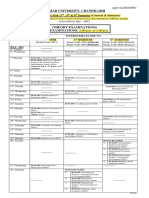

MMC at 1Pb

MMC at 1Pb

You might also like

- PMP® Exam Prep, 10th Edition (Rita Mulcahy) - DNG Academy - (Iqbal Burcha)Document21 pagesPMP® Exam Prep, 10th Edition (Rita Mulcahy) - DNG Academy - (Iqbal Burcha)Uzair Khan100% (1)

- ReSA B44 AUD Final PB With AnswerDocument21 pagesReSA B44 AUD Final PB With AnswerAlliah Mae Acosta100% (1)

- At Preweek HandoutsDocument24 pagesAt Preweek HandoutsCleifairy MuNo ratings yet

- Working Capital ManagementDocument71 pagesWorking Capital ManagementNaveen Kumar Rudrangi100% (2)

- AT Quizzer 1 - Overview of Auditing (2TAY1718)Document12 pagesAT Quizzer 1 - Overview of Auditing (2TAY1718)JimmyChaoNo ratings yet

- CH 1 Quiz With AnswersDocument7 pagesCH 1 Quiz With AnswersBeverly Ann Caparoso100% (3)

- At 502questionsDocument77 pagesAt 502questionsJosephkevin Yap100% (5)

- Test Bank For Quiz BeeDocument5 pagesTest Bank For Quiz BeeRandy PaderesNo ratings yet

- First Preboard ExamsDocument4 pagesFirst Preboard ExamsRandy PaderesNo ratings yet

- May 2019 First PBDocument6 pagesMay 2019 First PBRandy PaderesNo ratings yet

- MMC at 1PbDocument4 pagesMMC at 1PbRandy PaderesNo ratings yet

- Midterm Questions PDFDocument9 pagesMidterm Questions PDFJhanvi SinghNo ratings yet

- QC, Pea, Ap 1Document3 pagesQC, Pea, Ap 1ALLYSON BURAGANo ratings yet

- Quiz PDFDocument4 pagesQuiz PDFAlizahNo ratings yet

- First Board Simulation. at With Answer KeyDocument10 pagesFirst Board Simulation. at With Answer KeyKatzkie Montemayor GodinezNo ratings yet

- ACCO 3116 MidtermDocument11 pagesACCO 3116 MidtermLiyana ChuaNo ratings yet

- AT - First Preboard (October 2011)Document12 pagesAT - First Preboard (October 2011)Kim Cristian MaañoNo ratings yet

- CH 02Document12 pagesCH 02jessa angelaNo ratings yet

- AT Quiz 1Document2 pagesAT Quiz 1CattleyaNo ratings yet

- Auditing and Assurance: Principles: Midterm ExamDocument5 pagesAuditing and Assurance: Principles: Midterm ExamKemerut100% (1)

- Audit ReviewerDocument28 pagesAudit ReviewerBrigit MartinezNo ratings yet

- Practice Examination in Auditing TheoryDocument28 pagesPractice Examination in Auditing TheoryGabriel PonceNo ratings yet

- Preboard Exam - AuditDocument10 pagesPreboard Exam - AuditLeopoldo Reuteras Morte IINo ratings yet

- The Financial Statement AuditDocument4 pagesThe Financial Statement Audittorresthyrene28No ratings yet

- AT - Diagnostic Examfor PrintingDocument8 pagesAT - Diagnostic Examfor PrintingMichaela PortarcosNo ratings yet

- Assurance EngagementsDocument7 pagesAssurance EngagementsXarina LudoviceNo ratings yet

- AT - PreWeek - May 2022Document24 pagesAT - PreWeek - May 2022Miguel ManagoNo ratings yet

- Aud Qlfy Exam RWDocument7 pagesAud Qlfy Exam RWYeji BabeNo ratings yet

- N C O B A A: Ational Ollege F Usiness ND RTSDocument9 pagesN C O B A A: Ational Ollege F Usiness ND RTSNico evansNo ratings yet

