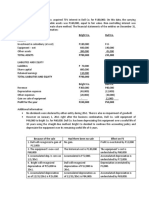

PROBLEM 7 Solution AFAR1 - Donggo

PROBLEM 7 Solution AFAR1 - Donggo

You might also like

- Answers - Activity 2.4 2.5 and 3.1Document38 pagesAnswers - Activity 2.4 2.5 and 3.1Tine Vasiana Duerme83% (6)

- Valuing Stocks The Warren Buffett WayDocument10 pagesValuing Stocks The Warren Buffett WaybogatishankarNo ratings yet

- Partnership Liquidation. Alynna Joy P. IbanezDocument32 pagesPartnership Liquidation. Alynna Joy P. IbanezAllynna Joy83% (6)

- Dividend and BondsDocument3 pagesDividend and BondsJanuary Ann Bete100% (1)

- Davaoeños' Culture and Traditions: Created By: Desiree AdanzaDocument16 pagesDavaoeños' Culture and Traditions: Created By: Desiree AdanzaArj Sulit Centino Daqui100% (4)

- Case Study - Corp Finance - Padgett Paper ProductsDocument26 pagesCase Study - Corp Finance - Padgett Paper ProductsJed Estanislao100% (1)

- Chapter 3 MCQ Afar 2 CompressDocument73 pagesChapter 3 MCQ Afar 2 Compresstaehyung kimNo ratings yet

- Estate Tax Sample Problems 2Document7 pagesEstate Tax Sample Problems 2Arj Sulit Centino Daqui0% (1)

- Chapter 18 CompilationDocument21 pagesChapter 18 CompilationMaria Licuanan0% (1)

- B.) CC, P25,000: PP, P21,000 Aa, P38,000Document22 pagesB.) CC, P25,000: PP, P21,000 Aa, P38,000Wendelyn TutorNo ratings yet

- Problem 7-15 Part ADocument7 pagesProblem 7-15 Part AImelda100% (1)

- DIFFICULTDocument7 pagesDIFFICULTQueen ValleNo ratings yet

- Dayag BusinessCombDocument3 pagesDayag BusinessCombtaherehNo ratings yet

- Equity Method (First Year of Acquisition)Document3 pagesEquity Method (First Year of Acquisition)Angel Chane OstrazNo ratings yet

- ConsolidationDocument91 pagesConsolidationKNVS Siva KumarNo ratings yet

- AFAR8717 Joint Arrangement SolutionsDocument2 pagesAFAR8717 Joint Arrangement SolutionsGJames ApostolNo ratings yet

- Part 2 Joint Arrangements Class Consultation PDFDocument6 pagesPart 2 Joint Arrangements Class Consultation PDFidk520055No ratings yet

- C.4 SOLUTIONS (Problems I - VIII)Document55 pagesC.4 SOLUTIONS (Problems I - VIII)Bianca AcoymoNo ratings yet

- Chapter 3 Problem I - Cost MethodDocument5 pagesChapter 3 Problem I - Cost MethodJIL Masapang Victoria ChapterNo ratings yet

- GEN4Document7 pagesGEN4Mylene HeragaNo ratings yet

- C.5 SOLUTIONS (Problems I - XV)Document59 pagesC.5 SOLUTIONS (Problems I - XV)Bianca AcoymoNo ratings yet

- Student Number: 201913610: A. Consolidated Retained EarningsDocument11 pagesStudent Number: 201913610: A. Consolidated Retained Earningsjayjay storageNo ratings yet

- Chapter-14 Intermediate AccountingDocument26 pagesChapter-14 Intermediate AccountingDanica Mae GenaviaNo ratings yet

- Calvo, Jhoanne C.-BSA 2-1-Chapter 4-Problem 11-20Document12 pagesCalvo, Jhoanne C.-BSA 2-1-Chapter 4-Problem 11-20Jhoanne CalvoNo ratings yet

- Solution Chapter 3 Rev FinalDocument82 pagesSolution Chapter 3 Rev FinalDieter LudwigNo ratings yet

- IAS 28 Sol. Man.Document27 pagesIAS 28 Sol. Man.asher phoenixNo ratings yet

- RESA MCQsDocument56 pagesRESA MCQsWendelyn Tutor100% (1)

- Chapter 3 - Problem IDocument23 pagesChapter 3 - Problem IRoldan Arca PagaposNo ratings yet

