Download as pdf or txt

You might also like

- Case 21Document14 pagesCase 21Gabriela LueiroNo ratings yet

- Chapter 16 Sol 2020 WKDocument53 pagesChapter 16 Sol 2020 WKVu Khanh LeNo ratings yet

- CBSE Class 12 Accountancy Important FormulasDocument3 pagesCBSE Class 12 Accountancy Important Formulasrio_harcan100% (2)

- CFAP 1 AAFR Summer 2017Document10 pagesCFAP 1 AAFR Summer 2017Aqib SheikhNo ratings yet

- Capital Reduction & Reconstruction: Liability AssetsDocument10 pagesCapital Reduction & Reconstruction: Liability AssetsOnaderu Oluwagbenga EnochNo ratings yet

- Wesco Financial Corporation: To Our ShareholdersDocument8 pagesWesco Financial Corporation: To Our ShareholdersChidananda SahuNo ratings yet

- Wesco Financial Corporation: To Our ShareholdersDocument8 pagesWesco Financial Corporation: To Our ShareholdersChidananda SahuNo ratings yet

- Wesco Financial Corporation: To Our ShareholdersDocument8 pagesWesco Financial Corporation: To Our ShareholdersChidananda SahuNo ratings yet

- Wesco Financial Corporation: Letter To Shareholders To Our ShareholdersDocument8 pagesWesco Financial Corporation: Letter To Shareholders To Our ShareholdersChidananda SahuNo ratings yet

- Wesco Financial Corporation: Letter To Shareholders To Our ShareholdersDocument9 pagesWesco Financial Corporation: Letter To Shareholders To Our ShareholdersChidananda SahuNo ratings yet

- Wesco Financial Corporation: Letter To Shareholders To Our ShareholdersDocument7 pagesWesco Financial Corporation: Letter To Shareholders To Our ShareholdersChidananda SahuNo ratings yet

- Wesco Shareholder Letter 2007Document7 pagesWesco Shareholder Letter 2007eblochNo ratings yet

- Wesco Financial Corporation: Letter To Shareholders To Our ShareholdersDocument9 pagesWesco Financial Corporation: Letter To Shareholders To Our ShareholdersChidananda Sahu100% (1)

- Wesco Financial Corporation: Letter To Shareholders To Our ShareholdersDocument9 pagesWesco Financial Corporation: Letter To Shareholders To Our ShareholdersChidananda SahuNo ratings yet

- Wesco Financial Corporation: Letter To Shareholders To Our ShareholdersDocument8 pagesWesco Financial Corporation: Letter To Shareholders To Our ShareholdersChidananda SahuNo ratings yet

- Wesco Financial Corporation: Letter To Shareholders To Our ShareholdersDocument7 pagesWesco Financial Corporation: Letter To Shareholders To Our ShareholdersChidananda SahuNo ratings yet

- Wesco Financial Corporation: Letter To Shareholders To Our ShareholdersDocument7 pagesWesco Financial Corporation: Letter To Shareholders To Our ShareholdersstiggonNo ratings yet

- W. R. Berkley Corporation Reports Third Quarter Results: Net Income of $94 Million, Book Value Per Share Up 6%Document6 pagesW. R. Berkley Corporation Reports Third Quarter Results: Net Income of $94 Million, Book Value Per Share Up 6%Tariq AliNo ratings yet

- X423.8 Assignment 8Document5 pagesX423.8 Assignment 8FBNo ratings yet

- Wesco Financial Munger LettersDocument286 pagesWesco Financial Munger LettersIrelandYardNo ratings yet

- Laporan Keuangan Dan PajakDocument39 pagesLaporan Keuangan Dan PajakpurnamaNo ratings yet

- Accounting For Financial ManagementDocument42 pagesAccounting For Financial ManagementTIDURLANo ratings yet

- Wesco Charlie Munger Letters 1983 2009 CollectionDocument286 pagesWesco Charlie Munger Letters 1983 2009 Collectionevolve_usNo ratings yet

