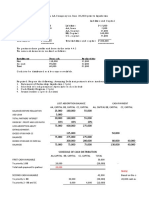

Midterm Quiz 01 - Adjusting Entries From Accrual To Provision For Uncollectible Accounts

Midterm Quiz 01 - Adjusting Entries From Accrual To Provision For Uncollectible Accounts

You might also like

- Adjusting EntriesDocument71 pagesAdjusting EntriesLeteSsie66% (29)

- Corporate Banking - Interview PrepDocument3 pagesCorporate Banking - Interview PrepsensibledeveshNo ratings yet

- Adjusting Entries Exercises - EditedDocument4 pagesAdjusting Entries Exercises - EditedCINDY LIAN CABILLON100% (2)

- Computerised Accounting Practice Set Using Xero Online Accounting: Australian EditionFrom EverandComputerised Accounting Practice Set Using Xero Online Accounting: Australian EditionNo ratings yet

- 162 001Document1 page162 001Christian Mark AbarquezNo ratings yet

- ACT1101, PRB, Midterm, Wit Ans KeyDocument5 pagesACT1101, PRB, Midterm, Wit Ans KeyDyen100% (1)

- Know Your Customer Form (Kyc)Document2 pagesKnow Your Customer Form (Kyc)Shivanand ShirolNo ratings yet

- Answer Key - Exercises - Adjusting EntriesDocument4 pagesAnswer Key - Exercises - Adjusting EntriesAlexa AbaryNo ratings yet

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- Exercises II - Adjusting TransactionsDocument2 pagesExercises II - Adjusting TransactionsJowjie TV80% (5)

- ADJUSTING ENTRIES Answer QUIZ ACCRUALS & DEFERRALSDocument5 pagesADJUSTING ENTRIES Answer QUIZ ACCRUALS & DEFERRALSHassanhor Guro BacolodNo ratings yet

- INSTRUCTIONS: Select The Correct Answer For Each of The Following Questions. Mark OnlyDocument15 pagesINSTRUCTIONS: Select The Correct Answer For Each of The Following Questions. Mark OnlyMendoza Ron NixonNo ratings yet

- Cash Basis Accrual Basis Exercises With AnswersDocument6 pagesCash Basis Accrual Basis Exercises With AnswersRNo ratings yet

- D Web OPResume Upload 10178 Project 30551 File 50130 Accountingweek4HWyouSKQODocument6 pagesD Web OPResume Upload 10178 Project 30551 File 50130 Accountingweek4HWyouSKQOChristy Wu100% (1)

- Adjusting Entries Christine Gamba CargoDocument5 pagesAdjusting Entries Christine Gamba Cargoelma wagwag100% (2)

- Assignment Accounting AJE GUIANGDocument14 pagesAssignment Accounting AJE GUIANGIce Voltaire B. GuiangNo ratings yet

- Cfas Exam3 ProblemsDocument8 pagesCfas Exam3 ProblemspolxrixNo ratings yet

- Adjusting Entries Exercises LandscapeDocument3 pagesAdjusting Entries Exercises LandscapeTatyanna Kaliah100% (3)

- ACCTG1 PrefinalsDocument23 pagesACCTG1 PrefinalsJAN RAY CUISON VISPERAS100% (1)

- Adjusting Journal EntriesDocument8 pagesAdjusting Journal EntriesChaaaNo ratings yet

- IA2 Prelim ExamDocument7 pagesIA2 Prelim ExamJohn FloresNo ratings yet

- Adjusting Entry - AnswerDocument8 pagesAdjusting Entry - AnswerReighjon Ashley C. TolentinoNo ratings yet

- Ac101 Prelim ExamDocument1 pageAc101 Prelim ExamMariam� AmilNo ratings yet

- ACCTING Pg. 217Document2 pagesACCTING Pg. 217Now OnwooNo ratings yet

- Midterm Exam-Adjusting EntriesDocument5 pagesMidterm Exam-Adjusting EntriesHassanhor Guro BacolodNo ratings yet

- Comm 457Document4 pagesComm 457reetNo ratings yet

- Homework On Current Liabilities 1st Term Sy2018-2019Document4 pagesHomework On Current Liabilities 1st Term Sy2018-2019RedNo ratings yet

