Table of Content

Table of Content

You might also like

- Declaration of Beneficial Owner (Bo) Form IIDocument2 pagesDeclaration of Beneficial Owner (Bo) Form IIMahamadali DesaiNo ratings yet

- Corporete Governance Final ExamDocument7 pagesCorporete Governance Final Examcn comNo ratings yet

- Corporate GovernanceDocument24 pagesCorporate GovernancexakiahmedNo ratings yet

- Challenges For Financial Managers in A Changing Economic EnvironmentDocument7 pagesChallenges For Financial Managers in A Changing Economic EnvironmentFaria MehboobNo ratings yet

- CSR by Shreya, Siddharth, PrabirDocument20 pagesCSR by Shreya, Siddharth, PrabirSiddharth JhaNo ratings yet

- International Business EnvironmentDocument11 pagesInternational Business Environmentkenedy simwingaNo ratings yet

- Chapter One & TwoDocument25 pagesChapter One & TwoSaviusNo ratings yet

- Firm's Environment, Governance and Strategy: Strategic Financial ManagementDocument14 pagesFirm's Environment, Governance and Strategy: Strategic Financial ManagementAnish MittalNo ratings yet

- Factors For Financial EngineeringDocument8 pagesFactors For Financial EngineeringMuhaiminul IslamNo ratings yet

- Globalisation and CSR CH 6 12122022 091357pmDocument21 pagesGlobalisation and CSR CH 6 12122022 091357pmHadia ZafarNo ratings yet

- Week 1 Chapter 1: Strategic Management and Strategic CompetitivenessDocument7 pagesWeek 1 Chapter 1: Strategic Management and Strategic CompetitivenessRosalie Colarte LangbayNo ratings yet

- Module 7Document13 pagesModule 7efrenNo ratings yet

- Chapter Five Regulation of Financial Markets and Institutions and Financial InnovationDocument22 pagesChapter Five Regulation of Financial Markets and Institutions and Financial InnovationMikias DegwaleNo ratings yet

- Corporate Governance by N.santosh RanganathDocument7 pagesCorporate Governance by N.santosh RanganathnsrnathNo ratings yet

- The Significant Transformation of The Banking Industry in India Is Clearly EvidentDocument69 pagesThe Significant Transformation of The Banking Industry in India Is Clearly EvidentJayesh BhanushaliNo ratings yet

- Introduction To Business Environment-pg-1-FinalDocument64 pagesIntroduction To Business Environment-pg-1-FinalAnantha NagNo ratings yet

- Sandip University, Nasik: Assignment On Law of Corporat FinanceDocument17 pagesSandip University, Nasik: Assignment On Law of Corporat FinanceJinal ShahNo ratings yet

- Multinational Company NoteDocument39 pagesMultinational Company Notetsion alemayehuNo ratings yet

- Emerging Trends in Corporate Governance PracticesDocument9 pagesEmerging Trends in Corporate Governance PracticesDr-Rahat KhanNo ratings yet

- CG CHP 15Document18 pagesCG CHP 15lani anggrainiNo ratings yet

- Financial Crises SuggestionsDocument36 pagesFinancial Crises Suggestions03216055440No ratings yet

- Chap 1&2Document7 pagesChap 1&2Moin AhmedNo ratings yet

- Stakeholders and Sustainable Corporate Governance in NigeriaDocument154 pagesStakeholders and Sustainable Corporate Governance in NigeriabastuswitaNo ratings yet

- Part 1-Overview of Strategic Financial Management: TOPIC 1: Business PlanningDocument24 pagesPart 1-Overview of Strategic Financial Management: TOPIC 1: Business PlanningCenith CheeNo ratings yet

- Title of Module: Introduction To International Business: 2. Overview/Introduction 3. Learning Outcome/ObjectiveDocument9 pagesTitle of Module: Introduction To International Business: 2. Overview/Introduction 3. Learning Outcome/ObjectiveJaymarie ColomaNo ratings yet

- Globalisation, Trade Liberalisation and Foreign Investment. Material For Sections 1 and 2 of 3A EconomicsDocument43 pagesGlobalisation, Trade Liberalisation and Foreign Investment. Material For Sections 1 and 2 of 3A EconomicsTristanNo ratings yet

- Impact of The International Business Environment On Global OrganisationsDocument9 pagesImpact of The International Business Environment On Global OrganisationsSachin SinghNo ratings yet

