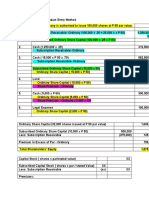

IA Valix 2020 (Problem 4-2 Answer Key)

IA Valix 2020 (Problem 4-2 Answer Key)

You might also like

- INTERMEDIATE ACCOUNTING Vol. 1 (2021 Edition) - Valix, Peralta & Valix - XLSX Chapter 2Document8 pagesINTERMEDIATE ACCOUNTING Vol. 1 (2021 Edition) - Valix, Peralta & Valix - XLSX Chapter 2Rodolfo Manalac100% (1)

- Chapter 4: Accounting For Accounts Receivables: Problem 4-1 Dreamer CompanyDocument4 pagesChapter 4: Accounting For Accounts Receivables: Problem 4-1 Dreamer CompanyDarry Pascua96% (25)

- VALIX - IA 1 (2020 Ver.) Government GrantDocument9 pagesVALIX - IA 1 (2020 Ver.) Government GrantAriean Joy DequiñaNo ratings yet

- IA Valix 2020 (Problem 4-5 To 4-13 Answer Key)Document3 pagesIA Valix 2020 (Problem 4-5 To 4-13 Answer Key)Baby Mushroom67% (3)

- Intermediate Accounting 1 (Far 3) Accounting For Trade and Other ReceivablesDocument6 pagesIntermediate Accounting 1 (Far 3) Accounting For Trade and Other ReceivablesJennilyn BercasioNo ratings yet

- Problem 12-2 To 6Document3 pagesProblem 12-2 To 6MYCO PONCE PAQUENo ratings yet

- ACC 101 - Accounts Receivable Sample ProblemsDocument2 pagesACC 101 - Accounts Receivable Sample ProblemsAdyang71% (7)

- Cost Accounting Chapter5 Exercise1 7Document16 pagesCost Accounting Chapter5 Exercise1 7Baby MushroomNo ratings yet

- Chapter 6 Cost Accounting Problem 1-3Document6 pagesChapter 6 Cost Accounting Problem 1-3Baby MushroomNo ratings yet

- IA Valix 2020 (Problem 4-5 To 4-13 Answer Key)Document3 pagesIA Valix 2020 (Problem 4-5 To 4-13 Answer Key)Baby Mushroom67% (3)

- IA Valix 2020 (Problem 4-1 Answer)Document8 pagesIA Valix 2020 (Problem 4-1 Answer)Baby Mushroom100% (1)

- IA Activity 2 Chapter 4&5Document9 pagesIA Activity 2 Chapter 4&5Sunghoon SsiNo ratings yet

- IA 1 Valix 2020 Ver. Accounts ReceivableDocument8 pagesIA 1 Valix 2020 Ver. Accounts ReceivableAriean Joy DequiñaNo ratings yet

- Chapter4 IA Midterm BuenaventuraDocument10 pagesChapter4 IA Midterm BuenaventuraAnonnNo ratings yet

- Ia-Chap 4&5 SolutionsDocument18 pagesIa-Chap 4&5 SolutionsRoselyn IgartaNo ratings yet

- IA Valix 2020 (Problem 4-4 Answer Key)Document3 pagesIA Valix 2020 (Problem 4-4 Answer Key)Baby MushroomNo ratings yet

- IA Valix 2020 (Problem 4-3 Answer Key) PDFDocument4 pagesIA Valix 2020 (Problem 4-3 Answer Key) PDFBaby MushroomNo ratings yet

- Intermediate Accounting Chapter 23 To 35Document101 pagesIntermediate Accounting Chapter 23 To 35Blue SkyNo ratings yet

- Cabael-Ae109-Proof of CashDocument4 pagesCabael-Ae109-Proof of CashJanine MadriagaNo ratings yet

- Chapter 3-5 To 3-13Document9 pagesChapter 3-5 To 3-13XENA LOPEZNo ratings yet

- Problem 7 - 6 & 7Document2 pagesProblem 7 - 6 & 7Micah April SabularseNo ratings yet