- FAR-01 Trade & Other PayableDocument3 pagesFAR-01 Trade & Other PayablehIgh QuaLIty SVT100% (1)

- 3 Adjusting Entries HandoutsDocument10 pages3 Adjusting Entries HandoutsJuan Dela CruzNo ratings yet

- August 20 DiscussionDocument26 pagesAugust 20 DiscussionJOSCEL SYJONGTIANNo ratings yet

- Seeds of The Nations Accounting Quiz ON Basic AccountingDocument25 pagesSeeds of The Nations Accounting Quiz ON Basic AccountingHershey GalvezNo ratings yet

- ADJUSTING ENTRIES NewDocument47 pagesADJUSTING ENTRIES NewShane Kim100% (1)

- Correction of ErrorsDocument15 pagesCorrection of ErrorsEliyah Jhonson100% (1)

- Coactg1 Common Exam ReviewerDocument7 pagesCoactg1 Common Exam ReviewerIvy Rose BorasNo ratings yet

- Intermediate Accounting 1 Problems and SolutionDocument26 pagesIntermediate Accounting 1 Problems and SolutionRAFALLO, ABMYR ROSE R.No ratings yet

- Polytechnic University of The Philippines College of Accountancy Santa Maria, BulacanDocument3 pagesPolytechnic University of The Philippines College of Accountancy Santa Maria, BulacanJudith Batisan100% (1)

- Exercise. AdjustmentsDocument6 pagesExercise. AdjustmentsDavid Con Rivero79% (14)

- H05.FA2-01 Trade & Other Payables - HernandezDocument5 pagesH05.FA2-01 Trade & Other Payables - HernandezBea GarciaNo ratings yet

- FAR-07 Trade & Other PayableDocument3 pagesFAR-07 Trade & Other PayableKim Cristian MaañoNo ratings yet

- Adjusting Entries For Bad DebtsDocument6 pagesAdjusting Entries For Bad DebtsKristine IvyNo ratings yet

- Adjustments Quiz 1Document6 pagesAdjustments Quiz 1Christine Mae BurgosNo ratings yet

- NOTES PROBLEMS ACCTG-323-newDocument3 pagesNOTES PROBLEMS ACCTG-323-newJoyluxxiNo ratings yet

- Quiz 02 - FAR - UCP - ANS KEYDocument9 pagesQuiz 02 - FAR - UCP - ANS KEYkarim abitagoNo ratings yet

- Cabigon Problem 1 AuditDocument2 pagesCabigon Problem 1 AuditGianrie Gwyneth CabigonNo ratings yet

- Adjusting Entries Discussion and SolutionDocument6 pagesAdjusting Entries Discussion and SolutionGarp BarrocaNo ratings yet

- Adjusting Entries and Promissory NotesDocument6 pagesAdjusting Entries and Promissory Noteselma wagwagNo ratings yet

- Seatwork 3-Liabilities 22Aug2019JMDocument3 pagesSeatwork 3-Liabilities 22Aug2019JMJoseph II MendozaNo ratings yet

- Activity 4 - Basic AccountingDocument3 pagesActivity 4 - Basic AccountingEunice MartinezNo ratings yet

- 2019.1.19 20 Aud Prob Error Correction Cash Inventory Non Financial Assets Equity PDFDocument25 pages2019.1.19 20 Aud Prob Error Correction Cash Inventory Non Financial Assets Equity PDFMae-shane SagayoNo ratings yet

- Seatwork in Audit 2-3Document8 pagesSeatwork in Audit 2-3Shr BnNo ratings yet

- Error Correction Problem 1: Lord Gen A. Rilloraza, CPADocument5 pagesError Correction Problem 1: Lord Gen A. Rilloraza, CPAMae-shane SagayoNo ratings yet

- Financial Accounting and Reporting: Exercise 1Document8 pagesFinancial Accounting and Reporting: Exercise 1Lenneth Mones0% (1)

- ACCT1101 Wk6 Tutorial 5 SolutionsDocument7 pagesACCT1101 Wk6 Tutorial 5 SolutionskyleNo ratings yet

