Download as doc, pdf, or txt

You might also like

- The Cash Account in The General Ledger of Hendry CorporationDocument1 pageThe Cash Account in The General Ledger of Hendry Corporationamit raajNo ratings yet

- Accountancy Review Center (ARC) of The Philippines Inc.: First Pre-Board ExaminationDocument26 pagesAccountancy Review Center (ARC) of The Philippines Inc.: First Pre-Board ExaminationCarlo AgravanteNo ratings yet

- Quiz Results: Week 12: Conceptual Framework: Expenses Quizzer 2Document31 pagesQuiz Results: Week 12: Conceptual Framework: Expenses Quizzer 2marie aniceteNo ratings yet

- Reviewer Intacc 1n2Document58 pagesReviewer Intacc 1n2John100% (1)

- Chapter 16 Solution ManualDocument54 pagesChapter 16 Solution ManualJose Matalo67% (3)

- Accounting For Special Transactions ExamDocument19 pagesAccounting For Special Transactions ExamKeon Screeven100% (2)

- A Project Report On Financial Statement AnalysisDocument74 pagesA Project Report On Financial Statement AnalysisSushmita Barla100% (3)

- Activity - Audit of InventoryDocument2 pagesActivity - Audit of InventoryRyan DueÑas GuevarraNo ratings yet

- Auditing JPIADocument18 pagesAuditing JPIAAken Lieram Ats AnaNo ratings yet

- Intermediate Acctg A 1 10Document10 pagesIntermediate Acctg A 1 10Leonila RiveraNo ratings yet

- Partnership Liquidation InstallmentDocument1 pagePartnership Liquidation InstallmentAkira Marantal ValdezNo ratings yet

- Advanced Accounting Home Office, Branch and Agency TransactionsDocument7 pagesAdvanced Accounting Home Office, Branch and Agency TransactionsMajoy Bantoc100% (1)

- Module No. 1 - Week 1 Businessn CombinationDocument5 pagesModule No. 1 - Week 1 Businessn CombinationJayaAntolinAyusteNo ratings yet

- Audit of Cash and Cash EquivalentsDocument9 pagesAudit of Cash and Cash Equivalentspatricia100% (1)

- MODAUD1 UNIT 4 Audit of Inventories PDFDocument9 pagesMODAUD1 UNIT 4 Audit of Inventories PDFJoey WassigNo ratings yet

- PDF Afar Week1 Compiled Questions CompressDocument78 pagesPDF Afar Week1 Compiled Questions CompressIo AyaNo ratings yet

- AP.2906 InvestmentsDocument6 pagesAP.2906 InvestmentsmoNo ratings yet

- DocxDocument12 pagesDocxNothingNo ratings yet

- MODULE 1 2 Bonds PayableDocument10 pagesMODULE 1 2 Bonds PayableFujoshi BeeNo ratings yet

- National Federation of Junior Philipinne Institute of Accountants - National Capital Region Auditing (Aud)Document14 pagesNational Federation of Junior Philipinne Institute of Accountants - National Capital Region Auditing (Aud)Tricia Jen TobiasNo ratings yet

- AFAR FinalMockBoard BDocument11 pagesAFAR FinalMockBoard BCattleyaNo ratings yet

- LTCCDocument2 pagesLTCCN JoNo ratings yet

- AFAR Review Midterm ExamDocument10 pagesAFAR Review Midterm ExamZyrah Mae SaezNo ratings yet

- Quiz - Intangible Assets With QuestionsDocument3 pagesQuiz - Intangible Assets With Questionsjanus lopezNo ratings yet

- Auditing ProblemsDocument6 pagesAuditing ProblemsMaurice AgbayaniNo ratings yet

- Reviewer 1st PB P1 1920Document7 pagesReviewer 1st PB P1 1920Therese AcostaNo ratings yet

- ACC 211 Review AssignmentDocument5 pagesACC 211 Review Assignmentglrosaaa cNo ratings yet

- Instruction: Show Your Solution. No Solution Incorrect AnswerDocument1 pageInstruction: Show Your Solution. No Solution Incorrect AnswerRian ChiseiNo ratings yet

- CH 13Document19 pagesCH 13pesoload100No ratings yet

- National Federation of Junior Philippine Institute of Accountants Financial AccountingDocument8 pagesNational Federation of Junior Philippine Institute of Accountants Financial AccountingWeaFernandezNo ratings yet

- CLINCHERDocument1 pageCLINCHERJerauld BucolNo ratings yet

- Applied Auditing Quiz #1 (Diagnostic Exam)Document15 pagesApplied Auditing Quiz #1 (Diagnostic Exam)xjammerNo ratings yet

- TX12 - Estate TaxDocument14 pagesTX12 - Estate TaxPatrick Kyle AgraviadorNo ratings yet