- How The Corporate Governance Affects Organizational Strategy: Lessons From Jordan Environment.Document15 pagesHow The Corporate Governance Affects Organizational Strategy: Lessons From Jordan Environment.IOSRjournalNo ratings yet

- Financial Engineering AnuDocument11 pagesFinancial Engineering AnuThaiseer MohammedNo ratings yet

- PESTEL Analysis of Organized Jewellery SectorDocument5 pagesPESTEL Analysis of Organized Jewellery SectorSIMRAN SHOKEENNo ratings yet

- Case Study of Corporate Governance in Taiwan: Trends and RecommendationsDocument29 pagesCase Study of Corporate Governance in Taiwan: Trends and RecommendationsariaNo ratings yet

- OECD Why We Need Corporate GovernanceDocument4 pagesOECD Why We Need Corporate GovernanceMaggie QueridoNo ratings yet

- Vhurinosara Tapiwanashe A BS Assignment 1Document8 pagesVhurinosara Tapiwanashe A BS Assignment 1Victor HoveNo ratings yet

- Case Study of Corporate Governance in Taiwan: Trends and RecommendationsDocument28 pagesCase Study of Corporate Governance in Taiwan: Trends and RecommendationsdwijaluNo ratings yet

- GBM ReportDocument5 pagesGBM ReportMarie Faith MaramagNo ratings yet

- The Importance of International Accounting StandardsDocument3 pagesThe Importance of International Accounting Standardssohansharma75No ratings yet

- Ibc AbhiDocument15 pagesIbc AbhiAbhijit BansalNo ratings yet

- Exam Form: Assignment Exam Time: 3 DaysDocument16 pagesExam Form: Assignment Exam Time: 3 DaysTrang DươngNo ratings yet

- Importance of International BusinessDocument4 pagesImportance of International BusinesssandilyaNo ratings yet

- Emerging IssuesDocument8 pagesEmerging IssuesAnonymous wSSh4uGNo ratings yet

- Importance of Capital StructureDocument2 pagesImportance of Capital StructureShruti JoseNo ratings yet

- Entrepreneurship Development - Unit IIDocument14 pagesEntrepreneurship Development - Unit IIRitikshankar YadavNo ratings yet

- Ensayo Riesgo Gobierno CorporativoDocument5 pagesEnsayo Riesgo Gobierno CorporativojuanNo ratings yet

- 1 FM 304 Lesson 1Document15 pages1 FM 304 Lesson 1lovely tinguhaNo ratings yet

- MPIB7103 Assignment 2 (201805)Document7 pagesMPIB7103 Assignment 2 (201805)Masri Abdul LasiNo ratings yet

- FinTech RegTech and SupTech - What They Mean For Financial Supervision FINALDocument19 pagesFinTech RegTech and SupTech - What They Mean For Financial Supervision FINALirvandi syahputraNo ratings yet

- Corporate Governance in The 21st CenturyDocument8 pagesCorporate Governance in The 21st CenturymayhemclubNo ratings yet

- Running Head: Government Regulations On Financial Innovations 1Document8 pagesRunning Head: Government Regulations On Financial Innovations 1Cornelius Kings 'Con'No ratings yet

- Financial Statements Analysis: Wealth Creation and Wealth Maximisation at Telecom Company From 2010 To 2012Document11 pagesFinancial Statements Analysis: Wealth Creation and Wealth Maximisation at Telecom Company From 2010 To 2012IOSRjournalNo ratings yet

- Mayanja Yasin ProposalDocument15 pagesMayanja Yasin ProposalSuleiman AbdulNo ratings yet

- Corporate Governance in Developing and Emerging Countries. The Case of RomaniaDocument10 pagesCorporate Governance in Developing and Emerging Countries. The Case of RomaniashevabrustNo ratings yet

- Corp. Governance 1Document11 pagesCorp. Governance 1ridhiNo ratings yet

- Introduce To Management AccountingDocument9 pagesIntroduce To Management AccountingSagung AdvaitaNo ratings yet

- ON Corporate Governance IN India": A On "Oecd RecommendationsDocument25 pagesON Corporate Governance IN India": A On "Oecd RecommendationsUrvesh ParmarNo ratings yet

- Financial and Investment Skills YCMOU AssignmentDocument5 pagesFinancial and Investment Skills YCMOU AssignmentSufiyan MogalNo ratings yet

