Download as xlsx, pdf, or txt

You might also like

- Fundamentals of Financial Management 14th Edition Brigham Solutions ManualDocument38 pagesFundamentals of Financial Management 14th Edition Brigham Solutions Manualjeanbarnettxv9v100% (15)

- LYXORDocument5 pagesLYXORRamalu Dinesh Reddy50% (2)

- Obadiah Vineyard CaseDocument3 pagesObadiah Vineyard CaseGodfrey Macwan50% (2)

- Coca-Cola: Residual Income Valuation Exercise & Coca-Cola: Residual Income Valuation Exercise (TN)Document7 pagesCoca-Cola: Residual Income Valuation Exercise & Coca-Cola: Residual Income Valuation Exercise (TN)sarthak mendiratta100% (1)

- Applications For Financial FuturesDocument12 pagesApplications For Financial FuturesNikki JainNo ratings yet

- Chapter 7 BVDocument2 pagesChapter 7 BVprasoonNo ratings yet

- NOPAT Calculations Wacc CalculationDocument1 pageNOPAT Calculations Wacc CalculationRohit BhardawajNo ratings yet

- Case 68 Sweet DreamsDocument12 pagesCase 68 Sweet Dreams3happy3No ratings yet

- Gitman pmf13 ppt09Document56 pagesGitman pmf13 ppt09moonaafreenNo ratings yet

- Finance Chapter 9Document36 pagesFinance Chapter 9mamarcus-1100% (2)

- Coca-Cola (Ticker Symbol KO On NYSE) : Standardized Balance Sheet and Income Statement (Millions)Document6 pagesCoca-Cola (Ticker Symbol KO On NYSE) : Standardized Balance Sheet and Income Statement (Millions)Sayan BiswasNo ratings yet

- Chestnut FoodsDocument2 pagesChestnut FoodsNiyanthesh Reddy25% (4)

- Mogen, Inc. Case StudyDocument18 pagesMogen, Inc. Case StudyAirlangga Prima Satria MaruapeyNo ratings yet

- Marriott Corporation Case SolutionDocument4 pagesMarriott Corporation Case SolutionAsif RahmanNo ratings yet

- Ameritrade Case SolutionDocument34 pagesAmeritrade Case SolutionAbhishek GargNo ratings yet

- Padgett Paper Products Case StudyDocument7 pagesPadgett Paper Products Case StudyDavey FranciscoNo ratings yet

- Beta Management QuestionsDocument1 pageBeta Management QuestionsbjhhjNo ratings yet

- C19a Rio's SpreadsheetDocument8 pagesC19a Rio's SpreadsheetaluiscgNo ratings yet

- 001 The State of South Carolina - SDocument49 pages001 The State of South Carolina - Smeghnakd697625% (4)

- PresentationDocument15 pagesPresentationapi-241493839No ratings yet

- DocumentDocument2 pagesDocumentSarkis SepetjianNo ratings yet

- Bodie Industrial SupplyDocument14 pagesBodie Industrial SupplyHectorZaratePomajulca100% (2)

- M2 Universal: Case PresentationDocument12 pagesM2 Universal: Case PresentationKalyan MukkamulaNo ratings yet

- HW3 SolDocument13 pagesHW3 SolTowweyBerezNo ratings yet

- Corp Fin Case 1 NextelDocument5 pagesCorp Fin Case 1 NextelPedro José ZapataNo ratings yet

- LT1 - LyxorDocument3 pagesLT1 - LyxorMark Paolo Navata100% (1)

- Walt Disney Company S Sleeping Beauty Bonds Duration Analysis1628238200Document22 pagesWalt Disney Company S Sleeping Beauty Bonds Duration Analysis1628238200Rauf JaferiNo ratings yet

- Final Exam Questions Portfolio ManagementDocument9 pagesFinal Exam Questions Portfolio ManagementThảo Như Trần NgọcNo ratings yet

- Chapter 6 Review in ClassDocument32 pagesChapter 6 Review in Classjimmy_chou1314No ratings yet

- Diageo Was Conglomerate Involved in Food and Beverage Industry in 1997Document6 pagesDiageo Was Conglomerate Involved in Food and Beverage Industry in 1997Prashant BezNo ratings yet

