Download as pdf or txt

You might also like

- Manual Instructions For Sap Note 3167391 Edocument Mexico - Annex 20 V4.0: Full SolutionDocument4 pagesManual Instructions For Sap Note 3167391 Edocument Mexico - Annex 20 V4.0: Full SolutionDarioNo ratings yet

- Globalization and Its Impact of Insurance Industry in IndiaDocument10 pagesGlobalization and Its Impact of Insurance Industry in IndiaRiaz Ahmed100% (1)

- MBA Project On General InsuranceDocument71 pagesMBA Project On General InsuranceJoshi Ambeah75% (16)

- Joint Initiative Of: Icai Accounting & Auditing AdvisoryDocument48 pagesJoint Initiative Of: Icai Accounting & Auditing AdvisoryBhanu prasanna kumarNo ratings yet

- The Impact of Covid-19 On The Automotive Industry in IndiaDocument8 pagesThe Impact of Covid-19 On The Automotive Industry in IndiaIAEME PublicationNo ratings yet

- IJAAS Covid 19PandemicandFinancialReportingJoshiprintDocument10 pagesIJAAS Covid 19PandemicandFinancialReportingJoshiprintTaymaa OmoushNo ratings yet

- In Press, Accepted Manuscript - Note To UsersDocument9 pagesIn Press, Accepted Manuscript - Note To UsersSabbir AhmmedNo ratings yet

- Auditors Responsibility in Assessing Going ConcerDocument17 pagesAuditors Responsibility in Assessing Going ConcerNasrullah DjamilNo ratings yet

- Plagiarism Scan Report: Exclude Url: NoneDocument2 pagesPlagiarism Scan Report: Exclude Url: NoneSaurabh SinghNo ratings yet

- Retail Market Conduct Task Force Report Initial Findings and Observations About The Impact of COVID-19 On Retail Market ConductDocument30 pagesRetail Market Conduct Task Force Report Initial Findings and Observations About The Impact of COVID-19 On Retail Market ConductTarbNo ratings yet

- Bajaj AllianzDocument99 pagesBajaj AllianzYASH PRAJAPATINo ratings yet

- HDFC Ergo Annual Report Fy 2020 21Document136 pagesHDFC Ergo Annual Report Fy 2020 21krishnashastriNo ratings yet

- Bajaj Allianz Life: Company Based ResearchDocument18 pagesBajaj Allianz Life: Company Based ResearchInika jainNo ratings yet

- Ey Impact of The Pandemic On Indian Corporate ResultsDocument37 pagesEy Impact of The Pandemic On Indian Corporate ResultsAbhinav NaiduNo ratings yet

- COVID-19 and Indian Economy: Impact On Growth, Manufacturing, Trade and MSME SectorDocument25 pagesCOVID-19 and Indian Economy: Impact On Growth, Manufacturing, Trade and MSME SectorVipul ManglaNo ratings yet

- Financial Review and Financial Distress On Covid 19 Pandemic A Comparison of Two South East Asia Countries in The Real Estate and Property Sub SectorsDocument8 pagesFinancial Review and Financial Distress On Covid 19 Pandemic A Comparison of Two South East Asia Countries in The Real Estate and Property Sub SectorsInternational Journal of Innovative Science and Research Technology100% (1)

- Report On Public Issues by General Insurance Companies: SEBI Committee On Disclosures and Accounting Standards (SCODA)Document37 pagesReport On Public Issues by General Insurance Companies: SEBI Committee On Disclosures and Accounting Standards (SCODA)Chandra KumarNo ratings yet

- Covid-19 Impact On Indian Economy-1Document9 pagesCovid-19 Impact On Indian Economy-1samama lodhiNo ratings yet

- Covid 19 Impact On Indian EconomyDocument15 pagesCovid 19 Impact On Indian EconomyPratik WankhedeNo ratings yet

- Synopsis: Impact of COVID-19 On Indian Industry: Challenges and OpportunitiesDocument7 pagesSynopsis: Impact of COVID-19 On Indian Industry: Challenges and OpportunitiesSarita MoreNo ratings yet

- Impact of COVID-19 On IBCDocument13 pagesImpact of COVID-19 On IBCdevendra bankarNo ratings yet

- Chapter - 1 (Industry Analysis) : M S Ramaiah Institute of Management, BangaloreDocument72 pagesChapter - 1 (Industry Analysis) : M S Ramaiah Institute of Management, BangaloreAnubhav SoodNo ratings yet

- Bhumika 18132006Document4 pagesBhumika 18132006Jay MarwahaNo ratings yet

- PWC Insights Examples Reporting Impact of Covid 19 On Going Concern and Subsequent EventsDocument10 pagesPWC Insights Examples Reporting Impact of Covid 19 On Going Concern and Subsequent EventsSuman UroojNo ratings yet