- Intermediate Accounting Chapter 17 and 18Document9 pagesIntermediate Accounting Chapter 17 and 18avilastephjaneNo ratings yet

- c3 AnswersDocument66 pagesc3 AnswersRuiz, CherryjaneNo ratings yet

- Chapter18 BuenaventuraDocument6 pagesChapter18 BuenaventuraAnonnNo ratings yet

- Some Advac Problems by DayagDocument6 pagesSome Advac Problems by DayagElijah Montefalco100% (1)

- Quiz Chapter 4 Consol. Fs Part 1Document7 pagesQuiz Chapter 4 Consol. Fs Part 1Avril Denise NavarroNo ratings yet

- Bright Co. Dull Co. AssetsDocument5 pagesBright Co. Dull Co. AssetsJJ JaumNo ratings yet

- Solman Chapter 3Document6 pagesSolman Chapter 3Kyla RoxasNo ratings yet

- SOLMAN CHAPTER 14 INVESTMENTS IN ASSOCIATES - IA PART 1B - 2020edDocument27 pagesSOLMAN CHAPTER 14 INVESTMENTS IN ASSOCIATES - IA PART 1B - 2020edMeeka CalimagNo ratings yet

- Consolidation Q76Document4 pagesConsolidation Q76johny SahaNo ratings yet

- FR Mock Exam 4 - SolutionsDocument13 pagesFR Mock Exam 4 - Solutionsiram2005No ratings yet

- Problem I Cost ModelDocument76 pagesProblem I Cost ModelSia DLSLNo ratings yet

- Act2 1Document6 pagesAct2 1Kath LeynesNo ratings yet

- Multiple Choice ACCSTDocument5 pagesMultiple Choice ACCSTJaene L.No ratings yet

- Cost Model Skeletal Approach Ans KeysDocument4 pagesCost Model Skeletal Approach Ans KeysMelvin BagasinNo ratings yet

- Solution Chapter 5 Rev FinalDocument84 pagesSolution Chapter 5 Rev FinalMiya Crizxen RevibesNo ratings yet

- ASSIGNMENT#2Document5 pagesASSIGNMENT#2Kristine Esplana ToraldeNo ratings yet

- Assignment#2Document5 pagesAssignment#2Kristine Esplana ToraldeNo ratings yet

- Intercompany Sale of Fixed AssetsDocument5 pagesIntercompany Sale of Fixed AssetsasdasdaNo ratings yet

- CMPC 131 SolutionsDocument3 pagesCMPC 131 SolutionsNhel AlvaroNo ratings yet

- AFAR-01A (Supplemental Material To Partnership Accounting)Document2 pagesAFAR-01A (Supplemental Material To Partnership Accounting)Maricris AlilinNo ratings yet

- p1 Quiz With TheoryDocument16 pagesp1 Quiz With TheoryRica RegorisNo ratings yet

- Ppe ProblemDocument3 pagesPpe ProblemJanuary Ann BeteNo ratings yet

- 07 Quiz 1 - SCMDocument1 page07 Quiz 1 - SCMJen DeloyNo ratings yet

- Cost and Equity MethodDocument11 pagesCost and Equity MethoddmangiginNo ratings yet

- Total P450,000Document20 pagesTotal P450,000Love FreddyNo ratings yet

- Problem 1: Answer and SolutionDocument2 pagesProblem 1: Answer and SolutionMitch Tokong MinglanaNo ratings yet

- Strategic Cost ManagementDocument7 pagesStrategic Cost ManagementAngeline RamirezNo ratings yet

- Multiple Choices - ComputationalDocument25 pagesMultiple Choices - ComputationalShenna Mae MateoNo ratings yet

- Business Com ActivityDocument2 pagesBusiness Com ActivityAlyssa AnnNo ratings yet

- p1 Quiz With TheoryDocument15 pagesp1 Quiz With TheoryGrace CorpoNo ratings yet

- Investment in AssociateDocument7 pagesInvestment in AssociatenenzzmariaNo ratings yet

- Consolidated Net Income For 20x5Document13 pagesConsolidated Net Income For 20x5Ryan PatitoNo ratings yet

- Profe03 Activity Chapter 7Document5 pagesProfe03 Activity Chapter 7eloisa celisNo ratings yet

