Download as xlsx, pdf, or txt

You might also like

- 3 Cash Flow Model 0Document14 pages3 Cash Flow Model 0kumarmayurNo ratings yet

- Base Case 1 Downside Case 2 Upside Case 3: InputsDocument34 pagesBase Case 1 Downside Case 2 Upside Case 3: InputsjamesNo ratings yet

- Ch03 P15 SolutionsDocument16 pagesCh03 P15 SolutionsM E0% (1)

- FM - HPCL - 10Hrs - Final 1705Document18 pagesFM - HPCL - 10Hrs - Final 1705sudeepregmi2007No ratings yet

- Axial 5 Minute DCF ToolDocument11 pagesAxial 5 Minute DCF ToolziuziNo ratings yet

- Trend AnalysisDocument9 pagesTrend Analysisshades13579No ratings yet

- Task 1 - Example AnswerDocument9 pagesTask 1 - Example AnswerMinh Hoàng 2001 NguyễnNo ratings yet

- Task 3 - Example AnswerDocument8 pagesTask 3 - Example AnswerMinh Hoàng 2001 NguyễnNo ratings yet

- MacroDocument8 pagesMacroAngie TorresNo ratings yet

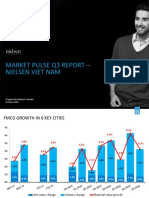

- Nielsen Market Pulse Q3 2016Document8 pagesNielsen Market Pulse Q3 2016K57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- Ceo2023 Crosstabs Final All 1Document14 pagesCeo2023 Crosstabs Final All 1Karlin RickNo ratings yet

- Peer Company COmparision For Startups NewDocument2 pagesPeer Company COmparision For Startups NewBiki BhaiNo ratings yet

- Basic Economic FiguresDocument3 pagesBasic Economic FiguresJestine Marcel FerraerNo ratings yet

- Ca Manish Chokshi Presence in Capital MarketDocument127 pagesCa Manish Chokshi Presence in Capital Marketthe libyan guyNo ratings yet

- 352 - Infographic Market Pulse Q1 2018 - 1525948613Document2 pages352 - Infographic Market Pulse Q1 2018 - 1525948613K57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- Market Pulse Q1 - 18Document2 pagesMarket Pulse Q1 - 18Duy Nguyen Ho ThienNo ratings yet

- Axis Bank InvestmentDocument32 pagesAxis Bank Investment22satendraNo ratings yet

- CCAFDocument8 pagesCCAFsanket patilNo ratings yet

- DCF Template - v1Document1 pageDCF Template - v1prathmesh KolteNo ratings yet

- Proximus Consensus Ahead of q1 2023Document4 pagesProximus Consensus Ahead of q1 2023Laurent MillerNo ratings yet

- Fortnightly Banking Update: Deposit Growth Moderated But Bank Credit Growth Moderates Even MoreDocument3 pagesFortnightly Banking Update: Deposit Growth Moderated But Bank Credit Growth Moderates Even Morekumar ganeshNo ratings yet

- DMG Events Diplomatic Networking Event - Presentation SlidesDocument36 pagesDMG Events Diplomatic Networking Event - Presentation Slideslaura030701No ratings yet

- Views On Markets and SectorsDocument19 pagesViews On Markets and SectorskundansudNo ratings yet

- Fixed and Saving Deposit Rate VACDocument8 pagesFixed and Saving Deposit Rate VACvinishchandraaNo ratings yet

- Ejercicio Expectativas MacroDocument4 pagesEjercicio Expectativas MacroDavid AlvarezNo ratings yet

- Assumptions: Dec-YE Unit 2018A 2019A 2020A 2021E 2022E 2023E 2024E 2025EDocument3 pagesAssumptions: Dec-YE Unit 2018A 2019A 2020A 2021E 2022E 2023E 2024E 2025ENouf ANo ratings yet

- 01-3 Plan Lineal VendedorDocument26 pages01-3 Plan Lineal VendedorJefer AnHe VelezNo ratings yet

- BNM - Analisis Financiero Estructural Nov 2000 - Oct 2001Document2 pagesBNM - Analisis Financiero Estructural Nov 2000 - Oct 2001gonzaloromaniNo ratings yet

- Q3 2022-FinalDocument71 pagesQ3 2022-FinalcarunsbbhNo ratings yet

- Industry ReportDocument77 pagesIndustry ReportabhishakxtNo ratings yet

- Real GDP Growth (Annual Percent Change)Document3 pagesReal GDP Growth (Annual Percent Change)matilda.amsNo ratings yet

