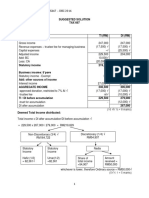

Solution Tax667 - Dec 2016

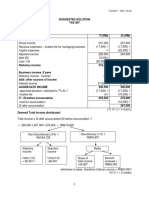

Solution Tax667 - Dec 2016

You might also like

- MICPA at Full Set Note USEDocument61 pagesMICPA at Full Set Note USEHafiz Musannef100% (1)

- Suggested Solution Far 660 Final Exam JUNE 2019Document6 pagesSuggested Solution Far 660 Final Exam JUNE 2019Nur ShahiraNo ratings yet

- Chapter 4Document45 pagesChapter 4Yanjing Liu67% (3)

- Chapter - 8 Management of ReceivablesDocument6 pagesChapter - 8 Management of ReceivablesadhishcaNo ratings yet

- PS2Document18 pagesPS2Thanh NguyenNo ratings yet

- Solution Test 1Document3 pagesSolution Test 1anis izzatiNo ratings yet

- Dec 2014Document2 pagesDec 2014Zahiratul QamarinaNo ratings yet

- ABC and XYZ - AnswerDocument6 pagesABC and XYZ - AnswerMohammad El HajjNo ratings yet

- Chapter2 Premium LiabilitiesDocument23 pagesChapter2 Premium LiabilitiesReighjon Ashley C. TolentinoNo ratings yet

- House ProDocument7 pagesHouse Prosb_jainNo ratings yet

- Common Test Aud 689 Answer All Questions Time: 1 Hour 45 MinutesDocument8 pagesCommon Test Aud 689 Answer All Questions Time: 1 Hour 45 MinutesNur Dina AbsbNo ratings yet

- Arens Chapter20Document105 pagesArens Chapter20rochielanciolaNo ratings yet

- MBA 504 Ch5 SolutionsDocument12 pagesMBA 504 Ch5 SolutionspheeyonaNo ratings yet

- Income From House Property PracticalDocument52 pagesIncome From House Property PracticalShreekanta DattaNo ratings yet

- Cost II Chapter ThreeDocument11 pagesCost II Chapter ThreeSemira100% (1)

- Chapter 4 Solutions: A) Explain The FollowingDocument23 pagesChapter 4 Solutions: A) Explain The FollowingAdebayo Yusuff AdesholaNo ratings yet

- PVC Analysis QNDocument14 pagesPVC Analysis QNAnipa HubertNo ratings yet

- ACC406 - Chapter - 13 - Relevant - Costing - IIDocument20 pagesACC406 - Chapter - 13 - Relevant - Costing - IIkaylatolentino4No ratings yet

- Chap 24 - Investment in Associate - Basic Principle Fin Acct 1 - Barter Summary Team PDFDocument5 pagesChap 24 - Investment in Associate - Basic Principle Fin Acct 1 - Barter Summary Team PDFSuper JhedNo ratings yet

- 9 Trade CreditDocument13 pages9 Trade CreditMohammad DwidarNo ratings yet

- 1a. Investment in Associate - LectureDocument14 pages1a. Investment in Associate - Lecturekyle GipulanNo ratings yet

- Provision Contingency Liabilities and CoDocument16 pagesProvision Contingency Liabilities and CoPipz G. Castro100% (1)

- Theory of Accounts L. R. Cabarles Toa.112 - Impairment of Assets Lecture NotesDocument5 pagesTheory of Accounts L. R. Cabarles Toa.112 - Impairment of Assets Lecture NotesPia DagmanNo ratings yet

- Lesson 4-Quantitative TechniquesDocument7 pagesLesson 4-Quantitative TechniquesLuiNo ratings yet

- Pfrs 2 Share-Based PaymentsDocument3 pagesPfrs 2 Share-Based PaymentsR.A.No ratings yet

- Tax Q&A - Income From Investment and Other SourcesDocument3 pagesTax Q&A - Income From Investment and Other SourcesHadifliNo ratings yet