- Quiz 2 AnswersDocument7 pagesQuiz 2 AnswersAlyssa CasimiroNo ratings yet

- Financial Statement Analysis - Illustrative Problem - FOR STUDENTSDocument6 pagesFinancial Statement Analysis - Illustrative Problem - FOR STUDENTShobi stanNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Module 1 ESTATE TAXATIONDocument7 pagesModule 1 ESTATE TAXATIONArj Sulit Centino DaquiNo ratings yet

- Total Quality ManagementDocument13 pagesTotal Quality ManagementArj Sulit Centino DaquiNo ratings yet

- Quiz Partnership 1Document2 pagesQuiz Partnership 1Arj Sulit Centino DaquiNo ratings yet

- Auditing Agricultural Industries - Prelim ReportDocument78 pagesAuditing Agricultural Industries - Prelim ReportArj Sulit Centino DaquiNo ratings yet

- Documentation On Custom ClearanceDocument8 pagesDocumentation On Custom ClearanceArj Sulit Centino DaquiNo ratings yet

- Reporting Sched For Midterms and FinalsDocument1 pageReporting Sched For Midterms and FinalsArj Sulit Centino DaquiNo ratings yet

- Pop Culture Midterm Assigned Report (Daque)Document13 pagesPop Culture Midterm Assigned Report (Daque)Arj Sulit Centino DaquiNo ratings yet

- Popular Culture in Zamboanga City: By: Vinz Patrick E. PerochoDocument15 pagesPopular Culture in Zamboanga City: By: Vinz Patrick E. PerochoArj Sulit Centino DaquiNo ratings yet

- The Culture of The PhilippinesDocument13 pagesThe Culture of The PhilippinesArj Sulit Centino DaquiNo ratings yet

- Statistical Analysis With Software Application Lesson 4Document2 pagesStatistical Analysis With Software Application Lesson 4Arj Sulit Centino DaquiNo ratings yet

- Statistical Analysis With Software Application Lesson 2Document2 pagesStatistical Analysis With Software Application Lesson 2Arj Sulit Centino DaquiNo ratings yet

- Multiple Choice QuestionsDocument6 pagesMultiple Choice QuestionsCandy DollNo ratings yet

- Tencent Holdings 0700.HK Compelling Risk-Reward With Echoes of 2018 Opportunity Buy With 73 UpsideDocument24 pagesTencent Holdings 0700.HK Compelling Risk-Reward With Echoes of 2018 Opportunity Buy With 73 UpsideweishingNo ratings yet

- FM PRRDocument6 pagesFM PRRMansi Kaushik XI -ENo ratings yet

- Chapter 6 SOPL-SOFP-FormatDocument3 pagesChapter 6 SOPL-SOFP-FormatShowenah ThiruNo ratings yet

- Reading 25 Non-Current (Long-Term) LiabilitiesDocument31 pagesReading 25 Non-Current (Long-Term) LiabilitiesNeerajNo ratings yet

- Fundamental Equity Analysis - S&P 100 Index Components (OEX Index)Document205 pagesFundamental Equity Analysis - S&P 100 Index Components (OEX Index)Q.M.S Advisors LLCNo ratings yet

- AFAR02 05 CORPORATE Liquidation HandoutDocument3 pagesAFAR02 05 CORPORATE Liquidation HandoutNicoleNo ratings yet

- FORM TP 2017101 Test Code 01239010 MAY/JUNE 2017: Paper 01 - General ProficiencyDocument14 pagesFORM TP 2017101 Test Code 01239010 MAY/JUNE 2017: Paper 01 - General ProficiencyChelsea BynoeNo ratings yet

- Sap Asset Depreciation: Author - Gobi SuppiahDocument7 pagesSap Asset Depreciation: Author - Gobi SuppiahAbdullahNo ratings yet

- Printing Company - Business Plan 2007Document22 pagesPrinting Company - Business Plan 2007EdgladNo ratings yet

- Degree of Financial Leverage Formula Excel TemplateDocument4 pagesDegree of Financial Leverage Formula Excel TemplateSyed Mursaleen ShahNo ratings yet

- Abuscom Journal EntriesDocument27 pagesAbuscom Journal EntriesMac b IBANEZNo ratings yet

- M&A PitchbookDocument32 pagesM&A PitchbookScott BeiersdorferNo ratings yet

- FAR 3MC The Conceptual Framework of Financial ReportingDocument4 pagesFAR 3MC The Conceptual Framework of Financial ReportingHassanhor Guro Bacolod100% (1)