- Home Office and Branch Accounting PDFDocument3 pagesHome Office and Branch Accounting PDFJisselle Marie Custodio0% (1)

- AFAR-01 (Partnership Formation & Operations)Document6 pagesAFAR-01 (Partnership Formation & Operations)Nathalie Shien DagaragaNo ratings yet

- AP - Loans & ReceivablesDocument11 pagesAP - Loans & ReceivablesDiane PascualNo ratings yet

- Preliminary ExaminationDocument5 pagesPreliminary ExaminationRen EyNo ratings yet

- CHAPTER 12 - RR REVENUES From Contracts With Customers: Jan 02, 20x5Document13 pagesCHAPTER 12 - RR REVENUES From Contracts With Customers: Jan 02, 20x5Jane DizonNo ratings yet

- Lyceum First Preboard 2020Document3 pagesLyceum First Preboard 2020Jordan Tobiagon100% (1)

- Home Office and Branch Acccounting 2020Document3 pagesHome Office and Branch Acccounting 2020ReilpeterNo ratings yet

- ACT1205 - Module 3 - Audit of InvestmentsDocument6 pagesACT1205 - Module 3 - Audit of InvestmentsIo AyaNo ratings yet

- TERMINAL OUTPUT FOR THE FINAL TERM EditedDocument3 pagesTERMINAL OUTPUT FOR THE FINAL TERM EditedMillen Austria0% (1)

- Karkits Corporation PDFDocument4 pagesKarkits Corporation PDFRachel LeachonNo ratings yet

- AP03-03-Audit of Liabilities - EncryptedDocument7 pagesAP03-03-Audit of Liabilities - EncryptedMark Ehrolle S. SisonNo ratings yet

- This Study Resource Was: Cebu Cpar CenterDocument9 pagesThis Study Resource Was: Cebu Cpar CenterGlizette SamaniegoNo ratings yet

- ACP 311-Accounting For Special Transactions: Installment LiquidationDocument28 pagesACP 311-Accounting For Special Transactions: Installment Liquidationcynthia reyesNo ratings yet

- Part 2 Oblig and Contracts PDFDocument13 pagesPart 2 Oblig and Contracts PDFMichelle PepitoNo ratings yet

- Business Combination and Consolidated FS Part 1Document6 pagesBusiness Combination and Consolidated FS Part 1markNo ratings yet

- Applied Auditing Review Course Pre-Board - Answer KeyDocument13 pagesApplied Auditing Review Course Pre-Board - Answer KeyROMAR A. PIGANo ratings yet

- Aud ProbDocument9 pagesAud ProbKulet AkoNo ratings yet

- BSA 3202 Topic 2 - Joint ArrangementsDocument14 pagesBSA 3202 Topic 2 - Joint ArrangementsjenieNo ratings yet

- AFARicpaDocument23 pagesAFARicpaRegine YbañezNo ratings yet

- Cpa Review School of The Philippines: (P1,832,400-P598,400-P19,200-P180,000-P65,000-P73,000-P178,200)Document10 pagesCpa Review School of The Philippines: (P1,832,400-P598,400-P19,200-P180,000-P65,000-P73,000-P178,200)RIZA LUMAADNo ratings yet

- Quiz Recl FinancingDocument1 pageQuiz Recl FinancingLou Brad IgnacioNo ratings yet

- Ap 9004-IntangiblesDocument5 pagesAp 9004-IntangiblesSirNo ratings yet

- Ncrcup FarDocument13 pagesNcrcup FarKenneth RobledoNo ratings yet

- Advanced Financial Accounting and Reporting: G.P. CostaDocument27 pagesAdvanced Financial Accounting and Reporting: G.P. CostaryanNo ratings yet

- ACCO30053-AACA1 Final-Examination 1st-Semester AY2021-2022 QUESTIONNAIREDocument12 pagesACCO30053-AACA1 Final-Examination 1st-Semester AY2021-2022 QUESTIONNAIREKabalaNo ratings yet

- Exercises On Cash PDFDocument6 pagesExercises On Cash PDFFely MaataNo ratings yet

- DocDocument3 pagesDocWansy Ferrer BallesterosNo ratings yet

- Audit Problems FinalDocument48 pagesAudit Problems FinalShane TabunggaoNo ratings yet

- AP.2904 - Cash and Cash EquivalentsDocument7 pagesAP.2904 - Cash and Cash EquivalentsRNo ratings yet

- Afar Merged PFD Cuties ClubDocument51 pagesAfar Merged PFD Cuties ClubKittenNo ratings yet

- Joint ArrangementDocument3 pagesJoint ArrangementAlliah Mae AcostaNo ratings yet

- Afar.3202 Corporate LiquidationDocument6 pagesAfar.3202 Corporate Liquidationruel c armillaNo ratings yet