- Chapter # 8 Exercise & Problems - AnswersDocument8 pagesChapter # 8 Exercise & Problems - AnswersZia UddinNo ratings yet

- Corporate Finance Model AnswerDocument3 pagesCorporate Finance Model AnswersrikanthNo ratings yet

- The Cost of Trade CreditDocument4 pagesThe Cost of Trade CreditWawex DavisNo ratings yet

- Practice Questions and Concepts of The Balanced ScorecardDocument8 pagesPractice Questions and Concepts of The Balanced ScorecardJuan Dela Cruz IIINo ratings yet

- Tutorial 5 - Marginal and Absorption Costing QuestionsDocument3 pagesTutorial 5 - Marginal and Absorption Costing QuestionsAnonymous 9GgsGYEf100% (1)

- Chapter Two-Accounting For InventoryDocument25 pagesChapter Two-Accounting For Inventoryzewdie100% (1)

- Receivable ManagementDocument40 pagesReceivable ManagementrenudhingraNo ratings yet

- Income Tax Guide UgandaDocument13 pagesIncome Tax Guide UgandaMoses LubangakeneNo ratings yet

- ZBB Vs ABB Traditional BudgetingDocument4 pagesZBB Vs ABB Traditional BudgetingAbhijeet KendoleNo ratings yet

- Diploma in Business Administration (Diba) BM 321 - Financial Accounting Assignment - 20%Document1 pageDiploma in Business Administration (Diba) BM 321 - Financial Accounting Assignment - 20%ranjinikpNo ratings yet

- ENCANA Corporation: The Cost of Capital: Weight of Debt Rate of Debt Tax Weight of Equity Rate of EquityDocument3 pagesENCANA Corporation: The Cost of Capital: Weight of Debt Rate of Debt Tax Weight of Equity Rate of EquityVamsi GunturuNo ratings yet

- 11 35Document8 pages11 35Wildan IrfansyahNo ratings yet

- Wacc Mini CaseDocument12 pagesWacc Mini CaseKishore NaiduNo ratings yet

- Table of Specifications Management Advisory Services: Remembering Understanding Application Analyzing Evaluating CreatingDocument25 pagesTable of Specifications Management Advisory Services: Remembering Understanding Application Analyzing Evaluating CreatingJoshua JoshNo ratings yet

- Tailieumienphi - VN Lecture Logistics Theory Lecture 16 Material Requirements PlanningDocument21 pagesTailieumienphi - VN Lecture Logistics Theory Lecture 16 Material Requirements PlanningBong ThoNo ratings yet

- Chapter 1 Cash and Cash Equivalent - REVIEWERDocument32 pagesChapter 1 Cash and Cash Equivalent - REVIEWERAiyana AlaniNo ratings yet

- Chapter 6 - Business StrategyDocument5 pagesChapter 6 - Business StrategySteffany RoqueNo ratings yet

- MFRS 101 - Ig - 042015Document24 pagesMFRS 101 - Ig - 042015Prasen RajNo ratings yet

- Fair Value Adjustment and Consolidation Adjustment Week 2Document9 pagesFair Value Adjustment and Consolidation Adjustment Week 2Omolaja IbukunNo ratings yet

- Test Aud 689 - Apr 2018Document3 pagesTest Aud 689 - Apr 2018Nur Dina AbsbNo ratings yet

- Accounting For RoyaltiesDocument19 pagesAccounting For RoyaltieskwameNo ratings yet

- Chapter 13 - CashFlow - STUDENTSDocument5 pagesChapter 13 - CashFlow - STUDENTSCalvin Fishy SuNo ratings yet

- Agan Interior Design - ExerciseDocument2 pagesAgan Interior Design - ExerciseLouieNo ratings yet

- Activity-Based Costing: A Tool To Aid Decision MakingDocument75 pagesActivity-Based Costing: A Tool To Aid Decision MakingNavleen Kaur100% (1)

