P-Cr-002r1sthandar LCC PDF

P-Cr-002r1sthandar LCC PDF

You might also like

- Maintenance Replacement and ReliabilityDocument17 pagesMaintenance Replacement and Reliabilitybederinadml100% (1)

- BCA 2015 Operations Planning GuideDocument52 pagesBCA 2015 Operations Planning Guideamenendezam100% (1)

- Economics of Chemical Plant Lec 33-36Document46 pagesEconomics of Chemical Plant Lec 33-36Muhammad Ahms100% (3)

- Estimation HandbookDocument54 pagesEstimation HandbookMathias Wafawanaka100% (1)

- Chap 6.0 Manufacturing Cost EstimationDocument20 pagesChap 6.0 Manufacturing Cost EstimationIR Ika EtyEtyka DoraNo ratings yet

- CoolingTower (ECP 09) AFCESA M&V TemplateDocument21 pagesCoolingTower (ECP 09) AFCESA M&V TemplatesubasratnaNo ratings yet

- Calculating The Sos in Natural Gas - Aga Report No. 10 To Aga Report No. 8Document11 pagesCalculating The Sos in Natural Gas - Aga Report No. 10 To Aga Report No. 8Malouk CheniouniNo ratings yet

- System Analysis Design AmityDocument29 pagesSystem Analysis Design Amitygaurav0% (1)

- Instrumentation QC Inspector Course & Interview QuestionsDocument12 pagesInstrumentation QC Inspector Course & Interview Questionszhangyili100% (2)

- Norsok O-CR-001r1 Life Cycle Cost For Systems & EquipmentDocument38 pagesNorsok O-CR-001r1 Life Cycle Cost For Systems & EquipmentspottedkelpieNo ratings yet

- Schuh2015 Article Cost-optimalSparePartsInventorDocument8 pagesSchuh2015 Article Cost-optimalSparePartsInventorvaleNo ratings yet

- 8.power Plant EconomicsDocument28 pages8.power Plant EconomicsRAVI KIRAN CHALLAGUNDLA100% (1)

- Unit 5Document43 pagesUnit 5Kama RajNo ratings yet

- Ch4 LectureDocument34 pagesCh4 Lectureebro nNo ratings yet

- Equipment Costs, Maintenance, Flow ChartDocument7 pagesEquipment Costs, Maintenance, Flow ChartYALLALING KULIGODNo ratings yet

- Norsok Standar Lyfe Cycle Cost PDFDocument38 pagesNorsok Standar Lyfe Cycle Cost PDFRobinsonNo ratings yet

- CE Lecture# 03Document22 pagesCE Lecture# 03ATTA100% (1)

- PPE Lecture3Document25 pagesPPE Lecture3Alvin IsmailNo ratings yet

- Total Solution Services For Advanced Maintenance of Thermal Power-Generation PlantsDocument6 pagesTotal Solution Services For Advanced Maintenance of Thermal Power-Generation PlantsRam MohanNo ratings yet

- Estimation of Operating CostsDocument20 pagesEstimation of Operating CostsGabriella PrathapsonNo ratings yet

- FLUKE - PDM OverviewDocument5 pagesFLUKE - PDM OverviewofedulloNo ratings yet

- Chapter 4 (Compatibility Mode)Document26 pagesChapter 4 (Compatibility Mode)AndualemEndrisNo ratings yet

- Costing and Project EvaluationDocument37 pagesCosting and Project Evaluationdani2611No ratings yet

- Lec 9Document39 pagesLec 9Mortada OthmanNo ratings yet

- Material Planning and Inventory ControlDocument7 pagesMaterial Planning and Inventory Controlsazzadasif.irlNo ratings yet

- Economics of Construction EquipmentDocument10 pagesEconomics of Construction Equipmentshubham chikuNo ratings yet

- Cost Estimation and EvaluationDocument4 pagesCost Estimation and EvaluationMuddassir DanishNo ratings yet