- IA2Document12 pagesIA2John FloresNo ratings yet

- ABM 1 Adjustments and WorksheetDocument4 pagesABM 1 Adjustments and WorksheetChelsie Coliflores100% (1)

- NonesDocument15 pagesNonesMary Rose Nones100% (3)

- Problem 1-10 (AICPA) : SolutionDocument3 pagesProblem 1-10 (AICPA) : SolutionElla Rence TablizoNo ratings yet

- Homework On Current LiabilitiesDocument3 pagesHomework On Current LiabilitiesalyssaNo ratings yet

- Problem 1,2,4 and 6Document4 pagesProblem 1,2,4 and 6Wendelyn JimenezNo ratings yet

- Review of The Accounting ProcessDocument4 pagesReview of The Accounting ProcessAngel TumamaoNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- 85184767Document9 pages85184767Garp BarrocaNo ratings yet

- Partnership FormationDocument51 pagesPartnership FormationGarp BarrocaNo ratings yet

- Cash and Cash Equivalents: Answer: CDocument142 pagesCash and Cash Equivalents: Answer: CGarp BarrocaNo ratings yet

- Ans Key Inst Liq4Document7 pagesAns Key Inst Liq4Garp BarrocaNo ratings yet

- Acctg13 Midterm Exam TQ 2021 2022 2nd SemDocument6 pagesAcctg13 Midterm Exam TQ 2021 2022 2nd SemGarp BarrocaNo ratings yet

- 52055576Document1 page52055576Garp BarrocaNo ratings yet

- Problem 1Document5 pagesProblem 1Garp BarrocaNo ratings yet

- Prelim Exercises Partnership Operation 28Document5 pagesPrelim Exercises Partnership Operation 28Garp BarrocaNo ratings yet

- InstructionsDocument7 pagesInstructionsGarp BarrocaNo ratings yet

- AtelengDocument2 pagesAtelengGarp BarrocaNo ratings yet

- College of Accountancy Pioneer Avenue, General Santos City: Ramon Magsaysay Memorial CollegesDocument21 pagesCollege of Accountancy Pioneer Avenue, General Santos City: Ramon Magsaysay Memorial CollegesGarp BarrocaNo ratings yet

- City of Iriga Vs CASURECODocument2 pagesCity of Iriga Vs CASURECOGarp BarrocaNo ratings yet

- PDF Solution Manual Partnership Amp Corporation 2014 2015 PDFDocument81 pagesPDF Solution Manual Partnership Amp Corporation 2014 2015 PDFGarp BarrocaNo ratings yet

- Prelim Quiz 1Document1 pagePrelim Quiz 1Garp BarrocaNo ratings yet

- Investment and Portfolio AnalysisDocument26 pagesInvestment and Portfolio Analysismakoto-sanNo ratings yet

- Aqua$Ure: IitseadDocument20 pagesAqua$Ure: IitseadestherNo ratings yet

- Pulse of Fintech 2018: Blockchain Investment Exceeds 2017 Annual TotalDocument2 pagesPulse of Fintech 2018: Blockchain Investment Exceeds 2017 Annual TotalSergio VinsennauNo ratings yet

- Tax System in IndiaDocument53 pagesTax System in Indiadeepakldh998899No ratings yet

- QUESTIONARRIEDocument4 pagesQUESTIONARRIEHarry HaranNo ratings yet

- Microsoft Financial Data - FY19Q1Document26 pagesMicrosoft Financial Data - FY19Q1trisanka banikNo ratings yet

- Prepayment - U22206001.st FinalDocument1 pagePrepayment - U22206001.st FinalDODI HARIYANTONo ratings yet

- Fy 2016 AuditedDocument222 pagesFy 2016 AuditedError 707No ratings yet

- Calculating Your Adjusted Cost BaseDocument2 pagesCalculating Your Adjusted Cost BaseKerry DouganNo ratings yet

- Introducing Broker Accounts: Fully Disclosed BrokersDocument1 pageIntroducing Broker Accounts: Fully Disclosed Brokersbwarner6986No ratings yet

- Firm Specific Determinants of Financial Distress EDocument8 pagesFirm Specific Determinants of Financial Distress ENhu NgocNo ratings yet