- Accenture Fin Model - Par - V1Document9 pagesAccenture Fin Model - Par - V1shahsamkit08No ratings yet

- Newbrook Long - Short Equity Strategy - 4Document3 pagesNewbrook Long - Short Equity Strategy - 4dch204No ratings yet

- Student Distribution at Plano ISD Senior HighsDocument4 pagesStudent Distribution at Plano ISD Senior HighsDavid StringfellowNo ratings yet

- Task 1 - DataDocument5 pagesTask 1 - DataMinh Hoàng 2001 NguyễnNo ratings yet

- Project FşnanceDocument2 pagesProject FşnanceAhmet ErNo ratings yet

- Macro Economics Aspects of BudgetDocument44 pagesMacro Economics Aspects of Budget6882535No ratings yet

- Dec-YE Unit 2018A 2019A 2020A 2021E 2022E 2023E 2024E 2025E Comments For StudentDocument1 pageDec-YE Unit 2018A 2019A 2020A 2021E 2022E 2023E 2024E 2025E Comments For StudentNouf ANo ratings yet

- Financial Modeling Mid-Term ExamDocument17 pagesFinancial Modeling Mid-Term ExamКамиль БайбуринNo ratings yet

- 1.0 Kenyas Public Debt Dr. Abraham RugoDocument17 pages1.0 Kenyas Public Debt Dr. Abraham RugoREJAY89No ratings yet

- RV Capital Factsheet 2017-03Document1 pageRV Capital Factsheet 2017-03Rocco HuangNo ratings yet

- GCA Altium Digital - Media & Internet Monitor Q3 2020Document26 pagesGCA Altium Digital - Media & Internet Monitor Q3 2020John SmithNo ratings yet

- 2019 2018 2017 2016 2015 AssetsDocument1 page2019 2018 2017 2016 2015 AssetsFaisal RafiqueNo ratings yet

- Weekly Economic & Financial Commentary 15julyDocument13 pagesWeekly Economic & Financial Commentary 15julyErick Abraham MarlissaNo ratings yet

- Tax BudgetDocument31 pagesTax BudgetJim ParkerNo ratings yet

- Nielsen Market Pulse Q2 2018Document6 pagesNielsen Market Pulse Q2 2018K57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- PLANILLA CADENAS PORCELANADocument2 pagesPLANILLA CADENAS PORCELANACarolina Andrea Miranda IrairaNo ratings yet

- Peer Company Comparison For StartupsDocument2 pagesPeer Company Comparison For StartupsBiki BhaiNo ratings yet

- Econometria Clase 3Document34 pagesEconometria Clase 3Alberto LopezNo ratings yet

- GDP (Usd Billion) & GDP Per Capital (Usd)Document8 pagesGDP (Usd Billion) & GDP Per Capital (Usd)Minh HảiNo ratings yet

- GDP (Usd Billion) & GDP Per Capital (Usd)Document8 pagesGDP (Usd Billion) & GDP Per Capital (Usd)Minh HảiNo ratings yet

- Ejemplo - Riesgo y RendimientoDocument24 pagesEjemplo - Riesgo y RendimientoMiguel GNo ratings yet

- Use of e Cigarettes Among Young People in Great Britain 2022Document14 pagesUse of e Cigarettes Among Young People in Great Britain 2022Susan CapellanNo ratings yet

- Investment Fund Performance ReportDocument2 pagesInvestment Fund Performance Reportmahindarseth963No ratings yet

- Corp Vs - Pers TaxDocument3 pagesCorp Vs - Pers TaxmrpoissonNo ratings yet

- Sketchers Financial ModelDocument56 pagesSketchers Financial ModelsaonNo ratings yet

- Consumer Insights AsiaDocument23 pagesConsumer Insights AsiaDương Huy Chương ĐặngNo ratings yet

- Propuesta OVBK - V2Document3 pagesPropuesta OVBK - V2JUAN CAMILO GUZMANNo ratings yet

- Middle East and North Africa Quarterly Economic Brief, January 2014: Growth Slowdown Heightens the Need for ReformsFrom EverandMiddle East and North Africa Quarterly Economic Brief, January 2014: Growth Slowdown Heightens the Need for ReformsNo ratings yet

- Math Practice Simplified: Decimals & Percents (Book H): Practicing the Concepts of Decimals and PercentagesFrom EverandMath Practice Simplified: Decimals & Percents (Book H): Practicing the Concepts of Decimals and PercentagesRating: 5 out of 5 stars5/5 (3)

