Download as pdf or txt

You might also like

- Use Cases For Example ATM SystemDocument54 pagesUse Cases For Example ATM SystemGayatri SharmaNo ratings yet

- Fiji Resort Marketing PlanDocument3 pagesFiji Resort Marketing PlanFinyxcoreNo ratings yet

- Technical Note Guidance On Corrosion Assessment of Ex EquipmentDocument7 pagesTechnical Note Guidance On Corrosion Assessment of Ex EquipmentParthiban NagarajanNo ratings yet

- Global Outlook MRODocument20 pagesGlobal Outlook MROryanyangyuNo ratings yet

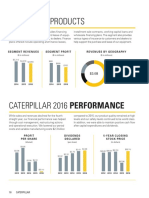

- Pages From 2016 Cat Ar-5Document1 pagePages From 2016 Cat Ar-5EngTamerNo ratings yet

- Long Term Outlook For Exploration - Richard Schodde - Minex Consulting, July 2013.Document53 pagesLong Term Outlook For Exploration - Richard Schodde - Minex Consulting, July 2013.Glenn ViklundNo ratings yet

- 011510Document211 pages011510Ann Arbor Government DocumentsNo ratings yet

- Chapter 1 ExerciseDocument4 pagesChapter 1 ExerciseCoffee JellyNo ratings yet

- Mutual Fund: Prepared For Empirical Asset Pricing Class at SAIFDocument25 pagesMutual Fund: Prepared For Empirical Asset Pricing Class at SAIFJoe23232232No ratings yet

- IFAB 2011 MarketsDocument80 pagesIFAB 2011 MarketscoriolisresearchNo ratings yet

- Private Debt Primer Oct 2023Document24 pagesPrivate Debt Primer Oct 2023Amber GuptaNo ratings yet

- Session 3 - Preety BhandariDocument30 pagesSession 3 - Preety Bhandari111No ratings yet

- Market Study: Plastic Films - WorldDocument7 pagesMarket Study: Plastic Films - WorldMikiskopjeNo ratings yet

- Iieiere: Be#Ftrtmettt FT AefyttffttssttDocument2 pagesIieiere: Be#Ftrtmettt FT AefyttffttssttRenzzyBautistaNo ratings yet

- 2011 Group Full Presentation - WEB English VersionDocument39 pages2011 Group Full Presentation - WEB English Versionosama anterNo ratings yet

- Knowledge Objectives: Understand The 4 Strategies For Foreign Expansion Understand The Benefits From Foreign ExpansionDocument24 pagesKnowledge Objectives: Understand The 4 Strategies For Foreign Expansion Understand The Benefits From Foreign Expansionravi_nyseNo ratings yet

- Global Marine Insurance Report 5ba3751806ccbDocument55 pagesGlobal Marine Insurance Report 5ba3751806ccb2250000046No ratings yet

- Rockefeller University GivingDocument2 pagesRockefeller University Givingelijoja06No ratings yet

- FDI Trends2006 2007 UnctadDocument16 pagesFDI Trends2006 2007 UnctadVictorFaucheretNo ratings yet

- World Pressure Sensitive Tapes - Current Overview and Future GrowthDocument36 pagesWorld Pressure Sensitive Tapes - Current Overview and Future GrowthNestor PaitaNo ratings yet

- Aid and Ebb Tide: A History of CIDA and Canadian Development AssistanceFrom EverandAid and Ebb Tide: A History of CIDA and Canadian Development AssistanceNo ratings yet

- The World of International Economics: Mcgraw-Hill/IrwinDocument21 pagesThe World of International Economics: Mcgraw-Hill/IrwinLA SyamsulNo ratings yet

- DOW Presentation at ECPA GA Jan262017 SharedDocument35 pagesDOW Presentation at ECPA GA Jan262017 SharedYu-Chih LinNo ratings yet

- 2 Impact of FDI and Trade On Environmental Quality in The CAFTA-DR RegionDocument7 pages2 Impact of FDI and Trade On Environmental Quality in The CAFTA-DR RegionNguyễn Thị Ngọc PhượngNo ratings yet

- Tutorial Letter 202/2021: International TradeDocument13 pagesTutorial Letter 202/2021: International TradetawandaNo ratings yet

- Benchmarking Study: Comparison of Performance in The E&P Upstream BusinessDocument17 pagesBenchmarking Study: Comparison of Performance in The E&P Upstream BusinessDeepesh PathakNo ratings yet

- Ir Introduction To DandE Unilever Brazil Tcm13-163693Document11 pagesIr Introduction To DandE Unilever Brazil Tcm13-163693Insomniac100% (2)

