Download as docx, pdf, or txt

You might also like

- Approval For Signing The Audit Report: M Jones 25.7.11Document52 pagesApproval For Signing The Audit Report: M Jones 25.7.11Kwasi Boatey100% (1)

- CA Foundation Accounts Theory Notes PDFDocument25 pagesCA Foundation Accounts Theory Notes PDFVedanti Kohli100% (8)

- Exercise 1 Sample Audit PlanDocument2 pagesExercise 1 Sample Audit PlanBennice 8No ratings yet

- LeaP-ABM-FABM1-Week 1 To 5Document4 pagesLeaP-ABM-FABM1-Week 1 To 5Paulo Amposta Carpio100% (1)

- Audit Planning MemorandumDocument7 pagesAudit Planning Memorandumkellychuunga100% (7)

- Auditing McqsDocument8 pagesAuditing McqsMusharaf HussainNo ratings yet

- Documentation (CH10) : Hand NoteDocument9 pagesDocumentation (CH10) : Hand NoteMd. Milon ChowdhuryNo ratings yet

- Directorate General of Shipping, Govt. of India: Ism Code Auditor Monitoring ReportDocument1 pageDirectorate General of Shipping, Govt. of India: Ism Code Auditor Monitoring ReportChetanNo ratings yet

- SME Governance Assessment Tool Worksheet: Response/Comment Source Commitment/Basic LevelDocument10 pagesSME Governance Assessment Tool Worksheet: Response/Comment Source Commitment/Basic LevelChahine SerghineNo ratings yet

- Test 3Document2 pagesTest 3Mr. Demon ExtraNo ratings yet

- Activity Sheet - Module 10Document2 pagesActivity Sheet - Module 10Chris JacksonNo ratings yet

- SA-580-written-representations NotesDocument11 pagesSA-580-written-representations NotesDarsini KumarNo ratings yet

- UAA Questionnaire - Initiative-A1fDocument9 pagesUAA Questionnaire - Initiative-A1fMary Justine AvanceñaNo ratings yet

- Obtaining An Engagement (CH2)Document7 pagesObtaining An Engagement (CH2)Md. Milon ChowdhuryNo ratings yet

- Lec 1-9Document26 pagesLec 1-9Linh PhanNo ratings yet

- Concept and Need For Assurance (CH1)Document16 pagesConcept and Need For Assurance (CH1)Md. Milon ChowdhuryNo ratings yet

- B6. Justification of Audit ReportDocument2 pagesB6. Justification of Audit Reportjuwelmahmud117No ratings yet

- ANNEXURE-1 Questionnaire: Dear, Sir/MadamDocument14 pagesANNEXURE-1 Questionnaire: Dear, Sir/MadamShubham TrivediNo ratings yet

- Basic ConceptsDocument10 pagesBasic ConceptsJohayra AbbasNo ratings yet

- Planning The Assignment (CH 3)Document17 pagesPlanning The Assignment (CH 3)Md. Milon ChowdhuryNo ratings yet

- Tutorial 9 - Audit Report MSDocument10 pagesTutorial 9 - Audit Report MSTeresa TanNo ratings yet

- CHAP 26. Internal and Government Financial Auditing and Operational AuditinDocument16 pagesCHAP 26. Internal and Government Financial Auditing and Operational AuditinNoroNo ratings yet

- Accounting DefinitionDocument4 pagesAccounting DefinitionMarjealyn PortugalNo ratings yet

- Audit December 2017 EngDocument17 pagesAudit December 2017 EngNthabiseng ButsanaNo ratings yet

- MSQS For ExamDocument6 pagesMSQS For ExamWali KhanNo ratings yet

- About AuditDocument6 pagesAbout AuditWali KhanNo ratings yet

- Controls Chapter Revision Questions AnswersDocument30 pagesControls Chapter Revision Questions AnswersNivneth PeirisNo ratings yet

- Accounts and AuditingDocument344 pagesAccounts and AuditingManisha Gupta100% (1)

- 8 MCQ - Overview of Risk-Based Audit ProcessDocument1 page8 MCQ - Overview of Risk-Based Audit ProcessRaisa LidasanNo ratings yet

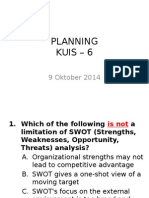

- Planning Kuis - 6: 9 Oktober 2014Document11 pagesPlanning Kuis - 6: 9 Oktober 2014Tito YustiawanNo ratings yet

- Aud Theory Comprehensive Self Review Quizzer MC PDFDocument20 pagesAud Theory Comprehensive Self Review Quizzer MC PDFZi VillarNo ratings yet

- Questioning Tool: Bookkeeping Nciii Page 1 of 1Document1 pageQuestioning Tool: Bookkeeping Nciii Page 1 of 1Roy SumugatNo ratings yet

- Week 6 (Non-Assurance & Related Services, Code of Ethics)Document33 pagesWeek 6 (Non-Assurance & Related Services, Code of Ethics)Beef Testosterone100% (1)

- Government An Management Audit ReportDocument8 pagesGovernment An Management Audit ReportLes ShinNo ratings yet

- VILLANUEVA Clarissa Micah ACTIVITY 12 02 22Document5 pagesVILLANUEVA Clarissa Micah ACTIVITY 12 02 22Clarissa Micah VillanuevaNo ratings yet

