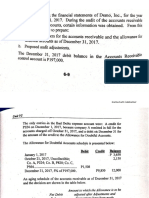

Cash and Receivables

Cash and Receivables

You might also like

- 85 Insurance Certificate 2015Document2 pages85 Insurance Certificate 2015SHARP HOA MANAGEMENT, INC100% (1)

- Problem 1Document6 pagesProblem 1novyNo ratings yet

- INSTRUCTIONS: Select The Correct Answer For Each of The Following Questions. Mark OnlyDocument15 pagesINSTRUCTIONS: Select The Correct Answer For Each of The Following Questions. Mark OnlyMendoza Ron NixonNo ratings yet

- Problems For Proof of Cash and Bank ReconDocument2 pagesProblems For Proof of Cash and Bank ReconTine Vasiana DuermeNo ratings yet

- Page Comprehensive Theories and ProblemsDocument7 pagesPage Comprehensive Theories and Problemsharley_quinn11No ratings yet

- Accounts Receivable 2Document10 pagesAccounts Receivable 2jade rotiaNo ratings yet

- Financial Planning and ForecastingDocument3 pagesFinancial Planning and ForecastingPrima FacieNo ratings yet

- DELL Annual Cash Flow Statement - Dell IncDocument3 pagesDELL Annual Cash Flow Statement - Dell IncmrkuroiNo ratings yet

- Audit of CashDocument14 pagesAudit of CashEll VNo ratings yet

- AP 59 1stPB - 5.06Document9 pagesAP 59 1stPB - 5.06Loren Lordwell MoyaniNo ratings yet

- Pak Enings HTDocument15 pagesPak Enings HTVincent SampianoNo ratings yet

- Chapter 2: Audit of Cash and Cash Equivalents: Internal Control Over CashDocument35 pagesChapter 2: Audit of Cash and Cash Equivalents: Internal Control Over CashEmey CalbayNo ratings yet

- Far Open PB Dec 2021Document16 pagesFar Open PB Dec 2021Mariane ValenzuelaNo ratings yet

- AFAR ProblemsDocument45 pagesAFAR ProblemsPrima FacieNo ratings yet

- 8506 - Installment SalesDocument4 pages8506 - Installment SalesAnonymous iNRMC4mgORNo ratings yet

- Auditing Problems Final Preboard Examination Batch 87 SET: Cpa Review School of The Philippines ManilaDocument12 pagesAuditing Problems Final Preboard Examination Batch 87 SET: Cpa Review School of The Philippines ManilaMarwin AceNo ratings yet

- With SOLNS AP Merged2 PDFDocument51 pagesWith SOLNS AP Merged2 PDFAlma Jean MonterozoNo ratings yet

- Discussion 2 Second SemDocument8 pagesDiscussion 2 Second SemEmey Calbay100% (1)

- Audit ReviewDocument6 pagesAudit ReviewArnel RemorinNo ratings yet

- G.M4 HW GWDocument3 pagesG.M4 HW GWClint Agustin M. RoblesNo ratings yet

- DrillDocument4 pagesDrillJEP WalwalNo ratings yet

- BLT 2009 Final Pre-Board September 19Document14 pagesBLT 2009 Final Pre-Board September 19Lester AguinaldoNo ratings yet

- Business Law SurecpaDocument35 pagesBusiness Law SurecpaChessaAlenelLigutom100% (1)

- Auditing Chapter 2Document7 pagesAuditing Chapter 2lopo100% (1)

- Apllied Auditing Q&ADocument10 pagesApllied Auditing Q&APeterJorgeVillarante100% (2)

- CLINCHERDocument1 pageCLINCHERJerauld BucolNo ratings yet

- Ad2 1Document13 pagesAd2 1MarjorieNo ratings yet

- Multiple Choice Problems 21 Lark Corp. Has Contract To Construct A P5,000,000 Cruise Ship at An Estimated Cost ofDocument12 pagesMultiple Choice Problems 21 Lark Corp. Has Contract To Construct A P5,000,000 Cruise Ship at An Estimated Cost ofRie Cabigon100% (1)