- Ch07 Compound Financial InstrumentDocument5 pagesCh07 Compound Financial InstrumentJessica AllyNo ratings yet

- Solution Far560 - Jun 2015 (S)Document7 pagesSolution Far560 - Jun 2015 (S)MUHAMAD MUKHAIRI MUHAMAD HANIFAHNo ratings yet

- Cost Volume Profit Analysis Review NotesDocument17 pagesCost Volume Profit Analysis Review NotesAlexis Kaye DayagNo ratings yet

- BBS 1st Year QuestionDocument2 pagesBBS 1st Year Questionsatya100% (1)

- Factoring ServicingDocument25 pagesFactoring ServicingTanya JaliNo ratings yet

- Tutorial 2 Capital Allowances - Q&ADocument8 pagesTutorial 2 Capital Allowances - Q&AKamal JabriNo ratings yet

- Cash Flow and Fund Flow StatementDocument23 pagesCash Flow and Fund Flow StatementRishul BhasinNo ratings yet

- Solution Tax667 - Dec 2016Document7 pagesSolution Tax667 - Dec 2016Zahiratul QamarinaNo ratings yet

- Suggested Answers TAX667 - DEC 2016Document7 pagesSuggested Answers TAX667 - DEC 2016diysNo ratings yet

- Solution Tax667 - Jun 2018Document9 pagesSolution Tax667 - Jun 2018Aiyani NabihahNo ratings yet

- Solution Test 2 (1) June 19Document5 pagesSolution Test 2 (1) June 19Nur Dina AbsbNo ratings yet

- Tybms - International MarketingDocument22 pagesTybms - International MarketingRithik ThakurNo ratings yet

- Handout CHE F343Document3 pagesHandout CHE F343Aryan ShuklaNo ratings yet

- Akshit Goyal 2020060472: Unit 2 ExercisesDocument5 pagesAkshit Goyal 2020060472: Unit 2 ExercisesAkshit GoyalNo ratings yet

- The Foreign Exchange MarketDocument33 pagesThe Foreign Exchange MarketShantanu ChoudhuryNo ratings yet

- TATA Family TreeDocument1 pageTATA Family Treemehulchauhan_9950% (2)

- GRADE 9 Ems ExamDocument10 pagesGRADE 9 Ems ExamZam100% (1)

- Mdra0101 443864197Document2 pagesMdra0101 443864197DavidNo ratings yet

- QuestalltDocument9 pagesQuestalltSubin chhatriaNo ratings yet

- Philippineusa 140219175321 Phpapp01Document32 pagesPhilippineusa 140219175321 Phpapp01BJ AmbatNo ratings yet

- Ratio Analysis of Vardhman TextileDocument46 pagesRatio Analysis of Vardhman TextileAjit Sharma100% (1)

- RBI Grade B 28 May 2022 Memory Based Paper (English)Document22 pagesRBI Grade B 28 May 2022 Memory Based Paper (English)VinayRajNo ratings yet

- State of Digital Adoption in Construction 2024Document48 pagesState of Digital Adoption in Construction 2024drafteramdNo ratings yet

- Company Name Exchange:Ticker Watch Lists Ount Raised ($usdmm, Today'S Rate)Document953 pagesCompany Name Exchange:Ticker Watch Lists Ount Raised ($usdmm, Today'S Rate)Keval KatrodiyaNo ratings yet

- IMF 2020 Well SpentDocument341 pagesIMF 2020 Well SpentLuchi RussoNo ratings yet

- Grade 7 Tech Memo June 2019 1Document3 pagesGrade 7 Tech Memo June 2019 1emmanuelmutemba919No ratings yet

- Law New Syllabus Compiled QuestionsDocument98 pagesLaw New Syllabus Compiled Questionsenila upretiNo ratings yet

- Kaplan-M1 Ch2 PDocument22 pagesKaplan-M1 Ch2 PinbyNo ratings yet

- MODULE 16 Share-Based PaymentDocument8 pagesMODULE 16 Share-Based PaymentJanelleNo ratings yet

