Download as pdf or txt

You might also like

- Tax Workbook 2022 - NodrmDocument399 pagesTax Workbook 2022 - NodrmNosipho Nyathi100% (4)

- Afar 2 Module CH 7Document12 pagesAfar 2 Module CH 7KezNo ratings yet

- Construction ContractDocument19 pagesConstruction ContractThumb-up Premasthira100% (1)

- Field Guide for Construction Management: Management by Walking AroundFrom EverandField Guide for Construction Management: Management by Walking AroundRating: 4.5 out of 5 stars4.5/5 (4)

- Contract AccountDocument10 pagesContract AccountAhmad MustaqeemNo ratings yet

- 5 Long-Term Construction ContractDocument12 pages5 Long-Term Construction ContractMark TaysonNo ratings yet

- Week 10 Revenue Recognition-Long-term Construction Contract - ACTG341 Advanced Financial Accounting and Reporting 1Document12 pagesWeek 10 Revenue Recognition-Long-term Construction Contract - ACTG341 Advanced Financial Accounting and Reporting 1Marilou Arcillas PanisalesNo ratings yet

- MODULE 8 (Part 1)Document6 pagesMODULE 8 (Part 1)trixie maeNo ratings yet

- Study Material On CMADocument9 pagesStudy Material On CMAjinendra8421001702No ratings yet

- Construction Project Site Supervision and Contract AdministrationDocument35 pagesConstruction Project Site Supervision and Contract AdministrationMark Emman CaseresNo ratings yet

- Construction Contracts: Learning OutcomesDocument29 pagesConstruction Contracts: Learning Outcomessadaf_gul_7100% (1)

- CONTRACT COSTING With IllustrationDocument10 pagesCONTRACT COSTING With IllustrationFikri SaiffullahNo ratings yet

- 5 Long Term Construction Contract 3e5ca4a29cf252303 Ffcc2ab83e9ecba CompressDocument12 pages5 Long Term Construction Contract 3e5ca4a29cf252303 Ffcc2ab83e9ecba Compressgelly studiesNo ratings yet

- Notes Chapter-4 Contract CostingDocument6 pagesNotes Chapter-4 Contract Costingshkabadi2005No ratings yet

- Week 7: Conventional Contractual Arrangement I (7.0) : 7.1 Traditional Types of ContractDocument5 pagesWeek 7: Conventional Contractual Arrangement I (7.0) : 7.1 Traditional Types of ContractAmulie JarjuseyNo ratings yet

- Lo2 - Construction ContractsDocument19 pagesLo2 - Construction ContractsFazlin ZaibNo ratings yet

- +construction Contracts PDFDocument11 pages+construction Contracts PDFSheila DomalantaNo ratings yet

- Contracts CostingDocument13 pagesContracts CostingAman DhingraNo ratings yet

- Contract Costing: Concept Explanation DocumentDocument12 pagesContract Costing: Concept Explanation DocumentNikhil KasatNo ratings yet

- Cost Acc Tute AssignmentDocument3 pagesCost Acc Tute AssignmentAdesh MeshramNo ratings yet

- Module No. 2 Construction ContractsDocument18 pagesModule No. 2 Construction ContractsPrincess SagreNo ratings yet

- CONTRACTSDocument32 pagesCONTRACTSRajaSekhararayudu SanaNo ratings yet

- CPM Lecture 3 Contracts and Contract AdministratioDocument11 pagesCPM Lecture 3 Contracts and Contract AdministratioBusico Aivan Kent NatsuNo ratings yet

- What Is Cost Plus PricingDocument9 pagesWhat Is Cost Plus PricingMahider getachewNo ratings yet

- Fa - Topic 3 Contract AccountDocument9 pagesFa - Topic 3 Contract AccountERICK ABDINo ratings yet

- RR Construction Accounting QuestionsDocument18 pagesRR Construction Accounting QuestionsSharmaineMirandaNo ratings yet

- CCEC Lec02 Contracts CH 2Document27 pagesCCEC Lec02 Contracts CH 2Mustafa ZahidNo ratings yet

- Professional Practice: Contract and Types of TaxesDocument7 pagesProfessional Practice: Contract and Types of Taxessanchit guptaNo ratings yet

- 1 - CMPM, Contracts & Specifications (Edmodo)Document15 pages1 - CMPM, Contracts & Specifications (Edmodo)jhuascute06100% (1)

- Notes LTCCDocument2 pagesNotes LTCCMila Casandra CastañedaNo ratings yet

- UE-353 - Lecture # 8Document11 pagesUE-353 - Lecture # 8YUSRA SHUAIBNo ratings yet

