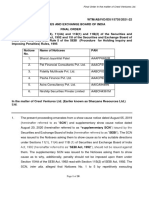

SEBI Adjudication Order Malabar Trading Company Ltd. (18:09:2020)

SEBI Adjudication Order Malabar Trading Company Ltd. (18:09:2020)

You might also like

- Car Petrol BillDocument1 pageCar Petrol BillRuchir Prasoon71% (14)

- International Consulting ContractDocument11 pagesInternational Consulting ContractGlobal NegotiatorNo ratings yet

- Return of Property ApplicationDocument10 pagesReturn of Property Applicationabdullah maknojia80% (5)

- Ashirvad CPVC - Price List - 1st March 2021Document14 pagesAshirvad CPVC - Price List - 1st March 2021Ujwal Elijah Gurram100% (1)

- Dey'S - Sample PDF - Accountancy-XII Exam Handbook 2021-22 (Term-I)Document73 pagesDey'S - Sample PDF - Accountancy-XII Exam Handbook 2021-22 (Term-I)icarus falls57% (7)

- Final Order in The Matter of Crest Ventures LTDDocument28 pagesFinal Order in The Matter of Crest Ventures LTDPratim MajumderNo ratings yet

- S. No. Name of The Noticee PANDocument51 pagesS. No. Name of The Noticee PANPratim MajumderNo ratings yet

- Ashirvad CPVC Pricelist 20-Jul-23Document18 pagesAshirvad CPVC Pricelist 20-Jul-23AniruddhaPalriwalaNo ratings yet

- CPVC Flowguard Price List 2023Document18 pagesCPVC Flowguard Price List 2023Nishant KetuNo ratings yet

- Empl CCDocument58 pagesEmpl CCGerry MalgapoNo ratings yet

- CPVC - Price List - 02nd April 2022Document14 pagesCPVC - Price List - 02nd April 2022Amit Agrawal100% (1)

- NEW CPVC - Price List - 2nd April 2022Document16 pagesNEW CPVC - Price List - 2nd April 2022Amit Agrawal100% (1)

- CPVC - Price List - 7th Oct 2022Document16 pagesCPVC - Price List - 7th Oct 2022Vijay SharmaNo ratings yet

- Ashirvad CPVC - Price List - 1st March 2021Document14 pagesAshirvad CPVC - Price List - 1st March 2021Ujwal Elijah GurramNo ratings yet

- Pfgbest Ice Agro I Daily Report 012910Document4 pagesPfgbest Ice Agro I Daily Report 012910gccommoditiesNo ratings yet

- Average IndicatorsDocument37 pagesAverage IndicatorsHarsh MisraNo ratings yet

- CIPS Level 5 - AD3 May14 Pre ReleaseDocument3 pagesCIPS Level 5 - AD3 May14 Pre ReleaseRakib Uddin AhmedNo ratings yet

- viewNitPdf 4505939Document6 pagesviewNitPdf 4505939gagandeep singhNo ratings yet

- Module III: Derivatives: Chapter 3: Exchange Traded Currency Derivatives in IndiaDocument8 pagesModule III: Derivatives: Chapter 3: Exchange Traded Currency Derivatives in Indiasantucan1No ratings yet

- GeM Bidding 6534016Document24 pagesGeM Bidding 6534016spirientconsultancyNo ratings yet

- Suppl ListDocument5 pagesSuppl ListAmar KumarNo ratings yet

- AVANIGADDADocument28 pagesAVANIGADDAAdi RameshNo ratings yet

- Jadual Waktu Kosong (15 Waktu)Document2 pagesJadual Waktu Kosong (15 Waktu)Jard SaidinNo ratings yet

- Pfgbest Ice Agro I Daily Report 012810Document4 pagesPfgbest Ice Agro I Daily Report 012810gccommoditiesNo ratings yet

- Swaps Made Available To Trade: Fixed-to-Floating Interest Rate Swap (USD)Document3 pagesSwaps Made Available To Trade: Fixed-to-Floating Interest Rate Swap (USD)sosnNo ratings yet

- GeM Bidding 6559740Document40 pagesGeM Bidding 6559740SUPRIYO PARAMANIKNo ratings yet

- Contract Cost Estimate Variation Form FirmDocument4 pagesContract Cost Estimate Variation Form Firmsaneeltandan1No ratings yet