- Pas 1: Presentation of Financial StatementsDocument16 pagesPas 1: Presentation of Financial StatementsKryzzel Anne JonNo ratings yet

- Official Journal C48: of The European UnionDocument5 pagesOfficial Journal C48: of The European UnionDaiuk.DakNo ratings yet

- Housing Loan Management: A Study of Kuc Bank LTD.: Kshitija Sawant, Shrikrishna MahajanDocument6 pagesHousing Loan Management: A Study of Kuc Bank LTD.: Kshitija Sawant, Shrikrishna MahajanGoogle WebNo ratings yet

- Basics of Accounting: By: Dr. Bhupendra Singh HadaDocument84 pagesBasics of Accounting: By: Dr. Bhupendra Singh HadaAryanSinghNo ratings yet

- 2002 Sing J Legal Stud 455Document35 pages2002 Sing J Legal Stud 455me elkNo ratings yet

- Lecture 11&12 Statement of Cash Flows - NUS ACC1002 2020 SpringDocument57 pagesLecture 11&12 Statement of Cash Flows - NUS ACC1002 2020 SpringZenyuiNo ratings yet

- MCQ-Business-Management (2 Files Merged)Document47 pagesMCQ-Business-Management (2 Files Merged)Sakthivel PoovanNo ratings yet

- Mission VisionmmDocument11 pagesMission VisionmmHumayra SalsabilNo ratings yet

- Valuing Common Stocks: Chapter 7 Tool Kit For Stock ValuationDocument20 pagesValuing Common Stocks: Chapter 7 Tool Kit For Stock ValuationElias DEBSNo ratings yet

- Factors Influencing Attitudes and Intention To Adopt Financial Technology Services Among The End Users in Lagos State NigeriaDocument9 pagesFactors Influencing Attitudes and Intention To Adopt Financial Technology Services Among The End Users in Lagos State NigeriaGagah PratamaNo ratings yet

- Safe OP - Working Machinery On Slopes: General Safety Rules and GuidanceDocument2 pagesSafe OP - Working Machinery On Slopes: General Safety Rules and Guidanceminov minovitchNo ratings yet

Download as docx, pdf, or txt

You might also like

- MICPA at Full Set Note USEDocument61 pagesMICPA at Full Set Note USEHafiz Musannef100% (1)

- Suggested Solution Far 660 Final Exam JUNE 2019Document6 pagesSuggested Solution Far 660 Final Exam JUNE 2019Nur ShahiraNo ratings yet

- Chapter 4Document45 pagesChapter 4Yanjing Liu67% (3)

- Chapter - 8 Management of ReceivablesDocument6 pagesChapter - 8 Management of ReceivablesadhishcaNo ratings yet

- PS2Document18 pagesPS2Thanh NguyenNo ratings yet

- Solution Test 1Document3 pagesSolution Test 1anis izzatiNo ratings yet

- Dec 2014Document2 pagesDec 2014Zahiratul QamarinaNo ratings yet

- ABC and XYZ - AnswerDocument6 pagesABC and XYZ - AnswerMohammad El HajjNo ratings yet

- Chapter2 Premium LiabilitiesDocument23 pagesChapter2 Premium LiabilitiesReighjon Ashley C. TolentinoNo ratings yet

- House ProDocument7 pagesHouse Prosb_jainNo ratings yet

- Common Test Aud 689 Answer All Questions Time: 1 Hour 45 MinutesDocument8 pagesCommon Test Aud 689 Answer All Questions Time: 1 Hour 45 MinutesNur Dina AbsbNo ratings yet

- Arens Chapter20Document105 pagesArens Chapter20rochielanciolaNo ratings yet

- MBA 504 Ch5 SolutionsDocument12 pagesMBA 504 Ch5 SolutionspheeyonaNo ratings yet

- Income From House Property PracticalDocument52 pagesIncome From House Property PracticalShreekanta DattaNo ratings yet

