Ratio Analysis: ROA (Profit Margin Asset Turnover)

Ratio Analysis: ROA (Profit Margin Asset Turnover)

You might also like

- CMA FORMULA SHEET NEW SYLLABUS-Executive-RevisionDocument7 pagesCMA FORMULA SHEET NEW SYLLABUS-Executive-RevisionGANESH KUNJAPPA POOJARINo ratings yet

- Horace Vs Lasalle Bank National Ass. Et Al Circuit Court of Russell County Alabama 3-30-2011Document41 pagesHorace Vs Lasalle Bank National Ass. Et Al Circuit Court of Russell County Alabama 3-30-2011chunga85No ratings yet

- Islami Bank Bangladesh Limited: Bandarban BranchDocument8 pagesIslami Bank Bangladesh Limited: Bandarban Branchmu binNo ratings yet

- Formulas of Managerial Accounting Chapter 5Document2 pagesFormulas of Managerial Accounting Chapter 5Shahinul KabirNo ratings yet

- Accounting and Finance Formulas: A Simple IntroductionFrom EverandAccounting and Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- Cover PageDocument1 pageCover PageShahinul KabirNo ratings yet

- HR Practice of Nestlé BangladeshDocument16 pagesHR Practice of Nestlé BangladeshShahinul Kabir100% (1)

- SOURCES (Inflows of Cash) USES (Outflows of Cash) : TranslateDocument2 pagesSOURCES (Inflows of Cash) USES (Outflows of Cash) : TranslateRahul KapurNo ratings yet

- Financial Analysis (Chapter 3)Document18 pagesFinancial Analysis (Chapter 3)AsifMughalNo ratings yet

- Chapter 3 Financial Statment and AnalysisDocument7 pagesChapter 3 Financial Statment and AnalysisSusan ThapaNo ratings yet

- Financial Ratios FormulaDocument4 pagesFinancial Ratios FormulaKamlesh SinghNo ratings yet

- Financial Analysis (Chapter 3)Document18 pagesFinancial Analysis (Chapter 3)kazamNo ratings yet

- Ratios Notes and ProblemDocument6 pagesRatios Notes and ProblemAniket WaneNo ratings yet

- Financial Statement Analysis and Performance MeasurementDocument6 pagesFinancial Statement Analysis and Performance MeasurementBijaya DhakalNo ratings yet

- Financial Statement and Cash Flow AnalysisDocument6 pagesFinancial Statement and Cash Flow AnalysisSandra MoussaNo ratings yet

- Chapter 3Document61 pagesChapter 3Shrief MohiNo ratings yet

- Financial Analysis Cheat Sheet: by ViaDocument2 pagesFinancial Analysis Cheat Sheet: by Viaheehan6No ratings yet

- Ratio AnalysisDocument10 pagesRatio AnalysisUdayan KarnatakNo ratings yet

- Ratio Analysis DuPont AnalysisDocument7 pagesRatio Analysis DuPont Analysisshiv0308No ratings yet

- Financial AnalysisDocument2 pagesFinancial AnalysisdavewagNo ratings yet

- TIFA CheatSheet MM X MLDocument10 pagesTIFA CheatSheet MM X MLCorina Ioana BurceaNo ratings yet

- Topic 13 Financial Statement AnalysisDocument32 pagesTopic 13 Financial Statement AnalysisAbd AL Rahman Shah Bin Azlan ShahNo ratings yet

- Finance BBS3rd (Autosaved) 12Document29 pagesFinance BBS3rd (Autosaved) 12Ramesh GyawaliNo ratings yet

- Notes On Ratio AnalysisDocument12 pagesNotes On Ratio AnalysisVaishal90% (21)

- Chapter 2 - Financial Analysis (S202.)Document33 pagesChapter 2 - Financial Analysis (S202.)ha.nguyensanasNo ratings yet

- Analisa Ratio Keuangan LatihansoalDocument4 pagesAnalisa Ratio Keuangan Latihansoalxiao yung12No ratings yet

- Fa Cheat Sheet MM MLDocument8 pagesFa Cheat Sheet MM MLIrina StrizhkovaNo ratings yet

- Exam 1 Formula Sheet (1) - 2Document2 pagesExam 1 Formula Sheet (1) - 2haleeNo ratings yet

- Day 5 Ratios and Examples 2024Document18 pagesDay 5 Ratios and Examples 2024Kit KatNo ratings yet