- Intermediate Accounting 1 Valix Chapter 17Document2 pagesIntermediate Accounting 1 Valix Chapter 17Captain Shield100% (1)

- IA Activity 6 AssDocument6 pagesIA Activity 6 AssWeStan LegendsNo ratings yet

- Problem 5-4 5-5Document4 pagesProblem 5-4 5-5Jicelle MendozaNo ratings yet

- IA 1 Valix 2020 Ver. Problem 28Document6 pagesIA 1 Valix 2020 Ver. Problem 28Ariean Joy DequiñaNo ratings yet

- Valix Chapter 20Document22 pagesValix Chapter 20criszel4sobejanaNo ratings yet

- Padernal BSA 1A SW Problem 3 11Document1 pagePadernal BSA 1A SW Problem 3 11Fly ThoughtsNo ratings yet

- Assignment No. 2 (Solution)Document5 pagesAssignment No. 2 (Solution)Christine MalayoNo ratings yet

- Sacrosanct Company Problem 26 - 5 (INTACCS Problem)Document1 pageSacrosanct Company Problem 26 - 5 (INTACCS Problem)Ya NaNo ratings yet

- Affectionate CompanyDocument1 pageAffectionate CompanyAnonnNo ratings yet

- Chapter 1Document10 pagesChapter 1Lyca ArcenaNo ratings yet

- WatatapsDocument29 pagesWatatapsjessa mae zerdaNo ratings yet

- Chapter 33Document7 pagesChapter 33Shane Ivory ClaudioNo ratings yet

- Intermediate Accounting 3 2023 - Chap 1-9 Answer KeyDocument23 pagesIntermediate Accounting 3 2023 - Chap 1-9 Answer Keymain.krisselynreigne.moralesNo ratings yet

- MachineryDocument4 pagesMachineryDianna DayawonNo ratings yet

- Depletion of Universal CompanyDocument2 pagesDepletion of Universal CompanyJerbert JesalvaNo ratings yet

- Dainty Company Requirement: Prepare Journal Entries Debit CreditDocument1 pageDainty Company Requirement: Prepare Journal Entries Debit CreditAnonnNo ratings yet

- Chapter 31Document7 pagesChapter 31AnonnNo ratings yet

- Solution Chapter 20 Intermediate Accounting ValixDocument5 pagesSolution Chapter 20 Intermediate Accounting Valixnameless0% (1)

- Cfas Theories QuizletDocument4 pagesCfas Theories Quizletagm25No ratings yet

- Problem 9-1, 2 & 3Document3 pagesProblem 9-1, 2 & 3Micah April SabularseNo ratings yet

- Adjusted Bank BalanceDocument2 pagesAdjusted Bank BalanceChristy HabelNo ratings yet

- Proof of Cash and Bank Reconciliation - Formula and ExampleDocument5 pagesProof of Cash and Bank Reconciliation - Formula and ExampleJoyce Ericka P. BalonNo ratings yet

- IA Activity 1Document13 pagesIA Activity 1Sunghoon SsiNo ratings yet

- PPE Sample ProblemsDocument5 pagesPPE Sample ProblemsKathleen FrondozoNo ratings yet

- Chapter 2 Conceptual FrameworkDocument8 pagesChapter 2 Conceptual Frameworkdaniella chynnNo ratings yet

- Inventories Part 1 With AnswersDocument9 pagesInventories Part 1 With AnswersDyenNo ratings yet

- Royalty Company Required1 Required5 2020 Required2Document2 pagesRoyalty Company Required1 Required5 2020 Required2AnonnNo ratings yet

- Prelim Exam Accounting 2Document3 pagesPrelim Exam Accounting 2JM Singco Canoy100% (1)

- Chapter 3 (IA Proof Od Cash) PDFDocument6 pagesChapter 3 (IA Proof Od Cash) PDFBaby MushroomNo ratings yet

- Notes ReceivableDocument2 pagesNotes ReceivableGee Lysa Pascua VilbarNo ratings yet

- Accounting 1 - PPEDocument38 pagesAccounting 1 - PPEPortia TurianoNo ratings yet

