Download as rtf, pdf, or txt

You might also like

- Key Highlights of The Proposed GST Changes in Union Budget 2023 24 For Easy DigestDocument23 pagesKey Highlights of The Proposed GST Changes in Union Budget 2023 24 For Easy DigestshwetaNo ratings yet

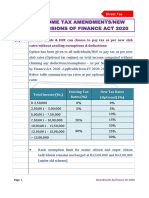

- Income Tax Amendments/New Provisions of Finance Act 2020Document46 pagesIncome Tax Amendments/New Provisions of Finance Act 2020shubhamworkNo ratings yet

- Decoding Indian Union Budget Finance Bil PDFDocument7 pagesDecoding Indian Union Budget Finance Bil PDFkumarNo ratings yet

- Amendments in Finance Bill 2022Document20 pagesAmendments in Finance Bill 2022Prashant MunotNo ratings yet

- Delayed Payment of Tax - Taxguru - inDocument2 pagesDelayed Payment of Tax - Taxguru - insukantabera215No ratings yet

- CBDT Notifies Rules For LTC Cash Voucher Scheme - Taxguru - inDocument3 pagesCBDT Notifies Rules For LTC Cash Voucher Scheme - Taxguru - inrituneshNo ratings yet

- Latest Circulars, Notifications and Press Releases: 2. This Notification Shall Come Into Force From The 1Document0 pagesLatest Circulars, Notifications and Press Releases: 2. This Notification Shall Come Into Force From The 1Ketan ThakkarNo ratings yet

- SKA - Sectionwise GST Analysis - Finance Bill 2021Document24 pagesSKA - Sectionwise GST Analysis - Finance Bill 2021Sandip GoyalNo ratings yet

- C-7, Pashchimi Marg, Vasant Vihar, New Delhi - 110057Document8 pagesC-7, Pashchimi Marg, Vasant Vihar, New Delhi - 110057Mahaveer DhelariyaNo ratings yet

- FBT Perks Vs FBTDocument5 pagesFBT Perks Vs FBTnirav_poptaniNo ratings yet

- FAQ On Budget FY 2020-21Document9 pagesFAQ On Budget FY 2020-21GUNANo ratings yet

- RSM India Newsflash - Employees Guidance On New Vs Old Tax Regime Individuals April 2020Document17 pagesRSM India Newsflash - Employees Guidance On New Vs Old Tax Regime Individuals April 2020Rohan JainNo ratings yet

- Page 1 of 2Document2 pagesPage 1 of 2Hr legaladviserNo ratings yet

- Going To File GST Refund Know The Important Changes in The Process First.Document2 pagesGoing To File GST Refund Know The Important Changes in The Process First.Richa SachdevaNo ratings yet

- Minimum Alternate TaxDocument5 pagesMinimum Alternate TaxVaibhav VijayNo ratings yet

- CA CS CMA Final Statutory Updates For Nov Dec 2020Document43 pagesCA CS CMA Final Statutory Updates For Nov Dec 2020Anu GraphicsNo ratings yet

- Decoding Indian Union BudgetDocument6 pagesDecoding Indian Union BudgetkumarNo ratings yet

- Taxation Assignment Budget Proposal 2020Document20 pagesTaxation Assignment Budget Proposal 2020Shivani DuttNo ratings yet

- Mat - PPT FinalDocument18 pagesMat - PPT FinalAkash PatelNo ratings yet

- Income Tax AmendmentsNew Provisions of Finance Act 2020Document26 pagesIncome Tax AmendmentsNew Provisions of Finance Act 2020Piyush HarlalkaNo ratings yet

- June 2020 SP 1Document7 pagesJune 2020 SP 1Avinash ShettyNo ratings yet

- Reverse Charge Mechanism in GST Regime With ChartDocument14 pagesReverse Charge Mechanism in GST Regime With ChartAnkur ShahNo ratings yet

- Taxguru - In-Reverse Charge Mechanism in GST Regime With ChartDocument20 pagesTaxguru - In-Reverse Charge Mechanism in GST Regime With Chartvikrant.chutke12No ratings yet

- Memo FB 2023Document90 pagesMemo FB 2023Maheshkumar PerlaNo ratings yet

- Article On Reverse Charge 28jul2017Document8 pagesArticle On Reverse Charge 28jul2017kumar45caNo ratings yet