- Financial Analysis RatiosDocument34 pagesFinancial Analysis Ratioskrishna priyaNo ratings yet

- Ratio FormulaeDocument3 pagesRatio FormulaeNandhaNo ratings yet

- Ratio AnalysisDocument13 pagesRatio Analysismuralib4u5No ratings yet

- Evaluating A Firm's Financial PerformanceDocument45 pagesEvaluating A Firm's Financial PerformancemarediarameezNo ratings yet

- Final Exam Ibrahim Helmy, Advanced FinanceDocument30 pagesFinal Exam Ibrahim Helmy, Advanced FinanceIbrahim HelmyNo ratings yet

- Ratio AnalysisDocument21 pagesRatio Analysissoumyasundar720No ratings yet

- Financial Ratio Analysis: Liquidity Ratio Debt Management Ratio Profitability Ratio Market Value RatioDocument16 pagesFinancial Ratio Analysis: Liquidity Ratio Debt Management Ratio Profitability Ratio Market Value RatioMatrika ThapaNo ratings yet

- RatiosDocument12 pagesRatiosOmer ArifNo ratings yet

- Financial Analysis1Document21 pagesFinancial Analysis1Umay PelitNo ratings yet

- Understanding Financial StatementsDocument53 pagesUnderstanding Financial StatementsRyanNo ratings yet

- Ratio Analysis in FinanceDocument19 pagesRatio Analysis in FinanceAhmed WaqasNo ratings yet

- Final Cheat Sheet FA ML X MM UpdatedDocument8 pagesFinal Cheat Sheet FA ML X MM UpdatedIrina StrizhkovaNo ratings yet

- ROE and ROA Ratios For Accounting SummaryDocument3 pagesROE and ROA Ratios For Accounting SummarymyzevelNo ratings yet

- Analysis 1Document59 pagesAnalysis 1Gautam M100% (1)

- Chapter 3Document8 pagesChapter 3NHƯ NGUYỄN LÂM TÂMNo ratings yet

- ACCCDocument6 pagesACCCAynalem KasaNo ratings yet

- Accounting KpisDocument6 pagesAccounting KpisHOCININo ratings yet

- Chapters 2 and 3 HandoutsDocument8 pagesChapters 2 and 3 HandoutsCarter LeeNo ratings yet

- Updated FSA Ratio SheetDocument4 pagesUpdated FSA Ratio Sheetmoussa toureNo ratings yet

- Analysis of Fianacial Statements-9Document25 pagesAnalysis of Fianacial Statements-9rohitsf22 olypm100% (1)

- 1) Activity RatiosDocument28 pages1) Activity RatiosNyanNo ratings yet

- Financial Statement Analysis (Ch.2)Document14 pagesFinancial Statement Analysis (Ch.2)TianyiNo ratings yet

- 1.1 Financial Analytics Toolkit (8 Pages) PDFDocument8 pages1.1 Financial Analytics Toolkit (8 Pages) PDFPartha Protim SahaNo ratings yet

- Cma Formula SheetDocument7 pagesCma Formula Sheetanushkamohanan0No ratings yet

- Acctg 14 NotesDocument22 pagesAcctg 14 NotesJeciel Mae M. CalubaNo ratings yet

- Ratios 1Document5 pagesRatios 1Ayush BankarNo ratings yet

- HO 4 Analisis Laporan KeuanganDocument44 pagesHO 4 Analisis Laporan KeuanganChintiaNo ratings yet

- Classification of RatiosDocument5 pagesClassification of Ratiostharani1771_32442248No ratings yet

- Ratios - Financial AnalysisDocument6 pagesRatios - Financial AnalysisMohamed EzzatNo ratings yet

- United International University: Assignment On Ratio Analysis & Dupont AnalysisDocument8 pagesUnited International University: Assignment On Ratio Analysis & Dupont AnalysisMostofa Reza PigeonNo ratings yet

- Fin Man ReviewerDocument1 pageFin Man ReviewerCharimaine GumaracNo ratings yet

- Major Accounting Terms: Asset - Any Item of Economic Value Owned by ADocument21 pagesMajor Accounting Terms: Asset - Any Item of Economic Value Owned by Aranisweta44No ratings yet

- BA 569 Financial RatiosDocument7 pagesBA 569 Financial RatiosMariaNo ratings yet

