Download as pdf or txt

You might also like

- Essentials of Financial Management 3rd Edition Brigham Solutions ManualDocument14 pagesEssentials of Financial Management 3rd Edition Brigham Solutions ManualDavidWilliamsxwdgs100% (14)

- Borser Business Plan For Crypto CurrencyDocument68 pagesBorser Business Plan For Crypto Currencyzeedanshan75% (4)

- Fundamentals of Financial Management Concise Edition 8th Edition Brigham Solutions ManualDocument26 pagesFundamentals of Financial Management Concise Edition 8th Edition Brigham Solutions ManualJadeFischerqtcj100% (62)

- The Following Questions Might Be Addressed When An Auditor Is Completing An Internal Control QuestionDocument1 pageThe Following Questions Might Be Addressed When An Auditor Is Completing An Internal Control QuestionSomething ChicNo ratings yet

- 01 Quiz 1Document2 pages01 Quiz 1anna mae orcioNo ratings yet

- Items 1Document7 pagesItems 1RYANNo ratings yet

- CasesDocument3 pagesCasesHL100% (1)

- Heagy and Lehmann Accounting Information SystemDocument53 pagesHeagy and Lehmann Accounting Information SystemVal Mercury Faburada100% (1)

- CMA2011 CatalogDocument5 pagesCMA2011 CatalogDaryl DizonNo ratings yet

- 1.1 Assignment1 Internal Audit and The Audit Committee and Types of AuditDocument4 pages1.1 Assignment1 Internal Audit and The Audit Committee and Types of AuditXexiannaNo ratings yet

- Ans To Exercises Stice Chap 1 and Hall Chap 1234 5 11 All ProblemsDocument188 pagesAns To Exercises Stice Chap 1 and Hall Chap 1234 5 11 All ProblemsLouise GazaNo ratings yet

- ACCA109Document31 pagesACCA109Elma Joyce BondocNo ratings yet

- Mancon Quiz 3Document25 pagesMancon Quiz 3Quendrick SurbanNo ratings yet

- MainDocument16 pagesMainArjay DeausenNo ratings yet

- Question 1 of 8: Fill in The BlanksDocument3 pagesQuestion 1 of 8: Fill in The BlanksPing Ping100% (1)

- Straight ProblemsDocument1 pageStraight ProblemsMaybelle100% (1)

- AIS Exercise Workbook 37Document37 pagesAIS Exercise Workbook 37Helen Rose CepedaNo ratings yet

- Chapter 2 Business ProcessesDocument2 pagesChapter 2 Business ProcessesChristlyn Joy BaralNo ratings yet

- 118.2 - Illustrative Examples - IFRS15 Part 1Document3 pages118.2 - Illustrative Examples - IFRS15 Part 1Ian De DiosNo ratings yet

- Applied Auditing Assignment 3Document2 pagesApplied Auditing Assignment 3Leny Joy DupoNo ratings yet

- Quiz 1 SolutionsDocument5 pagesQuiz 1 Solutionsgovt2No ratings yet

- FM Second AssignmentDocument3 pagesFM Second AssignmentpushmbaNo ratings yet

- AE120 - Final Activity 1Document1 pageAE120 - Final Activity 1Krystal shaneNo ratings yet

- Acc Chap 1Document17 pagesAcc Chap 1adahung23No ratings yet

- Apc 301 Week 8Document2 pagesApc 301 Week 8Angel Lourdie Lyn HosenillaNo ratings yet

- Karma Company Sells Televisions at An Average Price of P7Document1 pageKarma Company Sells Televisions at An Average Price of P7Nicole AguinaldoNo ratings yet

- Review Questions and ProblemsDocument4 pagesReview Questions and ProblemsIsha LarionNo ratings yet

- Chap 4Document7 pagesChap 4Christine Joy OriginalNo ratings yet

- Lesson 4 Expenditure Cycle PDFDocument19 pagesLesson 4 Expenditure Cycle PDFJoshua JunsayNo ratings yet