- Hilarious Company Required 1 300,000 12 Years Required 2Document10 pagesHilarious Company Required 1 300,000 12 Years Required 2Anonn0% (1)

- Ia Problem SolvingDocument3 pagesIa Problem SolvingApple RoncalNo ratings yet

- SUMMARY For INTERMEDIATE ACCOUNTING 2 PDFDocument20 pagesSUMMARY For INTERMEDIATE ACCOUNTING 2 PDFArtisan100% (1)

- Trade and Other Receivables 1. On December 31, 2013, The Accounts Receivable of Harem Company Had A Balance ofDocument11 pagesTrade and Other Receivables 1. On December 31, 2013, The Accounts Receivable of Harem Company Had A Balance ofJude SantosNo ratings yet

- Unit 2 Illustration ProblemDocument1 pageUnit 2 Illustration ProblemCharlene RodrigoNo ratings yet

- Problem 1 2 IAADocument1 pageProblem 1 2 IAAJUARE MaxineNo ratings yet

- Problem 4-2 (IAA)Document6 pagesProblem 4-2 (IAA)Rose Aubrey A CordovaNo ratings yet

- Chapter 4 To Chapter 5Document24 pagesChapter 4 To Chapter 5XENA LOPEZNo ratings yet

- Chap 4 and 5Document18 pagesChap 4 and 5Jerome MonserratNo ratings yet

- RECEIVABLESDocument64 pagesRECEIVABLESKimberly MonserratNo ratings yet

- Activity 4Document2 pagesActivity 4Bernadeth Adelaine DomingoNo ratings yet

- Chapter 5 (Exercise 1-7) CabreraDocument17 pagesChapter 5 (Exercise 1-7) CabreraBaby MushroomNo ratings yet

- 10 Essential Cooking MethodDocument4 pages10 Essential Cooking MethodBaby MushroomNo ratings yet

- What Is Carbonara?: Crispy Pancetta Is My Absolute Favorite Member of The Vegetable FoodDocument2 pagesWhat Is Carbonara?: Crispy Pancetta Is My Absolute Favorite Member of The Vegetable FoodBaby MushroomNo ratings yet

- 101 Tips For CookingDocument8 pages101 Tips For CookingBaby MushroomNo ratings yet

- Cost Accounting Chapter5 Problem1 3Document9 pagesCost Accounting Chapter5 Problem1 3Baby MushroomNo ratings yet

- IA Valix 2020 (Problem 4-3 Answer Key) PDFDocument4 pagesIA Valix 2020 (Problem 4-3 Answer Key) PDFBaby MushroomNo ratings yet

- Cost Accounting Exercise2 3Document2 pagesCost Accounting Exercise2 3Baby MushroomNo ratings yet

- IA Valix 2020 (Problem 4-1 Answer)Document8 pagesIA Valix 2020 (Problem 4-1 Answer)Baby Mushroom100% (1)

- Cost Accounting Chapter 10 Exercise 1 6Document5 pagesCost Accounting Chapter 10 Exercise 1 6Baby MushroomNo ratings yet

- IA Valix 2020 (Problem 4-4 Answer Key)Document3 pagesIA Valix 2020 (Problem 4-4 Answer Key)Baby MushroomNo ratings yet

- IA Valix 2020 (Problem 4-3 Answer Key) PDFDocument4 pagesIA Valix 2020 (Problem 4-3 Answer Key) PDFBaby MushroomNo ratings yet

- IA Valix 2020 (Problem 4-2 Answer Key)Document6 pagesIA Valix 2020 (Problem 4-2 Answer Key)Baby MushroomNo ratings yet

- IA Valix 2020 (Problem 4-4 Answer Key)Document3 pagesIA Valix 2020 (Problem 4-4 Answer Key)Baby MushroomNo ratings yet

- Chapter 3 (Problem 3-5-13) PDFDocument9 pagesChapter 3 (Problem 3-5-13) PDFBaby MushroomNo ratings yet