- Contract Costing of Indian Security Force at BangaloreDocument17 pagesContract Costing of Indian Security Force at BangaloreShravani ShravNo ratings yet

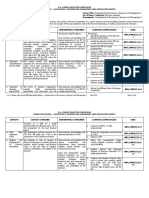

- Projects Analysis and Implementation Assignment-Ii: Group No: 4Document13 pagesProjects Analysis and Implementation Assignment-Ii: Group No: 4Bindu_Shree_4565No ratings yet

- Engineering ContractsDocument12 pagesEngineering ContractshimNo ratings yet

- Construction Contracts - Ias 11Document3 pagesConstruction Contracts - Ias 11Shariful HoqueNo ratings yet

- Chapter 3 Pfrs 15 Construction ContractDocument11 pagesChapter 3 Pfrs 15 Construction Contractshylabaguio15No ratings yet

- Chapter 4 Revenue Recognition 2Document52 pagesChapter 4 Revenue Recognition 2Brennan DayacapNo ratings yet

- AFAR-05: PFRS 15 - Revenue From Contracts With Customers: Construction AccountingDocument10 pagesAFAR-05: PFRS 15 - Revenue From Contracts With Customers: Construction AccountingManuNo ratings yet

- Chapter TwoDocument6 pagesChapter TwoBoshoo Archi100% (1)

- Accounting Standard-7: Construction ContractsDocument23 pagesAccounting Standard-7: Construction Contractsarun666100% (3)

- Module 8 Financial ConsiderationsDocument11 pagesModule 8 Financial ConsiderationsErlinda Olegario Marasigan0% (1)

- 1.Works-Conract Types FrameworkContractDocument52 pages1.Works-Conract Types FrameworkContractSuraj Gurung100% (1)

- AFAR 04 Construction AccountingDocument13 pagesAFAR 04 Construction Accountingmysweet surrenderNo ratings yet

- ContrsctDocument23 pagesContrsctMohammed Naeem Mohammed NaeemNo ratings yet

- Question BankDocument64 pagesQuestion BankshouryanNo ratings yet

- Accounting StandardDocument8 pagesAccounting StandardOnkar Ashok KeljiNo ratings yet

- Cotract Costing Project TopicDocument17 pagesCotract Costing Project TopicShravani Shrav100% (1)

- Types of ContractsDocument33 pagesTypes of ContractsIgombe IsaacNo ratings yet

- AFAR-04 (Construction Accounting)Document16 pagesAFAR-04 (Construction Accounting)Nathalie Shien DagaragaNo ratings yet

- Contract ContractDocument8 pagesContract ContractSherali silarNo ratings yet

- ContractDocument4 pagesContractsanjeev2812No ratings yet

- Types of ContratsDocument3 pagesTypes of ContratsSwapnil BorateNo ratings yet

- 01 Module I NotesDocument7 pages01 Module I NotesHeri TrionoNo ratings yet

- Contra CT Costing: Chap Ter OutlineDocument52 pagesContra CT Costing: Chap Ter OutlineGARUIS MELINo ratings yet

- Contract Accounting PDFDocument29 pagesContract Accounting PDFrachel100% (1)

- Types of Construction ContractsDocument7 pagesTypes of Construction ContractsJaymar Palomares OrilloNo ratings yet

- Construcion ContractDocument43 pagesConstrucion Contractvaskarmitra20No ratings yet

- Assignment 1558529720 SmsDocument43 pagesAssignment 1558529720 SmsSmit JariwalaNo ratings yet

- Chapter 7Document2 pagesChapter 7Maria DyNo ratings yet

- The Contractor Payment Application Audit: Guidance for Auditing AIA Documents G702 & G703From EverandThe Contractor Payment Application Audit: Guidance for Auditing AIA Documents G702 & G703No ratings yet

- Chapter 1: Circles Task 2 Focus OnDocument2 pagesChapter 1: Circles Task 2 Focus OnJona Mae Cuarto AyopNo ratings yet

- PFRS 11 - Joint ArrangementsDocument9 pagesPFRS 11 - Joint ArrangementsJona Mae Cuarto AyopNo ratings yet

- Let's Analyze-Long TermDocument2 pagesLet's Analyze-Long TermJona Mae Cuarto AyopNo ratings yet

- ConsignmentDocument2 pagesConsignmentJona Mae Cuarto AyopNo ratings yet

- Reducing The Equation of The Circle Into Its Standard FormDocument5 pagesReducing The Equation of The Circle Into Its Standard FormJona Mae Cuarto AyopNo ratings yet