- Cost & Cost ConceptsDocument51 pagesCost & Cost ConceptsEzhil Vendhan PalanisamyNo ratings yet

- Equip. Note PDFDocument16 pagesEquip. Note PDFhailush girmay100% (1)

- OverheadsDocument25 pagesOverheadslalitNo ratings yet

- A Life Cycle Cost Calculation and Management System For Machine ToolsDocument6 pagesA Life Cycle Cost Calculation and Management System For Machine ToolsOscar TeknikerNo ratings yet

- Economic ReportDocument9 pagesEconomic ReportYeeXuan TenNo ratings yet

- ENGG ZC242 Regular Solution MidsemDocument4 pagesENGG ZC242 Regular Solution MidsemymsyaseenNo ratings yet

- Life Cycle Cost Analysis Manual: State of Illinois Capital Development BoardDocument23 pagesLife Cycle Cost Analysis Manual: State of Illinois Capital Development Boardrizwan khanNo ratings yet

- SMRP Metric 1.3 Maintenance Unit CostDocument5 pagesSMRP Metric 1.3 Maintenance Unit CostJorge FracaroNo ratings yet

- Brick WorkDocument33 pagesBrick WorkIbrahim AliNo ratings yet

- Reee 002Document15 pagesReee 002Imran Nawaz MehthalNo ratings yet

- Evaluating Capital Cost Estimates-Aug-11Document8 pagesEvaluating Capital Cost Estimates-Aug-11Ashfaq NoorNo ratings yet

- Maintenance Management-4, 2019Document12 pagesMaintenance Management-4, 2019Suman KumarNo ratings yet

- National Thermal Power Corporation Limited: November 2002Document50 pagesNational Thermal Power Corporation Limited: November 2002SamNo ratings yet

- Depreciation Depreciation: by S KrugonDocument15 pagesDepreciation Depreciation: by S KrugonBRAHMAIAH NAKKANo ratings yet

- Lecture 6fDocument30 pagesLecture 6fhiteshNo ratings yet

- CEV633 Engineering Economics & Project ManagementDocument59 pagesCEV633 Engineering Economics & Project ManagementgnaniNo ratings yet

- Maintenance ManagementDocument44 pagesMaintenance ManagementDwi Putri Hidayat100% (4)

- 1.3 Maintenance Unit Cost: Business & Management MetricDocument3 pages1.3 Maintenance Unit Cost: Business & Management MetricAlexander Arias RuizNo ratings yet

- Operations ManagementDocument32 pagesOperations ManagementAsif S KhanNo ratings yet

- Lecture Note On Construction Equipment ManagementDocument84 pagesLecture Note On Construction Equipment ManagementAberaMamoJaletaNo ratings yet

- Preliminary Operations and Maintenance Plan: Cassadaga Wind FarmDocument9 pagesPreliminary Operations and Maintenance Plan: Cassadaga Wind FarmDivyansh Singh ChauhanNo ratings yet

- Costs Analysis of Constructions Heavy Eq PDFDocument13 pagesCosts Analysis of Constructions Heavy Eq PDFJuan Carlos Cruz ENo ratings yet

- Costing Formulas PDFDocument86 pagesCosting Formulas PDFsubbu100% (3)

- Operating Cost and Estimate of Cost: Submitted To: - Submitted By:-Prof - Gunjan DivediDocument10 pagesOperating Cost and Estimate of Cost: Submitted To: - Submitted By:-Prof - Gunjan DivediRohit SinghNo ratings yet

- Unit 6 PDFDocument10 pagesUnit 6 PDFpayal sachdevNo ratings yet

- Disclosure To Promote The Right To InformationDocument13 pagesDisclosure To Promote The Right To InformationAnonymous 1gp9bFNo ratings yet

- Maintenance FunctionsDocument41 pagesMaintenance FunctionsAryyaka SarkarNo ratings yet

