Download as pdf or txt

You might also like

- HO No. 1 - Financial Statements AnalysisDocument3 pagesHO No. 1 - Financial Statements AnalysisJOHANNANo ratings yet

- 01 - FS AnalysisDocument17 pages01 - FS AnalysisRyzel Borja0% (1)

- Unit 1 Written Assignment - Updated VersionDocument6 pagesUnit 1 Written Assignment - Updated VersionSimran Pannu100% (1)

- Mayes 8e CH03 Problem SetDocument8 pagesMayes 8e CH03 Problem SetBunga Mega WangiNo ratings yet

- Solution of Finanical Statement AnalysisDocument14 pagesSolution of Finanical Statement AnalysisMUHAMMAD AZAM100% (2)

- Investment and Portfolio Chapter 1Document24 pagesInvestment and Portfolio Chapter 1MarjonNo ratings yet

- Faction IM ScribdDocument32 pagesFaction IM ScribdAlex HoyeNo ratings yet

- A Two-Edged Sword: Salomon and The Separate Legal Entity DoctrineDocument6 pagesA Two-Edged Sword: Salomon and The Separate Legal Entity Doctrineazuma921No ratings yet

- Financial Statement AnalysisDocument6 pagesFinancial Statement AnalysisEmmanuel PenullarNo ratings yet

- Analysis and Interpretetion of Financial StatementsDocument4 pagesAnalysis and Interpretetion of Financial StatementsRida AzamNo ratings yet

- Handout 7 - Business FinanceDocument3 pagesHandout 7 - Business FinanceCeage SJNo ratings yet

- CH03 ProblemDocument3 pagesCH03 Problemtrangtran01010No ratings yet

- Financial Statement AnalysisDocument48 pagesFinancial Statement AnalysisCheryl LowNo ratings yet

- FABM2 W6 No Answer KeyDocument4 pagesFABM2 W6 No Answer KeyClintwest Caliste Autida BartinaNo ratings yet

- Common-Size Financial StatementsDocument16 pagesCommon-Size Financial StatementsApril IsidroNo ratings yet

- Quiz-FS AnalysisDocument3 pagesQuiz-FS AnalysisVergel MartinezNo ratings yet

- Acquisition & Mergers ValuationDocument18 pagesAcquisition & Mergers ValuationAqeel HanjraNo ratings yet

- FS AnalysisDocument5 pagesFS AnalysisLopezNo ratings yet

- 4PPT Financial StatementsDocument21 pages4PPT Financial Statements이시연No ratings yet

- Tutorial 6 With Solutions-Long-Term Debt-Paying Ability and ProfitabilityDocument5 pagesTutorial 6 With Solutions-Long-Term Debt-Paying Ability and ProfitabilityGing freexNo ratings yet

- 1 Manelcom Inc.-With AnswersDocument7 pages1 Manelcom Inc.-With AnswersAmir Aboul FotouhNo ratings yet

- Brewer Chapter 14 Alt ProbDocument8 pagesBrewer Chapter 14 Alt ProbAtif RehmanNo ratings yet

- Individual AssignmentDocument5 pagesIndividual AssignmentMuhammad Faiyam Shafiq 1911819630No ratings yet

- CHAPTER 11 - AnswerDocument16 pagesCHAPTER 11 - Answernash100% (1)

- Chapter # 5 Financial RatiosDocument30 pagesChapter # 5 Financial RatiosRooh Ullah KhanNo ratings yet

- MAS311 Financial Management Exercises Financial Statement AnalysisDocument4 pagesMAS311 Financial Management Exercises Financial Statement AnalysisLeanne QuintoNo ratings yet

- Financial Statement AnalysisDocument31 pagesFinancial Statement AnalysisbilalahmedbhuttoNo ratings yet

- Chapter 2 - Financial AnalysisDocument66 pagesChapter 2 - Financial AnalysisRAHKAESH NAIR A L UTHAIYA NAIR100% (1)