- May 09 Final Pre-Board (At)Document13 pagesMay 09 Final Pre-Board (At)Ashley Levy San PedroNo ratings yet

- IAT 2020 Final Preboard (Source SimEx4 RS)Document15 pagesIAT 2020 Final Preboard (Source SimEx4 RS)Mary Yvonne AresNo ratings yet

- Prof. Falsado Online SeatworkDocument9 pagesProf. Falsado Online SeatworkMarian Grace DelapuzNo ratings yet

- Midterm Exam EnjoyDocument14 pagesMidterm Exam EnjoygarciarhodjeannemarthaNo ratings yet

- Auditing Theory MCQs Arens, Elder and BeasleyDocument23 pagesAuditing Theory MCQs Arens, Elder and BeasleyLeigh PilapilNo ratings yet

- Semi FinalsDocument9 pagesSemi FinalsKIM RAGANo ratings yet

- First PreboardDocument5 pagesFirst PreboardRodmae VersonNo ratings yet

- At 3rdbatch FinPBDocument24 pagesAt 3rdbatch FinPBDarwin Ang100% (2)

- AUD Review 10234Document4 pagesAUD Review 10234PachiNo ratings yet

- Assignment 1 in Auditing TheoryDocument6 pagesAssignment 1 in Auditing TheoryfgfsgsrgrgNo ratings yet

- Auditing Test BankDocument34 pagesAuditing Test BanksninaricaNo ratings yet

- Auditing TheoryDocument13 pagesAuditing TheoryJamaica DavidNo ratings yet

- T R S A: HE Eview Chool of CcountancyDocument20 pagesT R S A: HE Eview Chool of CcountancyMae Danica CalunsagNo ratings yet

- Practice Examination IIIDocument13 pagesPractice Examination IIITwinie MendozaNo ratings yet

- PracExam On AudTheoDocument25 pagesPracExam On AudTheoPrancesNo ratings yet

- AT 3rdbatch 1stPBDocument12 pagesAT 3rdbatch 1stPBvangieolalia100% (2)

- Final Exam AUD002Document6 pagesFinal Exam AUD002KathleenNo ratings yet

- AuditingDocument8 pagesAuditingNan Laron ParrochaNo ratings yet

- Specialized Prelim Exam UCPDocument6 pagesSpecialized Prelim Exam UCPlois martinNo ratings yet

- Auditing Theory Final ExamDocument9 pagesAuditing Theory Final ExamGarcia Alizsandra L.No ratings yet

- Auditing Handout Practice Question With Key 1Document5 pagesAuditing Handout Practice Question With Key 1Rinajean Masisado RaymundoNo ratings yet

- Psa Challenge #4Document17 pagesPsa Challenge #4clarencerclacioNo ratings yet

- Colegio de Dagupan Arellano Street, Dagupan City School of Business and Accountancy Preliminary Examination Auditing TheoryDocument18 pagesColegio de Dagupan Arellano Street, Dagupan City School of Business and Accountancy Preliminary Examination Auditing TheoryFeelingerang MAYoraNo ratings yet

- Aud FeDocument11 pagesAud FeMark Domingo MendozaNo ratings yet

- The Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiFrom EverandThe Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiNo ratings yet

- Engagement Essentials: Preparation, Compilation, and Review of Financial StatementsFrom EverandEngagement Essentials: Preparation, Compilation, and Review of Financial StatementsNo ratings yet

- Annual Update and Practice Issues for Preparation, Compilation, and Review EngagementsFrom EverandAnnual Update and Practice Issues for Preparation, Compilation, and Review EngagementsNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: 2020 EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: 2020 EditionNo ratings yet

- c1049 PDFDocument7 pagesc1049 PDFRandy PaderesNo ratings yet

- Dasmariñas Chamber Singers Choir ProfileDocument1 pageDasmariñas Chamber Singers Choir ProfileRandy PaderesNo ratings yet

- Navigating Through The Corporate DNADocument30 pagesNavigating Through The Corporate DNARandy PaderesNo ratings yet