- The Professional CPA Review School: Financial Accounting & Reporting (Problems) May 2019 BatchDocument10 pagesThe Professional CPA Review School: Financial Accounting & Reporting (Problems) May 2019 BatchKriztleKateMontealtoGelogoNo ratings yet

- Cpa Review School of The Philippines ManilaDocument4 pagesCpa Review School of The Philippines Manilaxara mizpahNo ratings yet

- Advanced Financial Accounting and Reporting Accounting For PartnershipDocument6 pagesAdvanced Financial Accounting and Reporting Accounting For PartnershipMaria BeatriceNo ratings yet

- Comprehensive Examinations 2 (Part II)Document4 pagesComprehensive Examinations 2 (Part II)Yander Marl BautistaNo ratings yet

- Philippine MysteriesDocument41 pagesPhilippine MysteriesYes ChannelNo ratings yet

- LTCC - ExamDocument5 pagesLTCC - ExamLouise Anciano100% (1)

- D5Document12 pagesD5Mark Lord Morales BumagatNo ratings yet

- Vdocuments - MX - Advanced Financial Accounting 1Document11 pagesVdocuments - MX - Advanced Financial Accounting 1Sweet EmmeNo ratings yet

- PDF Afar Week1 Compiled Questions CompressDocument78 pagesPDF Afar Week1 Compiled Questions CompressIo AyaNo ratings yet

- Applied Auditing Review Course Pre-Board - FinalDocument13 pagesApplied Auditing Review Course Pre-Board - FinalROMAR A. PIGANo ratings yet

- CRC Auditing Oct 2022 (1st PB)Document18 pagesCRC Auditing Oct 2022 (1st PB)Rodmae VersonNo ratings yet

- Specialized FinalsDocument13 pagesSpecialized FinalsAmie Jane MirandaNo ratings yet

- AP 5906q ReceivablesDocument3 pagesAP 5906q ReceivablesJulia MirhanNo ratings yet

- College: of Business AdministrationDocument5 pagesCollege: of Business AdministrationAna Mae HernandezNo ratings yet

- ASCA301 Module 1 DiscussionDocument22 pagesASCA301 Module 1 DiscussionKaleu MellaNo ratings yet

- AT Quizzer 13 - Reporting Issues (2TAY1718) PDFDocument10 pagesAT Quizzer 13 - Reporting Issues (2TAY1718) PDFWihl Mathew Zalatar0% (1)

- Auditing Problems Test Banks - SHE Part 1Document5 pagesAuditing Problems Test Banks - SHE Part 1Alliah Mae ArbastoNo ratings yet

- Pre Week NewDocument30 pagesPre Week NewAnonymous wDganZNo ratings yet

- Audit Prob Q6 Proof of Cash 2021Document9 pagesAudit Prob Q6 Proof of Cash 2021Ivy BautistaNo ratings yet

- p2 5 PDF FreeDocument20 pagesp2 5 PDF FreeheyNo ratings yet

- Icare Mockboard - FARDocument25 pagesIcare Mockboard - FARDaniel TayobanaNo ratings yet

- Audprob Final Exam 1Document26 pagesAudprob Final Exam 1Joody CatacutanNo ratings yet

- Fin ExamDocument6 pagesFin ExamKissesNo ratings yet

- AP - TestbankDocument22 pagesAP - TestbankRamon Jonathan SapalaranNo ratings yet

- Activity #1Document5 pagesActivity #1Lyka Nicole DoradoNo ratings yet

- Book 6Document4 pagesBook 6Actg SolmanNo ratings yet

- Set DDocument6 pagesSet DJeremiah Navarro PilotonNo ratings yet

- AP.2904 - Cash and Cash EquivalentsDocument7 pagesAP.2904 - Cash and Cash EquivalentsRNo ratings yet

- Finals - Receivables 2 Exercises WithoutDocument4 pagesFinals - Receivables 2 Exercises WithoutA.B AmpuanNo ratings yet

- Investment AccountingDocument3 pagesInvestment AccountingMaxineNo ratings yet

- Chapter 10 Test BankDocument48 pagesChapter 10 Test BankDAN NGUYEN THE100% (1)