- 6.3 Applying Annual-Worth Analysis 6.3.1 Benefits of AE AnalysisDocument6 pages6.3 Applying Annual-Worth Analysis 6.3.1 Benefits of AE Analysisshintya nadaNo ratings yet

- Dire Dawa University Institute of Technology: Electrical Engineering Department Power System Planning and OperationDocument8 pagesDire Dawa University Institute of Technology: Electrical Engineering Department Power System Planning and OperationROBSANNo ratings yet

- Cost Analysis Using Break-Even Analysis: (Process Selection)Document28 pagesCost Analysis Using Break-Even Analysis: (Process Selection)zelalem wegayehuNo ratings yet

- Life Cycle CostingDocument61 pagesLife Cycle CostingMd Jalal Uddin Rumi100% (1)

- Case Study On The Profit Margin Model of Multi-Site Testing Technology For SemiconductorsDocument18 pagesCase Study On The Profit Margin Model of Multi-Site Testing Technology For SemiconductorsAJER JOURNALNo ratings yet

- Life Cycle Cost AnalysisDocument39 pagesLife Cycle Cost AnalysisJayaprakash SankaranNo ratings yet

- 12b.standard Costing XDocument18 pages12b.standard Costing XAbhinav AshishNo ratings yet

- Production and Maintenance Optimization Problems: Logistic Constraints and Leasing Warranty ServicesFrom EverandProduction and Maintenance Optimization Problems: Logistic Constraints and Leasing Warranty ServicesNo ratings yet

- Practical, Made Easy Guide To Building, Office And Home Automation Systems - Part OneFrom EverandPractical, Made Easy Guide To Building, Office And Home Automation Systems - Part OneNo ratings yet

- The Calibration of Flow Meters PDFDocument35 pagesThe Calibration of Flow Meters PDFRené Mora-CasalNo ratings yet

- Liquid Measurement Station Design 2017 ISHMDocument5 pagesLiquid Measurement Station Design 2017 ISHMMalouk CheniouniNo ratings yet

- Is 1448 (P 1) 2002 Determination of Acid Number of Petroleum Products by Potentiometric TitrationDocument17 pagesIs 1448 (P 1) 2002 Determination of Acid Number of Petroleum Products by Potentiometric TitrationMalouk CheniouniNo ratings yet

- Auditing Gas Measurement and Accounting Systems 2006 PDFDocument4 pagesAuditing Gas Measurement and Accounting Systems 2006 PDFMalouk CheniouniNo ratings yet

- Selection and Sizing of Control Valves For Natural Gas PDFDocument3 pagesSelection and Sizing of Control Valves For Natural Gas PDFMalouk CheniouniNo ratings yet

- Determination of Leakage and Unaccounted For Gas PDFDocument13 pagesDetermination of Leakage and Unaccounted For Gas PDFMalouk CheniouniNo ratings yet

- Calibration of An Ultrasonic Flow Meter For Hot Water PDFDocument8 pagesCalibration of An Ultrasonic Flow Meter For Hot Water PDFMalouk CheniouniNo ratings yet

- Elsevier - Ultrasonic Flow Metering Errors Due To Pulsating FlowDocument7 pagesElsevier - Ultrasonic Flow Metering Errors Due To Pulsating FlowMalouk CheniouniNo ratings yet

- AAP S8 SS Buttweld Fittings & Flanges E2 SDocument12 pagesAAP S8 SS Buttweld Fittings & Flanges E2 SMalouk CheniouniNo ratings yet

- T11 Coriolis PDFDocument19 pagesT11 Coriolis PDFMalouk Cheniouni100% (1)

- 83 Calibration Ultrasonic Flowmeters PDFDocument6 pages83 Calibration Ultrasonic Flowmeters PDFMalouk CheniouniNo ratings yet

- Model 500 (2350A) GC PDFDocument334 pagesModel 500 (2350A) GC PDFMalouk CheniouniNo ratings yet