- (Belén Díaz Díaz, Samuel O. Idowu, Philip Molyneu (B-Ok - Xyz)Document348 pages(Belén Díaz Díaz, Samuel O. Idowu, Philip Molyneu (B-Ok - Xyz)Lamraoui ZouNo ratings yet

- Good Corporate Governance Hinges On A Number of Elements Such As PrinciplesDocument15 pagesGood Corporate Governance Hinges On A Number of Elements Such As PrinciplesSonam GoyalNo ratings yet

- Financial EngineeringDocument26 pagesFinancial EngineeringRajan100% (6)

- Strategy, Value and Risk: Industry Dynamics and Advanced Financial ManagementFrom EverandStrategy, Value and Risk: Industry Dynamics and Advanced Financial ManagementNo ratings yet

- Finalised AssignmentDocument11 pagesFinalised AssignmentNuwan KumarasingheNo ratings yet

- Explore Measurements To Advance The Service Quality of Janashakthi Insurance Life Claims DepartmentDocument24 pagesExplore Measurements To Advance The Service Quality of Janashakthi Insurance Life Claims DepartmentNuwan KumarasingheNo ratings yet

- Task III - Cash Flow Analysis - ReportDocument7 pagesTask III - Cash Flow Analysis - ReportNuwan KumarasingheNo ratings yet

- Task I - Interpret and Complete Budgetary RequirementsDocument18 pagesTask I - Interpret and Complete Budgetary RequirementsNuwan KumarasingheNo ratings yet

- Draft - AssignmentDocument9 pagesDraft - AssignmentNuwan KumarasingheNo ratings yet

- E-Banking and Financial Performance of Commercial Banks in Sri LankaDocument15 pagesE-Banking and Financial Performance of Commercial Banks in Sri LankaNuwan KumarasingheNo ratings yet

- 310 Corporate GovernanceDocument24 pages310 Corporate GovernanceManojNo ratings yet

- 2223 BLP ws16 Ce01 GuideDocument18 pages2223 BLP ws16 Ce01 GuideZuniNo ratings yet

- Philippine Long Distance Telephone Co. Vs National Telecommunications Commission 190 SCRA 717 (GR No. 88404 October 18, 1990)Document6 pagesPhilippine Long Distance Telephone Co. Vs National Telecommunications Commission 190 SCRA 717 (GR No. 88404 October 18, 1990)Bob LawNo ratings yet

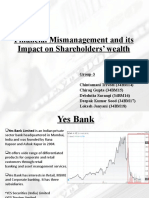

- Group3 - CFEV - Project Presentation - Fin-MismanagementDocument11 pagesGroup3 - CFEV - Project Presentation - Fin-MismanagementDeepak SoodNo ratings yet

- Comparative IndCo Challenges of Designing and Implementing Customized Training AnalysisDocument3 pagesComparative IndCo Challenges of Designing and Implementing Customized Training AnalysisSeemaNo ratings yet

- FEU List of Top 100 Stockholders As of 31 March 2020-MergedDocument8 pagesFEU List of Top 100 Stockholders As of 31 March 2020-MergedJohn M. RoyNo ratings yet

- Financial Strategy ALL MergedDocument379 pagesFinancial Strategy ALL MergedSushil PrajapatNo ratings yet

- 2020 Corpo AteneoDocument108 pages2020 Corpo AteneoQuennie DisturaNo ratings yet

- One Stop Company SecretaryDocument25 pagesOne Stop Company Secretaryaraza_962307No ratings yet

- CG&E Part 4Document75 pagesCG&E Part 4sanghamitra dasNo ratings yet

- ITCDocument6 pagesITCpavikuttyNo ratings yet

- Corporate Actions - Dividends, Bonus, Splits, Buyback EtcDocument37 pagesCorporate Actions - Dividends, Bonus, Splits, Buyback Etcagrawal.minNo ratings yet

- Mepal LeafDocument8 pagesMepal LeafMuhammadArshadNo ratings yet

- Formation Incoporation of CompaniesDocument21 pagesFormation Incoporation of CompaniesNAGARAJACHARI KAMMARANo ratings yet

- Section 73. Books To Be Kept Stock Transfer Agent. - Every Corporation Shall Keep and Carefully Preserve at ItsDocument9 pagesSection 73. Books To Be Kept Stock Transfer Agent. - Every Corporation Shall Keep and Carefully Preserve at ItsYarah MNo ratings yet

