Download as docx, pdf, or txt

You might also like

- fkchegg.comDocument4 pagesfkchegg.commisssunshine112No ratings yet

- Key Words: Perceptions Challenges Presumptive Taxation Category C' Tax PayersDocument18 pagesKey Words: Perceptions Challenges Presumptive Taxation Category C' Tax Payersmubarek oumerNo ratings yet

- Chapter Six Audit of Equity Dear Learners! Equity Refers To The Net Worth of The Business, I.E. The Amount Remaining AfterDocument12 pagesChapter Six Audit of Equity Dear Learners! Equity Refers To The Net Worth of The Business, I.E. The Amount Remaining Aftermubarek oumerNo ratings yet

- Zerodha PMLA PolicyDocument8 pagesZerodha PMLA PolicyAbhimanyu Yashwant AltekarNo ratings yet

- Payment & Settlement SystemsDocument50 pagesPayment & Settlement SystemssimpliceNo ratings yet

- Departement of Accounting and Finance Internal: Auditing Practice in Case of Wegagen BankDocument37 pagesDepartement of Accounting and Finance Internal: Auditing Practice in Case of Wegagen BankEyuael Solomon0% (1)

- WegagenDocument63 pagesWegagenYonas100% (1)

- 4 5868236919153887449-1Document49 pages4 5868236919153887449-1Fasiko Asmaro100% (1)

- Chapter OneDocument46 pagesChapter OneHabib Ibrahim100% (1)

- ProclamationDocument7 pagesProclamationBE KALUNo ratings yet

- Budget Administration Performance AnalysDocument70 pagesBudget Administration Performance Analysseblewongel demissie100% (1)

- Proposal by Afize JemalDocument54 pagesProposal by Afize Jemaloumer muktarNo ratings yet

- Cash Management and Public Sector PerforDocument37 pagesCash Management and Public Sector Performutiariska100% (1)

- June, 2016.ethiopiaDocument60 pagesJune, 2016.ethiopiasamuel debebeNo ratings yet

- 1.4. Objective of The StudyDocument5 pages1.4. Objective of The Studymubarek oumerNo ratings yet

- Arens AAS17 SM 22Document17 pagesArens AAS17 SM 22Nurul FarzanaNo ratings yet

- Jimma University: College of Business and Economics Department of Accounting Internal Auditing PracticeDocument6 pagesJimma University: College of Business and Economics Department of Accounting Internal Auditing PracticeReta TolesaNo ratings yet

- Factors Affecting Customer's Adoption of Internet Banking: in Case of Commercial Bank of Ethiopia By: Yoseph Degu WendaDocument58 pagesFactors Affecting Customer's Adoption of Internet Banking: in Case of Commercial Bank of Ethiopia By: Yoseph Degu Wendabereket nigussieNo ratings yet

- Research Proposal Khul Supermarket: Amanuel Wubshet Dagim Desalen Samson Damtew MR - GutaDocument23 pagesResearch Proposal Khul Supermarket: Amanuel Wubshet Dagim Desalen Samson Damtew MR - Gutasami damtewNo ratings yet

- The Revenue Cycle Is A Recurring Set of Business Activities and RelatedDocument6 pagesThe Revenue Cycle Is A Recurring Set of Business Activities and RelatedJna AlyssaNo ratings yet

- Acct II Chapter 4 EdDocument2 pagesAcct II Chapter 4 Edmubarek oumerNo ratings yet

- Misrak SeyoumDocument90 pagesMisrak SeyoumYemane MergiaNo ratings yet

- Chp-4 Capital Project FundDocument8 pagesChp-4 Capital Project FundkasimNo ratings yet

- Expert System For Banking Credit DecisionsDocument32 pagesExpert System For Banking Credit DecisionsBilal Ilyas100% (1)

- ABdiDocument27 pagesABdiferewe tesfayeNo ratings yet

- Research Proposal Assessment of Loan Management in Case of Dashen Bank in Gambella BranchDocument12 pagesResearch Proposal Assessment of Loan Management in Case of Dashen Bank in Gambella Branchnega cheruNo ratings yet