- PDF Audit of Cash Roque 2018 1 Compress PDFDocument87 pagesPDF Audit of Cash Roque 2018 1 Compress PDFFernando III PerezNo ratings yet

- Block Section - BS HM TMDocument7 pagesBlock Section - BS HM TMFernando III PerezNo ratings yet

- Block Section - BS Ac MaDocument9 pagesBlock Section - BS Ac MaFernando III PerezNo ratings yet

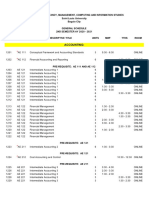

- AM Programs General ScheduleDocument20 pagesAM Programs General ScheduleFernando III PerezNo ratings yet

- Activity 1Document4 pagesActivity 1Fernando III PerezNo ratings yet

- The Relationship Between Working CapitalDocument8 pagesThe Relationship Between Working CapitalFernando III PerezNo ratings yet

- Articles of PartnershipDocument4 pagesArticles of PartnershipFernando III PerezNo ratings yet

- PrE6 Acctg Cycle and JournalizingDocument28 pagesPrE6 Acctg Cycle and JournalizingAlexa Mae SanchezNo ratings yet

- Lobj18 0007008 Question Bank of AccountingDocument223 pagesLobj18 0007008 Question Bank of AccountingHâ HiiNo ratings yet

- Roles Available in Microsoft Dynamics Great Plains 10 (1) .0Document28 pagesRoles Available in Microsoft Dynamics Great Plains 10 (1) .0josephjustNo ratings yet

- Liquidity of Short-Term Assets Related Debt-Paying AbilityDocument32 pagesLiquidity of Short-Term Assets Related Debt-Paying Abilitynadia titaNo ratings yet

- Accounting IA Sample Unit 1Document23 pagesAccounting IA Sample Unit 1CandiceNo ratings yet

- AccountingDocument5 pagesAccountingIhsan UllahNo ratings yet

- Cash Flow StatementDocument16 pagesCash Flow Statementrajesh337masssNo ratings yet

- Auditing - MIDTERM EXAMDocument9 pagesAuditing - MIDTERM EXAMmoNo ratings yet

- Accounting: Page 1 of 3Document3 pagesAccounting: Page 1 of 3Laskar REAZNo ratings yet

- Audit of ReceivableDocument4 pagesAudit of ReceivableMark Lord Morales Bumagat100% (2)

- Accounting Cycle For Merchandising ConcernDocument30 pagesAccounting Cycle For Merchandising ConcernMary100% (2)

- Raymond WC MGMTDocument66 pagesRaymond WC MGMTshwetakhamarNo ratings yet

- Accounting 1A Exam 1 - Spring 2014 - Section 1 - SolutionsDocument9 pagesAccounting 1A Exam 1 - Spring 2014 - Section 1 - SolutionsRishab KhandelwalNo ratings yet

- Ratio Analysis Part 1Document27 pagesRatio Analysis Part 1RAVI KUMARNo ratings yet

- Sec A - Group 3 - Hampton MachineDocument3 pagesSec A - Group 3 - Hampton MachineKasturi senNo ratings yet

- Cash Management in SBI Effect On Their Customers .Docx (3) - 1 (3) (Repaired)Document75 pagesCash Management in SBI Effect On Their Customers .Docx (3) - 1 (3) (Repaired)anas khanNo ratings yet

- Cash and Acrrual Basis QUIZDocument2 pagesCash and Acrrual Basis QUIZMarii M.100% (1)

- AccountsDocument135 pagesAccountsChinnam LalithaNo ratings yet

- I. MULTIPLE CHOICE. Select The Best Answer. Write The LETTER of Your Answer On A Sheet of Paper. Deadline Is On or Before June 7, 2020. (2pts Each)Document9 pagesI. MULTIPLE CHOICE. Select The Best Answer. Write The LETTER of Your Answer On A Sheet of Paper. Deadline Is On or Before June 7, 2020. (2pts Each)Hazel Seguerra BicadaNo ratings yet

- Oracle Open InterfaceDocument95 pagesOracle Open Interfacekishan_73No ratings yet

- Afm Theory NotesDocument28 pagesAfm Theory Notesjagannathreddy kvNo ratings yet

- Key Technical Questions For Finance InterviewsDocument27 pagesKey Technical Questions For Finance InterviewsSeb SNo ratings yet

- Audit of Liabilities Quiz 3Document3 pagesAudit of Liabilities Quiz 3Cattleya50% (2)

- Operating Cycle in Financial ManagementDocument6 pagesOperating Cycle in Financial Managementkamal joshiNo ratings yet

- "Working Capital Management" Dabur IndiaDocument58 pages"Working Capital Management" Dabur Indiatariquewali11100% (2)