- @1 Fundamentals of Financial Accounting - WSUDocument164 pages@1 Fundamentals of Financial Accounting - WSUDùķe HPNo ratings yet

- Merchandising ActivityDocument12 pagesMerchandising ActivityCherie Soriano Ananayo100% (2)

- Distinguishing Revenue, Profitability, and Risk MetricsDocument2 pagesDistinguishing Revenue, Profitability, and Risk MetricsminhanhNo ratings yet

- Introduction To AccountingDocument22 pagesIntroduction To AccountingAnamika Singh PariharNo ratings yet

- Nomisma Mobile Solutions Pvt. LTD Tax Payslip For December - 2018Document2 pagesNomisma Mobile Solutions Pvt. LTD Tax Payslip For December - 2018Dinesh SahuNo ratings yet

- Jupiter Management CompanyDocument15 pagesJupiter Management CompanyDhruv BansalNo ratings yet

- FM Unit 8 Lecture Notes - Capital BudgetingDocument4 pagesFM Unit 8 Lecture Notes - Capital BudgetingDebbie DebzNo ratings yet

- Credit Transaction CasesDocument10 pagesCredit Transaction CasesLianne Carmeli B. FronterasNo ratings yet

- Sample ResumeDocument1 pageSample ResumeKelvin Lim Wei LiangNo ratings yet

- Ca Inter Advanced Accounting MCQDocument210 pagesCa Inter Advanced Accounting MCQVikramNo ratings yet

- DeKalb 2009 Recommended BudgetDocument271 pagesDeKalb 2009 Recommended BudgetDeKalb Officers100% (1)

- Qualified Written Request TemplateDocument2 pagesQualified Written Request Templatepkelly68No ratings yet

- Example (Pty) LTD: Code Billing Name Billing Address Tax NumberDocument1 pageExample (Pty) LTD: Code Billing Name Billing Address Tax NumberKashif ehsanNo ratings yet

- Chapter 21 QADocument2 pagesChapter 21 QAjdbridgesNo ratings yet

- Matrix Poultry Business PlanDocument13 pagesMatrix Poultry Business Planomosebi isaac anuoluwapoNo ratings yet

- Questions BookDocument437 pagesQuestions BookShairish Ajmeri100% (1)

Download as docx, pdf, or txt

You might also like

- Adjusting EntriesDocument71 pagesAdjusting EntriesLeteSsie66% (29)

- Corporate Banking - Interview PrepDocument3 pagesCorporate Banking - Interview PrepsensibledeveshNo ratings yet

- Adjusting Entries Exercises - EditedDocument4 pagesAdjusting Entries Exercises - EditedCINDY LIAN CABILLON100% (2)

- Computerised Accounting Practice Set Using Xero Online Accounting: Australian EditionFrom EverandComputerised Accounting Practice Set Using Xero Online Accounting: Australian EditionNo ratings yet

- 162 001Document1 page162 001Christian Mark AbarquezNo ratings yet

- ACT1101, PRB, Midterm, Wit Ans KeyDocument5 pagesACT1101, PRB, Midterm, Wit Ans KeyDyen100% (1)

- Know Your Customer Form (Kyc)Document2 pagesKnow Your Customer Form (Kyc)Shivanand ShirolNo ratings yet

- Answer Key - Exercises - Adjusting EntriesDocument4 pagesAnswer Key - Exercises - Adjusting EntriesAlexa AbaryNo ratings yet

- Computerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionFrom EverandComputerised Accounting Practice Set Using MYOB AccountRight - Advanced Level: Australian EditionNo ratings yet

- Exercises II - Adjusting TransactionsDocument2 pagesExercises II - Adjusting TransactionsJowjie TV80% (5)

- ADJUSTING ENTRIES Answer QUIZ ACCRUALS & DEFERRALSDocument5 pagesADJUSTING ENTRIES Answer QUIZ ACCRUALS & DEFERRALSHassanhor Guro BacolodNo ratings yet

- INSTRUCTIONS: Select The Correct Answer For Each of The Following Questions. Mark OnlyDocument15 pagesINSTRUCTIONS: Select The Correct Answer For Each of The Following Questions. Mark OnlyMendoza Ron NixonNo ratings yet