- EDITED INTERNAL AUDITING RESEARCH PAPER First ...... RETADocument42 pagesEDITED INTERNAL AUDITING RESEARCH PAPER First ...... RETAReta TolesaNo ratings yet

- The Payment SystemDocument19 pagesThe Payment SystemLoredana IrinaNo ratings yet

- Amanda 1-5Document68 pagesAmanda 1-5olasmart OluwaleNo ratings yet

- 1.1 Back Ground of The StudyDocument7 pages1.1 Back Ground of The StudyKibretNo ratings yet

- Bikila ResearchDocument57 pagesBikila ResearchBobasa S AhmedNo ratings yet

- Attitude of Students Towards Usage of Social Media in Mizan Tepi University Tepi Campus StudentsDocument26 pagesAttitude of Students Towards Usage of Social Media in Mizan Tepi University Tepi Campus StudentsManamagna OjuluNo ratings yet

- Lesson 2 - Banking Issues in The 21st Century (Compatibility Mode)Document46 pagesLesson 2 - Banking Issues in The 21st Century (Compatibility Mode)Nicky Abela83% (6)

- Payment System Oversight FrameworkDocument16 pagesPayment System Oversight FrameworkNarayanPrajapatiNo ratings yet

- AUDITING PRINCIPLE Complete-Diploma Notes 2020Document153 pagesAUDITING PRINCIPLE Complete-Diploma Notes 2020Kethia Kahashi100% (1)

- 1.2 Objectives of Branch Accounts Parent FirmDocument2 pages1.2 Objectives of Branch Accounts Parent Firmtemedebere0% (1)

- Fraud, Internal Control and Cash: Accounting Principles, Ninth EditionDocument49 pagesFraud, Internal Control and Cash: Accounting Principles, Ninth EditionNuttakan Meesuk100% (1)

- Advance Assignement TwoDocument1 pageAdvance Assignement TwoSolomon AbebeNo ratings yet

- Tilahun BogaleDocument95 pagesTilahun Bogaleguadie workuNo ratings yet

- Rais12 SM CH03Document46 pagesRais12 SM CH03Maliha JahanNo ratings yet

- Financial Accounting 1 Unit 2Document22 pagesFinancial Accounting 1 Unit 2AbdirahmanNo ratings yet

- Biniam HMariamDocument72 pagesBiniam HMariambaya alexNo ratings yet

- Arens AAS17 SM 23Document20 pagesArens AAS17 SM 23Nurul FarzanaNo ratings yet

- Illustration On Special Revenue FundDocument2 pagesIllustration On Special Revenue FundJichang Hik0% (1)

- Internal Control Over Cash of Wegagen BankDocument3 pagesInternal Control Over Cash of Wegagen Bankmubarek oumer100% (10)

- LLLLDocument20 pagesLLLLNavy KizzNo ratings yet

- Technical Guide On Stock and Receivables Audit - IASBDocument15 pagesTechnical Guide On Stock and Receivables Audit - IASBRohil MistryNo ratings yet

- UntitledDocument46 pagesUntitledMagarsaa Qana'iiNo ratings yet

- MESFINMENAMOFINALPAPERMBA2018Document82 pagesMESFINMENAMOFINALPAPERMBA2018Sew 23No ratings yet

- Chapter 21 The Statement of Cash Flows RevisitedDocument123 pagesChapter 21 The Statement of Cash Flows RevisitedkasebNo ratings yet

- Does Microfinance Really Help The Poor? Evidence From Rural Households in EthiopiaDocument16 pagesDoes Microfinance Really Help The Poor? Evidence From Rural Households in EthiopiaZewdu EskeziaNo ratings yet

- Aksum UniversityDocument43 pagesAksum Universitytesfay100% (1)

- Effect of Misrepresentation of Information in A Financial StatementDocument82 pagesEffect of Misrepresentation of Information in A Financial Statementachiever usangaNo ratings yet

- Fundamentals of Accounting Lesson 1 2 Acctng Equation DONEDocument13 pagesFundamentals of Accounting Lesson 1 2 Acctng Equation DONEkim fernandoNo ratings yet

- Gadise Teshome PPDocument6 pagesGadise Teshome PPTewodrose Teklehawariat BelayhunNo ratings yet