- IA Valix 2020 (Problem 4-1 Answer)Document8 pagesIA Valix 2020 (Problem 4-1 Answer)Baby Mushroom100% (1)

Download as pdf or txt

You might also like

- INTERMEDIATE ACCOUNTING Vol. 1 (2021 Edition) - Valix, Peralta & Valix - XLSX Chapter 2Document8 pagesINTERMEDIATE ACCOUNTING Vol. 1 (2021 Edition) - Valix, Peralta & Valix - XLSX Chapter 2Rodolfo Manalac100% (1)

- Chapter 4: Accounting For Accounts Receivables: Problem 4-1 Dreamer CompanyDocument4 pagesChapter 4: Accounting For Accounts Receivables: Problem 4-1 Dreamer CompanyDarry Pascua96% (25)

- VALIX - IA 1 (2020 Ver.) Government GrantDocument9 pagesVALIX - IA 1 (2020 Ver.) Government GrantAriean Joy DequiñaNo ratings yet

- IA Valix 2020 (Problem 4-5 To 4-13 Answer Key)Document3 pagesIA Valix 2020 (Problem 4-5 To 4-13 Answer Key)Baby Mushroom67% (3)

- Intermediate Accounting 1 (Far 3) Accounting For Trade and Other ReceivablesDocument6 pagesIntermediate Accounting 1 (Far 3) Accounting For Trade and Other ReceivablesJennilyn BercasioNo ratings yet

- Problem 12-2 To 6Document3 pagesProblem 12-2 To 6MYCO PONCE PAQUENo ratings yet

- ACC 101 - Accounts Receivable Sample ProblemsDocument2 pagesACC 101 - Accounts Receivable Sample ProblemsAdyang71% (7)

- Cost Accounting Chapter5 Exercise1 7Document16 pagesCost Accounting Chapter5 Exercise1 7Baby MushroomNo ratings yet

- Chapter 6 Cost Accounting Problem 1-3Document6 pagesChapter 6 Cost Accounting Problem 1-3Baby MushroomNo ratings yet

- IA Valix 2020 (Problem 4-5 To 4-13 Answer Key)Document3 pagesIA Valix 2020 (Problem 4-5 To 4-13 Answer Key)Baby Mushroom67% (3)

- IA Valix 2020 (Problem 4-1 Answer)Document8 pagesIA Valix 2020 (Problem 4-1 Answer)Baby Mushroom100% (1)

- IA Activity 2 Chapter 4&5Document9 pagesIA Activity 2 Chapter 4&5Sunghoon SsiNo ratings yet

- IA 1 Valix 2020 Ver. Accounts ReceivableDocument8 pagesIA 1 Valix 2020 Ver. Accounts ReceivableAriean Joy DequiñaNo ratings yet

- Chapter4 IA Midterm BuenaventuraDocument10 pagesChapter4 IA Midterm BuenaventuraAnonnNo ratings yet

- Ia-Chap 4&5 SolutionsDocument18 pagesIa-Chap 4&5 SolutionsRoselyn IgartaNo ratings yet

- IA Valix 2020 (Problem 4-4 Answer Key)Document3 pagesIA Valix 2020 (Problem 4-4 Answer Key)Baby MushroomNo ratings yet

- IA Valix 2020 (Problem 4-3 Answer Key) PDFDocument4 pagesIA Valix 2020 (Problem 4-3 Answer Key) PDFBaby MushroomNo ratings yet

- Intermediate Accounting Chapter 23 To 35Document101 pagesIntermediate Accounting Chapter 23 To 35Blue SkyNo ratings yet

- Cabael-Ae109-Proof of CashDocument4 pagesCabael-Ae109-Proof of CashJanine MadriagaNo ratings yet

- Chapter 3-5 To 3-13Document9 pagesChapter 3-5 To 3-13XENA LOPEZNo ratings yet

- Problem 7 - 6 & 7Document2 pagesProblem 7 - 6 & 7Micah April SabularseNo ratings yet

- Intermediate Accounting 1 Valix Chapter 17Document2 pagesIntermediate Accounting 1 Valix Chapter 17Captain Shield100% (1)