- Audit 2 - TheoriesDocument2 pagesAudit 2 - TheoriesJoy ConsigeneNo ratings yet

- Chapter 10 Test BankDocument48 pagesChapter 10 Test BankRujean Salar AltejarNo ratings yet

- Audit of Cash and Cash Equivalents: Problem No. 20Document6 pagesAudit of Cash and Cash Equivalents: Problem No. 20Robel MurilloNo ratings yet

- Audit of ReceivablesDocument2 pagesAudit of ReceivablesCarmelaNo ratings yet

- Learning CurveDocument13 pagesLearning CurvePrima FacieNo ratings yet

- Ratio Analysis Theory - Selim Mohammad SaiduzzamanDocument19 pagesRatio Analysis Theory - Selim Mohammad SaiduzzamanPrima FacieNo ratings yet

- Cebu Institute of Technology - University: Use The Following Information For The Next Two QuestionsDocument13 pagesCebu Institute of Technology - University: Use The Following Information For The Next Two QuestionsPrima Facie50% (2)

- AFAR ProblemsDocument45 pagesAFAR ProblemsPrima FacieNo ratings yet

- AudCA2 Act2 Current LiabDocument4 pagesAudCA2 Act2 Current LiabPrima FacieNo ratings yet

- Audit of ReceivablesDocument11 pagesAudit of ReceivablesPrima Facie100% (1)

- G.R. No. 222743 SummaryDocument4 pagesG.R. No. 222743 SummaryPrima FacieNo ratings yet

- Chapter 03 Audit of Receivables & SalesDocument27 pagesChapter 03 Audit of Receivables & SalesPrima FacieNo ratings yet

- Assurance Engagements and Related ServicesDocument28 pagesAssurance Engagements and Related ServicesPrima FacieNo ratings yet

- SolutionsToPracticeProblems Working Capital ManagementDocument2 pagesSolutionsToPracticeProblems Working Capital ManagementPrima Facie100% (1)

- The Code of Professional EthicsDocument33 pagesThe Code of Professional EthicsPrima FacieNo ratings yet

- Estate of Sima Wei (A.k.a. Rufino Guy Susim)Document49 pagesEstate of Sima Wei (A.k.a. Rufino Guy Susim)MarivicTalomaNo ratings yet

- Bancoro Amended Complaint 00133192Document27 pagesBancoro Amended Complaint 00133192vpjNo ratings yet

- 6 Minute English Bitcoin: Digital Crypto-CurrencyDocument5 pages6 Minute English Bitcoin: Digital Crypto-CurrencyLeonardo Baloís Gómez CuauroNo ratings yet

- Test Bank For The Economics of Money Banking and Financial Markets 6th Canadian Edition Mishkin DownloadDocument32 pagesTest Bank For The Economics of Money Banking and Financial Markets 6th Canadian Edition Mishkin Downloadariananavarrofkaeicyprn100% (20)

- Financial Accounting F3 25 August RetakeDocument12 pagesFinancial Accounting F3 25 August RetakeMohammed HamzaNo ratings yet

- Paper14 PDFDocument94 pagesPaper14 PDFShilpa Arora NarangNo ratings yet

- Action Construction EquipmentDocument8 pagesAction Construction EquipmentP.B VeeraraghavuluNo ratings yet

- MR Smith Recently Faced A Choice Between Being A AnDocument1 pageMR Smith Recently Faced A Choice Between Being A Antrilocksp SinghNo ratings yet

- ASS Accountingcycleofaservicebusiness FJPDocument59 pagesASS Accountingcycleofaservicebusiness FJPArlyn Ragudos BSA1No ratings yet

- West Bengal Service RuleDocument84 pagesWest Bengal Service RulesukujeNo ratings yet

- Determinants of Commercial Banks' Performance A Case of NepalDocument13 pagesDeterminants of Commercial Banks' Performance A Case of NepalAyush Nikhil75% (4)

- Sale of Goods Act, 1930Document84 pagesSale of Goods Act, 1930Sparsh Agrawal0% (1)