- Highlights of Key Changes in GST W.E.F January 01, 2022Document5 pagesHighlights of Key Changes in GST W.E.F January 01, 2022sumathiravirajNo ratings yet

- Mat AmtDocument10 pagesMat AmtarafatNo ratings yet

- VILGST - CGST - Circular - Instruction No. 01 - 2022-GSTDocument4 pagesVILGST - CGST - Circular - Instruction No. 01 - 2022-GSTJAYKISHAN VIDHWANINo ratings yet

- F6zwe FinbillDocument22 pagesF6zwe FinbillZvikomborero Tavonga MuchandibayaNo ratings yet

- Reverse Charge Mechanism in GST Regime With Chart – Updated Till Date - Taxguru - inDocument19 pagesReverse Charge Mechanism in GST Regime With Chart – Updated Till Date - Taxguru - inAjit GuptaNo ratings yet

- Reply For Hashim KhanDocument2 pagesReply For Hashim Khanhamza awan0% (1)

- Cir 188 20 2022 CGSTDocument4 pagesCir 188 20 2022 CGSTAtanu Kumar SenNo ratings yet

- Service Tax Changes Process Amounting To Manufacture or Production of Goods Excluding Alcoholic Beverages For Human ConsumptionDocument5 pagesService Tax Changes Process Amounting To Manufacture or Production of Goods Excluding Alcoholic Beverages For Human ConsumptionYesBroker InNo ratings yet

- Sales Tax Recent ChangesDocument2 pagesSales Tax Recent ChangesMishal RizwanNo ratings yet

- Circular 1 2021Document2 pagesCircular 1 2021NESL WebsiteNo ratings yet

- Circular CGST 197Document5 pagesCircular CGST 197Jaipur-B Gr-2No ratings yet

- UnionBudget-2020-Presentation by CA BM BiyaniDocument83 pagesUnionBudget-2020-Presentation by CA BM BiyaniMohammad AfrozNo ratings yet

- Do You Know GST - August 2021Document11 pagesDo You Know GST - August 2021CA Ranjan MehtaNo ratings yet

- Circular No.45Document5 pagesCircular No.45Hr legaladviserNo ratings yet

- Special Provisions Relating To Taxation of IncomeDocument27 pagesSpecial Provisions Relating To Taxation of IncomeABC 123No ratings yet

- Important GST Amendments in Budget 2023 - Taxguru - in PDFDocument10 pagesImportant GST Amendments in Budget 2023 - Taxguru - in PDFPawan AswaniNo ratings yet

- Section 206AADocument8 pagesSection 206AATaxation TaxNo ratings yet

- Reverse Charge Mechanism in GST Regime With ChartDocument6 pagesReverse Charge Mechanism in GST Regime With ChartSwathi VikashiniNo ratings yet

- Charge of Income TaxDocument72 pagesCharge of Income TaxAkanksha BohraNo ratings yet

- Page 1 of 8Document8 pagesPage 1 of 8Faiqa HamidNo ratings yet

- 2013 P T D 1420Document6 pages2013 P T D 1420haseeb AhsanNo ratings yet

- Finance Bill 2009 - Direct Tax Proposals: Presentation By: CA. Kapil Goel, ACA, LLB Chartered Accountant New DelhiDocument43 pagesFinance Bill 2009 - Direct Tax Proposals: Presentation By: CA. Kapil Goel, ACA, LLB Chartered Accountant New Delhipuritansoul100% (2)

- Taxable Event in GST 3.1 Meaning of Taxable EventDocument24 pagesTaxable Event in GST 3.1 Meaning of Taxable Eventhariom bajpaiNo ratings yet

- GST Update124Document6 pagesGST Update124suhani singhNo ratings yet

- Instructions For Filling Out FORM ITR 3Document231 pagesInstructions For Filling Out FORM ITR 3Samantha JNo ratings yet

- Claim of ITC As GSTR-2B Is Mandatory W.E.F. 01.01.2022Document3 pagesClaim of ITC As GSTR-2B Is Mandatory W.E.F. 01.01.2022ravindra kumar jainNo ratings yet

- Circular Refund 147-1.5 Times RefundDocument5 pagesCircular Refund 147-1.5 Times Refundbanerjeeankita13No ratings yet