- Cost II Chapter ThreeDocument11 pagesCost II Chapter ThreeSemira100% (1)

- Chapter 4 Solutions: A) Explain The FollowingDocument23 pagesChapter 4 Solutions: A) Explain The FollowingAdebayo Yusuff AdesholaNo ratings yet

- PVC Analysis QNDocument14 pagesPVC Analysis QNAnipa HubertNo ratings yet

- ACC406 - Chapter - 13 - Relevant - Costing - IIDocument20 pagesACC406 - Chapter - 13 - Relevant - Costing - IIkaylatolentino4No ratings yet

- Chap 24 - Investment in Associate - Basic Principle Fin Acct 1 - Barter Summary Team PDFDocument5 pagesChap 24 - Investment in Associate - Basic Principle Fin Acct 1 - Barter Summary Team PDFSuper JhedNo ratings yet

- 9 Trade CreditDocument13 pages9 Trade CreditMohammad DwidarNo ratings yet

- 1a. Investment in Associate - LectureDocument14 pages1a. Investment in Associate - Lecturekyle GipulanNo ratings yet

- Provision Contingency Liabilities and CoDocument16 pagesProvision Contingency Liabilities and CoPipz G. Castro100% (1)

- Theory of Accounts L. R. Cabarles Toa.112 - Impairment of Assets Lecture NotesDocument5 pagesTheory of Accounts L. R. Cabarles Toa.112 - Impairment of Assets Lecture NotesPia DagmanNo ratings yet

- Lesson 4-Quantitative TechniquesDocument7 pagesLesson 4-Quantitative TechniquesLuiNo ratings yet

- Pfrs 2 Share-Based PaymentsDocument3 pagesPfrs 2 Share-Based PaymentsR.A.No ratings yet

- Tax Q&A - Income From Investment and Other SourcesDocument3 pagesTax Q&A - Income From Investment and Other SourcesHadifliNo ratings yet

- Chapter # 8 Exercise & Problems - AnswersDocument8 pagesChapter # 8 Exercise & Problems - AnswersZia UddinNo ratings yet

- Corporate Finance Model AnswerDocument3 pagesCorporate Finance Model AnswersrikanthNo ratings yet

- The Cost of Trade CreditDocument4 pagesThe Cost of Trade CreditWawex DavisNo ratings yet

- Practice Questions and Concepts of The Balanced ScorecardDocument8 pagesPractice Questions and Concepts of The Balanced ScorecardJuan Dela Cruz IIINo ratings yet

- Tutorial 5 - Marginal and Absorption Costing QuestionsDocument3 pagesTutorial 5 - Marginal and Absorption Costing QuestionsAnonymous 9GgsGYEf100% (1)

- Chapter Two-Accounting For InventoryDocument25 pagesChapter Two-Accounting For Inventoryzewdie100% (1)

- Receivable ManagementDocument40 pagesReceivable ManagementrenudhingraNo ratings yet

- Income Tax Guide UgandaDocument13 pagesIncome Tax Guide UgandaMoses LubangakeneNo ratings yet

- ZBB Vs ABB Traditional BudgetingDocument4 pagesZBB Vs ABB Traditional BudgetingAbhijeet KendoleNo ratings yet

- Diploma in Business Administration (Diba) BM 321 - Financial Accounting Assignment - 20%Document1 pageDiploma in Business Administration (Diba) BM 321 - Financial Accounting Assignment - 20%ranjinikpNo ratings yet

- ENCANA Corporation: The Cost of Capital: Weight of Debt Rate of Debt Tax Weight of Equity Rate of EquityDocument3 pagesENCANA Corporation: The Cost of Capital: Weight of Debt Rate of Debt Tax Weight of Equity Rate of EquityVamsi GunturuNo ratings yet

- 11 35Document8 pages11 35Wildan IrfansyahNo ratings yet

- Wacc Mini CaseDocument12 pagesWacc Mini CaseKishore NaiduNo ratings yet

- Table of Specifications Management Advisory Services: Remembering Understanding Application Analyzing Evaluating CreatingDocument25 pagesTable of Specifications Management Advisory Services: Remembering Understanding Application Analyzing Evaluating CreatingJoshua JoshNo ratings yet