- A 109 SMDocument39 pagesA 109 SMRam Krishna KrishNo ratings yet

- CH 22: Lease, Hire Purchase and Project FinancingDocument7 pagesCH 22: Lease, Hire Purchase and Project FinancingMukul KadyanNo ratings yet

- Estimating Beta Value.: Tax RateDocument16 pagesEstimating Beta Value.: Tax Ratesanz0875% (4)

- QuestionsDocument1 pageQuestionselin elizma100% (1)

- Wrigley Gum 21Document18 pagesWrigley Gum 21Fidelity RoadNo ratings yet

- 8db6 - ING Insurance - Asia-PacificDocument16 pages8db6 - ING Insurance - Asia-PacificJessica LopezNo ratings yet

- Arcadian Business CaseDocument20 pagesArcadian Business CaseHeniNo ratings yet

- Case 8 Finance CPK - Syndicate 2 YP56BDocument13 pagesCase 8 Finance CPK - Syndicate 2 YP56BBerni RahmanNo ratings yet

- 683 Sol 01Document715 pages683 Sol 01ottieNo ratings yet

- Integrative Case 10 1 Projected Financial Statements For StarbucDocument2 pagesIntegrative Case 10 1 Projected Financial Statements For StarbucAmit PandeyNo ratings yet

- Test 04Document3 pagesTest 04rgonzalez666No ratings yet

- Answers To Practice Questions: Risk and ReturnDocument11 pagesAnswers To Practice Questions: Risk and ReturnmasterchocoNo ratings yet

- Solution Ipa Week 1 Chapter 3Document47 pagesSolution Ipa Week 1 Chapter 3Aura MaghfiraNo ratings yet

- Homework Assignment 1 KeyDocument6 pagesHomework Assignment 1 KeymetetezcanNo ratings yet

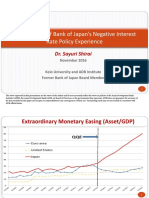

- An Overview of Bank of Japan Negative Interest Rate Policy ExperienceDocument12 pagesAn Overview of Bank of Japan Negative Interest Rate Policy ExperienceADBI Events100% (1)

- Chapter 5 - Group DisposalsDocument4 pagesChapter 5 - Group DisposalsSheikh Mass JahNo ratings yet

- Harley DavidsonDocument4 pagesHarley DavidsonExpert AnswersNo ratings yet

- SAPM Assignment For MBADocument2 pagesSAPM Assignment For MBARahul AroraNo ratings yet

- Practice Casestudy SolutionsDocument6 pagesPractice Casestudy SolutionsnurNo ratings yet

- Deutsche Bank and The Road To Basel IiiDocument2 pagesDeutsche Bank and The Road To Basel IiiNEERAJ N RCBS100% (1)

- Calaveras Vineyards ExhibitsDocument9 pagesCalaveras Vineyards ExhibitsAbhishek Mani TripathiNo ratings yet

- EViews 2nd Week Assignment With SolutionDocument12 pagesEViews 2nd Week Assignment With SolutionFagbola Oluwatobi OmolajaNo ratings yet

- Cost of Capital at AmeritradeDocument3 pagesCost of Capital at AmeritradeAnkur JainNo ratings yet

- MidlandDocument4 pagesMidlandsophieNo ratings yet

- Case Write Up Sample 2Document4 pagesCase Write Up Sample 2veda20No ratings yet

- Caso Dupont - Keren MendesDocument17 pagesCaso Dupont - Keren MendesKeren NovaesNo ratings yet

- Buffett CaseDocument15 pagesBuffett CaseElizabeth MillerNo ratings yet

- Hello GunaDocument10 pagesHello GunaMajed Abou AlkhirNo ratings yet

- Ratio Formula RemarksDocument7 pagesRatio Formula RemarksmgajenNo ratings yet

- Sampa Video Inc.: Thousand of Dollars Exhibit 4Document2 pagesSampa Video Inc.: Thousand of Dollars Exhibit 4nimarNo ratings yet

- SearsvswalmartDocument7 pagesSearsvswalmartXie KeyangNo ratings yet

- HDFC by IshanDocument14 pagesHDFC by IshanIshan MalikNo ratings yet

- Balanced - Dataset - Comparison: P-ValueDocument21 pagesBalanced - Dataset - Comparison: P-ValueChinniah DevarNo ratings yet

- Principles and Methods of Law and Economics Enhancing Normative Analysis Oct 2005 PDFDocument394 pagesPrinciples and Methods of Law and Economics Enhancing Normative Analysis Oct 2005 PDFMarcelo Mardones Osorio100% (3)