- FABM2-WPS OfficeDocument2 pagesFABM2-WPS OfficeAliza KhateNo ratings yet

- Topic 2 The Statement of Financial PositionDocument38 pagesTopic 2 The Statement of Financial PositionTanmay Sharma100% (1)

- Financial Statements and AnalysisDocument48 pagesFinancial Statements and AnalysiskEBAY100% (1)

- INSTRUCTION: Make Sure Your Mobile Phone Is in Silent Mode and Place It at The Front Together With Bags & BooksDocument2 pagesINSTRUCTION: Make Sure Your Mobile Phone Is in Silent Mode and Place It at The Front Together With Bags & BooksSUPPLYOFFICE EVSUBCNo ratings yet

- Cases Creditors ViewDocument6 pagesCases Creditors ViewCassy MilloNo ratings yet

- Framework For Preparation and Presentation of Financial StatementsDocument5 pagesFramework For Preparation and Presentation of Financial Statementssamartha umbareNo ratings yet

- Fm2quizb4 QoDocument10 pagesFm2quizb4 QoYe YongshiNo ratings yet

- Assignment NO 1 POFDocument15 pagesAssignment NO 1 POFMuhammad AsimNo ratings yet

- 6th Sem MADocument7 pages6th Sem MAjayanth jNo ratings yet

- CheeklistDocument3 pagesCheeklistNahum DaichaNo ratings yet

- FINANCIAL STATEMENT ANALYSIS - Practice Set PDFDocument4 pagesFINANCIAL STATEMENT ANALYSIS - Practice Set PDFDwight Manikan EchagueNo ratings yet

- Midterm Fin 254 Summer 2020Document5 pagesMidterm Fin 254 Summer 2020Salauddin Imran MumitNo ratings yet

- Mock Midterm Exam - Financial AccountingDocument3 pagesMock Midterm Exam - Financial Accountinglamvolamvo0912No ratings yet

- Accounts Unit 01Document5 pagesAccounts Unit 01Sana JKNo ratings yet

- Exercises For Chapter 23 EFA2Document13 pagesExercises For Chapter 23 EFA2tuananh leNo ratings yet

- Fabm 2 - Module 6Document8 pagesFabm 2 - Module 6Kelvin SaplaNo ratings yet

- Ratio Ananlysis MathsDocument2 pagesRatio Ananlysis Mathsekonbiswas37No ratings yet

- Financial Management 02Document20 pagesFinancial Management 02Bby28No ratings yet

- Midterm Revision AnswersDocument10 pagesMidterm Revision AnswersAhmed IsmaelNo ratings yet

- Тasks for individual workDocument7 pagesТasks for individual workДарина БережнаяNo ratings yet

- New Era University: College of AccountancyDocument3 pagesNew Era University: College of AccountancyJoan LaroyaNo ratings yet

- Antonio Huerta Exercise 4Document2 pagesAntonio Huerta Exercise 4Toño H' ChauNo ratings yet

- FM II Ch-3Document9 pagesFM II Ch-3mearghaile4No ratings yet

- Accountingtools: Balance Sheet DefinitionDocument5 pagesAccountingtools: Balance Sheet DefinitionHosty PuffNo ratings yet

- General Discussion of Balance Sheet: Accounting Principles AssetsDocument15 pagesGeneral Discussion of Balance Sheet: Accounting Principles AssetsNazmul Hossain RahatNo ratings yet

- Handout - Financial AnalysisDocument18 pagesHandout - Financial Analysisroseberrylacopia18No ratings yet

- Assumption College of Nabunturan: Nabunturan, Davao de Oro ProvinceDocument7 pagesAssumption College of Nabunturan: Nabunturan, Davao de Oro ProvinceJudithaNo ratings yet

- TQ in Financial Management (Pre-Final)Document8 pagesTQ in Financial Management (Pre-Final)Christine LealNo ratings yet

- Notes For Ratios: Accounting Principles AssetsDocument14 pagesNotes For Ratios: Accounting Principles AssetsSudhanshu MathurNo ratings yet