- Stock Reort: Date Receipt Register No. Material Description Opening Balance Receipt Quantity Total QuantityDocument2 pagesStock Reort: Date Receipt Register No. Material Description Opening Balance Receipt Quantity Total QuantitysssadangiNo ratings yet

- FMEX Assignment Group2Document16 pagesFMEX Assignment Group2Raju SharmaNo ratings yet

- GeM Bidding 4795248Document6 pagesGeM Bidding 4795248Abhi SharmaNo ratings yet

- Logiq 500 GEDocument407 pagesLogiq 500 GEJoana PauloNo ratings yet

- Assignment 1 Tabulation SheetDocument10 pagesAssignment 1 Tabulation SheetKALIDAS MANU.MNo ratings yet

- Project Chart With FormulasDocument18 pagesProject Chart With FormulasLiza GeorgeNo ratings yet

- Murrey Math With Slope2Document14 pagesMurrey Math With Slope2Sam D'sozaNo ratings yet

- Petrol BillDocument1 pagePetrol Billas.linkedin20No ratings yet

- GeM Bidding 6005890Document38 pagesGeM Bidding 6005890DHEERAJ JAINNo ratings yet

- Register SPP - Sp2D (Up, Tu, LS) : Pemerintah Kabupaten SimeulueDocument4 pagesRegister SPP - Sp2D (Up, Tu, LS) : Pemerintah Kabupaten SimeulueFirmanSimeulueNo ratings yet

- RHD Schedule of Rates 2019 PDFDocument10 pagesRHD Schedule of Rates 2019 PDFQing DongNo ratings yet

- 11A For Digitally SingDocument1 page11A For Digitally SingSAURAV KUMARNo ratings yet

- Calibration Maintance ChartDocument1 pageCalibration Maintance ChartSundara NayakanNo ratings yet

- Calibration Maintance ChartDocument1 pageCalibration Maintance ChartSundara NayakanNo ratings yet

- Terms N Cnditions AssignmentDocument10 pagesTerms N Cnditions AssignmentarchundimNo ratings yet

- Statistics at A Glance Contract: Bursa Malaysia Derivatives Trading Summary Date: 03 February 2021 (Wednesday)Document94 pagesStatistics at A Glance Contract: Bursa Malaysia Derivatives Trading Summary Date: 03 February 2021 (Wednesday)laugra16No ratings yet

- Main Sanitary Store (Zakhira)Document7 pagesMain Sanitary Store (Zakhira)Subhas MishraNo ratings yet

- Nos. System Name of Tanks Contract No Contractor/ InvestorDocument20 pagesNos. System Name of Tanks Contract No Contractor/ InvestorNadeeshani MunasingheNo ratings yet

- GeM Bidding 5691429Document7 pagesGeM Bidding 5691429DHEERAJ JAINNo ratings yet

- Ink Tack Analysis: Travis Drew - Madalyn Krapez-FewsterDocument8 pagesInk Tack Analysis: Travis Drew - Madalyn Krapez-FewsterTrần NamNo ratings yet

- For PAC NewDocument9 pagesFor PAC NewRahul ChauhanNo ratings yet

- Domain: PeriodDocument21 pagesDomain: PerioddpnairNo ratings yet

- Tata MetaliksDocument2 pagesTata MetaliksRakesh KumarNo ratings yet

- Bit TorquesDocument1 pageBit TorquesEloy RosilloNo ratings yet

- ROH Sistem 19 April 2024Document3 pagesROH Sistem 19 April 2024setioNo ratings yet

- View Tender FileDocument364 pagesView Tender FileEngy RamadanNo ratings yet

- 2 15P01 PDFDocument82 pages2 15P01 PDFMike2322No ratings yet

- Cash MemoDocument2 pagesCash MemoLALRINCHHANA HRAHSELNo ratings yet

- F4 Remap RPT - ShareDocument1 pageF4 Remap RPT - SharehaniabeNo ratings yet

- GeM Bidding 5179742Document70 pagesGeM Bidding 5179742G K SINGHNo ratings yet

- Aryan 6278 ChallanDocument2 pagesAryan 6278 Challankirti tanwarNo ratings yet

- Statistics at A Glance Contract: Bursa Malaysia Derivatives Trading Summary Date: 28 April 2021 (Wednesday)Document114 pagesStatistics at A Glance Contract: Bursa Malaysia Derivatives Trading Summary Date: 28 April 2021 (Wednesday)dougNo ratings yet

