Download as doc, pdf, or txt

You might also like

- Altea CM (Customer Management)Document8 pagesAltea CM (Customer Management)NathanaelNo ratings yet

- Accounting Activity 2019Document17 pagesAccounting Activity 2019Cleiton Dave Malabuyoc0% (2)

- Accounting ExerciseDocument2 pagesAccounting ExerciseRahul Gupta100% (1)

- SEO - Live Project Track 3Document4 pagesSEO - Live Project Track 3Kamal Matharoo100% (1)

- Activity Sheet Adjusting Entries DeferralsDocument1 pageActivity Sheet Adjusting Entries DeferralsShania LiwanagNo ratings yet

- Adjustments Quiz 2Document6 pagesAdjustments Quiz 2Loey ParkNo ratings yet

- Assignment Number 2 Financial Accounting Reporting 1Document8 pagesAssignment Number 2 Financial Accounting Reporting 1Sheina Jane AbarquezNo ratings yet

- 14 AdjustmentsssDocument7 pages14 AdjustmentsssZaheer Ahmed SwatiNo ratings yet

- Accounting Problems and Exercises4 Accounting Cycle IllustrationDocument1 pageAccounting Problems and Exercises4 Accounting Cycle IllustrationMario Agoncillo50% (2)

- Card Number Booklet Number Merchant Outlet Outletcode Outlettype Erpcode Descriptive Outlet NameDocument7 pagesCard Number Booklet Number Merchant Outlet Outletcode Outlettype Erpcode Descriptive Outlet Namepawan soniNo ratings yet

- 01 Quiz 1Document2 pages01 Quiz 1Laisan SantosNo ratings yet

- Worksheet PreparationDocument3 pagesWorksheet PreparationJon PangilinanNo ratings yet

- Chapter 10Document16 pagesChapter 10Charlene LeynesNo ratings yet

- Exercise 3 Leah GarciaDocument12 pagesExercise 3 Leah GarciaMa Sophia Mikaela EreceNo ratings yet

- Lecture Notes - Chapter 7Document17 pagesLecture Notes - Chapter 7Nova Grace LatinaNo ratings yet

- Journalizing Exercises 10Document11 pagesJournalizing Exercises 10John DelaPaz0% (1)

- Accounting Equation ActivityDocument3 pagesAccounting Equation ActivityGJ BadenasNo ratings yet

- Accounting For Merchandising Operations LongDocument2 pagesAccounting For Merchandising Operations Longgk concepcionNo ratings yet

- Philippine Christian University Dasmariñas Campus: AssignmentDocument9 pagesPhilippine Christian University Dasmariñas Campus: AssignmentJonathan Joshua FilioNo ratings yet

- Simple and Compound EntryDocument4 pagesSimple and Compound EntryJezeil DimasNo ratings yet

- 01 Activity 2Document4 pages01 Activity 2Laisan SantosNo ratings yet

- 2accounting Lesson - Accounting EquationDocument6 pages2accounting Lesson - Accounting EquationFlorante SilangNo ratings yet

- Accounting Cycle of A Merchandising BusinessDocument2 pagesAccounting Cycle of A Merchandising BusinessAnne Alag100% (1)

- Module 2 - Completing The Accounting CycleDocument45 pagesModule 2 - Completing The Accounting CycleShane TorrieNo ratings yet

- Santa Rosa Campus City of Santa Rosa, Laguna: Polytechnic University of The PhilippinesDocument19 pagesSanta Rosa Campus City of Santa Rosa, Laguna: Polytechnic University of The Philippinesareum100% (1)

- Commenced Business With A Capital of 1Document4 pagesCommenced Business With A Capital of 1sonika7100% (1)

- Special Journals Cherry Lopez Wear Ever Store BSA13Document12 pagesSpecial Journals Cherry Lopez Wear Ever Store BSA13Erika RepedroNo ratings yet

- Chapter 5 Double Entry Bookkeeping For A Service ProviderDocument8 pagesChapter 5 Double Entry Bookkeeping For A Service ProviderPaw Verdillo100% (1)

- XYZ CompanyDocument8 pagesXYZ CompanyLala Bub100% (1)

- CHAPTER 4: DO IT! 1 Worksheet: Blessie, Capital Jan. 1, 2019 961,900Document3 pagesCHAPTER 4: DO IT! 1 Worksheet: Blessie, Capital Jan. 1, 2019 961,900CacjungoyNo ratings yet

- Chart of Accounts General Ledger General Ledger Page No. Page No. Assets IncomeDocument44 pagesChart of Accounts General Ledger General Ledger Page No. Page No. Assets IncomeJireh RiveraNo ratings yet