- Eng 13Document1 pageEng 13Randy PaderesNo ratings yet

- Journal Voucher: Date: ParticularsDocument1 pageJournal Voucher: Date: ParticularsRandy PaderesNo ratings yet

- Bangko Sentral Pilipinas: The GovernorDocument4 pagesBangko Sentral Pilipinas: The GovernorRandy PaderesNo ratings yet

- Thesis Statement: Online Education May Become More Advantageous For The Society As A WholeDocument1 pageThesis Statement: Online Education May Become More Advantageous For The Society As A WholeRandy PaderesNo ratings yet

- ENG13Document1 pageENG13Randy PaderesNo ratings yet

- 2017-An Ordinance Enacting The Revised Pasig Revenue CodeDocument194 pages2017-An Ordinance Enacting The Revised Pasig Revenue CodeRandy PaderesNo ratings yet

- Dasmarinas SingersDocument2 pagesDasmarinas SingersRandy PaderesNo ratings yet

- SampleDocument5 pagesSampleRandy PaderesNo ratings yet

- Information Technology Part 1Document4 pagesInformation Technology Part 1Randy PaderesNo ratings yet

- First Preboard ExamsDocument4 pagesFirst Preboard ExamsRandy PaderesNo ratings yet

- Final Preboard ExamsDocument5 pagesFinal Preboard ExamsRandy PaderesNo ratings yet

- AT 07 Audit EvidenceDocument6 pagesAT 07 Audit EvidenceRandy PaderesNo ratings yet

- Competing With Dual Business Models - A Contingency ApproachDocument17 pagesCompeting With Dual Business Models - A Contingency ApproachCaio PeretNo ratings yet

- CAT 2003 Question Paper (Leaked) by CrackuDocument71 pagesCAT 2003 Question Paper (Leaked) by Crackuenzogaming475No ratings yet

- Internship Report On Elite Paint and Chemical Industries Ltd. (EPCIL)Document60 pagesInternship Report On Elite Paint and Chemical Industries Ltd. (EPCIL)Bithee Devi100% (1)

- Materials Management (MM) : Curriculum: Introduction To ERP Using Global BikeDocument46 pagesMaterials Management (MM) : Curriculum: Introduction To ERP Using Global BikeToño Gomez BarredaNo ratings yet

- Ilovepdf Merged PDFDocument666 pagesIlovepdf Merged PDFchandraNo ratings yet

- Shannon's Demon, Parrando's ParadoxDocument4 pagesShannon's Demon, Parrando's ParadoxjohnthomastNo ratings yet

- Organization and Management Module 2: Quarter 1 - Week 2Document15 pagesOrganization and Management Module 2: Quarter 1 - Week 2juvelyn luegoNo ratings yet

- 4 Ways Cloud ERP Can Boost Your Bottom LineDocument2 pages4 Ways Cloud ERP Can Boost Your Bottom LineDexNo ratings yet

- FTT SPCDocument12 pagesFTT SPCKaya Eralp AsabNo ratings yet

- Session 1 - PRIMAN ASMPH - September 22, 2020 - LaxamanaDocument120 pagesSession 1 - PRIMAN ASMPH - September 22, 2020 - LaxamanaErnestoNo ratings yet

- 1 The Defense Proposal Amreeth MullapudiDocument1 page1 The Defense Proposal Amreeth MullapudikarunasevasadanNo ratings yet

- Current Valuation AS139437103Document6 pagesCurrent Valuation AS139437103Kiran KumarNo ratings yet

- 1200 4404 1 PBDocument9 pages1200 4404 1 PBNaufal FarhanNo ratings yet

- 10.annual Report FY 2023Document115 pages10.annual Report FY 2023faarehaNo ratings yet

- Office Relocation WBSDocument3 pagesOffice Relocation WBSsheilasch88No ratings yet

- Reviewer in EntrepreneurshipDocument6 pagesReviewer in EntrepreneurshipRachelle Anne SaldeNo ratings yet