- Sharpe RatiosDocument56 pagesSharpe RatiosbobmezzNo ratings yet

- Cost of Capital & Profitability Analysis of Beximco Pharmaceuticals Ltd.Document40 pagesCost of Capital & Profitability Analysis of Beximco Pharmaceuticals Ltd.Marshal Richard86% (7)

- HW 6 - AkDocument6 pagesHW 6 - AkSuvaid KcNo ratings yet

- Financial Management MCQDocument2 pagesFinancial Management MCQRajendra Pansare88% (8)

- The Capital Asset Pricing ModelDocument27 pagesThe Capital Asset Pricing ModelThái NguyễnNo ratings yet

- Portfolio ManagementDocument104 pagesPortfolio ManagementAbhijit ErandeNo ratings yet

- CAPMDocument60 pagesCAPMJerine TanNo ratings yet

- Determination of Swap Ratio in Merger: Case of Reliance Natural Resources Ltd. and Reliance Power Ltd. MergerDocument14 pagesDetermination of Swap Ratio in Merger: Case of Reliance Natural Resources Ltd. and Reliance Power Ltd. MergerAswani B RajNo ratings yet

- Finance Decisions: Unit IvDocument70 pagesFinance Decisions: Unit IvFara HameedNo ratings yet

- Test Bank For Intermediate Financial Management 12th Edition Brigham Daves 1285850033 9781285850030Document36 pagesTest Bank For Intermediate Financial Management 12th Edition Brigham Daves 1285850033 9781285850030ReneeRyancnefw100% (29)

- Business Administration CSS 2000 2020Document32 pagesBusiness Administration CSS 2000 2020Jelly FishNo ratings yet

- Catastrophic Risk and The Capital Markets: Berkshire Hathaway and Warren Buffett's Success Volatility Pumping Cat ReinsuranceDocument15 pagesCatastrophic Risk and The Capital Markets: Berkshire Hathaway and Warren Buffett's Success Volatility Pumping Cat ReinsuranceAlex VartanNo ratings yet

- Slide 6Document37 pagesSlide 6Akash SinghNo ratings yet

- Chapter 7. Risk and Return Student VersionDocument5 pagesChapter 7. Risk and Return Student VersionTú UyênNo ratings yet

- Asset Pricing Principles: Charles P. Jones, Investments: Principles and Concepts, Twelfth Edition, John Wiley & SonsDocument34 pagesAsset Pricing Principles: Charles P. Jones, Investments: Principles and Concepts, Twelfth Edition, John Wiley & SonsGeorgina AlpertNo ratings yet

- Investment Valuation and Asset Pricing Models and Methods James W Kolari Full ChapterDocument67 pagesInvestment Valuation and Asset Pricing Models and Methods James W Kolari Full Chapterangel.attaway709100% (5)

- Analysis of Equity Based Mutual Funds in India: Sahil JainDocument4 pagesAnalysis of Equity Based Mutual Funds in India: Sahil JainInternational Organization of Scientific Research (IOSR)No ratings yet

- Risk & Return PPDocument40 pagesRisk & Return PPAnneHumayraAnasNo ratings yet

- Sapm QBDocument8 pagesSapm QBSiva KumarNo ratings yet

- BBPW3103 Financial Management IDocument399 pagesBBPW3103 Financial Management IPhewit Tyme100% (3)

- Portfolio Evaluation TechniquesDocument18 pagesPortfolio Evaluation TechniquesMonalisa BagdeNo ratings yet

- Security Analysis and Portfolio Management QBDocument13 pagesSecurity Analysis and Portfolio Management QBAnonymous y3E7iaNo ratings yet

- 2229 - Investments - S1 - G.ottonelloDocument4 pages2229 - Investments - S1 - G.ottonelloNeal EricksonNo ratings yet

- Investment Assign 2 - QuestionsDocument7 pagesInvestment Assign 2 - QuestionsYuhan KENo ratings yet

- Corporate Valuation Modeling For Strategic FinanciDocument15 pagesCorporate Valuation Modeling For Strategic FinancinadiahalusNo ratings yet

- Lecture 6 - Additional Note On CAPM DerivationDocument5 pagesLecture 6 - Additional Note On CAPM DerivationJohnNo ratings yet