- Impact of Covid 19 On Banking and Insurance SectorDocument6 pagesImpact of Covid 19 On Banking and Insurance SectorPrasanna KumarNo ratings yet

- Conduct of Business Regulation and Covid-19: A Review of The Gulf Insurance IndustryDocument14 pagesConduct of Business Regulation and Covid-19: A Review of The Gulf Insurance IndustryRAVI SONKARNo ratings yet

- Iais Global Insurance Market Report 2020Document15 pagesIais Global Insurance Market Report 2020JorkosNo ratings yet

- Globalization and Its Impact of Insurance Industry in India: Riaz AhemadDocument10 pagesGlobalization and Its Impact of Insurance Industry in India: Riaz AhemadAlok NayakNo ratings yet

- KSHITIJA SIP FinalDocument57 pagesKSHITIJA SIP Finalkshitija upadhyayNo ratings yet

- Challenges To MSME During Covid 19Document6 pagesChallenges To MSME During Covid 19robertphilNo ratings yet

- A. Survive, Revive and Growth Strategies Adopted by EmamiDocument9 pagesA. Survive, Revive and Growth Strategies Adopted by EmamiShivani DuttNo ratings yet

- Group Annual Report 2020Document260 pagesGroup Annual Report 2020Prysmian GroupNo ratings yet

- Role of Private Sector in Insurance BusinessDocument52 pagesRole of Private Sector in Insurance BusinessTrilok AshpalNo ratings yet

- IBC After COVIDDocument6 pagesIBC After COVIDRitwik PrakashNo ratings yet

- HR Project in HDFCDocument69 pagesHR Project in HDFCJdahiya90No ratings yet

- Accounting HammadDocument7 pagesAccounting Hammadshan khanNo ratings yet

- Behavioral nanceandCOVID-19 Cognitive Errors That Determine The Nancial FutureDocument6 pagesBehavioral nanceandCOVID-19 Cognitive Errors That Determine The Nancial FutureWahyuni MertasariNo ratings yet

- Assignment Financial Impact On EntitiesDocument5 pagesAssignment Financial Impact On EntitiesannyswardahNo ratings yet

- Impact of Covid-19 On MSME Sector in India A LiterDocument7 pagesImpact of Covid-19 On MSME Sector in India A LiterHashmita MistriNo ratings yet

- The Impact of COVID-19 Pandemic On The Financial Performance of Firms On The Indonesia Stock ExchangeDocument18 pagesThe Impact of COVID-19 Pandemic On The Financial Performance of Firms On The Indonesia Stock Exchange409005091No ratings yet

- The COVID-19 pandemic will have a significant impact on Financial Reporting for companies around the world. Discuss the validity of this statement with reference to specific areas of the financial statementsDocument6 pagesThe COVID-19 pandemic will have a significant impact on Financial Reporting for companies around the world. Discuss the validity of this statement with reference to specific areas of the financial statementsMaria GeorgiouNo ratings yet

- Case Study Asc302Document17 pagesCase Study Asc302Izzah Batrisyia Khairul HadiNo ratings yet

- Project On General Insurance in IndiaDocument26 pagesProject On General Insurance in IndiarajNo ratings yet

- Final Draft Report - 14 SeptDocument50 pagesFinal Draft Report - 14 Septneelove1No ratings yet

- Value Conservation To Value Creation: COVID-19: Path To RecoveryDocument25 pagesValue Conservation To Value Creation: COVID-19: Path To RecoveryPrem RavalNo ratings yet

- Insurance Sector in INDIADocument61 pagesInsurance Sector in INDIAAnkita JoshiNo ratings yet

- Preprint Not Peer Reviewed: Economic Re-Engineering: Covid-19Document5 pagesPreprint Not Peer Reviewed: Economic Re-Engineering: Covid-19Lavu NqabaNo ratings yet

- CoronavirusPandemicandBusinessDisruption IJAMR200514Document9 pagesCoronavirusPandemicandBusinessDisruption IJAMR200514Rizki NurhidayahNo ratings yet

- Privatization of InsuranceDocument60 pagesPrivatization of InsurancePrashant NathaniNo ratings yet

- Indian Insurance Sector: An Analytical Report by Group 3Document45 pagesIndian Insurance Sector: An Analytical Report by Group 3Kpvs ThusharNo ratings yet

- HDFC Recruitment of Financial Consultant of HDFC Standard Charterd Life InsuranceDocument98 pagesHDFC Recruitment of Financial Consultant of HDFC Standard Charterd Life InsuranceRajni MadanNo ratings yet