- IA Activity 6 AssDocument6 pagesIA Activity 6 AssWeStan LegendsNo ratings yet

- Problem 5-4 5-5Document4 pagesProblem 5-4 5-5Jicelle MendozaNo ratings yet

- IA 1 Valix 2020 Ver. Problem 28Document6 pagesIA 1 Valix 2020 Ver. Problem 28Ariean Joy DequiñaNo ratings yet

- Valix Chapter 20Document22 pagesValix Chapter 20criszel4sobejanaNo ratings yet

- Padernal BSA 1A SW Problem 3 11Document1 pagePadernal BSA 1A SW Problem 3 11Fly ThoughtsNo ratings yet

- Assignment No. 2 (Solution)Document5 pagesAssignment No. 2 (Solution)Christine MalayoNo ratings yet

- Sacrosanct Company Problem 26 - 5 (INTACCS Problem)Document1 pageSacrosanct Company Problem 26 - 5 (INTACCS Problem)Ya NaNo ratings yet

- Affectionate CompanyDocument1 pageAffectionate CompanyAnonnNo ratings yet

- Chapter 1Document10 pagesChapter 1Lyca ArcenaNo ratings yet

- WatatapsDocument29 pagesWatatapsjessa mae zerdaNo ratings yet

- Chapter 33Document7 pagesChapter 33Shane Ivory ClaudioNo ratings yet

- Intermediate Accounting 3 2023 - Chap 1-9 Answer KeyDocument23 pagesIntermediate Accounting 3 2023 - Chap 1-9 Answer Keymain.krisselynreigne.moralesNo ratings yet

- MachineryDocument4 pagesMachineryDianna DayawonNo ratings yet

- Depletion of Universal CompanyDocument2 pagesDepletion of Universal CompanyJerbert JesalvaNo ratings yet

- Dainty Company Requirement: Prepare Journal Entries Debit CreditDocument1 pageDainty Company Requirement: Prepare Journal Entries Debit CreditAnonnNo ratings yet

- Chapter 31Document7 pagesChapter 31AnonnNo ratings yet

- Solution Chapter 20 Intermediate Accounting ValixDocument5 pagesSolution Chapter 20 Intermediate Accounting Valixnameless0% (1)

- Cfas Theories QuizletDocument4 pagesCfas Theories Quizletagm25No ratings yet

- Problem 9-1, 2 & 3Document3 pagesProblem 9-1, 2 & 3Micah April SabularseNo ratings yet

- Adjusted Bank BalanceDocument2 pagesAdjusted Bank BalanceChristy HabelNo ratings yet

- Proof of Cash and Bank Reconciliation - Formula and ExampleDocument5 pagesProof of Cash and Bank Reconciliation - Formula and ExampleJoyce Ericka P. BalonNo ratings yet

- IA Activity 1Document13 pagesIA Activity 1Sunghoon SsiNo ratings yet

- PPE Sample ProblemsDocument5 pagesPPE Sample ProblemsKathleen FrondozoNo ratings yet

- Chapter 2 Conceptual FrameworkDocument8 pagesChapter 2 Conceptual Frameworkdaniella chynnNo ratings yet

- Inventories Part 1 With AnswersDocument9 pagesInventories Part 1 With AnswersDyenNo ratings yet

- Royalty Company Required1 Required5 2020 Required2Document2 pagesRoyalty Company Required1 Required5 2020 Required2AnonnNo ratings yet

- Prelim Exam Accounting 2Document3 pagesPrelim Exam Accounting 2JM Singco Canoy100% (1)

- Chapter 3 (IA Proof Od Cash) PDFDocument6 pagesChapter 3 (IA Proof Od Cash) PDFBaby MushroomNo ratings yet

- Notes ReceivableDocument2 pagesNotes ReceivableGee Lysa Pascua VilbarNo ratings yet

- Accounting 1 - PPEDocument38 pagesAccounting 1 - PPEPortia TurianoNo ratings yet