- Tax Planning With Reference To Managerial DecisionsDocument22 pagesTax Planning With Reference To Managerial DecisionsdharuvNo ratings yet

- Lobbying in 2011Document96 pagesLobbying in 2011Michael Gareth JohnsonNo ratings yet

- PERCENTAGE Paid Chapter Free PDFDocument35 pagesPERCENTAGE Paid Chapter Free PDFsudhanshu913579No ratings yet

- CFO - White Paper Global Cash ForecastingDocument29 pagesCFO - White Paper Global Cash Forecastingvic2clarionNo ratings yet

- Real Property TaxDocument158 pagesReal Property TaxJamesMorente100% (2)

- CFA二级思维导图Document2 pagesCFA二级思维导图tsuijulie1026No ratings yet

- Confirmation Letter - SannaDocument2 pagesConfirmation Letter - SannaSannauli Rusliani SihombingNo ratings yet

- Maricalum Mining Corp. vs. Florentino - JasperDocument2 pagesMaricalum Mining Corp. vs. Florentino - JasperJames LouNo ratings yet

- RBI Lender of Last ResortDocument18 pagesRBI Lender of Last ResortHemantVermaNo ratings yet

- Questionnaire For Early Stage Start UpDocument5 pagesQuestionnaire For Early Stage Start UpNeetika KatariaNo ratings yet

- AESL - Investor Presentation - January 24Document55 pagesAESL - Investor Presentation - January 24SHREYA NAIRNo ratings yet

- After A Death: What Steps Are Needed?Document12 pagesAfter A Death: What Steps Are Needed?Bill TaylorNo ratings yet

- Corporate Accounting: 3 Semester DBADocument54 pagesCorporate Accounting: 3 Semester DBAMaaz RaheelNo ratings yet

- Contemporary WorldDocument39 pagesContemporary WorldMARIA33% (3)

- ReportDocument14 pagesReportapi-274785089No ratings yet

- May 13, 2016 Strathmore TimesDocument31 pagesMay 13, 2016 Strathmore TimesStrathmore TimesNo ratings yet

Download as docx, pdf, or txt

You might also like

- 85 Insurance Certificate 2015Document2 pages85 Insurance Certificate 2015SHARP HOA MANAGEMENT, INC100% (1)

- Problem 1Document6 pagesProblem 1novyNo ratings yet

- INSTRUCTIONS: Select The Correct Answer For Each of The Following Questions. Mark OnlyDocument15 pagesINSTRUCTIONS: Select The Correct Answer For Each of The Following Questions. Mark OnlyMendoza Ron NixonNo ratings yet

- Problems For Proof of Cash and Bank ReconDocument2 pagesProblems For Proof of Cash and Bank ReconTine Vasiana DuermeNo ratings yet

- Page Comprehensive Theories and ProblemsDocument7 pagesPage Comprehensive Theories and Problemsharley_quinn11No ratings yet

- Accounts Receivable 2Document10 pagesAccounts Receivable 2jade rotiaNo ratings yet

- Financial Planning and ForecastingDocument3 pagesFinancial Planning and ForecastingPrima FacieNo ratings yet

- DELL Annual Cash Flow Statement - Dell IncDocument3 pagesDELL Annual Cash Flow Statement - Dell IncmrkuroiNo ratings yet

- Audit of CashDocument14 pagesAudit of CashEll VNo ratings yet

- AP 59 1stPB - 5.06Document9 pagesAP 59 1stPB - 5.06Loren Lordwell MoyaniNo ratings yet

- Pak Enings HTDocument15 pagesPak Enings HTVincent SampianoNo ratings yet

- Chapter 2: Audit of Cash and Cash Equivalents: Internal Control Over CashDocument35 pagesChapter 2: Audit of Cash and Cash Equivalents: Internal Control Over CashEmey CalbayNo ratings yet

- Far Open PB Dec 2021Document16 pagesFar Open PB Dec 2021Mariane ValenzuelaNo ratings yet