- Explanation For The Notification On Escalation Factors and Other Parameters, Dated 7.4.2015Document12 pagesExplanation For The Notification On Escalation Factors and Other Parameters, Dated 7.4.2015spgkumar7733No ratings yet

- SBI Challan FormDocument1 pageSBI Challan FormPandu ChinnuNo ratings yet

- Ubah JT 03 April 2024Document13 pagesUbah JT 03 April 2024deaaulNo ratings yet

- Affidavit: RespectivelyDocument6 pagesAffidavit: RespectivelyadvsonaliNo ratings yet

- Agreement Appointing Three Conciliators For Conciliation of DisputesDocument3 pagesAgreement Appointing Three Conciliators For Conciliation of DisputesShrishti enterprisesNo ratings yet

- Certificate of OriginDocument2 pagesCertificate of OriginRafael ManjarrezNo ratings yet

- Non Commercial LicenceDocument13 pagesNon Commercial Licenceharry_wisteriaNo ratings yet

- Tutorial 3Document6 pagesTutorial 3DC ChanNo ratings yet

- Brand Sublicense Contract Eng2Document6 pagesBrand Sublicense Contract Eng2Dody SilalahiNo ratings yet

- Bar Exam 151-200Document50 pagesBar Exam 151-200Glory TraderNo ratings yet

- 203A Eng 07 16Document5 pages203A Eng 07 16farithNo ratings yet

- Dwnload Full Management of Strategy Concepts International Edition 10th Edition Ireland Test Bank PDFDocument18 pagesDwnload Full Management of Strategy Concepts International Edition 10th Edition Ireland Test Bank PDFmikealfuitem100% (13)

- USCIS Lease ProspectusDocument4 pagesUSCIS Lease ProspectusDaniel J. SernovitzNo ratings yet

- Burger King Case LawDocument16 pagesBurger King Case LawharshagarwalindoreNo ratings yet

- Doas-Garden GroveDocument4 pagesDoas-Garden Groveshrine obenietaNo ratings yet

- Po0000 000221Document3 pagesPo0000 000221BAKINEC AZERSKIYNo ratings yet

- Sale of Goods ActDocument37 pagesSale of Goods ActTARUN RAJANINo ratings yet

- Comparative Table of ContractDocument3 pagesComparative Table of ContractAJ FHNo ratings yet

- PK Judments 2015 YLR 1845 PESHAWAR HIGH COURTDocument2 pagesPK Judments 2015 YLR 1845 PESHAWAR HIGH COURTghaffarkhan355No ratings yet

- Philbanking vs. TensuanDocument3 pagesPhilbanking vs. TensuankarleneNo ratings yet

- Bandagulan 2023 MechanicsDocument4 pagesBandagulan 2023 MechanicsCindy Quite MansuetoNo ratings yet

- Succession Cases Recit 1Document8 pagesSuccession Cases Recit 1Wilfredo Guerrero IIINo ratings yet

- Coke Vs Sps BernardoDocument2 pagesCoke Vs Sps Bernardoapril aranteNo ratings yet

- 9.heirs of Soledad Alido vs. Campano, 911 SCRA 148, July 29, 2019Document2 pages9.heirs of Soledad Alido vs. Campano, 911 SCRA 148, July 29, 2019Samuel John CahimatNo ratings yet

- CLC Covid-19 Claims and Disputes in Construction: 11 January 2021 1.1Document4 pagesCLC Covid-19 Claims and Disputes in Construction: 11 January 2021 1.1dewminiNo ratings yet

- $60 King Co Eviction Kit - REVISED 12.16.22Document104 pages$60 King Co Eviction Kit - REVISED 12.16.22Chris FongNo ratings yet

- SALE AGREEMENT Part PaymentDocument7 pagesSALE AGREEMENT Part PaymentUsama KHanNo ratings yet

- Capital Punishment: Death.: Afflictive PenaltiesDocument1 pageCapital Punishment: Death.: Afflictive PenaltiesJemaineNo ratings yet

- Finger Buildings - North To South Corridors IIDocument84 pagesFinger Buildings - North To South Corridors IIBoris SantosNo ratings yet