- TI FactsandFigures 2019Document6 pagesTI FactsandFigures 2019mNo ratings yet

- Oxfam's DFID CHASE PPA Year Three Annual ReviewDocument86 pagesOxfam's DFID CHASE PPA Year Three Annual ReviewOxfamNo ratings yet

- Oxfam's DFID CHASE PPA Year Three Annual ReviewDocument86 pagesOxfam's DFID CHASE PPA Year Three Annual ReviewOxfamNo ratings yet

- Oxfam's DFID CHASE PPA Year Three Annual ReviewDocument86 pagesOxfam's DFID CHASE PPA Year Three Annual ReviewOxfamNo ratings yet

- Oxfam's DFID CHASE PPA Year Three Annual ReviewDocument86 pagesOxfam's DFID CHASE PPA Year Three Annual ReviewOxfamNo ratings yet

- Oxfam's DFID CHASE PPA Year Three Annual ReviewDocument86 pagesOxfam's DFID CHASE PPA Year Three Annual ReviewOxfamNo ratings yet

- Strateges in International Context: Presented To Garima Tomar Presented by Puneet Ratnam Enroll-9147 spec.-I.BDocument26 pagesStrateges in International Context: Presented To Garima Tomar Presented by Puneet Ratnam Enroll-9147 spec.-I.BPuneet RatnamNo ratings yet

- WTO Anti - Dumping NegotiationsDocument26 pagesWTO Anti - Dumping NegotiationsashastriNo ratings yet

- Global Office Real Estate Review Midyear 2010Document30 pagesGlobal Office Real Estate Review Midyear 2010Colliers International ThailandNo ratings yet

- Joe BennecheDocument28 pagesJoe BennecheAsad AliNo ratings yet

- Chapter 10Document14 pagesChapter 10Zhairra Mae ElaironNo ratings yet

- External Debt Sustainability in AFRIQUEDocument23 pagesExternal Debt Sustainability in AFRIQUEsami kamlNo ratings yet

- Shipping Guarantee Fees 09122023Document1 pageShipping Guarantee Fees 09122023Raihan AdantinoNo ratings yet

- TSI-Article Pro 004Document6 pagesTSI-Article Pro 004Pat PathairushNo ratings yet

- Chapter 7 - International Strategy - Creating Value in Global MarketsDocument9 pagesChapter 7 - International Strategy - Creating Value in Global MarketsELMUNTHIR BEN AMMARNo ratings yet

- Mental Wellness Market by RegionDocument1 pageMental Wellness Market by RegionPrachi PandeyNo ratings yet

- 1 OverviewandUpdateotheGEF (Emilia Marieta)Document33 pages1 OverviewandUpdateotheGEF (Emilia Marieta)Zekuwan YusufNo ratings yet

- Cbi Sotm 2019 Vol1 04dDocument16 pagesCbi Sotm 2019 Vol1 04dAnthony StevenNo ratings yet

- Kahoot Company Presentation18September2019Document32 pagesKahoot Company Presentation18September2019Milton CocaNo ratings yet

- Empirical Asset Pricing: Classes 17-20: Debt Markets and BanksDocument23 pagesEmpirical Asset Pricing: Classes 17-20: Debt Markets and BanksJoe23232232No ratings yet

- Innovation in Latin America: Diagnosis and Questions: Mexico, DF, July 2010Document18 pagesInnovation in Latin America: Diagnosis and Questions: Mexico, DF, July 2010Ervin SalupareNo ratings yet

- Tourism in South Asia: December 2016Document12 pagesTourism in South Asia: December 2016Towsifuzzaman .365No ratings yet

- World Development IndicatorsDocument1 pageWorld Development IndicatorsjohnNo ratings yet

- ST and Trends FINAL-08Document18 pagesST and Trends FINAL-08anon-656678100% (1)

- MINERIA InvestChileWorkshop FinalDocument12 pagesMINERIA InvestChileWorkshop FinalAlberto LobonesNo ratings yet

- TCMB Cembureau - Brannvoll Presentation Final 1 Oct 3 2017Document41 pagesTCMB Cembureau - Brannvoll Presentation Final 1 Oct 3 2017umutNo ratings yet

- Wesp2021 CH3 SaDocument7 pagesWesp2021 CH3 SaImran KarimNo ratings yet

- Double Diamond Rugman PDFDocument16 pagesDouble Diamond Rugman PDFWaris Eka RatnawatiNo ratings yet

- National and Firm-Level AdvantageDocument14 pagesNational and Firm-Level Advantagesteven_c22003No ratings yet

