Download as pdf or txt

You might also like

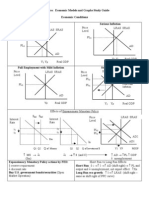

- AP Macroeconomic Models and Graphs Study GuideDocument23 pagesAP Macroeconomic Models and Graphs Study GuideAznAlexT90% (21)

- The Tier 4 Microfinance Institutions and Money Lenders Money Lenders RegulationDocument26 pagesThe Tier 4 Microfinance Institutions and Money Lenders Money Lenders RegulationCHARLES ODOKI OKELLANo ratings yet

- Local Tax Code and Its AmendmentsDocument9 pagesLocal Tax Code and Its AmendmentsNoel Ephraim AntiguaNo ratings yet

- CITIBANK Export Document Collections Application PDFDocument5 pagesCITIBANK Export Document Collections Application PDFSyed Fahad Bin NazeerNo ratings yet

- Debre Markos University College of Business and Economics Department of EconomicsDocument484 pagesDebre Markos University College of Business and Economics Department of EconomicsYeshiwas EwinetuNo ratings yet

- Certificate of Interest FY21 XXXXXXXX2355Document1 pageCertificate of Interest FY21 XXXXXXXX2355Bhoopndare PallNo ratings yet

- Chapter 24 CPWD ACCOUNTS CODEDocument5 pagesChapter 24 CPWD ACCOUNTS CODEarulraj1971No ratings yet

- CEWARN Communication Strategy Tender Dossier - 1 August 2019Document34 pagesCEWARN Communication Strategy Tender Dossier - 1 August 2019Anonymous WUAZ3A5tCxNo ratings yet

- Chap 6 - Financial Statements With AdjustmentDocument24 pagesChap 6 - Financial Statements With AdjustmentEli Syahirah100% (1)

- Republic of The Philippines: Department of Public Works and Highways Office of The District EngineerDocument106 pagesRepublic of The Philippines: Department of Public Works and Highways Office of The District EngineerMar JoeNo ratings yet

- Tender Document: Bharat Sanchar Nigam Ltd. (BSNL)Document32 pagesTender Document: Bharat Sanchar Nigam Ltd. (BSNL)engg.satyaNo ratings yet

- Disclosure in Financial Statements - Notes To AccountsDocument25 pagesDisclosure in Financial Statements - Notes To Accountseknath2000No ratings yet

- RTGSDocument14 pagesRTGSHarshUpadhyayNo ratings yet

- Depository and Settlement SystemsDocument34 pagesDepository and Settlement Systemsarchana_anuragiNo ratings yet

- Functions Commercial Bank & Nationalized BankDocument38 pagesFunctions Commercial Bank & Nationalized BankToriqul Islam JonyNo ratings yet

- Instructions Set of 8086Document63 pagesInstructions Set of 8086aymanaymanNo ratings yet

- A AtcDocument2 pagesA Atckupalking100% (1)

- Dimensions of Cash Flow Management: Prof. N. C. KarDocument74 pagesDimensions of Cash Flow Management: Prof. N. C. KarAshok100% (1)

- About Rtgs & NeftDocument5 pagesAbout Rtgs & NeftAbdulhussain JariwalaNo ratings yet

- AG Office AccountingDocument165 pagesAG Office AccountingabadeshNo ratings yet

- Schedule of ChargesDocument14 pagesSchedule of ChargeskrishmasethiNo ratings yet

- 1601 C CompensationDocument2 pages1601 C Compensationjon_cpaNo ratings yet

- 1 1 BondsDocument10 pages1 1 BondsyukiyurikiNo ratings yet

- United States Securities and Exchange Commission Washington, D.C. 20549 Form 1-U Current Report Pursuant To Regulation ADocument8 pagesUnited States Securities and Exchange Commission Washington, D.C. 20549 Form 1-U Current Report Pursuant To Regulation AAnthony ANTONIO TONY LABRON ADAMSNo ratings yet

- May 30 Provider Relief Fund FAQ RedlineDocument23 pagesMay 30 Provider Relief Fund FAQ RedlineRachel Cohrs100% (1)

- IRS Page 557Document75 pagesIRS Page 557Mark AustinNo ratings yet

- Form 8-K: Current Report Pursuant To Section 13 OR 15 (D) of The Securities Exchange Act of 1934Document22 pagesForm 8-K: Current Report Pursuant To Section 13 OR 15 (D) of The Securities Exchange Act of 1934g6hNo ratings yet

- Formulir 20-fDocument66 pagesFormulir 20-fAndre KusumaNo ratings yet

- BondDocument22 pagesBondBRAINSTORM Haroon RasheedNo ratings yet

- Introduction To Actuators: Primary Knowledge Participant GuideDocument10 pagesIntroduction To Actuators: Primary Knowledge Participant GuideInbanesan AkNo ratings yet

- Adjustments of Final AccountsDocument11 pagesAdjustments of Final AccountsUmesh Gaikwad50% (10)

