala - Job 36 - Policy 3Document1 pageJoann Honkala - Job 36 - Policy 3api-533261909No ratings yet

- Loan Shark CalculatorDocument18 pagesLoan Shark CalculatorTony MartinNo ratings yet

- National Seminar: On Emerging Dimensions of HRD in IndiaDocument17 pagesNational Seminar: On Emerging Dimensions of HRD in IndiamadhavimbaNo ratings yet

- MODULE 4 WACC Assignment MaterialDocument2 pagesMODULE 4 WACC Assignment MaterialJay LloydNo ratings yet

- Panama Papers - Chetan Kapur and Kabir Kapur 8Document629 pagesPanama Papers - Chetan Kapur and Kabir Kapur 8The Indian ExpressNo ratings yet

- IFRS Edition-2nd: The Accounting Information SystemDocument88 pagesIFRS Edition-2nd: The Accounting Information SystemmariaNo ratings yet

- Final Sip Mba Project PDFDocument87 pagesFinal Sip Mba Project PDFDisha JAINNo ratings yet

- PW84PRP4819931 SoaDocument5 pagesPW84PRP4819931 Soasadhamba3No ratings yet

- Tabulasi Data Kelompok 5 - Teori Akutansi 6BDocument4 pagesTabulasi Data Kelompok 5 - Teori Akutansi 6BDavid HernandezNo ratings yet