- Thirumalai Chemicals LTD - 2018 PDFDocument132 pagesThirumalai Chemicals LTD - 2018 PDFRavi PanaraNo ratings yet

- Asset AcquisitionDocument3 pagesAsset AcquisitionMerliza JusayanNo ratings yet

- London Listed Property Company Focused On Emerging Europe: Investor Presentation Q2 2016Document26 pagesLondon Listed Property Company Focused On Emerging Europe: Investor Presentation Q2 2016Alexandra BugaNo ratings yet

- Air India Annual Return 2022 23Document15 pagesAir India Annual Return 2022 23Ayush DuttaNo ratings yet

- Merger of Tata Steel and CorusDocument24 pagesMerger of Tata Steel and Coruspratik tanna100% (17)

- Raroc Cimb PDFDocument202 pagesRaroc Cimb PDFsaeful anwariNo ratings yet

- Group Company Liability: Martin Petrin Barnali ChoudhuryDocument26 pagesGroup Company Liability: Martin Petrin Barnali Choudhuryrishabh guptaNo ratings yet

- Corporation Code - de Leon PDFDocument1,114 pagesCorporation Code - de Leon PDFBelteshazzarL.Cabacang100% (1)

- Company Law Live Mock Test PDFDocument4 pagesCompany Law Live Mock Test PDFभगवा समर्थकNo ratings yet

- Financial Management Case Study ON Agency Problem Agency ProblemDocument3 pagesFinancial Management Case Study ON Agency Problem Agency ProblemV SHARAVANI MBANo ratings yet

- Quizzer in Corpo Set ADocument11 pagesQuizzer in Corpo Set ARon Nixon MendozaNo ratings yet

- Chapter 14 - Dividend PolicyDocument38 pagesChapter 14 - Dividend PolicyRAQAEL RHODENo ratings yet

- Opening A Business Is A Lot of Work, You Have To Comply With All The Requirements To Start. Here'S How You Go About ItDocument11 pagesOpening A Business Is A Lot of Work, You Have To Comply With All The Requirements To Start. Here'S How You Go About Itcamille agudaNo ratings yet

- Caac Fire and Rescue Volunteer Inc.: By-Laws OFDocument4 pagesCaac Fire and Rescue Volunteer Inc.: By-Laws OFJosephGerardBersalonaNo ratings yet

Download as docx, pdf, or txt

You might also like

- Declaration of Beneficial Owner (Bo) Form IIDocument2 pagesDeclaration of Beneficial Owner (Bo) Form IIMahamadali DesaiNo ratings yet

- Corporete Governance Final ExamDocument7 pagesCorporete Governance Final Examcn comNo ratings yet

- Corporate GovernanceDocument24 pagesCorporate GovernancexakiahmedNo ratings yet

- Challenges For Financial Managers in A Changing Economic EnvironmentDocument7 pagesChallenges For Financial Managers in A Changing Economic EnvironmentFaria MehboobNo ratings yet

- CSR by Shreya, Siddharth, PrabirDocument20 pagesCSR by Shreya, Siddharth, PrabirSiddharth JhaNo ratings yet

- International Business EnvironmentDocument11 pagesInternational Business Environmentkenedy simwingaNo ratings yet

- Chapter One & TwoDocument25 pagesChapter One & TwoSaviusNo ratings yet

- Firm's Environment, Governance and Strategy: Strategic Financial ManagementDocument14 pagesFirm's Environment, Governance and Strategy: Strategic Financial ManagementAnish MittalNo ratings yet

- Factors For Financial EngineeringDocument8 pagesFactors For Financial EngineeringMuhaiminul IslamNo ratings yet

- Globalisation and CSR CH 6 12122022 091357pmDocument21 pagesGlobalisation and CSR CH 6 12122022 091357pmHadia ZafarNo ratings yet

- Week 1 Chapter 1: Strategic Management and Strategic CompetitivenessDocument7 pagesWeek 1 Chapter 1: Strategic Management and Strategic CompetitivenessRosalie Colarte LangbayNo ratings yet

- Module 7Document13 pagesModule 7efrenNo ratings yet

- Chapter Five Regulation of Financial Markets and Institutions and Financial InnovationDocument22 pagesChapter Five Regulation of Financial Markets and Institutions and Financial InnovationMikias DegwaleNo ratings yet

- Corporate Governance by N.santosh RanganathDocument7 pagesCorporate Governance by N.santosh RanganathnsrnathNo ratings yet