- Microsoft Word - Chapter 06 Negotiable InstrumentsDocument9 pagesMicrosoft Word - Chapter 06 Negotiable InstrumentsDuy Trần TấnNo ratings yet

- Sample Real Estate Purchase & Sale Agreement Template: Aaron Hall Business Attorney Minneapolis, MinnesotaDocument13 pagesSample Real Estate Purchase & Sale Agreement Template: Aaron Hall Business Attorney Minneapolis, MinnesotabruuhhhhNo ratings yet

- GPF Bill Form 48Document8 pagesGPF Bill Form 48ChristoDeepthiNo ratings yet

- Diamond AccountDocument2 pagesDiamond AccountJagadeesh YathirajulaNo ratings yet

- Tax Benefit On Home Loan - Section 24, 80C, 80EE PDFDocument5 pagesTax Benefit On Home Loan - Section 24, 80C, 80EE PDFRajiv RanjanNo ratings yet

- Goldman v. Richmond (2019) Count 2 Documents: Consolidated Questions & ResponsesDocument122 pagesGoldman v. Richmond (2019) Count 2 Documents: Consolidated Questions & ResponsesActivate VirginiaNo ratings yet

- PAYE Tax TablesDocument3 pagesPAYE Tax TablesDanushka MarasingheNo ratings yet

- GPA Conversion ChartDocument1 pageGPA Conversion ChartPra DeepNo ratings yet

- Tax Burden UKDocument13 pagesTax Burden UKArturas GumuliauskasNo ratings yet

- 2015 CPNI-Compliance-Manual ABT Telecom 830402 PDFDocument34 pages2015 CPNI-Compliance-Manual ABT Telecom 830402 PDFFederal Communications Commission (FCC)No ratings yet

- Chart of AccountsDocument37 pagesChart of Accountsmrhanif_znNo ratings yet

- Trinidad and Tobago Emolument Income Tax 2012Document5 pagesTrinidad and Tobago Emolument Income Tax 2012Anand RockerNo ratings yet

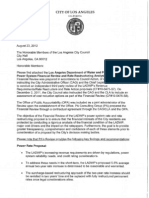

- LADWP Power Rate Proposal Cost Reduction ReportDocument143 pagesLADWP Power Rate Proposal Cost Reduction ReportBill RosendahlNo ratings yet

- Shall File A Return Under OathDocument17 pagesShall File A Return Under OathMixx MineNo ratings yet

- Senate Hearings: Treasury and General Government AppropriationsDocument562 pagesSenate Hearings: Treasury and General Government AppropriationsScribd Government DocsNo ratings yet

- 79.02 - Trinidad and Tobago Central Bank ActDocument80 pages79.02 - Trinidad and Tobago Central Bank ActOilmanGHNo ratings yet

- Compilation of Guidelines For Redress of Public Grievances - Naresh KadyanDocument290 pagesCompilation of Guidelines For Redress of Public Grievances - Naresh KadyanNaresh KadyanNo ratings yet

- Sample Sa: Escrow AgreementDocument4 pagesSample Sa: Escrow AgreementEins BalagtasNo ratings yet

- Chapter Two Investment Allowances NotesDocument12 pagesChapter Two Investment Allowances NotesTriila manillaNo ratings yet

- Nepal-Pia MCC AgreementDocument35 pagesNepal-Pia MCC AgreementBhava Nath DahalNo ratings yet

- Government Borrowing From The Banking System: Implications For Monetary and Financial StabilityDocument26 pagesGovernment Borrowing From The Banking System: Implications For Monetary and Financial StabilitySana NazNo ratings yet

- 2631-3008 (Tab C Exs. 94 (G-O) (PUBLIC)Document378 pages2631-3008 (Tab C Exs. 94 (G-O) (PUBLIC)GriswoldNo ratings yet

- Financial Management - Bond ValuationDocument17 pagesFinancial Management - Bond ValuationNoelia Mc DonaldNo ratings yet

- Banking ServicesDocument7 pagesBanking ServicesMr PenZoNo ratings yet

- Important Banking GK PDFDocument26 pagesImportant Banking GK PDFPriya BanothNo ratings yet

- (BW Version) Grad - Financial - Verification - Form 2021-2022Document2 pages(BW Version) Grad - Financial - Verification - Form 2021-2022Pao SuarezNo ratings yet

- Department of The Treasury: WASHINGTON, D.C. 20220Document26 pagesDepartment of The Treasury: WASHINGTON, D.C. 20220ForkLogNo ratings yet

- Chapter 6 - Amortization and Sinking FundsDocument10 pagesChapter 6 - Amortization and Sinking FundsAreeba AhsanNo ratings yet

- Amortisations and Sinking FundsDocument7 pagesAmortisations and Sinking FundsChari TawaNo ratings yet

- Chapter - ThreeDocument19 pagesChapter - Threemagarsa hirphaNo ratings yet

- 4 Year Mechanical Power: Dr. Mohamed Hammam 2020Document14 pages4 Year Mechanical Power: Dr. Mohamed Hammam 2020Mohamed HammamNo ratings yet