- Assignment For Finanacial Management IDocument12 pagesAssignment For Finanacial Management IHailu DemekeNo ratings yet

- Addtional Cash Flow Problems and SolutionsDocument7 pagesAddtional Cash Flow Problems and SolutionsHossein ParvardehNo ratings yet

- New Era University: College of AccountancyDocument4 pagesNew Era University: College of AccountancyPeta AkountNo ratings yet

- Internal Control of Fixed Assets: A Controller and Auditor's GuideFrom EverandInternal Control of Fixed Assets: A Controller and Auditor's GuideRating: 4 out of 5 stars4/5 (1)

- Jomar Box Company: Sales 7000x$60 $420,000Document1 pageJomar Box Company: Sales 7000x$60 $420,000MarjonNo ratings yet

- Excess Cash or Need To Borrow 111,300 297,600 (155,100) (22,800) 118,500 187,800Document3 pagesExcess Cash or Need To Borrow 111,300 297,600 (155,100) (22,800) 118,500 187,800Marjon0% (1)

- Case Study No.1Document2 pagesCase Study No.1MarjonNo ratings yet

- Fin. Anal Rafael 3Document4 pagesFin. Anal Rafael 3MarjonNo ratings yet

- Fin. Anal RafaelDocument6 pagesFin. Anal RafaelMarjonNo ratings yet

- Davao Oriental State College of Science and TechnologyDocument3 pagesDavao Oriental State College of Science and TechnologyMarjonNo ratings yet

- Marjon Limot & Jose Araneta Jr. December 09, 2020 Bsba-3B MWF (6:00PM-7:00PM) CBM130: Strategic Management Prof: Maam Teoxon Paired ActivityDocument3 pagesMarjon Limot & Jose Araneta Jr. December 09, 2020 Bsba-3B MWF (6:00PM-7:00PM) CBM130: Strategic Management Prof: Maam Teoxon Paired ActivityMarjonNo ratings yet

- BA132: International Business and Trade: (A Foreign Market Opportunity Assessment)Document2 pagesBA132: International Business and Trade: (A Foreign Market Opportunity Assessment)MarjonNo ratings yet

- Case StudyDocument7 pagesCase StudyMarjonNo ratings yet

- CRM ProposalDocument4 pagesCRM ProposalMarjonNo ratings yet

- FM131 AssignmentDocument1 pageFM131 AssignmentMarjonNo ratings yet

- BSP - Final Exam LUCHAVEZDocument16 pagesBSP - Final Exam LUCHAVEZMarjonNo ratings yet

- GOOD-GOVERNANCE QuizDocument1 pageGOOD-GOVERNANCE QuizMarjonNo ratings yet

- Personal Finance Quiz No.2Document3 pagesPersonal Finance Quiz No.2MarjonNo ratings yet

- Good Governance FormatDocument16 pagesGood Governance FormatMarjonNo ratings yet

- Ba132: International Business and Trade (Final Requirements)Document9 pagesBa132: International Business and Trade (Final Requirements)MarjonNo ratings yet

- CBM130 Quiz No.3Document2 pagesCBM130 Quiz No.3MarjonNo ratings yet

- Human Resource Management PPT Lesson 1Document10 pagesHuman Resource Management PPT Lesson 1MarjonNo ratings yet

- Investment and Portfolio Chapter 2Document32 pagesInvestment and Portfolio Chapter 2MarjonNo ratings yet

- Ba132: International Business and Trade: (A Foreign Market Opportunity Assessment)Document5 pagesBa132: International Business and Trade: (A Foreign Market Opportunity Assessment)MarjonNo ratings yet

- Performance Evaluation Form: Employee Name: Department: Location: Title: Performance Period: ManagerDocument4 pagesPerformance Evaluation Form: Employee Name: Department: Location: Title: Performance Period: ManagerMarjonNo ratings yet

- Philippines Money ColorsDocument1 pagePhilippines Money ColorsMarjonNo ratings yet