- Ultrasonic Gas Flow Meter BasicsDocument7 pagesUltrasonic Gas Flow Meter BasicsMalouk CheniouniNo ratings yet

- Brochure - E-RTG ElectrificationDocument12 pagesBrochure - E-RTG Electrification003086No ratings yet

- MT6763 Android ScatterDocument13 pagesMT6763 Android ScatterLim Bun Lio0% (2)

- Microprocessor Book by B Ram CompressDocument2 pagesMicroprocessor Book by B Ram CompressSanika LandeNo ratings yet

- ListDocument2 pagesListAman GuptaNo ratings yet

- 193PST - TF1700 User ManualDocument75 pages193PST - TF1700 User ManualDNo ratings yet

- ITT565-Lab-week7-NURUL IZZATIDocument7 pagesITT565-Lab-week7-NURUL IZZATI2023379679No ratings yet

- Face Recognition TechnologyDocument9 pagesFace Recognition TechnologySireesha TekuruNo ratings yet

- Binance-Api DocumentationDocument4 pagesBinance-Api DocumentationIrmak ErkolNo ratings yet

- Qcvs PBL User GuideDocument30 pagesQcvs PBL User GuidejwinstonjacobNo ratings yet

- Practical SEDocument6 pagesPractical SEMohammadNo ratings yet

- FCU-6000 System ManualDocument68 pagesFCU-6000 System Manualadavit73No ratings yet

- RSE-1A1 Mlk2 Overview PDFDocument12 pagesRSE-1A1 Mlk2 Overview PDFAnonymous fE2l3DzlNo ratings yet

- Programacion HTML5 CC3 and JSDocument654 pagesProgramacion HTML5 CC3 and JSErick FloresNo ratings yet

- E17-7-Assessing The Kpi For The Supply ChainDocument4 pagesE17-7-Assessing The Kpi For The Supply ChainAmd BustosNo ratings yet

- Fianl Essay of OMDocument4 pagesFianl Essay of OMApurbo Sarkar ShohagNo ratings yet

- When Technology and Humanity Cross 1Document2 pagesWhen Technology and Humanity Cross 1Shainna Panopio100% (1)

- TML Civil Engineering Transducers: Strain Gauge-TypeDocument2 pagesTML Civil Engineering Transducers: Strain Gauge-TypeHemlata VermaNo ratings yet

- Xda-Developers - SECRET CODES - Omnia 2 GT-i8000 PDFDocument3 pagesXda-Developers - SECRET CODES - Omnia 2 GT-i8000 PDFM Arshad Iqbal HarralNo ratings yet

- 5 Steps To Operational Excellence PDFDocument9 pages5 Steps To Operational Excellence PDFdrustagiNo ratings yet

- Job Interview QuestionsDocument2 pagesJob Interview QuestionsashvajNo ratings yet

- CRM Initiatives by Lic of IndiaDocument5 pagesCRM Initiatives by Lic of Indiashivacrazze0% (1)

- CRDeDocument97 pagesCRDeluisxdNo ratings yet

- Estrategia de Desarrollo y Plan de RecursosDocument9 pagesEstrategia de Desarrollo y Plan de RecursosFrancisco Martinez Gallardo LascurainNo ratings yet

- Mindwave and Arduino: FeaturesDocument6 pagesMindwave and Arduino: FeaturesSiva KumarNo ratings yet

- Don't KnowDocument1 pageDon't KnowWindsor LewisNo ratings yet

- Objectives of Digital BankingDocument10 pagesObjectives of Digital BankingGourav jamwalNo ratings yet

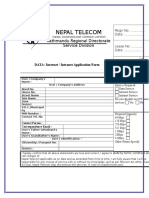

- Nepal Telecom: Kathmandu Regional Directorate Service DivisionDocument2 pagesNepal Telecom: Kathmandu Regional Directorate Service Divisionabhisek guptaNo ratings yet