- Formula Sheet - Finance - VTDocument11 pagesFormula Sheet - Finance - VTmariaajudamariaNo ratings yet

- Lecture 06Document21 pagesLecture 06Syed NayemNo ratings yet

- Closing Price and Returns, TurjoDocument6 pagesClosing Price and Returns, TurjoShahinul KabirNo ratings yet

- Fin 302 Formulas Chapter 10 and 11Document3 pagesFin 302 Formulas Chapter 10 and 11Shahinul KabirNo ratings yet

- Chapter-05 CVP RelationshipDocument29 pagesChapter-05 CVP RelationshipShahinul Kabir100% (4)

- Chapter 10Document30 pagesChapter 10Shahinul KabirNo ratings yet

- Chapter 1 New - FIN201Document12 pagesChapter 1 New - FIN201Shahinul KabirNo ratings yet

- Chapter 03 - Ratio - NEWDocument20 pagesChapter 03 - Ratio - NEWShahinul KabirNo ratings yet

- INB 301 - Chapter 6 - International Trade TheoryDocument14 pagesINB 301 - Chapter 6 - International Trade TheoryShahinul KabirNo ratings yet

- Ratio Analysis: ROA (Profit Margin Asset Turnover)Document5 pagesRatio Analysis: ROA (Profit Margin Asset Turnover)Shahinul KabirNo ratings yet

- Course Outline-Autumn, FIN 201Document5 pagesCourse Outline-Autumn, FIN 201Shahinul KabirNo ratings yet

- Course Outline Autumn 2020 - INB301 - Section 1Document8 pagesCourse Outline Autumn 2020 - INB301 - Section 1Shahinul KabirNo ratings yet

- Revised Course Outline - MIS 442Document5 pagesRevised Course Outline - MIS 442Shahinul KabirNo ratings yet

- MIS442 PPT FinalDocument20 pagesMIS442 PPT FinalShahinul KabirNo ratings yet

- Independent University, BangladeshDocument47 pagesIndependent University, BangladeshShahinul KabirNo ratings yet

- Essay On Corporate Social Responsibility in Ecommerce CompaniesDocument13 pagesEssay On Corporate Social Responsibility in Ecommerce CompaniesShahinul KabirNo ratings yet

- The Implementation of Social Responsiveness Initiatives: Case of LithuaniaDocument8 pagesThe Implementation of Social Responsiveness Initiatives: Case of LithuaniaShahinul KabirNo ratings yet

- AC - BUTU MUHAMMAD MALLAM - FEBRUARY, 2021 - 671968358 - FullStmtDocument6 pagesAC - BUTU MUHAMMAD MALLAM - FEBRUARY, 2021 - 671968358 - FullStmtmuhammad m butuNo ratings yet

- FCMH#16Document4 pagesFCMH#16culxNo ratings yet

- Commercial Bank OperationsDocument15 pagesCommercial Bank Operationsbonifacio gianga jrNo ratings yet

- Caraa PlayersDocument2 pagesCaraa PlayersBenidick PascuaNo ratings yet

- Chapter 1 - MFRS 116Document60 pagesChapter 1 - MFRS 116Muhammad Hazlami0% (1)

- The Morgan StanleyDocument7 pagesThe Morgan Stanleysarav3387No ratings yet

- NDocument36 pagesNRohitMaharjanNo ratings yet

- Chapter 20 SolutionsDocument10 pagesChapter 20 SolutionsIbnu GamingNo ratings yet

- Tax Calculator by Tax GurujiDocument4 pagesTax Calculator by Tax GurujiSunitKumarChauhanNo ratings yet

- Daftar Akun Foto PragaDocument1 pageDaftar Akun Foto PragaM.Aditya FirdausNo ratings yet

- 07192022103337.906 82864976 EoiDocument2 pages07192022103337.906 82864976 Eoidhananjay prahladkaNo ratings yet

- 06 DepreciationDocument28 pages06 DepreciationMitch TechsNo ratings yet

- Goa Tribal Employment Generation Programmegtegp Scheme - EDC GOADocument1 pageGoa Tribal Employment Generation Programmegtegp Scheme - EDC GOAEDCGOANo ratings yet