- The Widow's Dog by Mitford, Mary Russell, 1787-1855Document14 pagesThe Widow's Dog by Mitford, Mary Russell, 1787-1855Gutenberg.orgNo ratings yet

Download as pdf or txt

You might also like

- Car Petrol BillDocument1 pageCar Petrol BillRuchir Prasoon71% (14)

- International Consulting ContractDocument11 pagesInternational Consulting ContractGlobal NegotiatorNo ratings yet

- Return of Property ApplicationDocument10 pagesReturn of Property Applicationabdullah maknojia80% (5)

- Ashirvad CPVC - Price List - 1st March 2021Document14 pagesAshirvad CPVC - Price List - 1st March 2021Ujwal Elijah Gurram100% (1)

- Dey'S - Sample PDF - Accountancy-XII Exam Handbook 2021-22 (Term-I)Document73 pagesDey'S - Sample PDF - Accountancy-XII Exam Handbook 2021-22 (Term-I)icarus falls57% (7)

- Final Order in The Matter of Crest Ventures LTDDocument28 pagesFinal Order in The Matter of Crest Ventures LTDPratim MajumderNo ratings yet

- S. No. Name of The Noticee PANDocument51 pagesS. No. Name of The Noticee PANPratim MajumderNo ratings yet

- Ashirvad CPVC Pricelist 20-Jul-23Document18 pagesAshirvad CPVC Pricelist 20-Jul-23AniruddhaPalriwalaNo ratings yet

- CPVC Flowguard Price List 2023Document18 pagesCPVC Flowguard Price List 2023Nishant KetuNo ratings yet

- Empl CCDocument58 pagesEmpl CCGerry MalgapoNo ratings yet

- CPVC - Price List - 02nd April 2022Document14 pagesCPVC - Price List - 02nd April 2022Amit Agrawal100% (1)

- NEW CPVC - Price List - 2nd April 2022Document16 pagesNEW CPVC - Price List - 2nd April 2022Amit Agrawal100% (1)

- CPVC - Price List - 7th Oct 2022Document16 pagesCPVC - Price List - 7th Oct 2022Vijay SharmaNo ratings yet

- Ashirvad CPVC - Price List - 1st March 2021Document14 pagesAshirvad CPVC - Price List - 1st March 2021Ujwal Elijah GurramNo ratings yet

- Pfgbest Ice Agro I Daily Report 012910Document4 pagesPfgbest Ice Agro I Daily Report 012910gccommoditiesNo ratings yet

- Average IndicatorsDocument37 pagesAverage IndicatorsHarsh MisraNo ratings yet

- CIPS Level 5 - AD3 May14 Pre ReleaseDocument3 pagesCIPS Level 5 - AD3 May14 Pre ReleaseRakib Uddin AhmedNo ratings yet

- viewNitPdf 4505939Document6 pagesviewNitPdf 4505939gagandeep singhNo ratings yet

- Module III: Derivatives: Chapter 3: Exchange Traded Currency Derivatives in IndiaDocument8 pagesModule III: Derivatives: Chapter 3: Exchange Traded Currency Derivatives in Indiasantucan1No ratings yet

- GeM Bidding 6534016Document24 pagesGeM Bidding 6534016spirientconsultancyNo ratings yet

- Suppl ListDocument5 pagesSuppl ListAmar KumarNo ratings yet

- AVANIGADDADocument28 pagesAVANIGADDAAdi RameshNo ratings yet

- Jadual Waktu Kosong (15 Waktu)Document2 pagesJadual Waktu Kosong (15 Waktu)Jard SaidinNo ratings yet

- Pfgbest Ice Agro I Daily Report 012810Document4 pagesPfgbest Ice Agro I Daily Report 012810gccommoditiesNo ratings yet

- Swaps Made Available To Trade: Fixed-to-Floating Interest Rate Swap (USD)Document3 pagesSwaps Made Available To Trade: Fixed-to-Floating Interest Rate Swap (USD)sosnNo ratings yet

- GeM Bidding 6559740Document40 pagesGeM Bidding 6559740SUPRIYO PARAMANIKNo ratings yet

- Contract Cost Estimate Variation Form FirmDocument4 pagesContract Cost Estimate Variation Form Firmsaneeltandan1No ratings yet

- Stock Reort: Date Receipt Register No. Material Description Opening Balance Receipt Quantity Total QuantityDocument2 pagesStock Reort: Date Receipt Register No. Material Description Opening Balance Receipt Quantity Total QuantitysssadangiNo ratings yet