- AFAR Theories Reviewer For CPALEDocument25 pagesAFAR Theories Reviewer For CPALEColeen CunananNo ratings yet

- Step AcquisitionDocument2 pagesStep AcquisitionJamaica DavidNo ratings yet

- Assertion SummaryDocument3 pagesAssertion SummaryAprile AnonuevoNo ratings yet

- Modern Advanced Accounting in Canada Canadian 8th Edition Hilton Herauf Solution ManualDocument29 pagesModern Advanced Accounting in Canada Canadian 8th Edition Hilton Herauf Solution Manualandrea100% (25)

- MCQs On Correlation and Regression AnalysisDocument15 pagesMCQs On Correlation and Regression AnalysiskapuNo ratings yet

- Assignment June 2022Document3 pagesAssignment June 2022AirForce ManNo ratings yet

- 12Document16 pages12JDNo ratings yet

- Financial Statement AssignmentDocument2 pagesFinancial Statement Assignmentseatow6No ratings yet

- Tugas Managerial AccountinDocument3 pagesTugas Managerial Accountinlaurentinus fikaNo ratings yet

- SY BCom - Advanced Accounting & Auditing - Paper-IIDocument2 pagesSY BCom - Advanced Accounting & Auditing - Paper-IINitasha GoyalNo ratings yet

- BTP - Predicting Fraudulent Financial Statement Using Cash Flow ShenanigansDocument14 pagesBTP - Predicting Fraudulent Financial Statement Using Cash Flow Shenaniganserfina istyaningrumNo ratings yet

- MMPC 4 em 2023 24Document22 pagesMMPC 4 em 2023 24Rajni KumariNo ratings yet

- Exercise No.3 (Acctg 7) - TanDocument2 pagesExercise No.3 (Acctg 7) - TanFaith Reyna TanNo ratings yet

- Consolidated Balance Sheet of Steel Authority of India (In Rs. Crores) Mar-17 Mar-16 Mar-15 Equity and Liabilities Shareholder'S FundDocument4 pagesConsolidated Balance Sheet of Steel Authority of India (In Rs. Crores) Mar-17 Mar-16 Mar-15 Equity and Liabilities Shareholder'S FundPuneet GeraNo ratings yet

Download as docx, pdf, or txt

You might also like

- Answers - Activity 2.4 2.5 and 3.1Document38 pagesAnswers - Activity 2.4 2.5 and 3.1Tine Vasiana Duerme83% (6)

- Valuing Stocks The Warren Buffett WayDocument10 pagesValuing Stocks The Warren Buffett WaybogatishankarNo ratings yet

- Partnership Liquidation. Alynna Joy P. IbanezDocument32 pagesPartnership Liquidation. Alynna Joy P. IbanezAllynna Joy83% (6)

- Dividend and BondsDocument3 pagesDividend and BondsJanuary Ann Bete100% (1)

- Davaoeños' Culture and Traditions: Created By: Desiree AdanzaDocument16 pagesDavaoeños' Culture and Traditions: Created By: Desiree AdanzaArj Sulit Centino Daqui100% (4)

- Case Study - Corp Finance - Padgett Paper ProductsDocument26 pagesCase Study - Corp Finance - Padgett Paper ProductsJed Estanislao100% (1)

- Chapter 3 MCQ Afar 2 CompressDocument73 pagesChapter 3 MCQ Afar 2 Compresstaehyung kimNo ratings yet

- Estate Tax Sample Problems 2Document7 pagesEstate Tax Sample Problems 2Arj Sulit Centino Daqui0% (1)

- Chapter 18 CompilationDocument21 pagesChapter 18 CompilationMaria Licuanan0% (1)

- B.) CC, P25,000: PP, P21,000 Aa, P38,000Document22 pagesB.) CC, P25,000: PP, P21,000 Aa, P38,000Wendelyn TutorNo ratings yet

- Problem 7-15 Part ADocument7 pagesProblem 7-15 Part AImelda100% (1)

- DIFFICULTDocument7 pagesDIFFICULTQueen ValleNo ratings yet

- Dayag BusinessCombDocument3 pagesDayag BusinessCombtaherehNo ratings yet

- Equity Method (First Year of Acquisition)Document3 pagesEquity Method (First Year of Acquisition)Angel Chane OstrazNo ratings yet