- PFRS 10 13Document2 pagesPFRS 10 13Patrick RiveraNo ratings yet

- Notre Dame of Midsayap College: AssignmentDocument10 pagesNotre Dame of Midsayap College: Assignmentjaocent brixNo ratings yet

- TB Raiborn - Implementing Quality ConceptsDocument22 pagesTB Raiborn - Implementing Quality ConceptsJoan Grachell TaguilasoNo ratings yet

- Newfmtb2 1Document28 pagesNewfmtb2 1fasdsadsaNo ratings yet

- Advanced Accounting 2 Dayag Solution ManualpdfDocument3 pagesAdvanced Accounting 2 Dayag Solution ManualpdfAnonymous krSC21yNo ratings yet

- C36 Planning-W RevisionsDocument23 pagesC36 Planning-W RevisionsNicole Johnson100% (1)

- R3 - ARC - AP and ATDocument10 pagesR3 - ARC - AP and ATOliver SalamidaNo ratings yet

- AuditDocument1 pageAuditTrisha RafalloNo ratings yet

- Prepare The Current Liabilities Section of The Statement of Financial Position For The Layla Company As of December 31, 2020Document1 pagePrepare The Current Liabilities Section of The Statement of Financial Position For The Layla Company As of December 31, 2020versNo ratings yet

- AC 3101 Discussion ProblemDocument1 pageAC 3101 Discussion ProblemYohann Leonard HuanNo ratings yet

- Quiz#1Document10 pagesQuiz#1Danna BarredoNo ratings yet

- Experiential Exercise Class Work Activity 4th Week. Alizay Waheed Kayani 24347Document2 pagesExperiential Exercise Class Work Activity 4th Week. Alizay Waheed Kayani 24347Alizay Kayani100% (1)

- Chapter 10 Initiatives To Improve Business Ethics and Reduce CorruptionDocument2 pagesChapter 10 Initiatives To Improve Business Ethics and Reduce CorruptionMarienella MarollanoNo ratings yet

- SW - NpoDocument1 pageSW - NpoGwy HipolitoNo ratings yet

- Starting RightDocument2 pagesStarting RightRichie DonatoNo ratings yet

- Additional Data For The Period Were ProvidedDocument3 pagesAdditional Data For The Period Were Providedmoncarla lagon100% (1)

- Managerial Finance by Gtman 5th EditionDocument17 pagesManagerial Finance by Gtman 5th EditionIrfan Yaqoob100% (1)

- Chapter 04 AnsDocument4 pagesChapter 04 AnsDave Manalo100% (1)

- This Study Resource Was: Assignment 1 - Overview of Financial Markets and Interest RatesDocument2 pagesThis Study Resource Was: Assignment 1 - Overview of Financial Markets and Interest RatesArjay Dela PenaNo ratings yet

- 01 Task Performance 1 - SBADocument9 pages01 Task Performance 1 - SBAPrincess AletreNo ratings yet

- AUDIT Journal 16Document9 pagesAUDIT Journal 16Daena NicodemusNo ratings yet

- 03 ITF Interactive Session Technology Is Ipad A Disruptive TechnologyDocument2 pages03 ITF Interactive Session Technology Is Ipad A Disruptive TechnologyRiyan Yamin100% (1)

- Chapter 4 - Seat Work - Assignment #4 - ACCOUNTING FOR GOVERNMENT AND NON - PROFIT ORGANIZATIONSDocument3 pagesChapter 4 - Seat Work - Assignment #4 - ACCOUNTING FOR GOVERNMENT AND NON - PROFIT ORGANIZATIONSDonise Ronadel SantosNo ratings yet

- Leonila Rivera MGT9Document1 pageLeonila Rivera MGT9Asvag OndaNo ratings yet

- Managerial AccountingMid Term Examination (1) - CONSULTADocument7 pagesManagerial AccountingMid Term Examination (1) - CONSULTAMay Ramos100% (1)

- Chapter 5 SM HeheDocument9 pagesChapter 5 SM HeheMaricel De la CruzNo ratings yet