- Laporan Keuangan Dan PajakDocument39 pagesLaporan Keuangan Dan PajakFerry JohNo ratings yet

- Solutiondone 2-225Document1 pageSolutiondone 2-225trilocksp SinghNo ratings yet

- Wesco Charlie Munger Letters 1983 - 2009 CollectionDocument286 pagesWesco Charlie Munger Letters 1983 - 2009 Collectionbomby0100% (2)

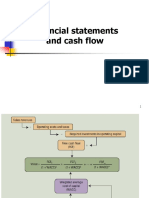

- Financial Statements, Cash Flow, and TaxesDocument43 pagesFinancial Statements, Cash Flow, and TaxesshimulNo ratings yet

- DeVry University Walmart ProjectDocument12 pagesDeVry University Walmart ProjectKristin ParkerNo ratings yet

- 2022EOFYSummaryDocument3 pages2022EOFYSummaryHanny KeeNo ratings yet

- Corporate FinanceDocument25 pagesCorporate FinanceTrần Ngọc TrungNo ratings yet

- UBL Annual Report 2018-158Document1 pageUBL Annual Report 2018-158IFRS LabNo ratings yet

- FM12 CH 03 ShowDocument30 pagesFM12 CH 03 ShowMagued MamdouhNo ratings yet

- Nasdaq Aaon 2003 2Document27 pagesNasdaq Aaon 2003 2Abi ZelekeNo ratings yet

- Lec 6Document26 pagesLec 6Mohamed AliNo ratings yet

- Case Solutions CH (1-8) II PDFDocument21 pagesCase Solutions CH (1-8) II PDFMajed MansourNo ratings yet

- Week 7 NotesDocument6 pagesWeek 7 NotescalebNo ratings yet

- Wesco 1990 Letter To ShareholdersDocument20 pagesWesco 1990 Letter To ShareholdersBuySideMetricsNo ratings yet

- SD 05684602Document13 pagesSD 05684602Miguel gagoNo ratings yet

- Tire City Inc.Document6 pagesTire City Inc.Samta Singh YadavNo ratings yet

- Chairman's Letter - 1978Document9 pagesChairman's Letter - 1978SuperGuyNo ratings yet

- The Smythe Davidson Corporation Just Issued Its Annual Report The CurrentDocument1 pageThe Smythe Davidson Corporation Just Issued Its Annual Report The CurrentMuhammad ShahidNo ratings yet

- Audited Consolidated Financial StatementDocument42 pagesAudited Consolidated Financial StatementAbigail EjiroNo ratings yet

- ACY4001 Individual Assignment 2 SolutionsDocument7 pagesACY4001 Individual Assignment 2 SolutionsMorris LoNo ratings yet

- 1987 PDFDocument26 pages1987 PDFAbhishek GauravNo ratings yet

- CH 05 - Suggested Study Questions With AnswersDocument11 pagesCH 05 - Suggested Study Questions With AnswersLuong Hoang VuNo ratings yet

- Capital Structure of TCSDocument36 pagesCapital Structure of TCSpassinikunj50% (2)

- SBR Mock1 As - s20 j21Document14 pagesSBR Mock1 As - s20 j21percy mapetereNo ratings yet

- Chairman's Letter - 1978Document10 pagesChairman's Letter - 1978Vinayak MegharajNo ratings yet

- Study Unit 20Document13 pagesStudy Unit 20Hazem El SayedNo ratings yet

- Financial Statements, Cash Flow, and TaxesDocument40 pagesFinancial Statements, Cash Flow, and TaxesKamran Ali AnsariNo ratings yet

- Purchase-Price Accounting Adjustments and The "Cash Flow" FallacyDocument6 pagesPurchase-Price Accounting Adjustments and The "Cash Flow" Fallacyfuckyouscribd12345No ratings yet

- CH 6 Case 4Document3 pagesCH 6 Case 4Hazem HalabiNo ratings yet

- Clase 1 Casos en Finanzas UDDDocument35 pagesClase 1 Casos en Finanzas UDDJuan Gallegos M.No ratings yet

