Download as docx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5822)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Hospital Supply Inc. - SolutionsDocument5 pagesHospital Supply Inc. - SolutionsMEERA JOSHY 192743633% (3)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Problems in Overhead AllocationDocument2 pagesProblems in Overhead AllocationMEERA JOSHY 1927436No ratings yet

- AI Basics Pages 1 - 50 - Flip PDF Download - FlipHTML5 PDFDocument196 pagesAI Basics Pages 1 - 50 - Flip PDF Download - FlipHTML5 PDFMEERA JOSHY 1927436No ratings yet

- Tax Changes in India and Morocco Taxation CiaDocument20 pagesTax Changes in India and Morocco Taxation CiaMEERA JOSHY 1927436No ratings yet

- Research Proposal ReportDocument5 pagesResearch Proposal ReportMEERA JOSHY 1927436No ratings yet

- November - 2015 - 1447761370 - 44 FosterDocument3 pagesNovember - 2015 - 1447761370 - 44 FosterMEERA JOSHY 1927436No ratings yet

- International Journal of Research ISSN NO:2236-6124Document21 pagesInternational Journal of Research ISSN NO:2236-6124MEERA JOSHY 1927436No ratings yet

- AI: A Game-Changer For Financial InclusionDocument13 pagesAI: A Game-Changer For Financial InclusionMEERA JOSHY 1927436No ratings yet

- Invoice 203265: GN Code: 3923.2100 - SwedenDocument2 pagesInvoice 203265: GN Code: 3923.2100 - SwedenArturo RiveroNo ratings yet

- MUXDocument5 pagesMUXAmit SahaNo ratings yet

- Aerodynamics of Rugby BallDocument5 pagesAerodynamics of Rugby BallChandra Harsha100% (1)

- Boli Interne Vol I Partea 1Document454 pagesBoli Interne Vol I Partea 1Murariu Diana100% (2)

- Chemistry Test of Concepts: The Test Will Take Approximately 120 MinutesDocument13 pagesChemistry Test of Concepts: The Test Will Take Approximately 120 MinutesOmar Ayman Mahmoud EssaNo ratings yet

- 014 - 030 Single Reduction Worm IntroductionDocument17 pages014 - 030 Single Reduction Worm IntroductionAlejandro MartinezNo ratings yet

- Digital Control Systems (Elective) : Suggested ReadingDocument1 pageDigital Control Systems (Elective) : Suggested ReadingBebo DiaNo ratings yet

- Ncert Solutions Class 12 Accountancy Part 2 Chapter 1 Accounting For Share CapitalDocument42 pagesNcert Solutions Class 12 Accountancy Part 2 Chapter 1 Accounting For Share CapitalcchendrimadaNo ratings yet

- HAQ Instructions (ARAMIS) 6-30-09Document16 pagesHAQ Instructions (ARAMIS) 6-30-09nurasyikahNo ratings yet

- Chapter 10 Dealing With Uncertainty: General ProcedureDocument15 pagesChapter 10 Dealing With Uncertainty: General ProcedureHannan Mahmood TonmoyNo ratings yet

- Arlec Wireless SecurityDocument10 pagesArlec Wireless Securityalfi56kNo ratings yet

- DS Workbook 23SC1202Document199 pagesDS Workbook 23SC1202Arjun JagiriNo ratings yet

- 1 s2.0 S1359431115011898 MainDocument11 pages1 s2.0 S1359431115011898 MainPatrice PariNo ratings yet

- Ritishree Offer EztruckDocument4 pagesRitishree Offer EztruckKali RathNo ratings yet

- Employee Background Verification SystemDocument5 pagesEmployee Background Verification SystemPayal ChauhanNo ratings yet

- Jargeous - Product - Catalog Ver 1220 Compressed PDFDocument16 pagesJargeous - Product - Catalog Ver 1220 Compressed PDFFirdaus YahyaNo ratings yet

- Athletics Throwing EventsDocument8 pagesAthletics Throwing EventsJehan PugosaNo ratings yet

- Evaporation of Different Liquids PDFDocument2 pagesEvaporation of Different Liquids PDFMandyNo ratings yet

- VIR - Reform in TelecommunicationsDocument10 pagesVIR - Reform in TelecommunicationsNgu HoangNo ratings yet

- Building Construction and Materials Report: Curtain Wall Building Type Building Name: Seagrams BuildingDocument6 pagesBuilding Construction and Materials Report: Curtain Wall Building Type Building Name: Seagrams BuildingAyushi AroraNo ratings yet

- Judi Online Di MedsosDocument11 pagesJudi Online Di MedsosHabibah HabibahNo ratings yet

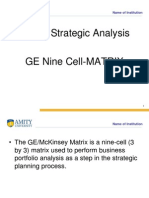

- GE - Nine CellDocument12 pagesGE - Nine CellNikita SangalNo ratings yet

- 08-01-17 EditionDocument28 pages08-01-17 EditionSan Mateo Daily JournalNo ratings yet

- 400 Bad Request 400 Bad Request Nginx/1.2.9Document13 pages400 Bad Request 400 Bad Request Nginx/1.2.9USAFVOSBNo ratings yet

- SpeechDocument5 pagesSpeechNiza Pinky IchiyuNo ratings yet

- Periodontal Ligament-SummerDocument24 pagesPeriodontal Ligament-Summerapi-3775747100% (1)

- Residence Time Distribution For Chemical ReactorsDocument71 pagesResidence Time Distribution For Chemical ReactorsJuan Carlos Serrano MedranoNo ratings yet

- Anand RathiDocument95 pagesAnand Rathivikramgupta195096% (25)

- Corporate Nvidia in BriefDocument2 pagesCorporate Nvidia in BriefakesplwebsiteNo ratings yet

- Lecturers HO No. 9 2023 Pre Week in Commercial LawDocument94 pagesLecturers HO No. 9 2023 Pre Week in Commercial LawElle WoodsNo ratings yet