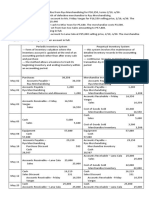

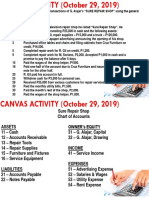

- Canvas Activity - Journalizing - Oct - 29 PDFDocument2 pagesCanvas Activity - Journalizing - Oct - 29 PDFJian Francisco100% (2)

- Problem 15Document1 pageProblem 15Alyssa Jane G. AlvarezNo ratings yet

- Module II - Analyzing Business TransactionsDocument4 pagesModule II - Analyzing Business TransactionsIj IlardeNo ratings yet

- Accounting Adjusting EntryDocument20 pagesAccounting Adjusting EntryClemencia Masiba100% (1)

- Accounting For Nonvat and Vat Registered Business Solution To Assign 1 Quiz 1Document16 pagesAccounting For Nonvat and Vat Registered Business Solution To Assign 1 Quiz 1Fider GracianNo ratings yet

- Assignment 6b FabmDocument4 pagesAssignment 6b FabmKhriza Joy SalvadorNo ratings yet

- Senior High School Department: Quarter 3 - Module 12: Adjusting Journal EntriesDocument14 pagesSenior High School Department: Quarter 3 - Module 12: Adjusting Journal EntriesJaye Ruanto100% (2)

- 2019 Review Quiz Without Answer SheetDocument4 pages2019 Review Quiz Without Answer SheetSittie HafsahNo ratings yet

- FSDocument44 pagesFSMaria Beatriz Aban Munda100% (2)

- w1 Fabmii Review of Basic Bookkeeping Skills Part2Document18 pagesw1 Fabmii Review of Basic Bookkeeping Skills Part2Mizuki YamizakiNo ratings yet

- Lesson 1 ExtendDocument6 pagesLesson 1 ExtendRoel Cababao50% (2)

- Accounting 1 Review Series Worksheet ExercisesDocument14 pagesAccounting 1 Review Series Worksheet ExercisesKayle Mallillin100% (2)

- PDF Journal Entries Tradingdocx CompressDocument79 pagesPDF Journal Entries Tradingdocx CompressMaskter TwinsetsNo ratings yet

- Whole Cycle - Accounting Act.Document26 pagesWhole Cycle - Accounting Act.IL MareNo ratings yet

- Diaz - Journal EntriesDocument4 pagesDiaz - Journal EntriesPangitkaNo ratings yet

- Financial Accounting and ReportingDocument1 pageFinancial Accounting and ReportingPaula BautistaNo ratings yet

- MERCHANDISINGDocument74 pagesMERCHANDISINGKisha Nicole R. EnanoriaNo ratings yet

- DDocument2 pagesDChy B0% (2)

- CHP 2 Exam Preparation ProblemsDocument3 pagesCHP 2 Exam Preparation ProblemsShawn JohnstonNo ratings yet

- EXERCISE/ ACTIVITIES 1.1 - Yung Dora Catan: Transactions Debit Credit A B C D e F G H I JDocument8 pagesEXERCISE/ ACTIVITIES 1.1 - Yung Dora Catan: Transactions Debit Credit A B C D e F G H I JCharrie Faye Magbitang HernandezNo ratings yet

- LESSON 10 Business TransactionsDocument8 pagesLESSON 10 Business TransactionsUnamadable UnleomarableNo ratings yet

- General Journal, GeveraDocument2 pagesGeneral Journal, GeveraFeiya LiuNo ratings yet

- Accounting Cycle and Book of AccountsDocument23 pagesAccounting Cycle and Book of AccountsChaaaNo ratings yet

- Short Case ActivitiesDocument2 pagesShort Case ActivitiesRaff LesiaaNo ratings yet

- SW-16 UTB Merchandising AsDocument4 pagesSW-16 UTB Merchandising AsAlexis Marie Balagot100% (1)

- Account Titles and Its ElementsDocument3 pagesAccount Titles and Its ElementsJeb PampliegaNo ratings yet

- Republic of The Philippines ISO 9001:2015 CERTIFIED: Prepared By: GERLY S. RADAM/instructor RALYN T. JAGUROS/instructorDocument7 pagesRepublic of The Philippines ISO 9001:2015 CERTIFIED: Prepared By: GERLY S. RADAM/instructor RALYN T. JAGUROS/instructorJessie Mark AnapadaNo ratings yet