- Chapter 15Document42 pagesChapter 15Ivo_Nicht100% (1)

- Kuwait Privatisation Project Holding Company K.S.C. (Closed) (Formerly Kuwait Privatisation Project Company K.S.C. (Closed)Document12 pagesKuwait Privatisation Project Holding Company K.S.C. (Closed) (Formerly Kuwait Privatisation Project Company K.S.C. (Closed)phckuwaitNo ratings yet

- 2007 Bos RaDocument93 pages2007 Bos RasaxobobNo ratings yet

- Material 1.1 Additional NotesDocument2 pagesMaterial 1.1 Additional NotesCristine Joy BenitezNo ratings yet

- FM in Construction 2Document23 pagesFM in Construction 2YosiNo ratings yet

- PPP Unit 1Document37 pagesPPP Unit 1nandaamaharajhNo ratings yet

- IAS 30 and IFRS 7 CPA Anthony NjiruDocument51 pagesIAS 30 and IFRS 7 CPA Anthony NjiruMovie MovieNo ratings yet

- Verizon Foundation - IRS 990 - Year 2008Document317 pagesVerizon Foundation - IRS 990 - Year 2008CaliforniaALLExposedNo ratings yet

- Dividend Growth Investing: A Step-by-Step Guide to Building a Dividend Portfolio for Early RetirementFrom EverandDividend Growth Investing: A Step-by-Step Guide to Building a Dividend Portfolio for Early RetirementNo ratings yet

- Wesco Financial Corporation: To Our ShareholdersDocument8 pagesWesco Financial Corporation: To Our ShareholdersChidananda SahuNo ratings yet

- Wesco Financial Corporation: To Our ShareholdersDocument8 pagesWesco Financial Corporation: To Our ShareholdersChidananda SahuNo ratings yet

- Wesco Financial Corporation: Letter To Shareholders To Our ShareholdersDocument9 pagesWesco Financial Corporation: Letter To Shareholders To Our ShareholdersChidananda Sahu100% (1)

- Wesco Financial Corporation: Letter To Shareholders To Our ShareholdersDocument8 pagesWesco Financial Corporation: Letter To Shareholders To Our ShareholdersChidananda SahuNo ratings yet

- Wesco Financial Corporation: Letter To Shareholders To Our ShareholdersDocument7 pagesWesco Financial Corporation: Letter To Shareholders To Our ShareholdersChidananda SahuNo ratings yet

- Wesco Financial Corporation: Letter To Shareholders To Our ShareholdersDocument9 pagesWesco Financial Corporation: Letter To Shareholders To Our ShareholdersChidananda SahuNo ratings yet

- Wesco Financial Corporation: To Our ShareholdersDocument8 pagesWesco Financial Corporation: To Our ShareholdersChidananda SahuNo ratings yet

- Wesco Financial Corporation: Letter To Shareholders To Our ShareholdersDocument8 pagesWesco Financial Corporation: Letter To Shareholders To Our ShareholdersChidananda SahuNo ratings yet

- Wesco Financial Corporation: Letter To Shareholders To Our ShareholdersDocument7 pagesWesco Financial Corporation: Letter To Shareholders To Our ShareholdersChidananda SahuNo ratings yet

- Wesco Financial Corporation: Letter To Shareholders To Our ShareholdersDocument9 pagesWesco Financial Corporation: Letter To Shareholders To Our ShareholdersChidananda SahuNo ratings yet

- State/UT Wise Aadhaar Saturation 30th April, 2020Document3 pagesState/UT Wise Aadhaar Saturation 30th April, 2020Chidananda SahuNo ratings yet

- Revision Test Paper Cap-Ii: Advanced Accounting Questions Accounting For DepartmentsDocument279 pagesRevision Test Paper Cap-Ii: Advanced Accounting Questions Accounting For Departmentsshankar k.c.No ratings yet