- Coop InstrumentDocument14 pagesCoop InstrumentJohn Wesley PascualNo ratings yet

- Câu hỏi Revision KTTKC 1 - CLCDocument3 pagesCâu hỏi Revision KTTKC 1 - CLC21Nguyễn Hương GiangNo ratings yet

- 13 - Chapter 07 - Change in Page 2 of 21 (1st Slide)Document21 pages13 - Chapter 07 - Change in Page 2 of 21 (1st Slide)nwohapeterNo ratings yet

- Govt MGT Audit Report TemplateDocument7 pagesGovt MGT Audit Report TemplateRheneir Mora100% (3)

- At.3218 - The Auditor S ReportDocument13 pagesAt.3218 - The Auditor S ReportDenny June CraususNo ratings yet

- Organizational Assessment Form: Session GuidesDocument5 pagesOrganizational Assessment Form: Session GuidesVen Daniel SuperableNo ratings yet

- Test 1 - Acc407 - Mar-Aug 2022 (Question)Document6 pagesTest 1 - Acc407 - Mar-Aug 2022 (Question)sabbyNo ratings yet

- Question Bank 2020 Auditing: Yr Sem 4 (Hons)Document21 pagesQuestion Bank 2020 Auditing: Yr Sem 4 (Hons)roaa ghanimNo ratings yet

- Ethical Obligations and Decision Making in Accounting Text and Cases 3Rd Edition Mintz Test Bank Full Chapter PDFDocument68 pagesEthical Obligations and Decision Making in Accounting Text and Cases 3Rd Edition Mintz Test Bank Full Chapter PDFSoniaLeecfab100% (11)

- C11 Audit Question BankDocument32 pagesC11 Audit Question Banksanjeevcnb888No ratings yet

- Questioning ToolDocument1 pageQuestioning ToolJanet PangulimaNo ratings yet

- Review CompleteDocument4 pagesReview CompleteMoeer razaNo ratings yet

- Questionnaire 2Document5 pagesQuestionnaire 2Riddhi PatelNo ratings yet

- Fundamentals of Auditing (ACC311) Quiz # 01Document3 pagesFundamentals of Auditing (ACC311) Quiz # 01MuddasirNo ratings yet

- BA2 PT Unit Test - 01 QuestionsDocument2 pagesBA2 PT Unit Test - 01 QuestionsSanjeev JayaratnaNo ratings yet

- 2 B IBM PMS TemplateDocument6 pages2 B IBM PMS TemplateAseem TyagiNo ratings yet

- Anglais 3 6 01 01Document6 pagesAnglais 3 6 01 01lb. zinouNo ratings yet

- 4 Notes - Audit Objectives and DocumentationDocument8 pages4 Notes - Audit Objectives and DocumentationFlor MorenoNo ratings yet

- Performance Appraisal For Admin OfficerDocument5 pagesPerformance Appraisal For Admin OfficerKaisar MukadamNo ratings yet

- AAA - TestDocument2 pagesAAA - Testakhil.ng6No ratings yet

- Annual Report Tool UpdatedDocument18 pagesAnnual Report Tool UpdatedShiv AnshuNo ratings yet

- Check List With Header ExamplesDocument4 pagesCheck List With Header ExamplesGovind BishtNo ratings yet

- Wa0001Document165 pagesWa0001Rishu SinghNo ratings yet

- F8 Sec E Chapter From 18-19Document11 pagesF8 Sec E Chapter From 18-19binodbhattarai350No ratings yet

- Digital Government Excellence: Lessons from Effective Digital LeadersFrom EverandDigital Government Excellence: Lessons from Effective Digital LeadersNo ratings yet

- Evidence (CH4+11)Document7 pagesEvidence (CH4+11)Md. Milon ChowdhuryNo ratings yet

- Question Pattern Summary For StudentsDocument15 pagesQuestion Pattern Summary For StudentsMd. Milon ChowdhuryNo ratings yet

- Documentation (CH10) : Hand NoteDocument9 pagesDocumentation (CH10) : Hand NoteMd. Milon ChowdhuryNo ratings yet

- Caat (CH 11)Document2 pagesCaat (CH 11)Md. Milon ChowdhuryNo ratings yet

- Assertions (CH4) : Hand NoteDocument2 pagesAssertions (CH4) : Hand NoteMd. Milon ChowdhuryNo ratings yet

- Obtaining An Engagement (CH2)Document7 pagesObtaining An Engagement (CH2)Md. Milon ChowdhuryNo ratings yet

- Planning The Assignment (CH 3)Document17 pagesPlanning The Assignment (CH 3)Md. Milon ChowdhuryNo ratings yet

- 2016 IIASB Standards Exposure DispositionDocument77 pages2016 IIASB Standards Exposure DispositionMd. Milon ChowdhuryNo ratings yet

- Expectation Gap (CH 1+4)Document2 pagesExpectation Gap (CH 1+4)Md. Milon ChowdhuryNo ratings yet

- Analytical Procudure (CH 3+11)Document6 pagesAnalytical Procudure (CH 3+11)Md. Milon ChowdhuryNo ratings yet

- Concept and Need For Assurance (CH1)Document16 pagesConcept and Need For Assurance (CH1)Md. Milon ChowdhuryNo ratings yet

- Proposed Enhancements To IPPF-August 2014Document26 pagesProposed Enhancements To IPPF-August 2014Md. Milon ChowdhuryNo ratings yet