- The Revenue Cycle: Sales To Cash Collections: FOSTER School of Business Acctg.320Document37 pagesThe Revenue Cycle: Sales To Cash Collections: FOSTER School of Business Acctg.320Shaina Shanee CuevasNo ratings yet

- Risk Focussed Internal Audit (RFIA) : Top of Form 0 False True 0Document9 pagesRisk Focussed Internal Audit (RFIA) : Top of Form 0 False True 0KARIPELLI PRATHIMANo ratings yet

- Assignment of Advanced Financialaccounting Post Graduate Regular ProgramDocument19 pagesAssignment of Advanced Financialaccounting Post Graduate Regular Programeferem100% (1)

- Docum AntationDocument76 pagesDocum AntationAmanuel KassaNo ratings yet

- Unit 2 Banking SystemDocument16 pagesUnit 2 Banking SystemMoti BekeleNo ratings yet

- Determinants of Foreign Direct Investment in EthiopiaDocument34 pagesDeterminants of Foreign Direct Investment in Ethiopiakedir mohammedNo ratings yet

- Jiksa 1Document34 pagesJiksa 1Abdii DhufeeraNo ratings yet

- Applied Audititng Chapter-OneDocument39 pagesApplied Audititng Chapter-OneKumera Dinkisa ToleraNo ratings yet

- 2.1 Characteristics of Plant Assets: Chapter Two 2 Accounting For Plant Assets and Intanguble AssetsDocument12 pages2.1 Characteristics of Plant Assets: Chapter Two 2 Accounting For Plant Assets and Intanguble Assetsmubarek oumer100% (1)

- Acct II Chapter 1Document10 pagesAcct II Chapter 1mubarek oumerNo ratings yet

- Acct II Chapter 4 EdDocument2 pagesAcct II Chapter 4 Edmubarek oumerNo ratings yet

- Globalization Is About The Interconnectedness of People and Businesses Across The WorldDocument3 pagesGlobalization Is About The Interconnectedness of People and Businesses Across The Worldmubarek oumerNo ratings yet

- Measures of Historical Rates of ReturnDocument2 pagesMeasures of Historical Rates of Returnmubarek oumerNo ratings yet

- Advantages of Indigenous Conflict ResolutionDocument4 pagesAdvantages of Indigenous Conflict Resolutionmubarek oumer100% (1)

- Ch-5 CostDocument24 pagesCh-5 Costmubarek oumerNo ratings yet

- Ch-4 StudentsDocument9 pagesCh-4 Studentsmubarek oumerNo ratings yet

- Chapter Two Audit of Receivables and Sales: Page - 1Document20 pagesChapter Two Audit of Receivables and Sales: Page - 1mubarek oumer100% (1)

- Chapter Seven The Over View of Auditing and Auditors in EthiopiaDocument22 pagesChapter Seven The Over View of Auditing and Auditors in Ethiopiamubarek oumer88% (25)

- Chapter FourDocument18 pagesChapter Fourmubarek oumerNo ratings yet

- Adigrat University Colleg of Bussiness and Economics Department of Accounting and FinaniceDocument53 pagesAdigrat University Colleg of Bussiness and Economics Department of Accounting and Finanicemubarek oumerNo ratings yet

- Chapter FiveDocument14 pagesChapter Fivemubarek oumerNo ratings yet

- Backup of Chapter OneDocument13 pagesBackup of Chapter Onemubarek oumerNo ratings yet

- Advanced Accounting Unit 5Document42 pagesAdvanced Accounting Unit 5mubarek oumerNo ratings yet

- ASTRACTDocument6 pagesASTRACTmubarek oumerNo ratings yet

- Benefits of Critical ThinkingDocument1 pageBenefits of Critical Thinkingmubarek oumerNo ratings yet

- Chapter One: 1.1 Back Ground of The StudyDocument30 pagesChapter One: 1.1 Back Ground of The Studymubarek oumerNo ratings yet

- Agreement of 100m Deal Via SolvenacyvaultDocument7 pagesAgreement of 100m Deal Via Solvenacyvaultjohn carstensNo ratings yet