- Pandit Automotive Pvt. Ltd.Document6 pagesPandit Automotive Pvt. Ltd.JudicialNo ratings yet

- 1995 Jan07 Subject-1995Document110 pages1995 Jan07 Subject-1995anonymous284.1.11No ratings yet

- Market Structure ShiftDocument2 pagesMarket Structure ShiftZahid BoraNo ratings yet

- ZUNG ZANG WOOD PRODUCTS SDN BHD & ORS V KWANDocument23 pagesZUNG ZANG WOOD PRODUCTS SDN BHD & ORS V KWANwedyinganywaysNo ratings yet

- CH 07Document100 pagesCH 07SamiNaserNo ratings yet

- Role-Model Leaders: Leadership Traits and ValuesDocument9 pagesRole-Model Leaders: Leadership Traits and ValuesRUTVIKA DHANESHKUMARKUNDAGOLNo ratings yet

- DG Bank Directory - WebsiteDocument1 pageDG Bank Directory - WebsiteKarla Charmagne SalivaNo ratings yet

- Hong KongDocument12 pagesHong KongThảo Nguyễn PhươngNo ratings yet

- Tempalte e BankingDocument12 pagesTempalte e Bankingcorneles tuanakottaNo ratings yet

- Livelihood Sustainability of Handloom Weavers: A Study in Sualkuchi, AssamDocument31 pagesLivelihood Sustainability of Handloom Weavers: A Study in Sualkuchi, AssamAbhishek VermaNo ratings yet

- Midterm PresentationDocument88 pagesMidterm PresentationRowell Ian Gana-anNo ratings yet

- Equal Payment SeriesDocument5 pagesEqual Payment SeriesMaya OlleikNo ratings yet

- Atikah Beauty SalonDocument15 pagesAtikah Beauty SalonEko Firdausta TariganNo ratings yet

- Assignment Print View 3.8Document5 pagesAssignment Print View 3.8Zach JaapNo ratings yet

- Define-Phase Yellow BeltDocument52 pagesDefine-Phase Yellow BeltBhadri NarayananNo ratings yet

- Fua Cun vs. Summers, 44 PHIL 705Document3 pagesFua Cun vs. Summers, 44 PHIL 705Vincent BernardoNo ratings yet

- ACT26 Ch05 Net-Taxable-EstateDocument7 pagesACT26 Ch05 Net-Taxable-EstateMark BajacanNo ratings yet

- Depreciation ExerciseDocument7 pagesDepreciation ExerciseMuskan LohariwalNo ratings yet

- ESG Data Free Trial - RefinitivDocument4 pagesESG Data Free Trial - RefinitivgodkabetaNo ratings yet

- PPDA Contracts 2023Document56 pagesPPDA Contracts 2023richard.musiimeNo ratings yet

- Accounting An Introduction NZ 2nd Edition Atrill Test BankDocument26 pagesAccounting An Introduction NZ 2nd Edition Atrill Test Banksophronianhat6dk2k100% (30)

- Indian Economic and Political History: Rajesh Bhattacharya Email: Virtual Lounge: TBADocument14 pagesIndian Economic and Political History: Rajesh Bhattacharya Email: Virtual Lounge: TBANaunihal KumarNo ratings yet

- David RicardoDocument11 pagesDavid RicardoAditi MalaniNo ratings yet

- November CY2022 Cold Storage WarehouseDocument27 pagesNovember CY2022 Cold Storage Warehousedexterbautistadecember161985No ratings yet

- Pleting The CycleDocument21 pagesPleting The CycleAL Babaran CanceranNo ratings yet

- Transunion Cibil ReportDocument39 pagesTransunion Cibil ReportSHREYAS KHANOLKARNo ratings yet

- CreditReport Piramal - Mahendra Jain - 2023 - 05 - 12 - 11 - 43 - 04.pdf 12-May-2023 PDFDocument7 pagesCreditReport Piramal - Mahendra Jain - 2023 - 05 - 12 - 11 - 43 - 04.pdf 12-May-2023 PDFGamer SinghNo ratings yet

- Corporations CH 12 Lecture 1Document18 pagesCorporations CH 12 Lecture 1Faisal SiddiquiNo ratings yet

- Feasibility StudiesDocument60 pagesFeasibility Studiesice100% (2)

- The New India Assurance Co. Ltd. (Government of India Undertaking)Document3 pagesThe New India Assurance Co. Ltd. (Government of India Undertaking)Amit YearnNo ratings yet