- ConsolidationDocument91 pagesConsolidationKNVS Siva KumarNo ratings yet

- AFAR8717 Joint Arrangement SolutionsDocument2 pagesAFAR8717 Joint Arrangement SolutionsGJames ApostolNo ratings yet

- Part 2 Joint Arrangements Class Consultation PDFDocument6 pagesPart 2 Joint Arrangements Class Consultation PDFidk520055No ratings yet

- C.4 SOLUTIONS (Problems I - VIII)Document55 pagesC.4 SOLUTIONS (Problems I - VIII)Bianca AcoymoNo ratings yet

- Chapter 3 Problem I - Cost MethodDocument5 pagesChapter 3 Problem I - Cost MethodJIL Masapang Victoria ChapterNo ratings yet

- GEN4Document7 pagesGEN4Mylene HeragaNo ratings yet

- C.5 SOLUTIONS (Problems I - XV)Document59 pagesC.5 SOLUTIONS (Problems I - XV)Bianca AcoymoNo ratings yet

- Student Number: 201913610: A. Consolidated Retained EarningsDocument11 pagesStudent Number: 201913610: A. Consolidated Retained Earningsjayjay storageNo ratings yet

- Chapter-14 Intermediate AccountingDocument26 pagesChapter-14 Intermediate AccountingDanica Mae GenaviaNo ratings yet

- Calvo, Jhoanne C.-BSA 2-1-Chapter 4-Problem 11-20Document12 pagesCalvo, Jhoanne C.-BSA 2-1-Chapter 4-Problem 11-20Jhoanne CalvoNo ratings yet

- Solution Chapter 3 Rev FinalDocument82 pagesSolution Chapter 3 Rev FinalDieter LudwigNo ratings yet

- IAS 28 Sol. Man.Document27 pagesIAS 28 Sol. Man.asher phoenixNo ratings yet

- RESA MCQsDocument56 pagesRESA MCQsWendelyn Tutor100% (1)

- Chapter 3 - Problem IDocument23 pagesChapter 3 - Problem IRoldan Arca PagaposNo ratings yet

- Intermediate Accounting Chapter 17 and 18Document9 pagesIntermediate Accounting Chapter 17 and 18avilastephjaneNo ratings yet

- c3 AnswersDocument66 pagesc3 AnswersRuiz, CherryjaneNo ratings yet

- Chapter18 BuenaventuraDocument6 pagesChapter18 BuenaventuraAnonnNo ratings yet

- Some Advac Problems by DayagDocument6 pagesSome Advac Problems by DayagElijah Montefalco100% (1)

- Quiz Chapter 4 Consol. Fs Part 1Document7 pagesQuiz Chapter 4 Consol. Fs Part 1Avril Denise NavarroNo ratings yet

- Bright Co. Dull Co. AssetsDocument5 pagesBright Co. Dull Co. AssetsJJ JaumNo ratings yet

- Solman Chapter 3Document6 pagesSolman Chapter 3Kyla RoxasNo ratings yet

- SOLMAN CHAPTER 14 INVESTMENTS IN ASSOCIATES - IA PART 1B - 2020edDocument27 pagesSOLMAN CHAPTER 14 INVESTMENTS IN ASSOCIATES - IA PART 1B - 2020edMeeka CalimagNo ratings yet

- Consolidation Q76Document4 pagesConsolidation Q76johny SahaNo ratings yet

- FR Mock Exam 4 - SolutionsDocument13 pagesFR Mock Exam 4 - Solutionsiram2005No ratings yet

- Problem I Cost ModelDocument76 pagesProblem I Cost ModelSia DLSLNo ratings yet

- Act2 1Document6 pagesAct2 1Kath LeynesNo ratings yet

- Multiple Choice ACCSTDocument5 pagesMultiple Choice ACCSTJaene L.No ratings yet

- Cost Model Skeletal Approach Ans KeysDocument4 pagesCost Model Skeletal Approach Ans KeysMelvin BagasinNo ratings yet

- Solution Chapter 5 Rev FinalDocument84 pagesSolution Chapter 5 Rev FinalMiya Crizxen RevibesNo ratings yet

- ASSIGNMENT#2Document5 pagesASSIGNMENT#2Kristine Esplana ToraldeNo ratings yet

- Assignment#2Document5 pagesAssignment#2Kristine Esplana ToraldeNo ratings yet

- Intercompany Sale of Fixed AssetsDocument5 pagesIntercompany Sale of Fixed AssetsasdasdaNo ratings yet