- Chartering Abbreviations 6Document8 pagesChartering Abbreviations 6efekaptanNo ratings yet

- 5-Page Resume Template - USDocument5 pages5-Page Resume Template - USPlayerOne ComputerShopNo ratings yet

- Blu Dart Presentation NewDocument12 pagesBlu Dart Presentation NewSATYAM CHATURVEDINo ratings yet

- Figure 26.1 The Directional Policy Matrix (DPM)Document2 pagesFigure 26.1 The Directional Policy Matrix (DPM)Abdela TuleNo ratings yet

- Acc3 5Document4 pagesAcc3 5dinda ardiyaniNo ratings yet

- Intertek KSA - Bahrain Training Calendar - H1 2021Document1 pageIntertek KSA - Bahrain Training Calendar - H1 2021Ashish ShrivastavaNo ratings yet

- Repair Kits-2Document2 pagesRepair Kits-2BryanNo ratings yet

- Harish Kumar Kandoi: Contact: +91 9874472220/9830714467Document3 pagesHarish Kumar Kandoi: Contact: +91 9874472220/9830714467Sabuj SarkarNo ratings yet

- Audit 2 Test About MaterilaityDocument5 pagesAudit 2 Test About MaterilaityShewanes GetiyeNo ratings yet

- Original For Recipient Duplicate For Transporter Triplicate For SupplierDocument1 pageOriginal For Recipient Duplicate For Transporter Triplicate For SupplierKarthik TNo ratings yet

- Panjab University, Chandigarh: Examination (Offline Mode) To Be Held in July - 2022Document2 pagesPanjab University, Chandigarh: Examination (Offline Mode) To Be Held in July - 2022Sumit SharmaNo ratings yet

- The Interrelationship Between Culture, Capital Structure, and Performance: Evidence From European RetailersDocument7 pagesThe Interrelationship Between Culture, Capital Structure, and Performance: Evidence From European RetailersNgọc Minh PhúNo ratings yet

Download as docx, pdf, or txt

You might also like

- PMP® Exam Prep, 10th Edition (Rita Mulcahy) - DNG Academy - (Iqbal Burcha)Document21 pagesPMP® Exam Prep, 10th Edition (Rita Mulcahy) - DNG Academy - (Iqbal Burcha)Uzair Khan100% (1)

- ReSA B44 AUD Final PB With AnswerDocument21 pagesReSA B44 AUD Final PB With AnswerAlliah Mae Acosta100% (1)

- At Preweek HandoutsDocument24 pagesAt Preweek HandoutsCleifairy MuNo ratings yet

- Working Capital ManagementDocument71 pagesWorking Capital ManagementNaveen Kumar Rudrangi100% (2)

- AT Quizzer 1 - Overview of Auditing (2TAY1718)Document12 pagesAT Quizzer 1 - Overview of Auditing (2TAY1718)JimmyChaoNo ratings yet

- CH 1 Quiz With AnswersDocument7 pagesCH 1 Quiz With AnswersBeverly Ann Caparoso100% (3)

- At 502questionsDocument77 pagesAt 502questionsJosephkevin Yap100% (5)

- Test Bank For Quiz BeeDocument5 pagesTest Bank For Quiz BeeRandy PaderesNo ratings yet

- First Preboard ExamsDocument4 pagesFirst Preboard ExamsRandy PaderesNo ratings yet

- May 2019 First PBDocument6 pagesMay 2019 First PBRandy PaderesNo ratings yet

- MMC at 1PbDocument4 pagesMMC at 1PbRandy PaderesNo ratings yet

- Midterm Questions PDFDocument9 pagesMidterm Questions PDFJhanvi SinghNo ratings yet

- QC, Pea, Ap 1Document3 pagesQC, Pea, Ap 1ALLYSON BURAGANo ratings yet

- Quiz PDFDocument4 pagesQuiz PDFAlizahNo ratings yet

- First Board Simulation. at With Answer KeyDocument10 pagesFirst Board Simulation. at With Answer KeyKatzkie Montemayor GodinezNo ratings yet