- NullDocument22 pagesNullapi-28191758100% (1)

- Case Carolina-Wilderness-Outfitters-Case-Study PDFDocument8 pagesCase Carolina-Wilderness-Outfitters-Case-Study PDFMira miguelito50% (2)

- Cffm8 Im Ch02Document16 pagesCffm8 Im Ch02rajendrakumarNo ratings yet

- FFM12, CH 02, IM, 01-08-09Document13 pagesFFM12, CH 02, IM, 01-08-09Kareyn Ann SumayloNo ratings yet

- Dwnload Full Essentials of Financial Management 3rd Edition Brigham Solutions Manual PDFDocument36 pagesDwnload Full Essentials of Financial Management 3rd Edition Brigham Solutions Manual PDFupwindscatterf9ebp100% (16)

- Moral Philosophy: Is The Area of Philosophy Concerned With Theories of Ethics, With How We Ought To Live Our LivesDocument25 pagesMoral Philosophy: Is The Area of Philosophy Concerned With Theories of Ethics, With How We Ought To Live Our LivesLily DaniaNo ratings yet

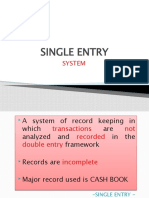

- 14single EntryDocument4 pages14single EntryLily DaniaNo ratings yet

- Lesson 6: Ethical Decision Making: Employee Rights Ethical Issues in The WorkplaceDocument24 pagesLesson 6: Ethical Decision Making: Employee Rights Ethical Issues in The WorkplaceLily DaniaNo ratings yet

- Lesson 5: Corporate Social Responsibility Ethics and Social Responsibility Enlightened Self InterestDocument35 pagesLesson 5: Corporate Social Responsibility Ethics and Social Responsibility Enlightened Self InterestLily DaniaNo ratings yet

- Ethics LAW Practice Reason: University of MindanaoDocument22 pagesEthics LAW Practice Reason: University of MindanaoLily DaniaNo ratings yet

- 10accounting ChangesDocument31 pages10accounting ChangesLily DaniaNo ratings yet

- Ethics and Business Week 1Document45 pagesEthics and Business Week 1Lily DaniaNo ratings yet

- 13cash and AccrualDocument6 pages13cash and AccrualLily DaniaNo ratings yet

- 15statement of Cash FlowsDocument26 pages15statement of Cash FlowsLily DaniaNo ratings yet

- Ethics As A Dimension of Social ResponsibilityDocument23 pagesEthics As A Dimension of Social ResponsibilityLily Dania100% (1)

- Ethics As A Dimension of Social ResponsibilityDocument7 pagesEthics As A Dimension of Social ResponsibilityLily DaniaNo ratings yet

- Auditing and Assurance ServicesDocument27 pagesAuditing and Assurance ServicesLily DaniaNo ratings yet

- Risk and Rates of Return CH06 PDFDocument16 pagesRisk and Rates of Return CH06 PDFLily DaniaNo ratings yet

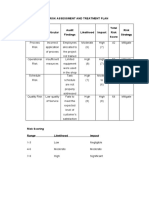

- Sample Only: Risk Assessment and Treatment PlanDocument1 pageSample Only: Risk Assessment and Treatment PlanLily DaniaNo ratings yet

- 2 - Premium and Warranty LiabilityDocument5 pages2 - Premium and Warranty LiabilityLily DaniaNo ratings yet

- Chapter 1 - Banks & Other Financial Intermediaries: 19 PersonsDocument4 pagesChapter 1 - Banks & Other Financial Intermediaries: 19 PersonsMary.Rose RosalesNo ratings yet

- Unit 2 Financial System and Its ComponenetsDocument54 pagesUnit 2 Financial System and Its Componenetsaishwarya raikar100% (1)

- SodapdfDocument22 pagesSodapdfYossantos SoloNo ratings yet

- Midterm Fin Oo4Document82 pagesMidterm Fin Oo4patricia gunio100% (1)