- Understanding of Risk Management Processes Applicable To Indian Life Insurance SectorDocument14 pagesUnderstanding of Risk Management Processes Applicable To Indian Life Insurance SectorSiva SankariNo ratings yet

- Minor Project PresentationDocument35 pagesMinor Project PresentationNikitha GeorgeNo ratings yet

- 2020 Third Quarter Results PresentationDocument36 pages2020 Third Quarter Results PresentationVincent ChanNo ratings yet

- Acquisory News Chronicle September 2020Document8 pagesAcquisory News Chronicle September 2020Acquisory Consulting LLPNo ratings yet

- 1607546412443 - final project منهجيةDocument4 pages1607546412443 - final project منهجيةSabreen IssaNo ratings yet

- Quickheal AnnualreportDocument229 pagesQuickheal AnnualreportPiyush HarlalkaNo ratings yet

- Malhotra CommitteeDocument5 pagesMalhotra CommitteeBibhash RoyNo ratings yet

- Indian Insurance Scenario A Critical Review On Life Insurance IndustryDocument8 pagesIndian Insurance Scenario A Critical Review On Life Insurance Industrykesharwanigopal123No ratings yet

- COVID-19 and Public–Private Partnerships in Asia and the Pacific: Guidance NoteFrom EverandCOVID-19 and Public–Private Partnerships in Asia and the Pacific: Guidance NoteNo ratings yet

- Management Accountant Jan-2016Document124 pagesManagement Accountant Jan-2016ABC 123No ratings yet

- Management Accountant March-2016Document124 pagesManagement Accountant March-2016ABC 123No ratings yet

- Guidance Note On Internal Audit of General Insurance CompaniesDocument128 pagesGuidance Note On Internal Audit of General Insurance CompaniesABC 123No ratings yet

- Management Accountant June-2016Document124 pagesManagement Accountant June-2016ABC 123No ratings yet

- Management Accountant OCTOBER 2017Document124 pagesManagement Accountant OCTOBER 2017ABC 123No ratings yet

- Management Accountant Dec-2016Document124 pagesManagement Accountant Dec-2016ABC 123No ratings yet

- Management Accountant Feb-2016Document124 pagesManagement Accountant Feb-2016ABC 123No ratings yet

- Management Accountant May-2016Document124 pagesManagement Accountant May-2016ABC 123No ratings yet

- Management Accountant Aug-2016Document124 pagesManagement Accountant Aug-2016ABC 123No ratings yet

- Management Accountant March-2017Document124 pagesManagement Accountant March-2017ABC 123No ratings yet

- Management Accountant April-2016Document124 pagesManagement Accountant April-2016ABC 123No ratings yet

- Management Accountant Feb-2017Document124 pagesManagement Accountant Feb-2017ABC 123No ratings yet

- Management Accountant May-2017Document124 pagesManagement Accountant May-2017ABC 123No ratings yet

- Management Accountant Nov 2017Document124 pagesManagement Accountant Nov 2017ABC 123No ratings yet

- Management Accountant June 2018Document124 pagesManagement Accountant June 2018ABC 123No ratings yet

- Management Accountant - June 2017Document132 pagesManagement Accountant - June 2017ABC 123No ratings yet

- Management Accountant Nov 2018Document124 pagesManagement Accountant Nov 2018ABC 123No ratings yet

- Management Accountant Jan-2017Document124 pagesManagement Accountant Jan-2017ABC 123No ratings yet

- Management Accountant Oct 2018Document124 pagesManagement Accountant Oct 2018ABC 123No ratings yet

- Management Accountant Dec 2018Document124 pagesManagement Accountant Dec 2018ABC 123No ratings yet

- Management Accountant April-2017Document124 pagesManagement Accountant April-2017ABC 123No ratings yet

- Management Accountant March 2018Document124 pagesManagement Accountant March 2018ABC 123No ratings yet

- Management Accountant March 2019Document124 pagesManagement Accountant March 2019ABC 123No ratings yet

- Management Accountant July 2018Document124 pagesManagement Accountant July 2018ABC 123No ratings yet

- Management Accountant FEBRUARY-2019Document124 pagesManagement Accountant FEBRUARY-2019ABC 123No ratings yet

- Management Accountant Jan-2019Document124 pagesManagement Accountant Jan-2019ABC 123No ratings yet

- Management Accountant January - 2018Document124 pagesManagement Accountant January - 2018ABC 123No ratings yet

- Management Accountant May2019Document124 pagesManagement Accountant May2019ABC 123No ratings yet