- CMPC 131 SolutionsDocument3 pagesCMPC 131 SolutionsNhel AlvaroNo ratings yet

- AFAR-01A (Supplemental Material To Partnership Accounting)Document2 pagesAFAR-01A (Supplemental Material To Partnership Accounting)Maricris AlilinNo ratings yet

- p1 Quiz With TheoryDocument16 pagesp1 Quiz With TheoryRica RegorisNo ratings yet

- Ppe ProblemDocument3 pagesPpe ProblemJanuary Ann BeteNo ratings yet

- 07 Quiz 1 - SCMDocument1 page07 Quiz 1 - SCMJen DeloyNo ratings yet

- Cost and Equity MethodDocument11 pagesCost and Equity MethoddmangiginNo ratings yet

- Total P450,000Document20 pagesTotal P450,000Love FreddyNo ratings yet

- Problem 1: Answer and SolutionDocument2 pagesProblem 1: Answer and SolutionMitch Tokong MinglanaNo ratings yet

- Strategic Cost ManagementDocument7 pagesStrategic Cost ManagementAngeline RamirezNo ratings yet

- Multiple Choices - ComputationalDocument25 pagesMultiple Choices - ComputationalShenna Mae MateoNo ratings yet

- Business Com ActivityDocument2 pagesBusiness Com ActivityAlyssa AnnNo ratings yet

- p1 Quiz With TheoryDocument15 pagesp1 Quiz With TheoryGrace CorpoNo ratings yet

- Investment in AssociateDocument7 pagesInvestment in AssociatenenzzmariaNo ratings yet

- Consolidated Net Income For 20x5Document13 pagesConsolidated Net Income For 20x5Ryan PatitoNo ratings yet

- Profe03 Activity Chapter 7Document5 pagesProfe03 Activity Chapter 7eloisa celisNo ratings yet

- Quiz 2 AnswersDocument7 pagesQuiz 2 AnswersAlyssa CasimiroNo ratings yet

- Financial Statement Analysis - Illustrative Problem - FOR STUDENTSDocument6 pagesFinancial Statement Analysis - Illustrative Problem - FOR STUDENTShobi stanNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Module 1 ESTATE TAXATIONDocument7 pagesModule 1 ESTATE TAXATIONArj Sulit Centino DaquiNo ratings yet

- Total Quality ManagementDocument13 pagesTotal Quality ManagementArj Sulit Centino DaquiNo ratings yet

- Quiz Partnership 1Document2 pagesQuiz Partnership 1Arj Sulit Centino DaquiNo ratings yet

- Auditing Agricultural Industries - Prelim ReportDocument78 pagesAuditing Agricultural Industries - Prelim ReportArj Sulit Centino DaquiNo ratings yet

- Documentation On Custom ClearanceDocument8 pagesDocumentation On Custom ClearanceArj Sulit Centino DaquiNo ratings yet

- Reporting Sched For Midterms and FinalsDocument1 pageReporting Sched For Midterms and FinalsArj Sulit Centino DaquiNo ratings yet

- Pop Culture Midterm Assigned Report (Daque)Document13 pagesPop Culture Midterm Assigned Report (Daque)Arj Sulit Centino DaquiNo ratings yet

- Popular Culture in Zamboanga City: By: Vinz Patrick E. PerochoDocument15 pagesPopular Culture in Zamboanga City: By: Vinz Patrick E. PerochoArj Sulit Centino DaquiNo ratings yet

- The Culture of The PhilippinesDocument13 pagesThe Culture of The PhilippinesArj Sulit Centino DaquiNo ratings yet

- Statistical Analysis With Software Application Lesson 4Document2 pagesStatistical Analysis With Software Application Lesson 4Arj Sulit Centino DaquiNo ratings yet

- Statistical Analysis With Software Application Lesson 2Document2 pagesStatistical Analysis With Software Application Lesson 2Arj Sulit Centino DaquiNo ratings yet

- Multiple Choice QuestionsDocument6 pagesMultiple Choice QuestionsCandy DollNo ratings yet

- Tencent Holdings 0700.HK Compelling Risk-Reward With Echoes of 2018 Opportunity Buy With 73 UpsideDocument24 pagesTencent Holdings 0700.HK Compelling Risk-Reward With Echoes of 2018 Opportunity Buy With 73 UpsideweishingNo ratings yet