- Chapter 02Document20 pagesChapter 02Thang TranNo ratings yet

- 6 Entrepreneurship Chapter Six LectureDocument43 pages6 Entrepreneurship Chapter Six LecturedebisahirpaNo ratings yet

- Short Notes MBA BANK and VIVADocument18 pagesShort Notes MBA BANK and VIVAArmanul HaqueNo ratings yet

- Lesson 2 The Financial System and Its RegulationDocument16 pagesLesson 2 The Financial System and Its RegulationEliza Calixto-SorianososNo ratings yet

- Entrepreneurship: Financing The New Venture and BeyondDocument31 pagesEntrepreneurship: Financing The New Venture and BeyondSiti Sarah Zalikha Binti Umar BakiNo ratings yet

- Sources of FinanceDocument17 pagesSources of FinanceNikita ParidaNo ratings yet

- Which Specific Entrepreneurial Traits You Could See in Suhag?Document8 pagesWhich Specific Entrepreneurial Traits You Could See in Suhag?Dnyaneshwari VyasNo ratings yet

- Analysis of Mutual FundDocument20 pagesAnalysis of Mutual FundKritika TNo ratings yet

- Financial Management PDFDocument111 pagesFinancial Management PDFcheri kok100% (1)

- MULTIFINANCINGDocument12 pagesMULTIFINANCINGAmadeusNo ratings yet

- Contemporary Financial Management 12th Edition Moyer Solutions ManualDocument35 pagesContemporary Financial Management 12th Edition Moyer Solutions Manualbyronrogersd1nw8100% (34)

- Merchant Banking VeenaDocument69 pagesMerchant Banking VeenaVEENA RANENo ratings yet

- Notificationfor Proposed Acquisitions Legal PersonDocument33 pagesNotificationfor Proposed Acquisitions Legal Personsmnponomarev0702No ratings yet

- Managing The Finance Function Managing The Finance Function: Group 10Document30 pagesManaging The Finance Function Managing The Finance Function: Group 10Ellen Rose NovoNo ratings yet

- Achieving Financial PerformanceDocument8 pagesAchieving Financial PerformanceozuwoNo ratings yet

- Survey Questionnaire Google FormsDocument6 pagesSurvey Questionnaire Google FormsAbby SulimaNo ratings yet

- Lucky Cement Strategic OptionsDocument5 pagesLucky Cement Strategic OptionsFahim QaiserNo ratings yet

- National MSME Policy 2020-2024 New 1Document28 pagesNational MSME Policy 2020-2024 New 1BURUNDI1No ratings yet

- Full Download Test Bank For The Economics of Money Banking and Financial Markets 12th Edition Mishkin PDF Full ChapterDocument36 pagesFull Download Test Bank For The Economics of Money Banking and Financial Markets 12th Edition Mishkin PDF Full Chaptermispleadtrews265p100% (26)

- Chapter 4Document14 pagesChapter 4Yosef KetemaNo ratings yet

- Test Bank For The Economics of Money Banking and Financial Markets 12th Edition MishkinDocument36 pagesTest Bank For The Economics of Money Banking and Financial Markets 12th Edition Mishkinordainer.cerule2q8q5g100% (32)

- 20 Start-Ups in India: Challenges and Government SupportDocument4 pages20 Start-Ups in India: Challenges and Government SupportAyush AgrawalNo ratings yet

- Assessing The Feasibility of A New Venture 1.1 Assessment and Evaluation of Entrepreneurial OpportunitiesDocument13 pagesAssessing The Feasibility of A New Venture 1.1 Assessment and Evaluation of Entrepreneurial OpportunitiesBereket Desalegn100% (1)

- Mechanical Articulating Axes Project Proposal by SlidesgoDocument41 pagesMechanical Articulating Axes Project Proposal by SlidesgoNajma AtchanyNo ratings yet

- Entrepreneurship ExamsDocument15 pagesEntrepreneurship ExamsKatrina CaveNo ratings yet