- FIRST - ACTIVITY - Structure of Academic TextsDocument3 pagesFIRST - ACTIVITY - Structure of Academic TextsJona Mae Cuarto Ayop0% (1)

- Lesson 2Document6 pagesLesson 2Jona Mae Cuarto AyopNo ratings yet

- Animal Feed MillDocument34 pagesAnimal Feed Millshani2750% (2)

- National TaxesDocument17 pagesNational TaxesAlex OndevillaNo ratings yet

- Proposed Syllabus Taxation 1 Atty. SaniDocument13 pagesProposed Syllabus Taxation 1 Atty. SaniZubair BatuaNo ratings yet

- Taxation - Deduction - Quizzer - CPA Review - 2017Document6 pagesTaxation - Deduction - Quizzer - CPA Review - 2017Kenneth Bryan Tegerero Tegio100% (1)

- Direct Taxation Compiled NotesDocument164 pagesDirect Taxation Compiled NotesSIDDHARTH ahlawatNo ratings yet

- Income Tax IndividualDocument22 pagesIncome Tax IndividualJohn Oicemen RocaNo ratings yet

- Final Income TaxationDocument7 pagesFinal Income TaxationJimmyChaoNo ratings yet

- Che Che H. Datingaling OMGT-2102: Answer: Taxable Income Is P700,000Document4 pagesChe Che H. Datingaling OMGT-2102: Answer: Taxable Income Is P700,000cheche datingalingNo ratings yet

- Week 6 Module 5 Analysis and Interpretation of Financial StatementsDocument31 pagesWeek 6 Module 5 Analysis and Interpretation of Financial StatementsZed Mercy86% (14)

- Investment in Debt SecuritiesDocument21 pagesInvestment in Debt SecuritiesAlarich CatayocNo ratings yet

- Excel Professional Services, Inc.: Cpa ReviewDocument11 pagesExcel Professional Services, Inc.: Cpa ReviewKuro HanabusaNo ratings yet

- Antero Sison JR v. AnchetaDocument4 pagesAntero Sison JR v. AnchetaL.C.ChengNo ratings yet

- Tax - Midterm NTC 2017Document12 pagesTax - Midterm NTC 2017Red YuNo ratings yet

- National Cannabis Industry Association White Paper: 280EDocument10 pagesNational Cannabis Industry Association White Paper: 280EMichael_Lee_RobertsNo ratings yet

- 3 - Income Tax On IndividualsDocument22 pages3 - Income Tax On IndividualsRylleMatthanCorderoNo ratings yet

- Taxation of Individuals 2016 Edition 7th Edition Spilker Test Bank 1Document36 pagesTaxation of Individuals 2016 Edition 7th Edition Spilker Test Bank 1troysalazartxqiwygaoj100% (29)

- FABM2 - Q1 - Module 5 - Analysis and Interpretation of Financial StatementsDocument37 pagesFABM2 - Q1 - Module 5 - Analysis and Interpretation of Financial StatementsHanzel NietesNo ratings yet

- Esso V CIRDocument4 pagesEsso V CIRWinnie Ann Daquil Lomosad-MisagalNo ratings yet

- Exclusions From Gross IncomeDocument29 pagesExclusions From Gross IncomeJC89% (9)

- Golpo 10 Task Performance 1.taxationDocument13 pagesGolpo 10 Task Performance 1.taxationNin JahNo ratings yet

- Taxation of Business IncomeDocument15 pagesTaxation of Business Incomekitderoger_391648570No ratings yet

- Gross Income TaxationDocument8 pagesGross Income TaxationJenelyn FloresNo ratings yet

- Income Taxation Business TaxationDocument62 pagesIncome Taxation Business TaxationAllen SoNo ratings yet

- CPALE CoverageDocument15 pagesCPALE CoverageMajariya Sahar SabladNo ratings yet

- Marubeni vs. CIRDocument2 pagesMarubeni vs. CIRJay-ar Rivera BadulisNo ratings yet

- Cpa Review - CGTDocument10 pagesCpa Review - CGTKenneth Bryan Tegerero TegioNo ratings yet

- ABM Fundamentals of ABM 2 CGDocument6 pagesABM Fundamentals of ABM 2 CGpaul cruzNo ratings yet

- Problem Exercises in Taxation: Prepared By: Dr. Jeannie P. LimDocument28 pagesProblem Exercises in Taxation: Prepared By: Dr. Jeannie P. LimJason Joseph AzuraNo ratings yet

- ABM11 BussMath Q2 Wk2 Gross-And-Net-EarningsDocument9 pagesABM11 BussMath Q2 Wk2 Gross-And-Net-EarningsArchimedes Arvie Garcia100% (1)