- ACCO 3116 MidtermDocument11 pagesACCO 3116 MidtermLiyana ChuaNo ratings yet

- AT - First Preboard (October 2011)Document12 pagesAT - First Preboard (October 2011)Kim Cristian MaañoNo ratings yet

- CH 02Document12 pagesCH 02jessa angelaNo ratings yet

- AT Quiz 1Document2 pagesAT Quiz 1CattleyaNo ratings yet

- Auditing and Assurance: Principles: Midterm ExamDocument5 pagesAuditing and Assurance: Principles: Midterm ExamKemerut100% (1)

- Audit ReviewerDocument28 pagesAudit ReviewerBrigit MartinezNo ratings yet

- Practice Examination in Auditing TheoryDocument28 pagesPractice Examination in Auditing TheoryGabriel PonceNo ratings yet

- Preboard Exam - AuditDocument10 pagesPreboard Exam - AuditLeopoldo Reuteras Morte IINo ratings yet

- The Financial Statement AuditDocument4 pagesThe Financial Statement Audittorresthyrene28No ratings yet

- AT - Diagnostic Examfor PrintingDocument8 pagesAT - Diagnostic Examfor PrintingMichaela PortarcosNo ratings yet

- Assurance EngagementsDocument7 pagesAssurance EngagementsXarina LudoviceNo ratings yet

- AT - PreWeek - May 2022Document24 pagesAT - PreWeek - May 2022Miguel ManagoNo ratings yet

- Aud Qlfy Exam RWDocument7 pagesAud Qlfy Exam RWYeji BabeNo ratings yet

- N C O B A A: Ational Ollege F Usiness ND RTSDocument9 pagesN C O B A A: Ational Ollege F Usiness ND RTSNico evansNo ratings yet

- May 09 Final Pre-Board (At)Document13 pagesMay 09 Final Pre-Board (At)Ashley Levy San PedroNo ratings yet

- IAT 2020 Final Preboard (Source SimEx4 RS)Document15 pagesIAT 2020 Final Preboard (Source SimEx4 RS)Mary Yvonne AresNo ratings yet

- Prof. Falsado Online SeatworkDocument9 pagesProf. Falsado Online SeatworkMarian Grace DelapuzNo ratings yet

- Midterm Exam EnjoyDocument14 pagesMidterm Exam EnjoygarciarhodjeannemarthaNo ratings yet

- Auditing Theory MCQs Arens, Elder and BeasleyDocument23 pagesAuditing Theory MCQs Arens, Elder and BeasleyLeigh PilapilNo ratings yet

- Semi FinalsDocument9 pagesSemi FinalsKIM RAGANo ratings yet

- First PreboardDocument5 pagesFirst PreboardRodmae VersonNo ratings yet

- At 3rdbatch FinPBDocument24 pagesAt 3rdbatch FinPBDarwin Ang100% (2)

- AUD Review 10234Document4 pagesAUD Review 10234PachiNo ratings yet

- Assignment 1 in Auditing TheoryDocument6 pagesAssignment 1 in Auditing TheoryfgfsgsrgrgNo ratings yet

- Auditing Test BankDocument34 pagesAuditing Test BanksninaricaNo ratings yet

- Auditing TheoryDocument13 pagesAuditing TheoryJamaica DavidNo ratings yet

- T R S A: HE Eview Chool of CcountancyDocument20 pagesT R S A: HE Eview Chool of CcountancyMae Danica CalunsagNo ratings yet

- Practice Examination IIIDocument13 pagesPractice Examination IIITwinie MendozaNo ratings yet

- PracExam On AudTheoDocument25 pagesPracExam On AudTheoPrancesNo ratings yet

- AT 3rdbatch 1stPBDocument12 pagesAT 3rdbatch 1stPBvangieolalia100% (2)