- Hilarious Company Required 1 300,000 12 Years Required 2Document10 pagesHilarious Company Required 1 300,000 12 Years Required 2Anonn0% (1)

- Ia Problem SolvingDocument3 pagesIa Problem SolvingApple RoncalNo ratings yet

- SUMMARY For INTERMEDIATE ACCOUNTING 2 PDFDocument20 pagesSUMMARY For INTERMEDIATE ACCOUNTING 2 PDFArtisan100% (1)

- Trade and Other Receivables 1. On December 31, 2013, The Accounts Receivable of Harem Company Had A Balance ofDocument11 pagesTrade and Other Receivables 1. On December 31, 2013, The Accounts Receivable of Harem Company Had A Balance ofJude SantosNo ratings yet

- Unit 2 Illustration ProblemDocument1 pageUnit 2 Illustration ProblemCharlene RodrigoNo ratings yet

- Problem 1 2 IAADocument1 pageProblem 1 2 IAAJUARE MaxineNo ratings yet

- Problem 4-2 (IAA)Document6 pagesProblem 4-2 (IAA)Rose Aubrey A CordovaNo ratings yet

- Chapter 4 To Chapter 5Document24 pagesChapter 4 To Chapter 5XENA LOPEZNo ratings yet

- Chap 4 and 5Document18 pagesChap 4 and 5Jerome MonserratNo ratings yet

- RECEIVABLESDocument64 pagesRECEIVABLESKimberly MonserratNo ratings yet

- Activity 4Document2 pagesActivity 4Bernadeth Adelaine DomingoNo ratings yet

- Chapter 5 (Exercise 1-7) CabreraDocument17 pagesChapter 5 (Exercise 1-7) CabreraBaby MushroomNo ratings yet

- 10 Essential Cooking MethodDocument4 pages10 Essential Cooking MethodBaby MushroomNo ratings yet

- What Is Carbonara?: Crispy Pancetta Is My Absolute Favorite Member of The Vegetable FoodDocument2 pagesWhat Is Carbonara?: Crispy Pancetta Is My Absolute Favorite Member of The Vegetable FoodBaby MushroomNo ratings yet

- 101 Tips For CookingDocument8 pages101 Tips For CookingBaby MushroomNo ratings yet

- Cost Accounting Chapter5 Problem1 3Document9 pagesCost Accounting Chapter5 Problem1 3Baby MushroomNo ratings yet

- IA Valix 2020 (Problem 4-3 Answer Key) PDFDocument4 pagesIA Valix 2020 (Problem 4-3 Answer Key) PDFBaby MushroomNo ratings yet

- Cost Accounting Exercise2 3Document2 pagesCost Accounting Exercise2 3Baby MushroomNo ratings yet

- IA Valix 2020 (Problem 4-1 Answer)Document8 pagesIA Valix 2020 (Problem 4-1 Answer)Baby Mushroom100% (1)

- Cost Accounting Chapter 10 Exercise 1 6Document5 pagesCost Accounting Chapter 10 Exercise 1 6Baby MushroomNo ratings yet

- IA Valix 2020 (Problem 4-4 Answer Key)Document3 pagesIA Valix 2020 (Problem 4-4 Answer Key)Baby MushroomNo ratings yet

- IA Valix 2020 (Problem 4-3 Answer Key) PDFDocument4 pagesIA Valix 2020 (Problem 4-3 Answer Key) PDFBaby MushroomNo ratings yet

- IA Valix 2020 (Problem 4-2 Answer Key)Document6 pagesIA Valix 2020 (Problem 4-2 Answer Key)Baby MushroomNo ratings yet

- IA Valix 2020 (Problem 4-4 Answer Key)Document3 pagesIA Valix 2020 (Problem 4-4 Answer Key)Baby MushroomNo ratings yet

- Chapter 3 (Problem 3-5-13) PDFDocument9 pagesChapter 3 (Problem 3-5-13) PDFBaby MushroomNo ratings yet

- IA Valix 2020 (Problem 4-1 Answer)Document8 pagesIA Valix 2020 (Problem 4-1 Answer)Baby Mushroom100% (1)