- Tailieumienphi - VN Lecture Logistics Theory Lecture 16 Material Requirements PlanningDocument21 pagesTailieumienphi - VN Lecture Logistics Theory Lecture 16 Material Requirements PlanningBong ThoNo ratings yet

- Chapter 1 Cash and Cash Equivalent - REVIEWERDocument32 pagesChapter 1 Cash and Cash Equivalent - REVIEWERAiyana AlaniNo ratings yet

- Chapter 6 - Business StrategyDocument5 pagesChapter 6 - Business StrategySteffany RoqueNo ratings yet

- MFRS 101 - Ig - 042015Document24 pagesMFRS 101 - Ig - 042015Prasen RajNo ratings yet

- Fair Value Adjustment and Consolidation Adjustment Week 2Document9 pagesFair Value Adjustment and Consolidation Adjustment Week 2Omolaja IbukunNo ratings yet

- Test Aud 689 - Apr 2018Document3 pagesTest Aud 689 - Apr 2018Nur Dina AbsbNo ratings yet

- Accounting For RoyaltiesDocument19 pagesAccounting For RoyaltieskwameNo ratings yet

- Chapter 13 - CashFlow - STUDENTSDocument5 pagesChapter 13 - CashFlow - STUDENTSCalvin Fishy SuNo ratings yet

- Agan Interior Design - ExerciseDocument2 pagesAgan Interior Design - ExerciseLouieNo ratings yet

- Activity-Based Costing: A Tool To Aid Decision MakingDocument75 pagesActivity-Based Costing: A Tool To Aid Decision MakingNavleen Kaur100% (1)

- Ch07 Compound Financial InstrumentDocument5 pagesCh07 Compound Financial InstrumentJessica AllyNo ratings yet

- Solution Far560 - Jun 2015 (S)Document7 pagesSolution Far560 - Jun 2015 (S)MUHAMAD MUKHAIRI MUHAMAD HANIFAHNo ratings yet

- Cost Volume Profit Analysis Review NotesDocument17 pagesCost Volume Profit Analysis Review NotesAlexis Kaye DayagNo ratings yet

- BBS 1st Year QuestionDocument2 pagesBBS 1st Year Questionsatya100% (1)

- Factoring ServicingDocument25 pagesFactoring ServicingTanya JaliNo ratings yet

- Tutorial 2 Capital Allowances - Q&ADocument8 pagesTutorial 2 Capital Allowances - Q&AKamal JabriNo ratings yet

- Cash Flow and Fund Flow StatementDocument23 pagesCash Flow and Fund Flow StatementRishul BhasinNo ratings yet

- Solution Tax667 - Dec 2016Document7 pagesSolution Tax667 - Dec 2016Zahiratul QamarinaNo ratings yet

- Suggested Answers TAX667 - DEC 2016Document7 pagesSuggested Answers TAX667 - DEC 2016diysNo ratings yet

- Solution Tax667 - Jun 2018Document9 pagesSolution Tax667 - Jun 2018Aiyani NabihahNo ratings yet

- Solution Test 2 (1) June 19Document5 pagesSolution Test 2 (1) June 19Nur Dina AbsbNo ratings yet

- Tybms - International MarketingDocument22 pagesTybms - International MarketingRithik ThakurNo ratings yet

- Handout CHE F343Document3 pagesHandout CHE F343Aryan ShuklaNo ratings yet

- Akshit Goyal 2020060472: Unit 2 ExercisesDocument5 pagesAkshit Goyal 2020060472: Unit 2 ExercisesAkshit GoyalNo ratings yet

- The Foreign Exchange MarketDocument33 pagesThe Foreign Exchange MarketShantanu ChoudhuryNo ratings yet

- TATA Family TreeDocument1 pageTATA Family Treemehulchauhan_9950% (2)