- AFAR ProblemsDocument45 pagesAFAR ProblemsPrima FacieNo ratings yet

- 8506 - Installment SalesDocument4 pages8506 - Installment SalesAnonymous iNRMC4mgORNo ratings yet

- Auditing Problems Final Preboard Examination Batch 87 SET: Cpa Review School of The Philippines ManilaDocument12 pagesAuditing Problems Final Preboard Examination Batch 87 SET: Cpa Review School of The Philippines ManilaMarwin AceNo ratings yet

- With SOLNS AP Merged2 PDFDocument51 pagesWith SOLNS AP Merged2 PDFAlma Jean MonterozoNo ratings yet

- Discussion 2 Second SemDocument8 pagesDiscussion 2 Second SemEmey Calbay100% (1)

- Audit ReviewDocument6 pagesAudit ReviewArnel RemorinNo ratings yet

- G.M4 HW GWDocument3 pagesG.M4 HW GWClint Agustin M. RoblesNo ratings yet

- DrillDocument4 pagesDrillJEP WalwalNo ratings yet

- BLT 2009 Final Pre-Board September 19Document14 pagesBLT 2009 Final Pre-Board September 19Lester AguinaldoNo ratings yet

- Business Law SurecpaDocument35 pagesBusiness Law SurecpaChessaAlenelLigutom100% (1)

- Auditing Chapter 2Document7 pagesAuditing Chapter 2lopo100% (1)

- Apllied Auditing Q&ADocument10 pagesApllied Auditing Q&APeterJorgeVillarante100% (2)

- CLINCHERDocument1 pageCLINCHERJerauld BucolNo ratings yet

- Ad2 1Document13 pagesAd2 1MarjorieNo ratings yet

- Multiple Choice Problems 21 Lark Corp. Has Contract To Construct A P5,000,000 Cruise Ship at An Estimated Cost ofDocument12 pagesMultiple Choice Problems 21 Lark Corp. Has Contract To Construct A P5,000,000 Cruise Ship at An Estimated Cost ofRie Cabigon100% (1)

- The Professional CPA Review School: Financial Accounting & Reporting (Problems) May 2019 BatchDocument10 pagesThe Professional CPA Review School: Financial Accounting & Reporting (Problems) May 2019 BatchKriztleKateMontealtoGelogoNo ratings yet

- Cpa Review School of The Philippines ManilaDocument4 pagesCpa Review School of The Philippines Manilaxara mizpahNo ratings yet

- Advanced Financial Accounting and Reporting Accounting For PartnershipDocument6 pagesAdvanced Financial Accounting and Reporting Accounting For PartnershipMaria BeatriceNo ratings yet

- Comprehensive Examinations 2 (Part II)Document4 pagesComprehensive Examinations 2 (Part II)Yander Marl BautistaNo ratings yet

- Philippine MysteriesDocument41 pagesPhilippine MysteriesYes ChannelNo ratings yet

- LTCC - ExamDocument5 pagesLTCC - ExamLouise Anciano100% (1)

- D5Document12 pagesD5Mark Lord Morales BumagatNo ratings yet

- Vdocuments - MX - Advanced Financial Accounting 1Document11 pagesVdocuments - MX - Advanced Financial Accounting 1Sweet EmmeNo ratings yet

- PDF Afar Week1 Compiled Questions CompressDocument78 pagesPDF Afar Week1 Compiled Questions CompressIo AyaNo ratings yet

- Applied Auditing Review Course Pre-Board - FinalDocument13 pagesApplied Auditing Review Course Pre-Board - FinalROMAR A. PIGANo ratings yet

- CRC Auditing Oct 2022 (1st PB)Document18 pagesCRC Auditing Oct 2022 (1st PB)Rodmae VersonNo ratings yet

- Specialized FinalsDocument13 pagesSpecialized FinalsAmie Jane MirandaNo ratings yet

- AP 5906q ReceivablesDocument3 pagesAP 5906q ReceivablesJulia MirhanNo ratings yet

- College: of Business AdministrationDocument5 pagesCollege: of Business AdministrationAna Mae HernandezNo ratings yet