- FMEX Assignment Group2Document16 pagesFMEX Assignment Group2Raju SharmaNo ratings yet

- GeM Bidding 4795248Document6 pagesGeM Bidding 4795248Abhi SharmaNo ratings yet

- Logiq 500 GEDocument407 pagesLogiq 500 GEJoana PauloNo ratings yet

- Assignment 1 Tabulation SheetDocument10 pagesAssignment 1 Tabulation SheetKALIDAS MANU.MNo ratings yet

- Project Chart With FormulasDocument18 pagesProject Chart With FormulasLiza GeorgeNo ratings yet

- Murrey Math With Slope2Document14 pagesMurrey Math With Slope2Sam D'sozaNo ratings yet

- Petrol BillDocument1 pagePetrol Billas.linkedin20No ratings yet

- GeM Bidding 6005890Document38 pagesGeM Bidding 6005890DHEERAJ JAINNo ratings yet

- Register SPP - Sp2D (Up, Tu, LS) : Pemerintah Kabupaten SimeulueDocument4 pagesRegister SPP - Sp2D (Up, Tu, LS) : Pemerintah Kabupaten SimeulueFirmanSimeulueNo ratings yet

- RHD Schedule of Rates 2019 PDFDocument10 pagesRHD Schedule of Rates 2019 PDFQing DongNo ratings yet

- 11A For Digitally SingDocument1 page11A For Digitally SingSAURAV KUMARNo ratings yet

- Calibration Maintance ChartDocument1 pageCalibration Maintance ChartSundara NayakanNo ratings yet

- Calibration Maintance ChartDocument1 pageCalibration Maintance ChartSundara NayakanNo ratings yet

- Terms N Cnditions AssignmentDocument10 pagesTerms N Cnditions AssignmentarchundimNo ratings yet

- Statistics at A Glance Contract: Bursa Malaysia Derivatives Trading Summary Date: 03 February 2021 (Wednesday)Document94 pagesStatistics at A Glance Contract: Bursa Malaysia Derivatives Trading Summary Date: 03 February 2021 (Wednesday)laugra16No ratings yet

- Main Sanitary Store (Zakhira)Document7 pagesMain Sanitary Store (Zakhira)Subhas MishraNo ratings yet

- Nos. System Name of Tanks Contract No Contractor/ InvestorDocument20 pagesNos. System Name of Tanks Contract No Contractor/ InvestorNadeeshani MunasingheNo ratings yet

- GeM Bidding 5691429Document7 pagesGeM Bidding 5691429DHEERAJ JAINNo ratings yet

- Ink Tack Analysis: Travis Drew - Madalyn Krapez-FewsterDocument8 pagesInk Tack Analysis: Travis Drew - Madalyn Krapez-FewsterTrần NamNo ratings yet

- For PAC NewDocument9 pagesFor PAC NewRahul ChauhanNo ratings yet

- Domain: PeriodDocument21 pagesDomain: PerioddpnairNo ratings yet

- Tata MetaliksDocument2 pagesTata MetaliksRakesh KumarNo ratings yet

- Bit TorquesDocument1 pageBit TorquesEloy RosilloNo ratings yet

- ROH Sistem 19 April 2024Document3 pagesROH Sistem 19 April 2024setioNo ratings yet

- View Tender FileDocument364 pagesView Tender FileEngy RamadanNo ratings yet

- 2 15P01 PDFDocument82 pages2 15P01 PDFMike2322No ratings yet

- Cash MemoDocument2 pagesCash MemoLALRINCHHANA HRAHSELNo ratings yet

- F4 Remap RPT - ShareDocument1 pageF4 Remap RPT - SharehaniabeNo ratings yet

- GeM Bidding 5179742Document70 pagesGeM Bidding 5179742G K SINGHNo ratings yet

- Aryan 6278 ChallanDocument2 pagesAryan 6278 Challankirti tanwarNo ratings yet

- Statistics at A Glance Contract: Bursa Malaysia Derivatives Trading Summary Date: 28 April 2021 (Wednesday)Document114 pagesStatistics at A Glance Contract: Bursa Malaysia Derivatives Trading Summary Date: 28 April 2021 (Wednesday)dougNo ratings yet