- Final Exam AUD002Document6 pagesFinal Exam AUD002KathleenNo ratings yet

- AuditingDocument8 pagesAuditingNan Laron ParrochaNo ratings yet

- Specialized Prelim Exam UCPDocument6 pagesSpecialized Prelim Exam UCPlois martinNo ratings yet

- Auditing Theory Final ExamDocument9 pagesAuditing Theory Final ExamGarcia Alizsandra L.No ratings yet

- Auditing Handout Practice Question With Key 1Document5 pagesAuditing Handout Practice Question With Key 1Rinajean Masisado RaymundoNo ratings yet

- Psa Challenge #4Document17 pagesPsa Challenge #4clarencerclacioNo ratings yet

- Colegio de Dagupan Arellano Street, Dagupan City School of Business and Accountancy Preliminary Examination Auditing TheoryDocument18 pagesColegio de Dagupan Arellano Street, Dagupan City School of Business and Accountancy Preliminary Examination Auditing TheoryFeelingerang MAYoraNo ratings yet

- Aud FeDocument11 pagesAud FeMark Domingo MendozaNo ratings yet

- The Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiFrom EverandThe Basel Ii "Use Test" - a Retail Credit Approach: Developing and Implementing Effective Retail Credit Risk Strategies Using Basel IiNo ratings yet

- Engagement Essentials: Preparation, Compilation, and Review of Financial StatementsFrom EverandEngagement Essentials: Preparation, Compilation, and Review of Financial StatementsNo ratings yet

- Annual Update and Practice Issues for Preparation, Compilation, and Review EngagementsFrom EverandAnnual Update and Practice Issues for Preparation, Compilation, and Review EngagementsNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: 2020 EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: 2020 EditionNo ratings yet

- c1049 PDFDocument7 pagesc1049 PDFRandy PaderesNo ratings yet

- Dasmariñas Chamber Singers Choir ProfileDocument1 pageDasmariñas Chamber Singers Choir ProfileRandy PaderesNo ratings yet

- Navigating Through The Corporate DNADocument30 pagesNavigating Through The Corporate DNARandy PaderesNo ratings yet

- Eng 13Document1 pageEng 13Randy PaderesNo ratings yet

- Journal Voucher: Date: ParticularsDocument1 pageJournal Voucher: Date: ParticularsRandy PaderesNo ratings yet

- Bangko Sentral Pilipinas: The GovernorDocument4 pagesBangko Sentral Pilipinas: The GovernorRandy PaderesNo ratings yet

- Thesis Statement: Online Education May Become More Advantageous For The Society As A WholeDocument1 pageThesis Statement: Online Education May Become More Advantageous For The Society As A WholeRandy PaderesNo ratings yet

- ENG13Document1 pageENG13Randy PaderesNo ratings yet

- 2017-An Ordinance Enacting The Revised Pasig Revenue CodeDocument194 pages2017-An Ordinance Enacting The Revised Pasig Revenue CodeRandy PaderesNo ratings yet

- Dasmarinas SingersDocument2 pagesDasmarinas SingersRandy PaderesNo ratings yet

- SampleDocument5 pagesSampleRandy PaderesNo ratings yet

- Information Technology Part 1Document4 pagesInformation Technology Part 1Randy PaderesNo ratings yet

- First Preboard ExamsDocument4 pagesFirst Preboard ExamsRandy PaderesNo ratings yet

- Final Preboard ExamsDocument5 pagesFinal Preboard ExamsRandy PaderesNo ratings yet

- AT 07 Audit EvidenceDocument6 pagesAT 07 Audit EvidenceRandy PaderesNo ratings yet

- Competing With Dual Business Models - A Contingency ApproachDocument17 pagesCompeting With Dual Business Models - A Contingency ApproachCaio PeretNo ratings yet

- CAT 2003 Question Paper (Leaked) by CrackuDocument71 pagesCAT 2003 Question Paper (Leaked) by Crackuenzogaming475No ratings yet

