You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5820)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Certificate of Employers Liability and Goods in Transit InsuranceDocument2 pagesCertificate of Employers Liability and Goods in Transit InsuranceMadiu Lakaran Severe BaldeNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Structural Defects Reference Manual For Low Rise BuildingsDocument295 pagesStructural Defects Reference Manual For Low Rise BuildingsvNo ratings yet

- Cumballa Hill Management Contract 27 July 18Document20 pagesCumballa Hill Management Contract 27 July 18naina vyasNo ratings yet

- Tax Gap: Corporate Income Tax Liability For Tax Year 2016Document1 pageTax Gap: Corporate Income Tax Liability For Tax Year 2016LokiNo ratings yet

- Food - The GuardianDocument7 pagesFood - The GuardianLoki100% (1)

- Scs 3Document8 pagesScs 3LokiNo ratings yet

- Social Insurance: Social Security and MedicareDocument26 pagesSocial Insurance: Social Security and MedicareLokiNo ratings yet

- Culture - The GuardianDocument8 pagesCulture - The GuardianLokiNo ratings yet

- 2019 Country Reports On Human Rights Practices - United States Department of StateDocument10 pages2019 Country Reports On Human Rights Practices - United States Department of StateLokiNo ratings yet

- Largest Income Tax Expenditures As of September 30, 2019Document2 pagesLargest Income Tax Expenditures As of September 30, 2019LokiNo ratings yet

- Language Learning With Free PodcastsDocument3 pagesLanguage Learning With Free PodcastsLokiNo ratings yet

- Unmatched Transactions and Balances: Restated Fiscal Year Fiscal Year 2019 2018Document1 pageUnmatched Transactions and Balances: Restated Fiscal Year Fiscal Year 2019 2018LokiNo ratings yet

- Note 23. Long-Term Fiscal ProjectionsDocument6 pagesNote 23. Long-Term Fiscal ProjectionsLokiNo ratings yet

- Tax Assessments: Required Supplementary Information (Unaudited) 208Document1 pageTax Assessments: Required Supplementary Information (Unaudited) 208LokiNo ratings yet

- Notes To The Financial Statements27Document1 pageNotes To The Financial Statements27LokiNo ratings yet

- United States Government Other Information (Unaudited) For The Years Ended September 30, 2019, and 2018Document2 pagesUnited States Government Other Information (Unaudited) For The Years Ended September 30, 2019, and 2018LokiNo ratings yet

- Notes To The Financial Statements26 PDFDocument1 pageNotes To The Financial Statements26 PDFLokiNo ratings yet

- Deferred Maintenance and RepairsDocument1 pageDeferred Maintenance and RepairsLokiNo ratings yet

- Note 24. Stewardship Land and Heritage Assets: 161 Notes To The Financial StatementsDocument1 pageNote 24. Stewardship Land and Heritage Assets: 161 Notes To The Financial StatementsLokiNo ratings yet

- Sustainability of Fiscal PolicyDocument11 pagesSustainability of Fiscal PolicyLokiNo ratings yet

- Note 19. Commitments: Long-Term Operating Leases As of September 30, 2019, and 2018Document3 pagesNote 19. Commitments: Long-Term Operating Leases As of September 30, 2019, and 2018LokiNo ratings yet

- Note 22. Social Insurance: 137 Notes To The Financial StatementsDocument18 pagesNote 22. Social Insurance: 137 Notes To The Financial StatementsLokiNo ratings yet

- Notes To The Financial Statements18Document7 pagesNotes To The Financial Statements18LokiNo ratings yet

- Note 25. Disclosure Entities and Related PartiesDocument5 pagesNote 25. Disclosure Entities and Related PartiesLokiNo ratings yet

- Note 21. Fiduciary Activities: Thrift Savings PlanDocument2 pagesNote 21. Fiduciary Activities: Thrift Savings PlanLokiNo ratings yet

- Note 17. Collections and Refunds of Federal RevenueDocument3 pagesNote 17. Collections and Refunds of Federal RevenueLokiNo ratings yet

- Notes To The Financial Statements14Document1 pageNotes To The Financial Statements14LokiNo ratings yet

- Notes To The Financial Statements16Document2 pagesNotes To The Financial Statements16LokiNo ratings yet

- Notes To The Financial Statements20Document6 pagesNotes To The Financial Statements20LokiNo ratings yet

- Note 11. Federal Debt Securities Held by The Public and Accrued InterestDocument4 pagesNote 11. Federal Debt Securities Held by The Public and Accrued InterestLokiNo ratings yet

- Note 15. Insurance and Guarantee Program LiabilitiesDocument2 pagesNote 15. Insurance and Guarantee Program LiabilitiesLokiNo ratings yet