- Pi Withdrawal FormDocument4 pagesPi Withdrawal FormRaffy VelezNo ratings yet

- KYC Form - Entity (EN) For ClientDocument3 pagesKYC Form - Entity (EN) For ClientUsmän MïrżäNo ratings yet

- Forsage BUSD EngDocument32 pagesForsage BUSD EngSODOKINNo ratings yet

- Leadership and Case StudyDocument3 pagesLeadership and Case StudyJackNo ratings yet

- Quiz 1. Conceptual Framework and Accounting Standards: PointsDocument21 pagesQuiz 1. Conceptual Framework and Accounting Standards: PointsMarcus MonocayNo ratings yet

- Nebosh ExamDocument9 pagesNebosh Examzainjotun406No ratings yet

- Microeconomics Quiz IDocument6 pagesMicroeconomics Quiz IRohit MukherjeeNo ratings yet

- Haki Assignment 2Document9 pagesHaki Assignment 2Ray hansNo ratings yet

- Marine Electronics 2021 09 10Document52 pagesMarine Electronics 2021 09 10ANDREASBOULNo ratings yet

- SeaGrid Crew Management Crewing ProcedureDocument11 pagesSeaGrid Crew Management Crewing ProcedureCapt100% (1)

- Multinational - Africa Super Esco Accelaration Program Asap - Project Appraisal ReportDocument29 pagesMultinational - Africa Super Esco Accelaration Program Asap - Project Appraisal ReportAyoub EnergieNo ratings yet

- Cass R. Sunstein, On Property and ConstitutionalismDocument1 pageCass R. Sunstein, On Property and ConstitutionalismEm AlayzaNo ratings yet

- CGDocument23 pagesCGTeuku Rifqy RatzarsyahNo ratings yet

- Double Calendar SpreadsDocument22 pagesDouble Calendar SpreadsSasikumar ThangaveluNo ratings yet

- Financial Statements of A PartnershipDocument2 pagesFinancial Statements of A PartnershipMini NimNo ratings yet

- Benefit Illustration 6124175786Document4 pagesBenefit Illustration 6124175786Rajesh DommetiNo ratings yet

- 05 - US Tech - Eliminate The MiddlemanDocument5 pages05 - US Tech - Eliminate The Middlemansejita6795No ratings yet

- VDA 6.3 2016 Process Audit ChecklistDocument48 pagesVDA 6.3 2016 Process Audit ChecklistAlma RosalesNo ratings yet

- Federal Trade Commission Vs Allied Wallet Et AlDocument36 pagesFederal Trade Commission Vs Allied Wallet Et AlhyenadogNo ratings yet

- BSG Players GuideDocument41 pagesBSG Players GuideAdnan MeghaniNo ratings yet

- Soa VS MomDocument8 pagesSoa VS MomCharbel TawkNo ratings yet

- Accra Technical University: Faculty of Business Management and Public AdministrationDocument12 pagesAccra Technical University: Faculty of Business Management and Public AdministrationEunice AdzrakuNo ratings yet

- Valuation Model - Comps, Precedents, DCF, Football Field - BlankDocument10 pagesValuation Model - Comps, Precedents, DCF, Football Field - BlankNmaNo ratings yet

- Inventory System With Barcode Scanner ThesisDocument8 pagesInventory System With Barcode Scanner Thesisfjn3d3mc100% (2)

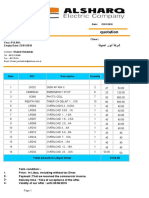

- Alsharq Electric CompanyDocument2 pagesAlsharq Electric CompanymuslimhammedNo ratings yet

- 4Document65 pages4Pappu KumarNo ratings yet

- PRIMAL™ AC-365 Acrylic Emulsion: Regional Product Availability DescriptionDocument3 pagesPRIMAL™ AC-365 Acrylic Emulsion: Regional Product Availability DescriptionLong An ĐỗNo ratings yet

- Income Based Valuation Discounted Cash Flows Group 2Document90 pagesIncome Based Valuation Discounted Cash Flows Group 2natalie clyde mates100% (1)