- The Significant Transformation of The Banking Industry in India Is Clearly EvidentDocument69 pagesThe Significant Transformation of The Banking Industry in India Is Clearly EvidentJayesh BhanushaliNo ratings yet

- Introduction To Business Environment-pg-1-FinalDocument64 pagesIntroduction To Business Environment-pg-1-FinalAnantha NagNo ratings yet

- Sandip University, Nasik: Assignment On Law of Corporat FinanceDocument17 pagesSandip University, Nasik: Assignment On Law of Corporat FinanceJinal ShahNo ratings yet

- Multinational Company NoteDocument39 pagesMultinational Company Notetsion alemayehuNo ratings yet

- Emerging Trends in Corporate Governance PracticesDocument9 pagesEmerging Trends in Corporate Governance PracticesDr-Rahat KhanNo ratings yet

- CG CHP 15Document18 pagesCG CHP 15lani anggrainiNo ratings yet

- Financial Crises SuggestionsDocument36 pagesFinancial Crises Suggestions03216055440No ratings yet

- Chap 1&2Document7 pagesChap 1&2Moin AhmedNo ratings yet

- Stakeholders and Sustainable Corporate Governance in NigeriaDocument154 pagesStakeholders and Sustainable Corporate Governance in NigeriabastuswitaNo ratings yet

- Part 1-Overview of Strategic Financial Management: TOPIC 1: Business PlanningDocument24 pagesPart 1-Overview of Strategic Financial Management: TOPIC 1: Business PlanningCenith CheeNo ratings yet

- Title of Module: Introduction To International Business: 2. Overview/Introduction 3. Learning Outcome/ObjectiveDocument9 pagesTitle of Module: Introduction To International Business: 2. Overview/Introduction 3. Learning Outcome/ObjectiveJaymarie ColomaNo ratings yet

- Globalisation, Trade Liberalisation and Foreign Investment. Material For Sections 1 and 2 of 3A EconomicsDocument43 pagesGlobalisation, Trade Liberalisation and Foreign Investment. Material For Sections 1 and 2 of 3A EconomicsTristanNo ratings yet

- Impact of The International Business Environment On Global OrganisationsDocument9 pagesImpact of The International Business Environment On Global OrganisationsSachin SinghNo ratings yet

- How The Corporate Governance Affects Organizational Strategy: Lessons From Jordan Environment.Document15 pagesHow The Corporate Governance Affects Organizational Strategy: Lessons From Jordan Environment.IOSRjournalNo ratings yet

- Financial Engineering AnuDocument11 pagesFinancial Engineering AnuThaiseer MohammedNo ratings yet

- PESTEL Analysis of Organized Jewellery SectorDocument5 pagesPESTEL Analysis of Organized Jewellery SectorSIMRAN SHOKEENNo ratings yet

- Case Study of Corporate Governance in Taiwan: Trends and RecommendationsDocument29 pagesCase Study of Corporate Governance in Taiwan: Trends and RecommendationsariaNo ratings yet

- OECD Why We Need Corporate GovernanceDocument4 pagesOECD Why We Need Corporate GovernanceMaggie QueridoNo ratings yet

- Vhurinosara Tapiwanashe A BS Assignment 1Document8 pagesVhurinosara Tapiwanashe A BS Assignment 1Victor HoveNo ratings yet

- Case Study of Corporate Governance in Taiwan: Trends and RecommendationsDocument28 pagesCase Study of Corporate Governance in Taiwan: Trends and RecommendationsdwijaluNo ratings yet

- GBM ReportDocument5 pagesGBM ReportMarie Faith MaramagNo ratings yet

- The Importance of International Accounting StandardsDocument3 pagesThe Importance of International Accounting Standardssohansharma75No ratings yet

- Ibc AbhiDocument15 pagesIbc AbhiAbhijit BansalNo ratings yet

- Exam Form: Assignment Exam Time: 3 DaysDocument16 pagesExam Form: Assignment Exam Time: 3 DaysTrang DươngNo ratings yet

- Importance of International BusinessDocument4 pagesImportance of International BusinesssandilyaNo ratings yet

- Emerging IssuesDocument8 pagesEmerging IssuesAnonymous wSSh4uGNo ratings yet

- Importance of Capital StructureDocument2 pagesImportance of Capital StructureShruti JoseNo ratings yet

- Entrepreneurship Development - Unit IIDocument14 pagesEntrepreneurship Development - Unit IIRitikshankar YadavNo ratings yet