- Annuity CalculatorDocument2 pagesAnnuity CalculatorBlueQuillNo ratings yet

- AdasdDocument4 pagesAdasdPrime JavateNo ratings yet

- MTP (TVM Questikon)Document11 pagesMTP (TVM Questikon)prashanttiwari155282No ratings yet

- Chapter 29-Monetary SystemDocument56 pagesChapter 29-Monetary SystemSharonNo ratings yet

- Wesleyan University - Philippines: Name: Year&Block: 4bsa1 Course: ActivityDocument12 pagesWesleyan University - Philippines: Name: Year&Block: 4bsa1 Course: ActivitySophia JunelleNo ratings yet

- ENG - Soal Mojakoe Pengantar Akuntansi UAS Genap 2021 - 2022Document9 pagesENG - Soal Mojakoe Pengantar Akuntansi UAS Genap 2021 - 202202Adibah Seila NafazaNo ratings yet

- Aski Presentation 2Document23 pagesAski Presentation 2Reinmaxine VelasquezNo ratings yet

- BFS L1 Imp QuestionsDocument20 pagesBFS L1 Imp QuestionsVishnu Roy0% (1)

- Answer Question 6.6Document3 pagesAnswer Question 6.6Lee Li HengNo ratings yet

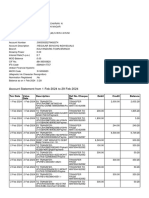

- Account Statement From 1 Feb 2024 To 29 Feb 2024: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument9 pagesAccount Statement From 1 Feb 2024 To 29 Feb 2024: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancepruthvicharan.iasramNo ratings yet

- Ice Task 2 Delta LTD QuestionDocument5 pagesIce Task 2 Delta LTD QuestionarronyeagarNo ratings yet

- Principles of Managerial Finance 13th Edition Gitman Test BankDocument25 pagesPrinciples of Managerial Finance 13th Edition Gitman Test BankSheilaEllisgxsnNo ratings yet

- Eva MvaDocument7 pagesEva MvaPrakhar GuptaNo ratings yet

- Negotiated Dealing System (NDS) :: Submitted by Roll NODocument12 pagesNegotiated Dealing System (NDS) :: Submitted by Roll NOKartik VariyaNo ratings yet

- Ejaz Naseer NBP Reprort 2018Document58 pagesEjaz Naseer NBP Reprort 2018Tayyab ali gardaziNo ratings yet

Download as docx, pdf, or txt

You might also like

- CMA FORMULA SHEET NEW SYLLABUS-Executive-RevisionDocument7 pagesCMA FORMULA SHEET NEW SYLLABUS-Executive-RevisionGANESH KUNJAPPA POOJARINo ratings yet

- Horace Vs Lasalle Bank National Ass. Et Al Circuit Court of Russell County Alabama 3-30-2011Document41 pagesHorace Vs Lasalle Bank National Ass. Et Al Circuit Court of Russell County Alabama 3-30-2011chunga85No ratings yet

- Islami Bank Bangladesh Limited: Bandarban BranchDocument8 pagesIslami Bank Bangladesh Limited: Bandarban Branchmu binNo ratings yet

- Formulas of Managerial Accounting Chapter 5Document2 pagesFormulas of Managerial Accounting Chapter 5Shahinul KabirNo ratings yet

- Accounting and Finance Formulas: A Simple IntroductionFrom EverandAccounting and Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- Cover PageDocument1 pageCover PageShahinul KabirNo ratings yet

- HR Practice of Nestlé BangladeshDocument16 pagesHR Practice of Nestlé BangladeshShahinul Kabir100% (1)

- SOURCES (Inflows of Cash) USES (Outflows of Cash) : TranslateDocument2 pagesSOURCES (Inflows of Cash) USES (Outflows of Cash) : TranslateRahul KapurNo ratings yet

- Financial Analysis (Chapter 3)Document18 pagesFinancial Analysis (Chapter 3)AsifMughalNo ratings yet

- Chapter 3 Financial Statment and AnalysisDocument7 pagesChapter 3 Financial Statment and AnalysisSusan ThapaNo ratings yet

- Financial Ratios FormulaDocument4 pagesFinancial Ratios FormulaKamlesh SinghNo ratings yet

- Financial Analysis (Chapter 3)Document18 pagesFinancial Analysis (Chapter 3)kazamNo ratings yet

- Ratios Notes and ProblemDocument6 pagesRatios Notes and ProblemAniket WaneNo ratings yet