- Cash Basis Accrual Basis Exercises With AnswersDocument6 pagesCash Basis Accrual Basis Exercises With AnswersRNo ratings yet

- D Web OPResume Upload 10178 Project 30551 File 50130 Accountingweek4HWyouSKQODocument6 pagesD Web OPResume Upload 10178 Project 30551 File 50130 Accountingweek4HWyouSKQOChristy Wu100% (1)

- Adjusting Entries Christine Gamba CargoDocument5 pagesAdjusting Entries Christine Gamba Cargoelma wagwag100% (2)

- Assignment Accounting AJE GUIANGDocument14 pagesAssignment Accounting AJE GUIANGIce Voltaire B. GuiangNo ratings yet

- Cfas Exam3 ProblemsDocument8 pagesCfas Exam3 ProblemspolxrixNo ratings yet

- Adjusting Entries Exercises LandscapeDocument3 pagesAdjusting Entries Exercises LandscapeTatyanna Kaliah100% (3)

- ACCTG1 PrefinalsDocument23 pagesACCTG1 PrefinalsJAN RAY CUISON VISPERAS100% (1)

- Adjusting Journal EntriesDocument8 pagesAdjusting Journal EntriesChaaaNo ratings yet

- IA2 Prelim ExamDocument7 pagesIA2 Prelim ExamJohn FloresNo ratings yet

- Adjusting Entry - AnswerDocument8 pagesAdjusting Entry - AnswerReighjon Ashley C. TolentinoNo ratings yet

- Ac101 Prelim ExamDocument1 pageAc101 Prelim ExamMariam� AmilNo ratings yet

- ACCTING Pg. 217Document2 pagesACCTING Pg. 217Now OnwooNo ratings yet

- Midterm Exam-Adjusting EntriesDocument5 pagesMidterm Exam-Adjusting EntriesHassanhor Guro BacolodNo ratings yet

- Comm 457Document4 pagesComm 457reetNo ratings yet

- Homework On Current Liabilities 1st Term Sy2018-2019Document4 pagesHomework On Current Liabilities 1st Term Sy2018-2019RedNo ratings yet

- FAR-01 Trade & Other PayableDocument3 pagesFAR-01 Trade & Other PayablehIgh QuaLIty SVT100% (1)

- 3 Adjusting Entries HandoutsDocument10 pages3 Adjusting Entries HandoutsJuan Dela CruzNo ratings yet

- August 20 DiscussionDocument26 pagesAugust 20 DiscussionJOSCEL SYJONGTIANNo ratings yet

- Seeds of The Nations Accounting Quiz ON Basic AccountingDocument25 pagesSeeds of The Nations Accounting Quiz ON Basic AccountingHershey GalvezNo ratings yet

- ADJUSTING ENTRIES NewDocument47 pagesADJUSTING ENTRIES NewShane Kim100% (1)

- Correction of ErrorsDocument15 pagesCorrection of ErrorsEliyah Jhonson100% (1)

- Coactg1 Common Exam ReviewerDocument7 pagesCoactg1 Common Exam ReviewerIvy Rose BorasNo ratings yet

- Intermediate Accounting 1 Problems and SolutionDocument26 pagesIntermediate Accounting 1 Problems and SolutionRAFALLO, ABMYR ROSE R.No ratings yet

- Polytechnic University of The Philippines College of Accountancy Santa Maria, BulacanDocument3 pagesPolytechnic University of The Philippines College of Accountancy Santa Maria, BulacanJudith Batisan100% (1)

- Exercise. AdjustmentsDocument6 pagesExercise. AdjustmentsDavid Con Rivero79% (14)

- H05.FA2-01 Trade & Other Payables - HernandezDocument5 pagesH05.FA2-01 Trade & Other Payables - HernandezBea GarciaNo ratings yet

- FAR-07 Trade & Other PayableDocument3 pagesFAR-07 Trade & Other PayableKim Cristian MaañoNo ratings yet

- Adjusting Entries For Bad DebtsDocument6 pagesAdjusting Entries For Bad DebtsKristine IvyNo ratings yet

- Adjustments Quiz 1Document6 pagesAdjustments Quiz 1Christine Mae BurgosNo ratings yet