- Biznet Dedicated Internet - Connection Setting - Linksys RouterDocument4 pagesBiznet Dedicated Internet - Connection Setting - Linksys RouterHanafi AljazaNo ratings yet

Download as pdf or txt

You might also like

- Maintenance Replacement and ReliabilityDocument17 pagesMaintenance Replacement and Reliabilitybederinadml100% (1)

- BCA 2015 Operations Planning GuideDocument52 pagesBCA 2015 Operations Planning Guideamenendezam100% (1)

- Economics of Chemical Plant Lec 33-36Document46 pagesEconomics of Chemical Plant Lec 33-36Muhammad Ahms100% (3)

- Estimation HandbookDocument54 pagesEstimation HandbookMathias Wafawanaka100% (1)

- Chap 6.0 Manufacturing Cost EstimationDocument20 pagesChap 6.0 Manufacturing Cost EstimationIR Ika EtyEtyka DoraNo ratings yet

- CoolingTower (ECP 09) AFCESA M&V TemplateDocument21 pagesCoolingTower (ECP 09) AFCESA M&V TemplatesubasratnaNo ratings yet

- Calculating The Sos in Natural Gas - Aga Report No. 10 To Aga Report No. 8Document11 pagesCalculating The Sos in Natural Gas - Aga Report No. 10 To Aga Report No. 8Malouk CheniouniNo ratings yet

- System Analysis Design AmityDocument29 pagesSystem Analysis Design Amitygaurav0% (1)

- Instrumentation QC Inspector Course & Interview QuestionsDocument12 pagesInstrumentation QC Inspector Course & Interview Questionszhangyili100% (2)

- Norsok O-CR-001r1 Life Cycle Cost For Systems & EquipmentDocument38 pagesNorsok O-CR-001r1 Life Cycle Cost For Systems & EquipmentspottedkelpieNo ratings yet

- Schuh2015 Article Cost-optimalSparePartsInventorDocument8 pagesSchuh2015 Article Cost-optimalSparePartsInventorvaleNo ratings yet

- 8.power Plant EconomicsDocument28 pages8.power Plant EconomicsRAVI KIRAN CHALLAGUNDLA100% (1)

- Unit 5Document43 pagesUnit 5Kama RajNo ratings yet

- Ch4 LectureDocument34 pagesCh4 Lectureebro nNo ratings yet

- Equipment Costs, Maintenance, Flow ChartDocument7 pagesEquipment Costs, Maintenance, Flow ChartYALLALING KULIGODNo ratings yet

- Norsok Standar Lyfe Cycle Cost PDFDocument38 pagesNorsok Standar Lyfe Cycle Cost PDFRobinsonNo ratings yet

- CE Lecture# 03Document22 pagesCE Lecture# 03ATTA100% (1)

- PPE Lecture3Document25 pagesPPE Lecture3Alvin IsmailNo ratings yet

- Total Solution Services For Advanced Maintenance of Thermal Power-Generation PlantsDocument6 pagesTotal Solution Services For Advanced Maintenance of Thermal Power-Generation PlantsRam MohanNo ratings yet

- Estimation of Operating CostsDocument20 pagesEstimation of Operating CostsGabriella PrathapsonNo ratings yet

- FLUKE - PDM OverviewDocument5 pagesFLUKE - PDM OverviewofedulloNo ratings yet

- Chapter 4 (Compatibility Mode)Document26 pagesChapter 4 (Compatibility Mode)AndualemEndrisNo ratings yet

- Costing and Project EvaluationDocument37 pagesCosting and Project Evaluationdani2611No ratings yet

- Lec 9Document39 pagesLec 9Mortada OthmanNo ratings yet

- Material Planning and Inventory ControlDocument7 pagesMaterial Planning and Inventory Controlsazzadasif.irlNo ratings yet

- Economics of Construction EquipmentDocument10 pagesEconomics of Construction Equipmentshubham chikuNo ratings yet

- Cost Estimation and EvaluationDocument4 pagesCost Estimation and EvaluationMuddassir DanishNo ratings yet