- GRADE 9 Ems ExamDocument10 pagesGRADE 9 Ems ExamZam100% (1)

- Mdra0101 443864197Document2 pagesMdra0101 443864197DavidNo ratings yet

- QuestalltDocument9 pagesQuestalltSubin chhatriaNo ratings yet

- Philippineusa 140219175321 Phpapp01Document32 pagesPhilippineusa 140219175321 Phpapp01BJ AmbatNo ratings yet

- Ratio Analysis of Vardhman TextileDocument46 pagesRatio Analysis of Vardhman TextileAjit Sharma100% (1)

- RBI Grade B 28 May 2022 Memory Based Paper (English)Document22 pagesRBI Grade B 28 May 2022 Memory Based Paper (English)VinayRajNo ratings yet

- State of Digital Adoption in Construction 2024Document48 pagesState of Digital Adoption in Construction 2024drafteramdNo ratings yet

- Company Name Exchange:Ticker Watch Lists Ount Raised ($usdmm, Today'S Rate)Document953 pagesCompany Name Exchange:Ticker Watch Lists Ount Raised ($usdmm, Today'S Rate)Keval KatrodiyaNo ratings yet

- IMF 2020 Well SpentDocument341 pagesIMF 2020 Well SpentLuchi RussoNo ratings yet

- Grade 7 Tech Memo June 2019 1Document3 pagesGrade 7 Tech Memo June 2019 1emmanuelmutemba919No ratings yet

- Law New Syllabus Compiled QuestionsDocument98 pagesLaw New Syllabus Compiled Questionsenila upretiNo ratings yet

- Kaplan-M1 Ch2 PDocument22 pagesKaplan-M1 Ch2 PinbyNo ratings yet

- MODULE 16 Share-Based PaymentDocument8 pagesMODULE 16 Share-Based PaymentJanelleNo ratings yet

- Pas 1: Presentation of Financial StatementsDocument16 pagesPas 1: Presentation of Financial StatementsKryzzel Anne JonNo ratings yet

- Official Journal C48: of The European UnionDocument5 pagesOfficial Journal C48: of The European UnionDaiuk.DakNo ratings yet

- Housing Loan Management: A Study of Kuc Bank LTD.: Kshitija Sawant, Shrikrishna MahajanDocument6 pagesHousing Loan Management: A Study of Kuc Bank LTD.: Kshitija Sawant, Shrikrishna MahajanGoogle WebNo ratings yet

- Basics of Accounting: By: Dr. Bhupendra Singh HadaDocument84 pagesBasics of Accounting: By: Dr. Bhupendra Singh HadaAryanSinghNo ratings yet

- 2002 Sing J Legal Stud 455Document35 pages2002 Sing J Legal Stud 455me elkNo ratings yet

- Lecture 11&12 Statement of Cash Flows - NUS ACC1002 2020 SpringDocument57 pagesLecture 11&12 Statement of Cash Flows - NUS ACC1002 2020 SpringZenyuiNo ratings yet

- MCQ-Business-Management (2 Files Merged)Document47 pagesMCQ-Business-Management (2 Files Merged)Sakthivel PoovanNo ratings yet

- Mission VisionmmDocument11 pagesMission VisionmmHumayra SalsabilNo ratings yet

- Valuing Common Stocks: Chapter 7 Tool Kit For Stock ValuationDocument20 pagesValuing Common Stocks: Chapter 7 Tool Kit For Stock ValuationElias DEBSNo ratings yet

- Factors Influencing Attitudes and Intention To Adopt Financial Technology Services Among The End Users in Lagos State NigeriaDocument9 pagesFactors Influencing Attitudes and Intention To Adopt Financial Technology Services Among The End Users in Lagos State NigeriaGagah PratamaNo ratings yet

- Safe OP - Working Machinery On Slopes: General Safety Rules and GuidanceDocument2 pagesSafe OP - Working Machinery On Slopes: General Safety Rules and Guidanceminov minovitchNo ratings yet