- NOTES PROBLEMS ACCTG-323-newDocument3 pagesNOTES PROBLEMS ACCTG-323-newJoyluxxiNo ratings yet

- Quiz 02 - FAR - UCP - ANS KEYDocument9 pagesQuiz 02 - FAR - UCP - ANS KEYkarim abitagoNo ratings yet

- Cabigon Problem 1 AuditDocument2 pagesCabigon Problem 1 AuditGianrie Gwyneth CabigonNo ratings yet

- Adjusting Entries Discussion and SolutionDocument6 pagesAdjusting Entries Discussion and SolutionGarp BarrocaNo ratings yet

- Adjusting Entries and Promissory NotesDocument6 pagesAdjusting Entries and Promissory Noteselma wagwagNo ratings yet

- Seatwork 3-Liabilities 22Aug2019JMDocument3 pagesSeatwork 3-Liabilities 22Aug2019JMJoseph II MendozaNo ratings yet

- Activity 4 - Basic AccountingDocument3 pagesActivity 4 - Basic AccountingEunice MartinezNo ratings yet

- 2019.1.19 20 Aud Prob Error Correction Cash Inventory Non Financial Assets Equity PDFDocument25 pages2019.1.19 20 Aud Prob Error Correction Cash Inventory Non Financial Assets Equity PDFMae-shane SagayoNo ratings yet

- Seatwork in Audit 2-3Document8 pagesSeatwork in Audit 2-3Shr BnNo ratings yet

- Error Correction Problem 1: Lord Gen A. Rilloraza, CPADocument5 pagesError Correction Problem 1: Lord Gen A. Rilloraza, CPAMae-shane SagayoNo ratings yet

- Financial Accounting and Reporting: Exercise 1Document8 pagesFinancial Accounting and Reporting: Exercise 1Lenneth Mones0% (1)

- ACCT1101 Wk6 Tutorial 5 SolutionsDocument7 pagesACCT1101 Wk6 Tutorial 5 SolutionskyleNo ratings yet

- IA2Document12 pagesIA2John FloresNo ratings yet

- ABM 1 Adjustments and WorksheetDocument4 pagesABM 1 Adjustments and WorksheetChelsie Coliflores100% (1)

- NonesDocument15 pagesNonesMary Rose Nones100% (3)

- Problem 1-10 (AICPA) : SolutionDocument3 pagesProblem 1-10 (AICPA) : SolutionElla Rence TablizoNo ratings yet

- Homework On Current LiabilitiesDocument3 pagesHomework On Current LiabilitiesalyssaNo ratings yet

- Problem 1,2,4 and 6Document4 pagesProblem 1,2,4 and 6Wendelyn JimenezNo ratings yet

- Review of The Accounting ProcessDocument4 pagesReview of The Accounting ProcessAngel TumamaoNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- 85184767Document9 pages85184767Garp BarrocaNo ratings yet

- Partnership FormationDocument51 pagesPartnership FormationGarp BarrocaNo ratings yet

- Cash and Cash Equivalents: Answer: CDocument142 pagesCash and Cash Equivalents: Answer: CGarp BarrocaNo ratings yet

- Ans Key Inst Liq4Document7 pagesAns Key Inst Liq4Garp BarrocaNo ratings yet

- Acctg13 Midterm Exam TQ 2021 2022 2nd SemDocument6 pagesAcctg13 Midterm Exam TQ 2021 2022 2nd SemGarp BarrocaNo ratings yet

- 52055576Document1 page52055576Garp BarrocaNo ratings yet

- Problem 1Document5 pagesProblem 1Garp BarrocaNo ratings yet

- Prelim Exercises Partnership Operation 28Document5 pagesPrelim Exercises Partnership Operation 28Garp BarrocaNo ratings yet

- InstructionsDocument7 pagesInstructionsGarp BarrocaNo ratings yet

- AtelengDocument2 pagesAtelengGarp BarrocaNo ratings yet

- College of Accountancy Pioneer Avenue, General Santos City: Ramon Magsaysay Memorial CollegesDocument21 pagesCollege of Accountancy Pioneer Avenue, General Santos City: Ramon Magsaysay Memorial CollegesGarp BarrocaNo ratings yet