- Income Tax 7 Lakh CircularDocument3 pagesIncome Tax 7 Lakh CircularMCB ACCOUNT BRANCHNo ratings yet

- Section 115JC - Special Provisions For Payment of Tax by Certain Persons Other Than A Company.Document1 pageSection 115JC - Special Provisions For Payment of Tax by Certain Persons Other Than A Company.Anand LakraNo ratings yet

- Imposition If TaxDocument14 pagesImposition If TaxEDWARD BIRYETEGANo ratings yet

- Circular Refund 137 7 2020Document3 pagesCircular Refund 137 7 2020Shirish JainNo ratings yet

- FAQsonTDS 230221 120909Document8 pagesFAQsonTDS 230221 120909Bharath UGNo ratings yet

- RSM India Union Budget 2021 HighlightsDocument132 pagesRSM India Union Budget 2021 HighlightsSunil KumarNo ratings yet

- Circular No. 162 - 18 - 2021 - GSTDocument4 pagesCircular No. 162 - 18 - 2021 - GSTRamesh GoddumariNo ratings yet

- Guidance Note On Internal Audit of General Insurance CompaniesDocument128 pagesGuidance Note On Internal Audit of General Insurance CompaniesABC 123No ratings yet

- Management Accountant March-2016Document124 pagesManagement Accountant March-2016ABC 123No ratings yet

- Management Accountant April-2016Document124 pagesManagement Accountant April-2016ABC 123No ratings yet

- Management Accountant Feb-2016Document124 pagesManagement Accountant Feb-2016ABC 123No ratings yet

- Management Accountant Jan-2016Document124 pagesManagement Accountant Jan-2016ABC 123No ratings yet

- Management Accountant March-2017Document124 pagesManagement Accountant March-2017ABC 123No ratings yet

- Management Accountant May-2016Document124 pagesManagement Accountant May-2016ABC 123No ratings yet

- Management Accountant Aug-2016Document124 pagesManagement Accountant Aug-2016ABC 123No ratings yet

- Management Accountant June-2016Document124 pagesManagement Accountant June-2016ABC 123No ratings yet

- Management Accountant Dec-2016Document124 pagesManagement Accountant Dec-2016ABC 123No ratings yet

- Management Accountant Nov 2017Document124 pagesManagement Accountant Nov 2017ABC 123No ratings yet

- Management Accountant Feb-2017Document124 pagesManagement Accountant Feb-2017ABC 123No ratings yet

- Management Accountant June 2018Document124 pagesManagement Accountant June 2018ABC 123No ratings yet

- Management Accountant - June 2017Document132 pagesManagement Accountant - June 2017ABC 123No ratings yet

- Management Accountant May-2017Document124 pagesManagement Accountant May-2017ABC 123No ratings yet

- Management Accountant March 2018Document124 pagesManagement Accountant March 2018ABC 123No ratings yet

- Management Accountant OCTOBER 2017Document124 pagesManagement Accountant OCTOBER 2017ABC 123No ratings yet

- Management Accountant Oct 2018Document124 pagesManagement Accountant Oct 2018ABC 123No ratings yet

- Management Accountant April-2017Document124 pagesManagement Accountant April-2017ABC 123No ratings yet

- Management Accountant Dec 2018Document124 pagesManagement Accountant Dec 2018ABC 123No ratings yet

- Management Accountant Jan-2019Document124 pagesManagement Accountant Jan-2019ABC 123No ratings yet

- Management Accountant Jan-2017Document124 pagesManagement Accountant Jan-2017ABC 123No ratings yet

- Management Accountant Nov 2018Document124 pagesManagement Accountant Nov 2018ABC 123No ratings yet

- Management Accountant Nov 2019Document124 pagesManagement Accountant Nov 2019ABC 123No ratings yet

- Management Accountant July 2018Document124 pagesManagement Accountant July 2018ABC 123No ratings yet

- Management Accountant May2019Document124 pagesManagement Accountant May2019ABC 123No ratings yet

- Management Accountant March 2019Document124 pagesManagement Accountant March 2019ABC 123No ratings yet

- Management Accountant January - 2018Document124 pagesManagement Accountant January - 2018ABC 123No ratings yet

- Management Accountant FEBRUARY-2019Document124 pagesManagement Accountant FEBRUARY-2019ABC 123No ratings yet