- MFRS Glossary in Bahasa Malaysia - July2015Document66 pagesMFRS Glossary in Bahasa Malaysia - July2015Muhammad Yunus KamilNo ratings yet

- ACT NO. 2581, Commonly Known As Blue Sky LawDocument3 pagesACT NO. 2581, Commonly Known As Blue Sky LawLawstudesNo ratings yet

- 2013 03 07 - Ebix All Distraction No Clarity - FinalDocument19 pages2013 03 07 - Ebix All Distraction No Clarity - FinalgothamcityresearchNo ratings yet

- Financial Accounting Disposal of Asset and Good Will Week 3Document28 pagesFinancial Accounting Disposal of Asset and Good Will Week 3Hania SohailNo ratings yet

- CA Final Financial Reporting Self Study Notes by Ashwani JMLK3HFFDocument46 pagesCA Final Financial Reporting Self Study Notes by Ashwani JMLK3HFFJashwanthNo ratings yet

- Assignment Front Sheet: Qualification BTEC Level 4 HND Diploma in BusinessDocument17 pagesAssignment Front Sheet: Qualification BTEC Level 4 HND Diploma in BusinessNguyen Duc Quang (BTEC HN)No ratings yet

- Consolidation Wholly Owned With DifferentialDocument4 pagesConsolidation Wholly Owned With DifferentialashibhallauNo ratings yet

- D2Document12 pagesD2neo14No ratings yet

- Materi Lab 3 - Stock Investment PDFDocument4 pagesMateri Lab 3 - Stock Investment PDFPUTRI YANINo ratings yet

- 04 Change in Profit Sharing RatioDocument6 pages04 Change in Profit Sharing RatioSushant Giri GoswamiNo ratings yet

- Bryan Luke AKL SP WEEK 3Document6 pagesBryan Luke AKL SP WEEK 3Bryan LukeNo ratings yet

- Small and Medium-Sized Entities (Smes) : Page 1 of 6Document6 pagesSmall and Medium-Sized Entities (Smes) : Page 1 of 6globeth berbanoNo ratings yet

- AfarDocument11 pagesAfarDonna Mae HernandezNo ratings yet

- Introduction To Valuation: Case: Liston Mechanics CorporationDocument9 pagesIntroduction To Valuation: Case: Liston Mechanics CorporationKunal MehtaNo ratings yet

- Audit Problems 1 - PPE and IntangiblesDocument10 pagesAudit Problems 1 - PPE and IntangiblesPaula De RuedaNo ratings yet

- Afar Quizzer On Consolidation (Ifrs 10)Document9 pagesAfar Quizzer On Consolidation (Ifrs 10)john paul100% (1)

- Intangible AssetsDocument4 pagesIntangible AssetsDianna DayawonNo ratings yet

- Contracts Project RakshaDocument8 pagesContracts Project RakshaUdhithaa S K KotaNo ratings yet

- Dwnload Full Advanced Accounting 10th Edition Hoyle Solutions Manual PDFDocument22 pagesDwnload Full Advanced Accounting 10th Edition Hoyle Solutions Manual PDFwilliambrowntdoypjmnrc100% (19)

- Coke-Pepsi Part IIDocument56 pagesCoke-Pepsi Part IItkkt1015No ratings yet

- Solution Question in LMSDocument3 pagesSolution Question in LMSVMRONo ratings yet

- CFA Level 1 Practice Test 1 - 300hoursDocument21 pagesCFA Level 1 Practice Test 1 - 300hoursEstefany MariáteguiNo ratings yet

- Chapter 16Document27 pagesChapter 16Red Christian Palustre100% (1)

- P1 - Corporate Reporting April 09Document21 pagesP1 - Corporate Reporting April 09IrfanNo ratings yet

- My CoursesDocument23 pagesMy CoursesCasper John Nanas MuñozNo ratings yet

- Sample ProblemDocument3 pagesSample ProblemZaldy Magante MalasagaNo ratings yet