- Creating ValueDocument19 pagesCreating ValueAbhi SharmaNo ratings yet

- Texas McCombs Full-Time MBA Employment Report 2020Document18 pagesTexas McCombs Full-Time MBA Employment Report 2020Ankit ChatterjeeNo ratings yet

- SSRN Id3614875Document15 pagesSSRN Id3614875ghjhghNo ratings yet

- Bca - Gis SR 2023 05 19Document21 pagesBca - Gis SR 2023 05 19Pranab PattanaikNo ratings yet

- December 2020: Quarterly Commentary ReportDocument8 pagesDecember 2020: Quarterly Commentary ReportYog MehtaNo ratings yet

- Building Global Portfolios PDFDocument57 pagesBuilding Global Portfolios PDFSean CurleyNo ratings yet

- Pope To BishopsDocument1 pagePope To BishopsRegina EfraimNo ratings yet

- NM-AIST Student Wins Prestigious Norvatis Next Generation Scientist (NGS) Internship 2015Document2 pagesNM-AIST Student Wins Prestigious Norvatis Next Generation Scientist (NGS) Internship 2015Regina EfraimNo ratings yet

- Job PDFDocument8 pagesJob PDFRegina EfraimNo ratings yet

- S.A. Audits Final Report (Workstations Lakefield SGS)Document23 pagesS.A. Audits Final Report (Workstations Lakefield SGS)Regina EfraimNo ratings yet

- Sub-Thrust PlaysDocument6 pagesSub-Thrust PlaysRegina EfraimNo ratings yet

- Stern 2002Document9 pagesStern 2002Regina EfraimNo ratings yet

- MinRED Review NYANKANGA Geita 2006 FinalDocument17 pagesMinRED Review NYANKANGA Geita 2006 FinalRegina EfraimNo ratings yet

- Correcting For Negative Weights in Ordinary Kriging: Pergamon SOO9t.G3004 (%) 00005-2Document9 pagesCorrecting For Negative Weights in Ordinary Kriging: Pergamon SOO9t.G3004 (%) 00005-2Regina EfraimNo ratings yet

- S.A. Audits Final Report (Workstations Genalysis)Document10 pagesS.A. Audits Final Report (Workstations Genalysis)Regina EfraimNo ratings yet

- OrogenicGold Asjan2005 WorkshopUFRGS Brazil PDFDocument278 pagesOrogenicGold Asjan2005 WorkshopUFRGS Brazil PDFRegina EfraimNo ratings yet

- Anglogold Limited: Exploration WorkshopDocument10 pagesAnglogold Limited: Exploration WorkshopRegina EfraimNo ratings yet

- Chamberlain Et Al 2001 4th IAS Extended AbstractDocument3 pagesChamberlain Et Al 2001 4th IAS Extended AbstractRegina EfraimNo ratings yet

- EM953R Mod2Document59 pagesEM953R Mod2Regina EfraimNo ratings yet

- Mbuya 2003 PDFDocument173 pagesMbuya 2003 PDFRegina EfraimNo ratings yet

- Anglogold Limited: Exploration WorkshopDocument10 pagesAnglogold Limited: Exploration WorkshopRegina EfraimNo ratings yet

- Australasian Joint Ore Reserves Committee (Jorc)Document6 pagesAustralasian Joint Ore Reserves Committee (Jorc)Regina EfraimNo ratings yet

- Kroner Et Al 1997Document18 pagesKroner Et Al 1997Regina EfraimNo ratings yet

- AQC GuidelineDocument66 pagesAQC GuidelineRegina EfraimNo ratings yet

- Anglogold Limited: Exploration WorkshopDocument13 pagesAnglogold Limited: Exploration WorkshopRegina EfraimNo ratings yet

- Final Draft Appendix 5A Jorc 11 May 2004Document27 pagesFinal Draft Appendix 5A Jorc 11 May 2004Regina EfraimNo ratings yet

- Chamberlain Et Al 2000 Gold in 2000 Extended AbstractDocument4 pagesChamberlain Et Al 2000 Gold in 2000 Extended AbstractRegina EfraimNo ratings yet

- Evans Et Al 2000Document24 pagesEvans Et Al 2000Regina EfraimNo ratings yet

- Borg & Krogh 1999Document12 pagesBorg & Krogh 1999Regina EfraimNo ratings yet

- Anglogold Limited: Exploration WorkshopDocument14 pagesAnglogold Limited: Exploration WorkshopRegina EfraimNo ratings yet

- CED Geita Review 2006Document37 pagesCED Geita Review 2006Regina EfraimNo ratings yet