- FM PRRDocument6 pagesFM PRRMansi Kaushik XI -ENo ratings yet

- Chapter 6 SOPL-SOFP-FormatDocument3 pagesChapter 6 SOPL-SOFP-FormatShowenah ThiruNo ratings yet

- Reading 25 Non-Current (Long-Term) LiabilitiesDocument31 pagesReading 25 Non-Current (Long-Term) LiabilitiesNeerajNo ratings yet

- Fundamental Equity Analysis - S&P 100 Index Components (OEX Index)Document205 pagesFundamental Equity Analysis - S&P 100 Index Components (OEX Index)Q.M.S Advisors LLCNo ratings yet

- AFAR02 05 CORPORATE Liquidation HandoutDocument3 pagesAFAR02 05 CORPORATE Liquidation HandoutNicoleNo ratings yet

- FORM TP 2017101 Test Code 01239010 MAY/JUNE 2017: Paper 01 - General ProficiencyDocument14 pagesFORM TP 2017101 Test Code 01239010 MAY/JUNE 2017: Paper 01 - General ProficiencyChelsea BynoeNo ratings yet

- Sap Asset Depreciation: Author - Gobi SuppiahDocument7 pagesSap Asset Depreciation: Author - Gobi SuppiahAbdullahNo ratings yet

- Printing Company - Business Plan 2007Document22 pagesPrinting Company - Business Plan 2007EdgladNo ratings yet

- Degree of Financial Leverage Formula Excel TemplateDocument4 pagesDegree of Financial Leverage Formula Excel TemplateSyed Mursaleen ShahNo ratings yet

- Abuscom Journal EntriesDocument27 pagesAbuscom Journal EntriesMac b IBANEZNo ratings yet

- M&A PitchbookDocument32 pagesM&A PitchbookScott BeiersdorferNo ratings yet

- FAR 3MC The Conceptual Framework of Financial ReportingDocument4 pagesFAR 3MC The Conceptual Framework of Financial ReportingHassanhor Guro Bacolod100% (1)

- AFAR Theories Reviewer For CPALEDocument25 pagesAFAR Theories Reviewer For CPALEColeen CunananNo ratings yet

- Step AcquisitionDocument2 pagesStep AcquisitionJamaica DavidNo ratings yet

- Assertion SummaryDocument3 pagesAssertion SummaryAprile AnonuevoNo ratings yet

- Modern Advanced Accounting in Canada Canadian 8th Edition Hilton Herauf Solution ManualDocument29 pagesModern Advanced Accounting in Canada Canadian 8th Edition Hilton Herauf Solution Manualandrea100% (25)

- MCQs On Correlation and Regression AnalysisDocument15 pagesMCQs On Correlation and Regression AnalysiskapuNo ratings yet

- Assignment June 2022Document3 pagesAssignment June 2022AirForce ManNo ratings yet

- 12Document16 pages12JDNo ratings yet

- Financial Statement AssignmentDocument2 pagesFinancial Statement Assignmentseatow6No ratings yet

- Tugas Managerial AccountinDocument3 pagesTugas Managerial Accountinlaurentinus fikaNo ratings yet

- SY BCom - Advanced Accounting & Auditing - Paper-IIDocument2 pagesSY BCom - Advanced Accounting & Auditing - Paper-IINitasha GoyalNo ratings yet

- BTP - Predicting Fraudulent Financial Statement Using Cash Flow ShenanigansDocument14 pagesBTP - Predicting Fraudulent Financial Statement Using Cash Flow Shenaniganserfina istyaningrumNo ratings yet

- MMPC 4 em 2023 24Document22 pagesMMPC 4 em 2023 24Rajni KumariNo ratings yet

- Exercise No.3 (Acctg 7) - TanDocument2 pagesExercise No.3 (Acctg 7) - TanFaith Reyna TanNo ratings yet

- Consolidated Balance Sheet of Steel Authority of India (In Rs. Crores) Mar-17 Mar-16 Mar-15 Equity and Liabilities Shareholder'S FundDocument4 pagesConsolidated Balance Sheet of Steel Authority of India (In Rs. Crores) Mar-17 Mar-16 Mar-15 Equity and Liabilities Shareholder'S FundPuneet GeraNo ratings yet