- Management Accountant Nov 2019Document124 pagesManagement Accountant Nov 2019ABC 123No ratings yet

- Templates in Text and Chat - 327d21 PDFDocument3 pagesTemplates in Text and Chat - 327d21 PDFKRYSTEL WENDY LAHOMNo ratings yet

- Create A Seat Booking Form With Google Forms, Google Sheets and Google Apps Script - Yagisanatode - AppsScriptPulseDocument3 pagesCreate A Seat Booking Form With Google Forms, Google Sheets and Google Apps Script - Yagisanatode - AppsScriptPulsebrandy57279No ratings yet

- Law of Agency NotesDocument19 pagesLaw of Agency NotesChiedza Caroline ChikwehwaNo ratings yet

- Unit-8 Project Monitoring and ControlDocument98 pagesUnit-8 Project Monitoring and ControlPrà ShâñtNo ratings yet

- Report Sample-Supplier Factory AuditDocument24 pagesReport Sample-Supplier Factory AuditCarlosSánchezNo ratings yet

- Lista Fontes e Cabos Reparos 10.2023Document4 pagesLista Fontes e Cabos Reparos 10.2023amsacessorios00No ratings yet

- DLL in Commercial Cooking 7-Week 5Document5 pagesDLL in Commercial Cooking 7-Week 5JeeNha BonjoureNo ratings yet

- Kuala Lumpur: Answer Sheets: GBHDHFH: 23525: ABMC2054 Cost & Management Accounting IDocument30 pagesKuala Lumpur: Answer Sheets: GBHDHFH: 23525: ABMC2054 Cost & Management Accounting IJUN XIANG NGNo ratings yet

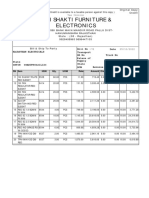

- Shri Shakti Furniture & Electronics: Credit OrginalDocument1 pageShri Shakti Furniture & Electronics: Credit OrginalRahul BansalNo ratings yet

- Outline ReportDocument11 pagesOutline ReportYt HuongNo ratings yet

- Semence Bonane Resume 2Document5 pagesSemence Bonane Resume 2api-240351783No ratings yet

- Making Omnichannel An Augmented Reality: The Current and Future State of The ArtDocument15 pagesMaking Omnichannel An Augmented Reality: The Current and Future State of The ArtRosario MoroccoNo ratings yet

- Relationship of Bank and CustomerDocument7 pagesRelationship of Bank and CustomerSelvenderan RamasamyNo ratings yet

- InternsDocument7 pagesInternsSadath KhanNo ratings yet

- Communication Skills: "Basic Principles of Effective Communication P-3"Document14 pagesCommunication Skills: "Basic Principles of Effective Communication P-3"Viral ShortsNo ratings yet

- Checklist of Requirements: Resource-Based Industries Service (Rbis)Document1 pageChecklist of Requirements: Resource-Based Industries Service (Rbis)MeowthemathicianNo ratings yet

- Ea 14Document4 pagesEa 14Nicole BatoyNo ratings yet

- Materiality AssessmentDocument4 pagesMateriality AssessmentDavid BoyerNo ratings yet

- EWB - App Form 07012020Document2 pagesEWB - App Form 07012020Francisco TaquioNo ratings yet

- Cloze TestDocument2 pagesCloze TestDuje GlavinaNo ratings yet

- Company Profile KAP Heliantono & Rekan Mei 2023Document12 pagesCompany Profile KAP Heliantono & Rekan Mei 2023Rezza PahlevyNo ratings yet

- End Term - Corporate FinanceDocument3 pagesEnd Term - Corporate FinanceDEBAPRIYA SARKARNo ratings yet

- FRABB IA Lubes&Greases EN042018Document24 pagesFRABB IA Lubes&Greases EN042018Hassan Ahmed100% (3)

- Report PDF Response ServletDocument2 pagesReport PDF Response ServletDeveshNo ratings yet

- 3dprinting at Gordon LibraryDocument1 page3dprinting at Gordon LibraryMatthew LinNo ratings yet

- Offer Letter 27-Dec-2019 PDFDocument25 pagesOffer Letter 27-Dec-2019 PDFIonutz AsafteiNo ratings yet

- FCA Checklist and Guide For Building Owners & Operators - AkitaBox EbookDocument7 pagesFCA Checklist and Guide For Building Owners & Operators - AkitaBox Ebooksenora dolce azulNo ratings yet

- Revaluation ModelDocument36 pagesRevaluation ModelMarjorie PalmaNo ratings yet

- Tourism Good Practice Guide PDFDocument38 pagesTourism Good Practice Guide PDFEva MarieNo ratings yet