- Ensayo Riesgo Gobierno CorporativoDocument5 pagesEnsayo Riesgo Gobierno CorporativojuanNo ratings yet

- 1 FM 304 Lesson 1Document15 pages1 FM 304 Lesson 1lovely tinguhaNo ratings yet

- MPIB7103 Assignment 2 (201805)Document7 pagesMPIB7103 Assignment 2 (201805)Masri Abdul LasiNo ratings yet

- FinTech RegTech and SupTech - What They Mean For Financial Supervision FINALDocument19 pagesFinTech RegTech and SupTech - What They Mean For Financial Supervision FINALirvandi syahputraNo ratings yet

- Corporate Governance in The 21st CenturyDocument8 pagesCorporate Governance in The 21st CenturymayhemclubNo ratings yet

- Running Head: Government Regulations On Financial Innovations 1Document8 pagesRunning Head: Government Regulations On Financial Innovations 1Cornelius Kings 'Con'No ratings yet

- Financial Statements Analysis: Wealth Creation and Wealth Maximisation at Telecom Company From 2010 To 2012Document11 pagesFinancial Statements Analysis: Wealth Creation and Wealth Maximisation at Telecom Company From 2010 To 2012IOSRjournalNo ratings yet

- Mayanja Yasin ProposalDocument15 pagesMayanja Yasin ProposalSuleiman AbdulNo ratings yet

- Corporate Governance in Developing and Emerging Countries. The Case of RomaniaDocument10 pagesCorporate Governance in Developing and Emerging Countries. The Case of RomaniashevabrustNo ratings yet

- Corp. Governance 1Document11 pagesCorp. Governance 1ridhiNo ratings yet

- Introduce To Management AccountingDocument9 pagesIntroduce To Management AccountingSagung AdvaitaNo ratings yet

- ON Corporate Governance IN India": A On "Oecd RecommendationsDocument25 pagesON Corporate Governance IN India": A On "Oecd RecommendationsUrvesh ParmarNo ratings yet

- Financial and Investment Skills YCMOU AssignmentDocument5 pagesFinancial and Investment Skills YCMOU AssignmentSufiyan MogalNo ratings yet

- (Belén Díaz Díaz, Samuel O. Idowu, Philip Molyneu (B-Ok - Xyz)Document348 pages(Belén Díaz Díaz, Samuel O. Idowu, Philip Molyneu (B-Ok - Xyz)Lamraoui ZouNo ratings yet

- Good Corporate Governance Hinges On A Number of Elements Such As PrinciplesDocument15 pagesGood Corporate Governance Hinges On A Number of Elements Such As PrinciplesSonam GoyalNo ratings yet

- Financial EngineeringDocument26 pagesFinancial EngineeringRajan100% (6)

- Strategy, Value and Risk: Industry Dynamics and Advanced Financial ManagementFrom EverandStrategy, Value and Risk: Industry Dynamics and Advanced Financial ManagementNo ratings yet

- Finalised AssignmentDocument11 pagesFinalised AssignmentNuwan KumarasingheNo ratings yet

- Explore Measurements To Advance The Service Quality of Janashakthi Insurance Life Claims DepartmentDocument24 pagesExplore Measurements To Advance The Service Quality of Janashakthi Insurance Life Claims DepartmentNuwan KumarasingheNo ratings yet

- Task III - Cash Flow Analysis - ReportDocument7 pagesTask III - Cash Flow Analysis - ReportNuwan KumarasingheNo ratings yet

- Task I - Interpret and Complete Budgetary RequirementsDocument18 pagesTask I - Interpret and Complete Budgetary RequirementsNuwan KumarasingheNo ratings yet

- Draft - AssignmentDocument9 pagesDraft - AssignmentNuwan KumarasingheNo ratings yet

- E-Banking and Financial Performance of Commercial Banks in Sri LankaDocument15 pagesE-Banking and Financial Performance of Commercial Banks in Sri LankaNuwan KumarasingheNo ratings yet

- 310 Corporate GovernanceDocument24 pages310 Corporate GovernanceManojNo ratings yet

- 2223 BLP ws16 Ce01 GuideDocument18 pages2223 BLP ws16 Ce01 GuideZuniNo ratings yet