- Cost & Cost ConceptsDocument51 pagesCost & Cost ConceptsEzhil Vendhan PalanisamyNo ratings yet

- Equip. Note PDFDocument16 pagesEquip. Note PDFhailush girmay100% (1)

- OverheadsDocument25 pagesOverheadslalitNo ratings yet

- A Life Cycle Cost Calculation and Management System For Machine ToolsDocument6 pagesA Life Cycle Cost Calculation and Management System For Machine ToolsOscar TeknikerNo ratings yet

- Economic ReportDocument9 pagesEconomic ReportYeeXuan TenNo ratings yet

- ENGG ZC242 Regular Solution MidsemDocument4 pagesENGG ZC242 Regular Solution MidsemymsyaseenNo ratings yet

- Life Cycle Cost Analysis Manual: State of Illinois Capital Development BoardDocument23 pagesLife Cycle Cost Analysis Manual: State of Illinois Capital Development Boardrizwan khanNo ratings yet

- SMRP Metric 1.3 Maintenance Unit CostDocument5 pagesSMRP Metric 1.3 Maintenance Unit CostJorge FracaroNo ratings yet

- Brick WorkDocument33 pagesBrick WorkIbrahim AliNo ratings yet

- Reee 002Document15 pagesReee 002Imran Nawaz MehthalNo ratings yet

- Evaluating Capital Cost Estimates-Aug-11Document8 pagesEvaluating Capital Cost Estimates-Aug-11Ashfaq NoorNo ratings yet

- Maintenance Management-4, 2019Document12 pagesMaintenance Management-4, 2019Suman KumarNo ratings yet

- National Thermal Power Corporation Limited: November 2002Document50 pagesNational Thermal Power Corporation Limited: November 2002SamNo ratings yet

- Depreciation Depreciation: by S KrugonDocument15 pagesDepreciation Depreciation: by S KrugonBRAHMAIAH NAKKANo ratings yet

- Lecture 6fDocument30 pagesLecture 6fhiteshNo ratings yet

- CEV633 Engineering Economics & Project ManagementDocument59 pagesCEV633 Engineering Economics & Project ManagementgnaniNo ratings yet

- Maintenance ManagementDocument44 pagesMaintenance ManagementDwi Putri Hidayat100% (4)

- 1.3 Maintenance Unit Cost: Business & Management MetricDocument3 pages1.3 Maintenance Unit Cost: Business & Management MetricAlexander Arias RuizNo ratings yet

- Operations ManagementDocument32 pagesOperations ManagementAsif S KhanNo ratings yet

- Lecture Note On Construction Equipment ManagementDocument84 pagesLecture Note On Construction Equipment ManagementAberaMamoJaletaNo ratings yet

- Preliminary Operations and Maintenance Plan: Cassadaga Wind FarmDocument9 pagesPreliminary Operations and Maintenance Plan: Cassadaga Wind FarmDivyansh Singh ChauhanNo ratings yet

- Costs Analysis of Constructions Heavy Eq PDFDocument13 pagesCosts Analysis of Constructions Heavy Eq PDFJuan Carlos Cruz ENo ratings yet

- Costing Formulas PDFDocument86 pagesCosting Formulas PDFsubbu100% (3)

- Operating Cost and Estimate of Cost: Submitted To: - Submitted By:-Prof - Gunjan DivediDocument10 pagesOperating Cost and Estimate of Cost: Submitted To: - Submitted By:-Prof - Gunjan DivediRohit SinghNo ratings yet

- Unit 6 PDFDocument10 pagesUnit 6 PDFpayal sachdevNo ratings yet

- Disclosure To Promote The Right To InformationDocument13 pagesDisclosure To Promote The Right To InformationAnonymous 1gp9bFNo ratings yet

- Maintenance FunctionsDocument41 pagesMaintenance FunctionsAryyaka SarkarNo ratings yet