- ASCA301 Module 1 DiscussionDocument22 pagesASCA301 Module 1 DiscussionKaleu MellaNo ratings yet

- AT Quizzer 13 - Reporting Issues (2TAY1718) PDFDocument10 pagesAT Quizzer 13 - Reporting Issues (2TAY1718) PDFWihl Mathew Zalatar0% (1)

- Auditing Problems Test Banks - SHE Part 1Document5 pagesAuditing Problems Test Banks - SHE Part 1Alliah Mae ArbastoNo ratings yet

- Pre Week NewDocument30 pagesPre Week NewAnonymous wDganZNo ratings yet

- Audit Prob Q6 Proof of Cash 2021Document9 pagesAudit Prob Q6 Proof of Cash 2021Ivy BautistaNo ratings yet

- p2 5 PDF FreeDocument20 pagesp2 5 PDF FreeheyNo ratings yet

- Icare Mockboard - FARDocument25 pagesIcare Mockboard - FARDaniel TayobanaNo ratings yet

- Audprob Final Exam 1Document26 pagesAudprob Final Exam 1Joody CatacutanNo ratings yet

- Fin ExamDocument6 pagesFin ExamKissesNo ratings yet

- AP - TestbankDocument22 pagesAP - TestbankRamon Jonathan SapalaranNo ratings yet

- Activity #1Document5 pagesActivity #1Lyka Nicole DoradoNo ratings yet

- Book 6Document4 pagesBook 6Actg SolmanNo ratings yet

- Set DDocument6 pagesSet DJeremiah Navarro PilotonNo ratings yet

- AP.2904 - Cash and Cash EquivalentsDocument7 pagesAP.2904 - Cash and Cash EquivalentsRNo ratings yet

- Finals - Receivables 2 Exercises WithoutDocument4 pagesFinals - Receivables 2 Exercises WithoutA.B AmpuanNo ratings yet

- Investment AccountingDocument3 pagesInvestment AccountingMaxineNo ratings yet

- Chapter 10 Test BankDocument48 pagesChapter 10 Test BankDAN NGUYEN THE100% (1)

- Audit 2 - TheoriesDocument2 pagesAudit 2 - TheoriesJoy ConsigeneNo ratings yet

- Chapter 10 Test BankDocument48 pagesChapter 10 Test BankRujean Salar AltejarNo ratings yet

- Audit of Cash and Cash Equivalents: Problem No. 20Document6 pagesAudit of Cash and Cash Equivalents: Problem No. 20Robel MurilloNo ratings yet

- Audit of ReceivablesDocument2 pagesAudit of ReceivablesCarmelaNo ratings yet

- Learning CurveDocument13 pagesLearning CurvePrima FacieNo ratings yet

- Ratio Analysis Theory - Selim Mohammad SaiduzzamanDocument19 pagesRatio Analysis Theory - Selim Mohammad SaiduzzamanPrima FacieNo ratings yet

- Cebu Institute of Technology - University: Use The Following Information For The Next Two QuestionsDocument13 pagesCebu Institute of Technology - University: Use The Following Information For The Next Two QuestionsPrima Facie50% (2)

- AFAR ProblemsDocument45 pagesAFAR ProblemsPrima FacieNo ratings yet

- AudCA2 Act2 Current LiabDocument4 pagesAudCA2 Act2 Current LiabPrima FacieNo ratings yet

- Audit of ReceivablesDocument11 pagesAudit of ReceivablesPrima Facie100% (1)

- G.R. No. 222743 SummaryDocument4 pagesG.R. No. 222743 SummaryPrima FacieNo ratings yet

- Chapter 03 Audit of Receivables & SalesDocument27 pagesChapter 03 Audit of Receivables & SalesPrima FacieNo ratings yet

- Assurance Engagements and Related ServicesDocument28 pagesAssurance Engagements and Related ServicesPrima FacieNo ratings yet

- SolutionsToPracticeProblems Working Capital ManagementDocument2 pagesSolutionsToPracticeProblems Working Capital ManagementPrima Facie100% (1)

- The Code of Professional EthicsDocument33 pagesThe Code of Professional EthicsPrima FacieNo ratings yet