- Financial Statement Analysis and Performance MeasurementDocument6 pagesFinancial Statement Analysis and Performance MeasurementBijaya DhakalNo ratings yet

- Financial Statement and Cash Flow AnalysisDocument6 pagesFinancial Statement and Cash Flow AnalysisSandra MoussaNo ratings yet

- Chapter 3Document61 pagesChapter 3Shrief MohiNo ratings yet

- Financial Analysis Cheat Sheet: by ViaDocument2 pagesFinancial Analysis Cheat Sheet: by Viaheehan6No ratings yet

- Ratio AnalysisDocument10 pagesRatio AnalysisUdayan KarnatakNo ratings yet

- Ratio Analysis DuPont AnalysisDocument7 pagesRatio Analysis DuPont Analysisshiv0308No ratings yet

- Financial AnalysisDocument2 pagesFinancial AnalysisdavewagNo ratings yet

- TIFA CheatSheet MM X MLDocument10 pagesTIFA CheatSheet MM X MLCorina Ioana BurceaNo ratings yet

- Topic 13 Financial Statement AnalysisDocument32 pagesTopic 13 Financial Statement AnalysisAbd AL Rahman Shah Bin Azlan ShahNo ratings yet

- Finance BBS3rd (Autosaved) 12Document29 pagesFinance BBS3rd (Autosaved) 12Ramesh GyawaliNo ratings yet

- Notes On Ratio AnalysisDocument12 pagesNotes On Ratio AnalysisVaishal90% (21)

- Chapter 2 - Financial Analysis (S202.)Document33 pagesChapter 2 - Financial Analysis (S202.)ha.nguyensanasNo ratings yet

- Analisa Ratio Keuangan LatihansoalDocument4 pagesAnalisa Ratio Keuangan Latihansoalxiao yung12No ratings yet

- Fa Cheat Sheet MM MLDocument8 pagesFa Cheat Sheet MM MLIrina StrizhkovaNo ratings yet

- Exam 1 Formula Sheet (1) - 2Document2 pagesExam 1 Formula Sheet (1) - 2haleeNo ratings yet

- Day 5 Ratios and Examples 2024Document18 pagesDay 5 Ratios and Examples 2024Kit KatNo ratings yet

- Financial Analysis RatiosDocument34 pagesFinancial Analysis Ratioskrishna priyaNo ratings yet

- Ratio FormulaeDocument3 pagesRatio FormulaeNandhaNo ratings yet

- Ratio AnalysisDocument13 pagesRatio Analysismuralib4u5No ratings yet

- Evaluating A Firm's Financial PerformanceDocument45 pagesEvaluating A Firm's Financial PerformancemarediarameezNo ratings yet

- Final Exam Ibrahim Helmy, Advanced FinanceDocument30 pagesFinal Exam Ibrahim Helmy, Advanced FinanceIbrahim HelmyNo ratings yet

- Ratio AnalysisDocument21 pagesRatio Analysissoumyasundar720No ratings yet

- Financial Ratio Analysis: Liquidity Ratio Debt Management Ratio Profitability Ratio Market Value RatioDocument16 pagesFinancial Ratio Analysis: Liquidity Ratio Debt Management Ratio Profitability Ratio Market Value RatioMatrika ThapaNo ratings yet

- RatiosDocument12 pagesRatiosOmer ArifNo ratings yet

- Financial Analysis1Document21 pagesFinancial Analysis1Umay PelitNo ratings yet

- Understanding Financial StatementsDocument53 pagesUnderstanding Financial StatementsRyanNo ratings yet

- Ratio Analysis in FinanceDocument19 pagesRatio Analysis in FinanceAhmed WaqasNo ratings yet

- Final Cheat Sheet FA ML X MM UpdatedDocument8 pagesFinal Cheat Sheet FA ML X MM UpdatedIrina StrizhkovaNo ratings yet

- ROE and ROA Ratios For Accounting SummaryDocument3 pagesROE and ROA Ratios For Accounting SummarymyzevelNo ratings yet

- Analysis 1Document59 pagesAnalysis 1Gautam M100% (1)

- Chapter 3Document8 pagesChapter 3NHƯ NGUYỄN LÂM TÂMNo ratings yet

- ACCCDocument6 pagesACCCAynalem KasaNo ratings yet

- Accounting KpisDocument6 pagesAccounting KpisHOCININo ratings yet

- Chapters 2 and 3 HandoutsDocument8 pagesChapters 2 and 3 HandoutsCarter LeeNo ratings yet