- City of Iriga Vs CASURECODocument2 pagesCity of Iriga Vs CASURECOGarp BarrocaNo ratings yet

- PDF Solution Manual Partnership Amp Corporation 2014 2015 PDFDocument81 pagesPDF Solution Manual Partnership Amp Corporation 2014 2015 PDFGarp BarrocaNo ratings yet

- Prelim Quiz 1Document1 pagePrelim Quiz 1Garp BarrocaNo ratings yet

- Investment and Portfolio AnalysisDocument26 pagesInvestment and Portfolio Analysismakoto-sanNo ratings yet

- Aqua$Ure: IitseadDocument20 pagesAqua$Ure: IitseadestherNo ratings yet

- Pulse of Fintech 2018: Blockchain Investment Exceeds 2017 Annual TotalDocument2 pagesPulse of Fintech 2018: Blockchain Investment Exceeds 2017 Annual TotalSergio VinsennauNo ratings yet

- Tax System in IndiaDocument53 pagesTax System in Indiadeepakldh998899No ratings yet

- QUESTIONARRIEDocument4 pagesQUESTIONARRIEHarry HaranNo ratings yet

- Microsoft Financial Data - FY19Q1Document26 pagesMicrosoft Financial Data - FY19Q1trisanka banikNo ratings yet

- Prepayment - U22206001.st FinalDocument1 pagePrepayment - U22206001.st FinalDODI HARIYANTONo ratings yet

- Fy 2016 AuditedDocument222 pagesFy 2016 AuditedError 707No ratings yet

- Calculating Your Adjusted Cost BaseDocument2 pagesCalculating Your Adjusted Cost BaseKerry DouganNo ratings yet

- Introducing Broker Accounts: Fully Disclosed BrokersDocument1 pageIntroducing Broker Accounts: Fully Disclosed Brokersbwarner6986No ratings yet

- Firm Specific Determinants of Financial Distress EDocument8 pagesFirm Specific Determinants of Financial Distress ENhu NgocNo ratings yet

- @1 Fundamentals of Financial Accounting - WSUDocument164 pages@1 Fundamentals of Financial Accounting - WSUDùķe HPNo ratings yet

- Merchandising ActivityDocument12 pagesMerchandising ActivityCherie Soriano Ananayo100% (2)

- Distinguishing Revenue, Profitability, and Risk MetricsDocument2 pagesDistinguishing Revenue, Profitability, and Risk MetricsminhanhNo ratings yet

- Introduction To AccountingDocument22 pagesIntroduction To AccountingAnamika Singh PariharNo ratings yet

- Nomisma Mobile Solutions Pvt. LTD Tax Payslip For December - 2018Document2 pagesNomisma Mobile Solutions Pvt. LTD Tax Payslip For December - 2018Dinesh SahuNo ratings yet

- Jupiter Management CompanyDocument15 pagesJupiter Management CompanyDhruv BansalNo ratings yet

- FM Unit 8 Lecture Notes - Capital BudgetingDocument4 pagesFM Unit 8 Lecture Notes - Capital BudgetingDebbie DebzNo ratings yet

- Credit Transaction CasesDocument10 pagesCredit Transaction CasesLianne Carmeli B. FronterasNo ratings yet

- Sample ResumeDocument1 pageSample ResumeKelvin Lim Wei LiangNo ratings yet

- Ca Inter Advanced Accounting MCQDocument210 pagesCa Inter Advanced Accounting MCQVikramNo ratings yet

- DeKalb 2009 Recommended BudgetDocument271 pagesDeKalb 2009 Recommended BudgetDeKalb Officers100% (1)

- Qualified Written Request TemplateDocument2 pagesQualified Written Request Templatepkelly68No ratings yet

- Example (Pty) LTD: Code Billing Name Billing Address Tax NumberDocument1 pageExample (Pty) LTD: Code Billing Name Billing Address Tax NumberKashif ehsanNo ratings yet

- Chapter 21 QADocument2 pagesChapter 21 QAjdbridgesNo ratings yet

- Matrix Poultry Business PlanDocument13 pagesMatrix Poultry Business Planomosebi isaac anuoluwapoNo ratings yet

- Questions BookDocument437 pagesQuestions BookShairish Ajmeri100% (1)