- Estate of Sima Wei (A.k.a. Rufino Guy Susim)Document49 pagesEstate of Sima Wei (A.k.a. Rufino Guy Susim)MarivicTalomaNo ratings yet

- Bancoro Amended Complaint 00133192Document27 pagesBancoro Amended Complaint 00133192vpjNo ratings yet

- 6 Minute English Bitcoin: Digital Crypto-CurrencyDocument5 pages6 Minute English Bitcoin: Digital Crypto-CurrencyLeonardo Baloís Gómez CuauroNo ratings yet

- Test Bank For The Economics of Money Banking and Financial Markets 6th Canadian Edition Mishkin DownloadDocument32 pagesTest Bank For The Economics of Money Banking and Financial Markets 6th Canadian Edition Mishkin Downloadariananavarrofkaeicyprn100% (20)

- Financial Accounting F3 25 August RetakeDocument12 pagesFinancial Accounting F3 25 August RetakeMohammed HamzaNo ratings yet

- Paper14 PDFDocument94 pagesPaper14 PDFShilpa Arora NarangNo ratings yet

- Action Construction EquipmentDocument8 pagesAction Construction EquipmentP.B VeeraraghavuluNo ratings yet

- MR Smith Recently Faced A Choice Between Being A AnDocument1 pageMR Smith Recently Faced A Choice Between Being A Antrilocksp SinghNo ratings yet

- ASS Accountingcycleofaservicebusiness FJPDocument59 pagesASS Accountingcycleofaservicebusiness FJPArlyn Ragudos BSA1No ratings yet

- West Bengal Service RuleDocument84 pagesWest Bengal Service RulesukujeNo ratings yet

- Determinants of Commercial Banks' Performance A Case of NepalDocument13 pagesDeterminants of Commercial Banks' Performance A Case of NepalAyush Nikhil75% (4)

- Sale of Goods Act, 1930Document84 pagesSale of Goods Act, 1930Sparsh Agrawal0% (1)

- Tax Planning With Reference To Managerial DecisionsDocument22 pagesTax Planning With Reference To Managerial DecisionsdharuvNo ratings yet

- Lobbying in 2011Document96 pagesLobbying in 2011Michael Gareth JohnsonNo ratings yet

- PERCENTAGE Paid Chapter Free PDFDocument35 pagesPERCENTAGE Paid Chapter Free PDFsudhanshu913579No ratings yet

- CFO - White Paper Global Cash ForecastingDocument29 pagesCFO - White Paper Global Cash Forecastingvic2clarionNo ratings yet

- Real Property TaxDocument158 pagesReal Property TaxJamesMorente100% (2)

- CFA二级思维导图Document2 pagesCFA二级思维导图tsuijulie1026No ratings yet

- Confirmation Letter - SannaDocument2 pagesConfirmation Letter - SannaSannauli Rusliani SihombingNo ratings yet

- Maricalum Mining Corp. vs. Florentino - JasperDocument2 pagesMaricalum Mining Corp. vs. Florentino - JasperJames LouNo ratings yet

- RBI Lender of Last ResortDocument18 pagesRBI Lender of Last ResortHemantVermaNo ratings yet

- Questionnaire For Early Stage Start UpDocument5 pagesQuestionnaire For Early Stage Start UpNeetika KatariaNo ratings yet

- AESL - Investor Presentation - January 24Document55 pagesAESL - Investor Presentation - January 24SHREYA NAIRNo ratings yet

- After A Death: What Steps Are Needed?Document12 pagesAfter A Death: What Steps Are Needed?Bill TaylorNo ratings yet

- Corporate Accounting: 3 Semester DBADocument54 pagesCorporate Accounting: 3 Semester DBAMaaz RaheelNo ratings yet

- Contemporary WorldDocument39 pagesContemporary WorldMARIA33% (3)

- ReportDocument14 pagesReportapi-274785089No ratings yet

- May 13, 2016 Strathmore TimesDocument31 pagesMay 13, 2016 Strathmore TimesStrathmore TimesNo ratings yet