- Updated FSA Ratio SheetDocument4 pagesUpdated FSA Ratio Sheetmoussa toureNo ratings yet

- Analysis of Fianacial Statements-9Document25 pagesAnalysis of Fianacial Statements-9rohitsf22 olypm100% (1)

- 1) Activity RatiosDocument28 pages1) Activity RatiosNyanNo ratings yet

- Financial Statement Analysis (Ch.2)Document14 pagesFinancial Statement Analysis (Ch.2)TianyiNo ratings yet

- 1.1 Financial Analytics Toolkit (8 Pages) PDFDocument8 pages1.1 Financial Analytics Toolkit (8 Pages) PDFPartha Protim SahaNo ratings yet

- Cma Formula SheetDocument7 pagesCma Formula Sheetanushkamohanan0No ratings yet

- Acctg 14 NotesDocument22 pagesAcctg 14 NotesJeciel Mae M. CalubaNo ratings yet

- Ratios 1Document5 pagesRatios 1Ayush BankarNo ratings yet

- HO 4 Analisis Laporan KeuanganDocument44 pagesHO 4 Analisis Laporan KeuanganChintiaNo ratings yet

- Classification of RatiosDocument5 pagesClassification of Ratiostharani1771_32442248No ratings yet

- Ratios - Financial AnalysisDocument6 pagesRatios - Financial AnalysisMohamed EzzatNo ratings yet

- United International University: Assignment On Ratio Analysis & Dupont AnalysisDocument8 pagesUnited International University: Assignment On Ratio Analysis & Dupont AnalysisMostofa Reza PigeonNo ratings yet

- Fin Man ReviewerDocument1 pageFin Man ReviewerCharimaine GumaracNo ratings yet

- Major Accounting Terms: Asset - Any Item of Economic Value Owned by ADocument21 pagesMajor Accounting Terms: Asset - Any Item of Economic Value Owned by Aranisweta44No ratings yet

- BA 569 Financial RatiosDocument7 pagesBA 569 Financial RatiosMariaNo ratings yet

- Formula Sheet - Finance - VTDocument11 pagesFormula Sheet - Finance - VTmariaajudamariaNo ratings yet

- Lecture 06Document21 pagesLecture 06Syed NayemNo ratings yet

- Closing Price and Returns, TurjoDocument6 pagesClosing Price and Returns, TurjoShahinul KabirNo ratings yet

- Fin 302 Formulas Chapter 10 and 11Document3 pagesFin 302 Formulas Chapter 10 and 11Shahinul KabirNo ratings yet

- Chapter-05 CVP RelationshipDocument29 pagesChapter-05 CVP RelationshipShahinul Kabir100% (4)

- Chapter 10Document30 pagesChapter 10Shahinul KabirNo ratings yet

- Chapter 1 New - FIN201Document12 pagesChapter 1 New - FIN201Shahinul KabirNo ratings yet

- Chapter 03 - Ratio - NEWDocument20 pagesChapter 03 - Ratio - NEWShahinul KabirNo ratings yet

- INB 301 - Chapter 6 - International Trade TheoryDocument14 pagesINB 301 - Chapter 6 - International Trade TheoryShahinul KabirNo ratings yet

- Ratio Analysis: ROA (Profit Margin Asset Turnover)Document5 pagesRatio Analysis: ROA (Profit Margin Asset Turnover)Shahinul KabirNo ratings yet

- Course Outline-Autumn, FIN 201Document5 pagesCourse Outline-Autumn, FIN 201Shahinul KabirNo ratings yet

- Course Outline Autumn 2020 - INB301 - Section 1Document8 pagesCourse Outline Autumn 2020 - INB301 - Section 1Shahinul KabirNo ratings yet

- Revised Course Outline - MIS 442Document5 pagesRevised Course Outline - MIS 442Shahinul KabirNo ratings yet

- MIS442 PPT FinalDocument20 pagesMIS442 PPT FinalShahinul KabirNo ratings yet

- Independent University, BangladeshDocument47 pagesIndependent University, BangladeshShahinul KabirNo ratings yet