- Internship Report On Elite Paint and Chemical Industries Ltd. (EPCIL)Document60 pagesInternship Report On Elite Paint and Chemical Industries Ltd. (EPCIL)Bithee Devi100% (1)

- Materials Management (MM) : Curriculum: Introduction To ERP Using Global BikeDocument46 pagesMaterials Management (MM) : Curriculum: Introduction To ERP Using Global BikeToño Gomez BarredaNo ratings yet

- Ilovepdf Merged PDFDocument666 pagesIlovepdf Merged PDFchandraNo ratings yet

- Shannon's Demon, Parrando's ParadoxDocument4 pagesShannon's Demon, Parrando's ParadoxjohnthomastNo ratings yet

- Organization and Management Module 2: Quarter 1 - Week 2Document15 pagesOrganization and Management Module 2: Quarter 1 - Week 2juvelyn luegoNo ratings yet

- 4 Ways Cloud ERP Can Boost Your Bottom LineDocument2 pages4 Ways Cloud ERP Can Boost Your Bottom LineDexNo ratings yet

- FTT SPCDocument12 pagesFTT SPCKaya Eralp AsabNo ratings yet

- Session 1 - PRIMAN ASMPH - September 22, 2020 - LaxamanaDocument120 pagesSession 1 - PRIMAN ASMPH - September 22, 2020 - LaxamanaErnestoNo ratings yet

- 1 The Defense Proposal Amreeth MullapudiDocument1 page1 The Defense Proposal Amreeth MullapudikarunasevasadanNo ratings yet

- Current Valuation AS139437103Document6 pagesCurrent Valuation AS139437103Kiran KumarNo ratings yet

- 1200 4404 1 PBDocument9 pages1200 4404 1 PBNaufal FarhanNo ratings yet

- 10.annual Report FY 2023Document115 pages10.annual Report FY 2023faarehaNo ratings yet

- Office Relocation WBSDocument3 pagesOffice Relocation WBSsheilasch88No ratings yet

- Reviewer in EntrepreneurshipDocument6 pagesReviewer in EntrepreneurshipRachelle Anne SaldeNo ratings yet

- Chartering Abbreviations 6Document8 pagesChartering Abbreviations 6efekaptanNo ratings yet

- 5-Page Resume Template - USDocument5 pages5-Page Resume Template - USPlayerOne ComputerShopNo ratings yet

- Blu Dart Presentation NewDocument12 pagesBlu Dart Presentation NewSATYAM CHATURVEDINo ratings yet

- Figure 26.1 The Directional Policy Matrix (DPM)Document2 pagesFigure 26.1 The Directional Policy Matrix (DPM)Abdela TuleNo ratings yet

- Acc3 5Document4 pagesAcc3 5dinda ardiyaniNo ratings yet

- Intertek KSA - Bahrain Training Calendar - H1 2021Document1 pageIntertek KSA - Bahrain Training Calendar - H1 2021Ashish ShrivastavaNo ratings yet

- Repair Kits-2Document2 pagesRepair Kits-2BryanNo ratings yet

- Harish Kumar Kandoi: Contact: +91 9874472220/9830714467Document3 pagesHarish Kumar Kandoi: Contact: +91 9874472220/9830714467Sabuj SarkarNo ratings yet

- Audit 2 Test About MaterilaityDocument5 pagesAudit 2 Test About MaterilaityShewanes GetiyeNo ratings yet

- Original For Recipient Duplicate For Transporter Triplicate For SupplierDocument1 pageOriginal For Recipient Duplicate For Transporter Triplicate For SupplierKarthik TNo ratings yet

- Panjab University, Chandigarh: Examination (Offline Mode) To Be Held in July - 2022Document2 pagesPanjab University, Chandigarh: Examination (Offline Mode) To Be Held in July - 2022Sumit SharmaNo ratings yet

- The Interrelationship Between Culture, Capital Structure, and Performance: Evidence From European RetailersDocument7 pagesThe Interrelationship Between Culture, Capital Structure, and Performance: Evidence From European RetailersNgọc Minh PhúNo ratings yet