- Math 134 Tutorial 8 Annuities Due, Deferred Annuities, Perpetuities and Calculus: First PrinciplesDocument5 pagesMath 134 Tutorial 8 Annuities Due, Deferred Annuities, Perpetuities and Calculus: First PrinciplesJVA ACCOUNTINGNo ratings yet

- Production, Society and THE OraganizationDocument10 pagesProduction, Society and THE OraganizationJVA ACCOUNTINGNo ratings yet

- Cover NG ReliefDocument116 pagesCover NG ReliefJVA ACCOUNTINGNo ratings yet

- Tuamuini: Schedule of SSS Contribution Employee FileDocument2 pagesTuamuini: Schedule of SSS Contribution Employee FileJVA ACCOUNTINGNo ratings yet

- Transaction HistoryDocument5 pagesTransaction HistoryLinh NguyễnNo ratings yet

- Annex II - Form A2 - RevisedDocument3 pagesAnnex II - Form A2 - RevisedRamya RameshNo ratings yet

- Ejoh, N. O., Okpa, I. B., & Egbe, A. A. (2014) .Document15 pagesEjoh, N. O., Okpa, I. B., & Egbe, A. A. (2014) .Vita NataliaNo ratings yet

- What Is BaselIII Norms For BanksDocument3 pagesWhat Is BaselIII Norms For BanksCarbideman100% (1)

- Objective: Time: Faculty: MR Pramod Khandelwal: Banklaw - inDocument1 pageObjective: Time: Faculty: MR Pramod Khandelwal: Banklaw - inSarvjeet KaurNo ratings yet

- UtangDocument10 pagesUtangrex tanongNo ratings yet

- Bank of UgandaDocument12 pagesBank of Ugandaimmaculate nampijjaNo ratings yet

- Bank Alfalah Clearance DepartmentDocument7 pagesBank Alfalah Clearance Departmenthassan_shazaib100% (1)

- HDFC ReportDocument9 pagesHDFC ReportronaktejaniNo ratings yet

- Lecture Notes - Residential Mortgage Finance - Nov 11Document46 pagesLecture Notes - Residential Mortgage Finance - Nov 11nexis1No ratings yet

- Cap One StateDocument6 pagesCap One StatealiNo ratings yet

- Pasir Putih 1 31/03/22Document18 pagesPasir Putih 1 31/03/22Evonne L YKNo ratings yet

- Literature Review of Online Payment SystemDocument5 pagesLiterature Review of Online Payment Systemrobin75% (4)

- A Brief History & Development of Banking in India and Its FutureDocument12 pagesA Brief History & Development of Banking in India and Its FutureMani KrishNo ratings yet

- On Study of Cash Management at Axis BankDocument18 pagesOn Study of Cash Management at Axis BankHimanshu0% (1)

- Why Are Financial Institutions Special ?Document42 pagesWhy Are Financial Institutions Special ?azzaNo ratings yet

- Request For Electronic Policy Payout: Policy Number Name of Policy Holder Aadhaar Number PAN Mobile NumberDocument1 pageRequest For Electronic Policy Payout: Policy Number Name of Policy Holder Aadhaar Number PAN Mobile Numberrovensingh007No ratings yet

- Banking Awareness 2017 Reference Guide For IBPS PO VII PDFDocument114 pagesBanking Awareness 2017 Reference Guide For IBPS PO VII PDFAshutosh KumarNo ratings yet

- Chapter Title: List of Abbreviations List of Cases List of Table List of Figure PrefaceDocument13 pagesChapter Title: List of Abbreviations List of Cases List of Table List of Figure PrefaceASHU KNo ratings yet

- PR1 Abm C GR2Document35 pagesPR1 Abm C GR2Trisha Paola LaguraNo ratings yet

- BCBS 2018 Progress Report 2022Document76 pagesBCBS 2018 Progress Report 2022JulianNo ratings yet

- Statement of Account - 1700981538124nDocument4 pagesStatement of Account - 1700981538124nporagbhai00No ratings yet

- Introduction To Monetary PolicyDocument32 pagesIntroduction To Monetary PolicycaamitbhartiNo ratings yet

- A Study of Loans and Advances Offered in ICICI BankDocument3 pagesA Study of Loans and Advances Offered in ICICI BankNeha toshniwalNo ratings yet

- Usda Rural House GrantDocument2 pagesUsda Rural House GrantElisa Getlawgirl100% (1)

- Test Cases For ATM: Verifying The MessageDocument2 pagesTest Cases For ATM: Verifying The MessageAbdul WaheedNo ratings yet

- Banker Customer RelationshipDocument18 pagesBanker Customer RelationshipShahriar Kabir KhanNo ratings yet

- Truist Bank Powerpoint ActivityDocument12 pagesTruist Bank Powerpoint Activityapi-688079199No ratings yet