- Essay On Corporate Social Responsibility in Ecommerce CompaniesDocument13 pagesEssay On Corporate Social Responsibility in Ecommerce CompaniesShahinul KabirNo ratings yet

- The Implementation of Social Responsiveness Initiatives: Case of LithuaniaDocument8 pagesThe Implementation of Social Responsiveness Initiatives: Case of LithuaniaShahinul KabirNo ratings yet

- AC - BUTU MUHAMMAD MALLAM - FEBRUARY, 2021 - 671968358 - FullStmtDocument6 pagesAC - BUTU MUHAMMAD MALLAM - FEBRUARY, 2021 - 671968358 - FullStmtmuhammad m butuNo ratings yet

- FCMH#16Document4 pagesFCMH#16culxNo ratings yet

- Commercial Bank OperationsDocument15 pagesCommercial Bank Operationsbonifacio gianga jrNo ratings yet

- Caraa PlayersDocument2 pagesCaraa PlayersBenidick PascuaNo ratings yet

- Chapter 1 - MFRS 116Document60 pagesChapter 1 - MFRS 116Muhammad Hazlami0% (1)

- The Morgan StanleyDocument7 pagesThe Morgan Stanleysarav3387No ratings yet

- NDocument36 pagesNRohitMaharjanNo ratings yet

- Chapter 20 SolutionsDocument10 pagesChapter 20 SolutionsIbnu GamingNo ratings yet

- Tax Calculator by Tax GurujiDocument4 pagesTax Calculator by Tax GurujiSunitKumarChauhanNo ratings yet

- Daftar Akun Foto PragaDocument1 pageDaftar Akun Foto PragaM.Aditya FirdausNo ratings yet

- 07192022103337.906 82864976 EoiDocument2 pages07192022103337.906 82864976 Eoidhananjay prahladkaNo ratings yet

- 06 DepreciationDocument28 pages06 DepreciationMitch TechsNo ratings yet

- Goa Tribal Employment Generation Programmegtegp Scheme - EDC GOADocument1 pageGoa Tribal Employment Generation Programmegtegp Scheme - EDC GOAEDCGOANo ratings yet

- Annuity CalculatorDocument2 pagesAnnuity CalculatorBlueQuillNo ratings yet

- AdasdDocument4 pagesAdasdPrime JavateNo ratings yet

- MTP (TVM Questikon)Document11 pagesMTP (TVM Questikon)prashanttiwari155282No ratings yet

- Chapter 29-Monetary SystemDocument56 pagesChapter 29-Monetary SystemSharonNo ratings yet

- Wesleyan University - Philippines: Name: Year&Block: 4bsa1 Course: ActivityDocument12 pagesWesleyan University - Philippines: Name: Year&Block: 4bsa1 Course: ActivitySophia JunelleNo ratings yet

- ENG - Soal Mojakoe Pengantar Akuntansi UAS Genap 2021 - 2022Document9 pagesENG - Soal Mojakoe Pengantar Akuntansi UAS Genap 2021 - 202202Adibah Seila NafazaNo ratings yet

- Aski Presentation 2Document23 pagesAski Presentation 2Reinmaxine VelasquezNo ratings yet

- BFS L1 Imp QuestionsDocument20 pagesBFS L1 Imp QuestionsVishnu Roy0% (1)

- Answer Question 6.6Document3 pagesAnswer Question 6.6Lee Li HengNo ratings yet

- Account Statement From 1 Feb 2024 To 29 Feb 2024: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument9 pagesAccount Statement From 1 Feb 2024 To 29 Feb 2024: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancepruthvicharan.iasramNo ratings yet

- Ice Task 2 Delta LTD QuestionDocument5 pagesIce Task 2 Delta LTD QuestionarronyeagarNo ratings yet

- Principles of Managerial Finance 13th Edition Gitman Test BankDocument25 pagesPrinciples of Managerial Finance 13th Edition Gitman Test BankSheilaEllisgxsnNo ratings yet

- Eva MvaDocument7 pagesEva MvaPrakhar GuptaNo ratings yet

- Negotiated Dealing System (NDS) :: Submitted by Roll NODocument12 pagesNegotiated Dealing System (NDS) :: Submitted by Roll NOKartik VariyaNo ratings yet

- Ejaz Naseer NBP Reprort 2018Document58 pagesEjaz Naseer NBP Reprort 2018Tayyab ali gardaziNo ratings yet