- Cash AuditDocument9 pagesCash AuditChipo TuyaraNo ratings yet

- Q No.1 Use Following Title of Accounts To Complete Journal Entries of Given TransactionsDocument5 pagesQ No.1 Use Following Title of Accounts To Complete Journal Entries of Given TransactionsNoorNo ratings yet

- Agenda 15 - Transaction Limits in CBS System For Different Types of TransactionsDocument13 pagesAgenda 15 - Transaction Limits in CBS System For Different Types of TransactionsJay MeskaNo ratings yet

- Audit Pre TestDocument13 pagesAudit Pre Testpwcpresident.nfjpia2324No ratings yet

- Account MinistatementDocument7 pagesAccount MinistatementedemaronNo ratings yet

- Risk Management: Del Monte Philippines Inc. (DMPI)Document9 pagesRisk Management: Del Monte Philippines Inc. (DMPI)Pricia AbellaNo ratings yet

- PRELIM Quiz 1 Cash, CE, PCF, Bank ReconDocument8 pagesPRELIM Quiz 1 Cash, CE, PCF, Bank ReconApril Faye de la CruzNo ratings yet

- The Future of Payment in AfricaDocument17 pagesThe Future of Payment in AfricaNegera AbetuNo ratings yet

- Estatement20230611 000237433Document12 pagesEstatement20230611 000237433GUNAWATHY A/P MATHEVAN MoeNo ratings yet

- Annexure IDocument2 pagesAnnexure IscribdaashishNo ratings yet

- Liquidity Management in Janatha Credit Co-Operative Society LTDDocument6 pagesLiquidity Management in Janatha Credit Co-Operative Society LTDInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Final Financial Accounting ZU-019Document2 pagesFinal Financial Accounting ZU-019Iama FeministNo ratings yet

- The Revenue Cycle:: Cash Receipts System FlowchartDocument4 pagesThe Revenue Cycle:: Cash Receipts System FlowchartShyrine EjemNo ratings yet

- NCR NegoSale Batch 15123 062022Document37 pagesNCR NegoSale Batch 15123 062022Patrick LorenzoNo ratings yet

- Financial Statements: Nine Months Ended 31 March, 2009Document22 pagesFinancial Statements: Nine Months Ended 31 March, 2009Muhammad BakhshNo ratings yet

- Cash and Liquidity Management - Topic 3Document47 pagesCash and Liquidity Management - Topic 3kodeNo ratings yet

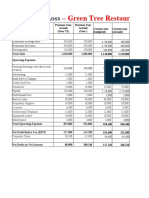

- Restaurant Financial HistoryDocument4 pagesRestaurant Financial HistoryStacy ParkerNo ratings yet

- Exercise 1Document3 pagesExercise 1Nor nimNo ratings yet

- Literature Review On Cash Management PDFDocument4 pagesLiterature Review On Cash Management PDFc5rjgvg7100% (1)

- Chapter 8. Unconventional Equivalence CalculationsDocument18 pagesChapter 8. Unconventional Equivalence CalculationsORK BUNSOKRAKMUNYNo ratings yet

- Demonetisation Essay Download Demonetisation Essay PDF For UPSC PreparationDocument11 pagesDemonetisation Essay Download Demonetisation Essay PDF For UPSC PreparationRahul NimmagaddaNo ratings yet

- CPALE REVIEWER by RDEDocument6 pagesCPALE REVIEWER by RDERachelle Dane EspañolaNo ratings yet

- Cta Level 1 Maf Test 2 - Paper 2 SolutionDocument8 pagesCta Level 1 Maf Test 2 - Paper 2 SolutionMunyaradzi DavvyNo ratings yet

- Assets Integration in New General LedgerDocument3 pagesAssets Integration in New General LedgerMahmoud HabeebNo ratings yet

- Bank Reconciliation StatementDocument6 pagesBank Reconciliation StatementHuma SamuelNo ratings yet

- Role of Technology in BankingDocument34 pagesRole of Technology in BankingPiyush ChavanNo ratings yet

- QSRP 2Document2 pagesQSRP 2Faye LouiseNo ratings yet

- Cfas Pas 1-16Document8 pagesCfas Pas 1-16Sagad KeithNo ratings yet