- 6.3 Applying Annual-Worth Analysis 6.3.1 Benefits of AE AnalysisDocument6 pages6.3 Applying Annual-Worth Analysis 6.3.1 Benefits of AE Analysisshintya nadaNo ratings yet

- Dire Dawa University Institute of Technology: Electrical Engineering Department Power System Planning and OperationDocument8 pagesDire Dawa University Institute of Technology: Electrical Engineering Department Power System Planning and OperationROBSANNo ratings yet

- Cost Analysis Using Break-Even Analysis: (Process Selection)Document28 pagesCost Analysis Using Break-Even Analysis: (Process Selection)zelalem wegayehuNo ratings yet

- Life Cycle CostingDocument61 pagesLife Cycle CostingMd Jalal Uddin Rumi100% (1)

- Case Study On The Profit Margin Model of Multi-Site Testing Technology For SemiconductorsDocument18 pagesCase Study On The Profit Margin Model of Multi-Site Testing Technology For SemiconductorsAJER JOURNALNo ratings yet

- Life Cycle Cost AnalysisDocument39 pagesLife Cycle Cost AnalysisJayaprakash SankaranNo ratings yet

- 12b.standard Costing XDocument18 pages12b.standard Costing XAbhinav AshishNo ratings yet

- Production and Maintenance Optimization Problems: Logistic Constraints and Leasing Warranty ServicesFrom EverandProduction and Maintenance Optimization Problems: Logistic Constraints and Leasing Warranty ServicesNo ratings yet

- Practical, Made Easy Guide To Building, Office And Home Automation Systems - Part OneFrom EverandPractical, Made Easy Guide To Building, Office And Home Automation Systems - Part OneNo ratings yet

- The Calibration of Flow Meters PDFDocument35 pagesThe Calibration of Flow Meters PDFRené Mora-CasalNo ratings yet

- Liquid Measurement Station Design 2017 ISHMDocument5 pagesLiquid Measurement Station Design 2017 ISHMMalouk CheniouniNo ratings yet

- Is 1448 (P 1) 2002 Determination of Acid Number of Petroleum Products by Potentiometric TitrationDocument17 pagesIs 1448 (P 1) 2002 Determination of Acid Number of Petroleum Products by Potentiometric TitrationMalouk CheniouniNo ratings yet

- Auditing Gas Measurement and Accounting Systems 2006 PDFDocument4 pagesAuditing Gas Measurement and Accounting Systems 2006 PDFMalouk CheniouniNo ratings yet

- Selection and Sizing of Control Valves For Natural Gas PDFDocument3 pagesSelection and Sizing of Control Valves For Natural Gas PDFMalouk CheniouniNo ratings yet

- Determination of Leakage and Unaccounted For Gas PDFDocument13 pagesDetermination of Leakage and Unaccounted For Gas PDFMalouk CheniouniNo ratings yet

- Calibration of An Ultrasonic Flow Meter For Hot Water PDFDocument8 pagesCalibration of An Ultrasonic Flow Meter For Hot Water PDFMalouk CheniouniNo ratings yet

- Elsevier - Ultrasonic Flow Metering Errors Due To Pulsating FlowDocument7 pagesElsevier - Ultrasonic Flow Metering Errors Due To Pulsating FlowMalouk CheniouniNo ratings yet

- AAP S8 SS Buttweld Fittings & Flanges E2 SDocument12 pagesAAP S8 SS Buttweld Fittings & Flanges E2 SMalouk CheniouniNo ratings yet

- T11 Coriolis PDFDocument19 pagesT11 Coriolis PDFMalouk Cheniouni100% (1)

- 83 Calibration Ultrasonic Flowmeters PDFDocument6 pages83 Calibration Ultrasonic Flowmeters PDFMalouk CheniouniNo ratings yet

- Model 500 (2350A) GC PDFDocument334 pagesModel 500 (2350A) GC PDFMalouk CheniouniNo ratings yet