- JOURNALIZINGDocument2 pagesJOURNALIZINGArneld SantiagoNo ratings yet

- Midterm Summative Examination (B-FND003) (ECO11 & ENR11) - Set A (Answers, Jan Marwin G. Alindog)Document6 pagesMidterm Summative Examination (B-FND003) (ECO11 & ENR11) - Set A (Answers, Jan Marwin G. Alindog)Vaseline QtipsNo ratings yet

- Merchandising Operations Under Periodic InventoryDocument36 pagesMerchandising Operations Under Periodic InventoryCharlyn galahanNo ratings yet

- Acc - Section 3B1 Cash BookDocument8 pagesAcc - Section 3B1 Cash BookNathefa LayneNo ratings yet

- SmartLogger ModBus Interface DefinitionsDocument50 pagesSmartLogger ModBus Interface DefinitionsgustavoNo ratings yet

- Iso 21308 2 2006Document15 pagesIso 21308 2 2006Milton PeñaNo ratings yet

- Pass4sure 312-50v9 DumpsDocument6 pagesPass4sure 312-50v9 Dumpsjpince0% (1)

- Curtis CatalogDocument9 pagesCurtis CatalogtharngalNo ratings yet

- Chap 6 Class 9 CompDocument7 pagesChap 6 Class 9 CompSaira AwanNo ratings yet

- Diagnostics GuideDocument588 pagesDiagnostics GuidejeronimostNo ratings yet

- Generation of Computers: Camarines Sur National High School Icf 7 Learning Activity Sheet Quarter 1, Week 4Document9 pagesGeneration of Computers: Camarines Sur National High School Icf 7 Learning Activity Sheet Quarter 1, Week 4Houstine ErisareNo ratings yet

- The Information AgeDocument6 pagesThe Information AgeMaria Amor TleonNo ratings yet

- Quectel Rm500Q-Gl: Iot/Embb-Optimized 5G Sub-6 GHZ M.2 ModuleDocument3 pagesQuectel Rm500Q-Gl: Iot/Embb-Optimized 5G Sub-6 GHZ M.2 Modulektmb motoNo ratings yet

- Lexmark Cxx10 MFP: Machine Type 7527-2Xx, - 4Xx, - 63XDocument394 pagesLexmark Cxx10 MFP: Machine Type 7527-2Xx, - 4Xx, - 63XOmar SanchezNo ratings yet

- NSN Brochure - UnlockedDocument1 pageNSN Brochure - UnlockedGhostWheels SSSNo ratings yet

- Notes: Introduction To Networking Monitoring and ManagementDocument12 pagesNotes: Introduction To Networking Monitoring and ManagementDevendra ChandoraNo ratings yet

- KAN Guide To MeasurementDocument23 pagesKAN Guide To MeasurementYuni AntoNo ratings yet

- CAMEL Feature1Document34 pagesCAMEL Feature1elson brito junior100% (1)

- Moto E4 Plus ManualDocument38 pagesMoto E4 Plus ManualElizabeth AllenNo ratings yet

- Occlusense Product Review Formatted Version Rev 3Document31 pagesOcclusense Product Review Formatted Version Rev 3Christian NguyễnNo ratings yet

- Nader Asfour 01-2022Document2 pagesNader Asfour 01-2022SAlmaa NANo ratings yet

- Modul Asymmetric EncryptionDocument1 pageModul Asymmetric EncryptionAnggri YulioNo ratings yet

- CRM Template: (Your Name)Document10 pagesCRM Template: (Your Name)Mustafa Ricky Pramana SeNo ratings yet

- SPThreads 3 MutexDocument37 pagesSPThreads 3 Mutexloopnumber2020No ratings yet

- Qy 2004aDocument1 pageQy 2004aLuis MiguelNo ratings yet

- Career Objective: Educational QualificationsDocument3 pagesCareer Objective: Educational Qualificationsmikesoni SNo ratings yet

- 3.6.1 Packet Tracer Implement Vlans and TrunkingDocument2 pages3.6.1 Packet Tracer Implement Vlans and TrunkingJohn FrinkNo ratings yet

- NetacadDocument24 pagesNetacadKaye CariñoNo ratings yet

- Deep Quant Finance BrochureDocument21 pagesDeep Quant Finance Brochureसंजीव कुमार झाNo ratings yet

- MSDN Magazine 11-03Document102 pagesMSDN Magazine 11-03Scri BdNo ratings yet

- 24v-Catalogue ASP 24v 17 e 012019 Ansicht ReduziertDocument116 pages24v-Catalogue ASP 24v 17 e 012019 Ansicht ReduzierturlatiNo ratings yet