- Explanation For The Notification On Escalation Factors and Other Parameters, Dated 7.4.2015Document12 pagesExplanation For The Notification On Escalation Factors and Other Parameters, Dated 7.4.2015spgkumar7733No ratings yet

- SBI Challan FormDocument1 pageSBI Challan FormPandu ChinnuNo ratings yet

- Ubah JT 03 April 2024Document13 pagesUbah JT 03 April 2024deaaulNo ratings yet

- Affidavit: RespectivelyDocument6 pagesAffidavit: RespectivelyadvsonaliNo ratings yet

- Agreement Appointing Three Conciliators For Conciliation of DisputesDocument3 pagesAgreement Appointing Three Conciliators For Conciliation of DisputesShrishti enterprisesNo ratings yet

- Certificate of OriginDocument2 pagesCertificate of OriginRafael ManjarrezNo ratings yet

- Non Commercial LicenceDocument13 pagesNon Commercial Licenceharry_wisteriaNo ratings yet

- Tutorial 3Document6 pagesTutorial 3DC ChanNo ratings yet

- Brand Sublicense Contract Eng2Document6 pagesBrand Sublicense Contract Eng2Dody SilalahiNo ratings yet

- Bar Exam 151-200Document50 pagesBar Exam 151-200Glory TraderNo ratings yet

- 203A Eng 07 16Document5 pages203A Eng 07 16farithNo ratings yet

- Dwnload Full Management of Strategy Concepts International Edition 10th Edition Ireland Test Bank PDFDocument18 pagesDwnload Full Management of Strategy Concepts International Edition 10th Edition Ireland Test Bank PDFmikealfuitem100% (13)

- USCIS Lease ProspectusDocument4 pagesUSCIS Lease ProspectusDaniel J. SernovitzNo ratings yet

- Burger King Case LawDocument16 pagesBurger King Case LawharshagarwalindoreNo ratings yet

- Doas-Garden GroveDocument4 pagesDoas-Garden Groveshrine obenietaNo ratings yet

- Po0000 000221Document3 pagesPo0000 000221BAKINEC AZERSKIYNo ratings yet

- Sale of Goods ActDocument37 pagesSale of Goods ActTARUN RAJANINo ratings yet

- Comparative Table of ContractDocument3 pagesComparative Table of ContractAJ FHNo ratings yet

- PK Judments 2015 YLR 1845 PESHAWAR HIGH COURTDocument2 pagesPK Judments 2015 YLR 1845 PESHAWAR HIGH COURTghaffarkhan355No ratings yet

- Philbanking vs. TensuanDocument3 pagesPhilbanking vs. TensuankarleneNo ratings yet

- Bandagulan 2023 MechanicsDocument4 pagesBandagulan 2023 MechanicsCindy Quite MansuetoNo ratings yet

- Succession Cases Recit 1Document8 pagesSuccession Cases Recit 1Wilfredo Guerrero IIINo ratings yet

- Coke Vs Sps BernardoDocument2 pagesCoke Vs Sps Bernardoapril aranteNo ratings yet

- 9.heirs of Soledad Alido vs. Campano, 911 SCRA 148, July 29, 2019Document2 pages9.heirs of Soledad Alido vs. Campano, 911 SCRA 148, July 29, 2019Samuel John CahimatNo ratings yet

- CLC Covid-19 Claims and Disputes in Construction: 11 January 2021 1.1Document4 pagesCLC Covid-19 Claims and Disputes in Construction: 11 January 2021 1.1dewminiNo ratings yet

- $60 King Co Eviction Kit - REVISED 12.16.22Document104 pages$60 King Co Eviction Kit - REVISED 12.16.22Chris FongNo ratings yet

- SALE AGREEMENT Part PaymentDocument7 pagesSALE AGREEMENT Part PaymentUsama KHanNo ratings yet

- Capital Punishment: Death.: Afflictive PenaltiesDocument1 pageCapital Punishment: Death.: Afflictive PenaltiesJemaineNo ratings yet

- Finger Buildings - North To South Corridors IIDocument84 pagesFinger Buildings - North To South Corridors IIBoris SantosNo ratings yet

- The Widow's Dog by Mitford, Mary Russell, 1787-1855Document14 pagesThe Widow's Dog by Mitford, Mary Russell, 1787-1855Gutenberg.orgNo ratings yet