- Ultrasonic Gas Flow Meter BasicsDocument7 pagesUltrasonic Gas Flow Meter BasicsMalouk CheniouniNo ratings yet

- Brochure - E-RTG ElectrificationDocument12 pagesBrochure - E-RTG Electrification003086No ratings yet

- MT6763 Android ScatterDocument13 pagesMT6763 Android ScatterLim Bun Lio0% (2)

- Microprocessor Book by B Ram CompressDocument2 pagesMicroprocessor Book by B Ram CompressSanika LandeNo ratings yet

- ListDocument2 pagesListAman GuptaNo ratings yet

- 193PST - TF1700 User ManualDocument75 pages193PST - TF1700 User ManualDNo ratings yet

- ITT565-Lab-week7-NURUL IZZATIDocument7 pagesITT565-Lab-week7-NURUL IZZATI2023379679No ratings yet

- Face Recognition TechnologyDocument9 pagesFace Recognition TechnologySireesha TekuruNo ratings yet

- Binance-Api DocumentationDocument4 pagesBinance-Api DocumentationIrmak ErkolNo ratings yet

- Qcvs PBL User GuideDocument30 pagesQcvs PBL User GuidejwinstonjacobNo ratings yet

- Practical SEDocument6 pagesPractical SEMohammadNo ratings yet

- FCU-6000 System ManualDocument68 pagesFCU-6000 System Manualadavit73No ratings yet

- RSE-1A1 Mlk2 Overview PDFDocument12 pagesRSE-1A1 Mlk2 Overview PDFAnonymous fE2l3DzlNo ratings yet

- Programacion HTML5 CC3 and JSDocument654 pagesProgramacion HTML5 CC3 and JSErick FloresNo ratings yet

- E17-7-Assessing The Kpi For The Supply ChainDocument4 pagesE17-7-Assessing The Kpi For The Supply ChainAmd BustosNo ratings yet

- Fianl Essay of OMDocument4 pagesFianl Essay of OMApurbo Sarkar ShohagNo ratings yet

- When Technology and Humanity Cross 1Document2 pagesWhen Technology and Humanity Cross 1Shainna Panopio100% (1)

- TML Civil Engineering Transducers: Strain Gauge-TypeDocument2 pagesTML Civil Engineering Transducers: Strain Gauge-TypeHemlata VermaNo ratings yet

- Xda-Developers - SECRET CODES - Omnia 2 GT-i8000 PDFDocument3 pagesXda-Developers - SECRET CODES - Omnia 2 GT-i8000 PDFM Arshad Iqbal HarralNo ratings yet

- 5 Steps To Operational Excellence PDFDocument9 pages5 Steps To Operational Excellence PDFdrustagiNo ratings yet

- Job Interview QuestionsDocument2 pagesJob Interview QuestionsashvajNo ratings yet

- CRM Initiatives by Lic of IndiaDocument5 pagesCRM Initiatives by Lic of Indiashivacrazze0% (1)

- CRDeDocument97 pagesCRDeluisxdNo ratings yet

- Estrategia de Desarrollo y Plan de RecursosDocument9 pagesEstrategia de Desarrollo y Plan de RecursosFrancisco Martinez Gallardo LascurainNo ratings yet

- Mindwave and Arduino: FeaturesDocument6 pagesMindwave and Arduino: FeaturesSiva KumarNo ratings yet

- Don't KnowDocument1 pageDon't KnowWindsor LewisNo ratings yet

- Objectives of Digital BankingDocument10 pagesObjectives of Digital BankingGourav jamwalNo ratings yet

- Nepal Telecom: Kathmandu Regional Directorate Service DivisionDocument2 pagesNepal Telecom: Kathmandu Regional Directorate Service Divisionabhisek guptaNo ratings yet

- Biznet Dedicated Internet - Connection Setting - Linksys RouterDocument4 pagesBiznet Dedicated Internet - Connection Setting - Linksys RouterHanafi AljazaNo ratings yet