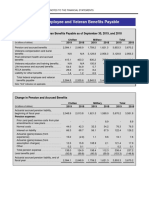

- Note 12. Federal Employee and Veteran Benefits PayableDocument10 pagesNote 12. Federal Employee and Veteran Benefits PayableLokiNo ratings yet

- Note 13. Environmental and Disposal LiabilitiesDocument2 pagesNote 13. Environmental and Disposal LiabilitiesLokiNo ratings yet

- Accounting For Non Proportional Treaties FinalDocument40 pagesAccounting For Non Proportional Treaties FinalGashaw100% (1)

- JapanDocument7 pagesJapanSandra RNo ratings yet

- Research On Impact of Covid On Life Insurance SectorDocument89 pagesResearch On Impact of Covid On Life Insurance SectorShivani KambliNo ratings yet

- It77 - Application For Registration As A Taxpayer or Changing of Registered Particulars Individual - External FormDocument6 pagesIt77 - Application For Registration As A Taxpayer or Changing of Registered Particulars Individual - External FormSamNo ratings yet

- Assignment of Insurance CargoDocument17 pagesAssignment of Insurance CargoKhairil Nazmi100% (1)

- Standalone Motor Own Damage Policy For Two WheelerDocument15 pagesStandalone Motor Own Damage Policy For Two WheelerAjith ChandranNo ratings yet

- Lori Has A Personal Umbrella Policy With A 1 MillionDocument1 pageLori Has A Personal Umbrella Policy With A 1 MillionAmit PandeyNo ratings yet

- Personal Budget ProjectDocument5 pagesPersonal Budget Projectapi-627175936No ratings yet

- B2B Assignment On Federated Insurance Case StudyDocument6 pagesB2B Assignment On Federated Insurance Case StudyJyoti PandeyNo ratings yet

- Examination: Subject SA1 Health and Care Specialist ApplicationsDocument168 pagesExamination: Subject SA1 Health and Care Specialist Applicationschan chadoNo ratings yet

- Blog Indo VS Blog BuleDocument5 pagesBlog Indo VS Blog BuleQustiyanNo ratings yet

- PNB V Welch, Fairchild - Co., Inc.Document11 pagesPNB V Welch, Fairchild - Co., Inc.Cathy BelgiraNo ratings yet

- Fine004 Test 1 2Document18 pagesFine004 Test 1 2Nageshwar SinghNo ratings yet

- State Life InsuranceDocument79 pagesState Life Insuranceqadirqadil100% (2)

- A. Agrarian Reform Cooperatives: PurposesDocument7 pagesA. Agrarian Reform Cooperatives: PurposesRosemarie Cruz100% (1)

- FireinsuranceDocument9 pagesFireinsurancesmit9993No ratings yet

- PolicyDocument3 pagesPolicyBahador HosseiniNo ratings yet

- Jay Ekbote FINAL PROJECT - HDFC ERGO Health InsuranceDocument71 pagesJay Ekbote FINAL PROJECT - HDFC ERGO Health InsuranceAditi SawantNo ratings yet

- Vita Student Management Limited: (If Applicable)Document11 pagesVita Student Management Limited: (If Applicable)hussah aldossaryNo ratings yet

- IC 38 Short Notes Chapter 2: Customer ServiceDocument10 pagesIC 38 Short Notes Chapter 2: Customer ServiceTaher BalasinorwalaNo ratings yet

- Topic 3 Chapter 9 Fundamental Legal PrinciplesDocument24 pagesTopic 3 Chapter 9 Fundamental Legal PrinciplesYu WenNo ratings yet

- 7 Sunlife Assurance Co of Canada V CA and Sps BacaniDocument3 pages7 Sunlife Assurance Co of Canada V CA and Sps BacaniGin FranciscoNo ratings yet

- Agency Code CSCSPV101/09 Agency Name CSC E Governance Services India Limited Agent's Contact No 9670102021 Contact Person Surjeet KumarDocument1 pageAgency Code CSCSPV101/09 Agency Name CSC E Governance Services India Limited Agent's Contact No 9670102021 Contact Person Surjeet KumarSUJEET KUMARNo ratings yet

- 27 Sps Nilo and Stella Cha V CADocument3 pages27 Sps Nilo and Stella Cha V CAJunNo ratings yet

- Social Security Administration Retirement, Survivors, and Disability InsuranceDocument12 pagesSocial Security Administration Retirement, Survivors, and Disability Insurancedsaer100% (1)

- Principles of Risk Management and Insurance 12Th Edition Rejda Test Bank Full Chapter PDFDocument34 pagesPrinciples of Risk Management and Insurance 12Th Edition Rejda Test Bank Full Chapter PDFJasonMoralesykcx100% (11)

- Mortgage IllustrationDocument7 pagesMortgage IllustrationMark JacksonNo ratings yet