- Philippine Long Distance Telephone Co. Vs National Telecommunications Commission 190 SCRA 717 (GR No. 88404 October 18, 1990)Document6 pagesPhilippine Long Distance Telephone Co. Vs National Telecommunications Commission 190 SCRA 717 (GR No. 88404 October 18, 1990)Bob LawNo ratings yet

- Group3 - CFEV - Project Presentation - Fin-MismanagementDocument11 pagesGroup3 - CFEV - Project Presentation - Fin-MismanagementDeepak SoodNo ratings yet

- Comparative IndCo Challenges of Designing and Implementing Customized Training AnalysisDocument3 pagesComparative IndCo Challenges of Designing and Implementing Customized Training AnalysisSeemaNo ratings yet

- FEU List of Top 100 Stockholders As of 31 March 2020-MergedDocument8 pagesFEU List of Top 100 Stockholders As of 31 March 2020-MergedJohn M. RoyNo ratings yet

- Financial Strategy ALL MergedDocument379 pagesFinancial Strategy ALL MergedSushil PrajapatNo ratings yet

- 2020 Corpo AteneoDocument108 pages2020 Corpo AteneoQuennie DisturaNo ratings yet

- One Stop Company SecretaryDocument25 pagesOne Stop Company Secretaryaraza_962307No ratings yet

- CG&E Part 4Document75 pagesCG&E Part 4sanghamitra dasNo ratings yet

- ITCDocument6 pagesITCpavikuttyNo ratings yet

- Corporate Actions - Dividends, Bonus, Splits, Buyback EtcDocument37 pagesCorporate Actions - Dividends, Bonus, Splits, Buyback Etcagrawal.minNo ratings yet

- Mepal LeafDocument8 pagesMepal LeafMuhammadArshadNo ratings yet

- Formation Incoporation of CompaniesDocument21 pagesFormation Incoporation of CompaniesNAGARAJACHARI KAMMARANo ratings yet

- Section 73. Books To Be Kept Stock Transfer Agent. - Every Corporation Shall Keep and Carefully Preserve at ItsDocument9 pagesSection 73. Books To Be Kept Stock Transfer Agent. - Every Corporation Shall Keep and Carefully Preserve at ItsYarah MNo ratings yet

- Thirumalai Chemicals LTD - 2018 PDFDocument132 pagesThirumalai Chemicals LTD - 2018 PDFRavi PanaraNo ratings yet

- Asset AcquisitionDocument3 pagesAsset AcquisitionMerliza JusayanNo ratings yet

- London Listed Property Company Focused On Emerging Europe: Investor Presentation Q2 2016Document26 pagesLondon Listed Property Company Focused On Emerging Europe: Investor Presentation Q2 2016Alexandra BugaNo ratings yet

- Air India Annual Return 2022 23Document15 pagesAir India Annual Return 2022 23Ayush DuttaNo ratings yet

- Merger of Tata Steel and CorusDocument24 pagesMerger of Tata Steel and Coruspratik tanna100% (17)

- Raroc Cimb PDFDocument202 pagesRaroc Cimb PDFsaeful anwariNo ratings yet

- Group Company Liability: Martin Petrin Barnali ChoudhuryDocument26 pagesGroup Company Liability: Martin Petrin Barnali Choudhuryrishabh guptaNo ratings yet

- Corporation Code - de Leon PDFDocument1,114 pagesCorporation Code - de Leon PDFBelteshazzarL.Cabacang100% (1)

- Company Law Live Mock Test PDFDocument4 pagesCompany Law Live Mock Test PDFभगवा समर्थकNo ratings yet

- Financial Management Case Study ON Agency Problem Agency ProblemDocument3 pagesFinancial Management Case Study ON Agency Problem Agency ProblemV SHARAVANI MBANo ratings yet

- Quizzer in Corpo Set ADocument11 pagesQuizzer in Corpo Set ARon Nixon MendozaNo ratings yet

- Chapter 14 - Dividend PolicyDocument38 pagesChapter 14 - Dividend PolicyRAQAEL RHODENo ratings yet

- Opening A Business Is A Lot of Work, You Have To Comply With All The Requirements To Start. Here'S How You Go About ItDocument11 pagesOpening A Business Is A Lot of Work, You Have To Comply With All The Requirements To Start. Here'S How You Go About Itcamille agudaNo ratings yet

- Caac Fire and Rescue Volunteer Inc.: By-Laws OFDocument4 pagesCaac Fire and Rescue Volunteer Inc.: By-Laws OFJosephGerardBersalonaNo ratings yet