- Anglogold Limited: Exploration WorkshopDocument12 pagesAnglogold Limited: Exploration WorkshopRegina EfraimNo ratings yet

- Banzi 2000Document10 pagesBanzi 2000Regina EfraimNo ratings yet

- Appendix 3 - 08.12023Document62 pagesAppendix 3 - 08.12023Regina EfraimNo ratings yet

- Ample IST: PpendixDocument58 pagesAmple IST: PpendixRegina EfraimNo ratings yet

- Tanzania Audits Final Report HumacDocument14 pagesTanzania Audits Final Report HumacRegina EfraimNo ratings yet

- SRS Template ExampleDocument16 pagesSRS Template ExampleabcNo ratings yet

- Bonds Payable Sample ProblemsDocument2 pagesBonds Payable Sample ProblemsErin LumogdangNo ratings yet

- Literature Review On RingwormDocument6 pagesLiterature Review On Ringwormissyeasif100% (1)

- Summary WordingDocument5 pagesSummary WordingDaniel JenkinsNo ratings yet

- Cook's Illustrated 078Document36 pagesCook's Illustrated 078vicky610100% (3)

- Yoga For Modern Age - 1Document181 pagesYoga For Modern Age - 1GayathriNo ratings yet

- Mongodb DocsDocument313 pagesMongodb DocsDevendra VermaNo ratings yet

- Bermundo Task 3 Iii-20Document2 pagesBermundo Task 3 Iii-20Jakeson Ranit BermundoNo ratings yet

- Language Planning and Placenaming in Australia by Flavia HodgesDocument21 pagesLanguage Planning and Placenaming in Australia by Flavia HodgesCyril Jude CornelioNo ratings yet

- DMEE ConfigurationDocument45 pagesDMEE Configurationgnikisi-1100% (1)

- Metal Joining (Fasteners)Document11 pagesMetal Joining (Fasteners)ganeshNo ratings yet

- How To Use The Bob Beck ProtocolDocument10 pagesHow To Use The Bob Beck ProtocolzuzumwiNo ratings yet

- 921-Article Text-3249-1-10-20220601Document14 pages921-Article Text-3249-1-10-20220601YuliaNo ratings yet

- Chicago Fed Survey April 2023Document2 pagesChicago Fed Survey April 2023Robert GarciaNo ratings yet

- Technological Institute of The Philippines: 938 Aurora Boulevard, Cubao, Quezon CityDocument140 pagesTechnological Institute of The Philippines: 938 Aurora Boulevard, Cubao, Quezon CityKaty Perry100% (1)

- Preliminary Research of Acacia Mangium Glulam Integration in The PhilippinesDocument7 pagesPreliminary Research of Acacia Mangium Glulam Integration in The PhilippinesHalivier Conol LegaspinaNo ratings yet

- Warid Telecom ReportDocument49 pagesWarid Telecom ReporthusnainjafriNo ratings yet

- Doing Business in Lao PDR: Tax & LegalDocument4 pagesDoing Business in Lao PDR: Tax & LegalParth Hemant PurandareNo ratings yet

- Srs 30 PDFDocument3 pagesSrs 30 PDFMichelle Joy Delos ReyesNo ratings yet

- 55 Selection of Appropriate Internal Process Challenge Devices PCDsDocument4 pages55 Selection of Appropriate Internal Process Challenge Devices PCDsRakeshNo ratings yet

- Electromagnetic Interference (EMI) in Power SuppliesDocument41 pagesElectromagnetic Interference (EMI) in Power SuppliesAmarnath M DamodaranNo ratings yet

- Bengur BryanDocument2 pagesBengur Bryancitybizlist11No ratings yet

- Choosing A Significator in Horary Astrology - Nina GryphonDocument4 pagesChoosing A Significator in Horary Astrology - Nina GryphonMarco SatoriNo ratings yet

- The Importance of Soft Skills To A Construction ProjectDocument9 pagesThe Importance of Soft Skills To A Construction ProjectJay SayNo ratings yet

- Inflationary Gap - WikipediaDocument15 pagesInflationary Gap - WikipediaKush KumarNo ratings yet

- On Intuitionistic Fuzzy Transportation Problem Using Pentagonal Intuitionistic Fuzzy Numbers Solved by Modi MethodDocument4 pagesOn Intuitionistic Fuzzy Transportation Problem Using Pentagonal Intuitionistic Fuzzy Numbers Solved by Modi MethodEditor IJTSRDNo ratings yet

- Asme B31.3Document2 pagesAsme B31.3Juan ortega castellarNo ratings yet

- Dimaampao Tax NotesDocument69 pagesDimaampao Tax NotestinctNo ratings yet