You might also like

- Investments BKM - 9e SolutionsDocument246 pagesInvestments BKM - 9e SolutionsMichael Ong100% (3)

- Convertible Loan AgreementDocument7 pagesConvertible Loan AgreementPoonamNo ratings yet

- Housing & Government Sponsored Enterprises FY 2013 Congressional JustificationDocument13 pagesHousing & Government Sponsored Enterprises FY 2013 Congressional Justificationjoko-jacksNo ratings yet

- Case Study StockDocument3 pagesCase Study StockMatt INo ratings yet

- IAnthus Investor Presentation - October 2019 Investor DeckDocument29 pagesIAnthus Investor Presentation - October 2019 Investor DeckAnonymous fJAvrhj80JNo ratings yet

- Philippine Deposit Insurance Corporation Notes To Financial StatementsDocument31 pagesPhilippine Deposit Insurance Corporation Notes To Financial Statementsarellano lawschoolNo ratings yet

- Blackstone BREIT Notice To StockholdersDocument3 pagesBlackstone BREIT Notice To StockholdersZerohedgeNo ratings yet

- Notes To Financial Statements 2019Document103 pagesNotes To Financial Statements 2019LokiNo ratings yet

- NewMethodForGSE RiskTransfer-MalayBansalDocument10 pagesNewMethodForGSE RiskTransfer-MalayBansaldocs22No ratings yet

- Blueprint For Restoring Safety and Soundness To The GSEs November 2018Document32 pagesBlueprint For Restoring Safety and Soundness To The GSEs November 2018GSE Safety and SoundnessNo ratings yet

- 2007-08-07 COMMENTS ON RECENT MARKET SPECULATION REGARDING THE GSEs - Weekly Aug 7 2007Document4 pages2007-08-07 COMMENTS ON RECENT MARKET SPECULATION REGARDING THE GSEs - Weekly Aug 7 2007Joshua RosnerNo ratings yet

- Fy 2018 Midyear UpdateDocument388 pagesFy 2018 Midyear UpdateNick ReismanNo ratings yet

- The Cost of Government Financial Interventions, Past and PresentDocument6 pagesThe Cost of Government Financial Interventions, Past and Presentalex1521dfNo ratings yet

- Fy 19 Enac FPDocument440 pagesFy 19 Enac FPThe Capitol PressroomNo ratings yet

- Tab C (2 of 2) - Notes To Financial StatementsDocument29 pagesTab C (2 of 2) - Notes To Financial Statementsarellano lawschoolNo ratings yet

- Fourth Quarter 2019 Earnings PresentationDocument26 pagesFourth Quarter 2019 Earnings PresentationShambavaNo ratings yet

- United States Government Notes To The Financial Statements For The Fiscal Years Ended September 30, 2019, and 2018Document13 pagesUnited States Government Notes To The Financial Statements For The Fiscal Years Ended September 30, 2019, and 2018LokiNo ratings yet

- Qau 1203Document15 pagesQau 1203TBP_Think_TankNo ratings yet

- Portfolio Disposition FAQs Update 05-02-11 - FinalDocument7 pagesPortfolio Disposition FAQs Update 05-02-11 - Finaleav206No ratings yet

- 2013 q2 Crescent Commentary Steve RomickDocument16 pages2013 q2 Crescent Commentary Steve RomickCanadianValueNo ratings yet

- ALI 05-25 R23 ALI-Bonds-due-2025-Amended-Offer-Supplement-04212021Document320 pagesALI 05-25 R23 ALI-Bonds-due-2025-Amended-Offer-Supplement-04212021Ram CervantesNo ratings yet

- Note 23. Long-Term Fiscal ProjectionsDocument6 pagesNote 23. Long-Term Fiscal ProjectionsLokiNo ratings yet

- Carson Senate Banking Testimony 9-10-19Document8 pagesCarson Senate Banking Testimony 9-10-19Stephen LoiaconiNo ratings yet

- Accounting Standard 12Document11 pagesAccounting Standard 12api-3828505100% (1)

- Strengths, Credit Rating'Document7 pagesStrengths, Credit Rating'sammitNo ratings yet

- Financial - Accounting Assig 1bDocument10 pagesFinancial - Accounting Assig 1btumonekongo02No ratings yet

- Note 25. Disclosure Entities and Related PartiesDocument5 pagesNote 25. Disclosure Entities and Related PartiesLokiNo ratings yet

- FitchDocument9 pagesFitchTiso Blackstar Group100% (1)

- Finance Report - AusiDocument6 pagesFinance Report - AusiMichael NguriNo ratings yet

- GSAM Municipal Fixed Income SarDocument156 pagesGSAM Municipal Fixed Income Sarjoe1lee_1No ratings yet

- MODULE 2: Government Grants & Government AssistanceDocument2 pagesMODULE 2: Government Grants & Government AssistancePauline Joy GenalagonNo ratings yet

- 69240asb55316 As12Document9 pages69240asb55316 As12cheyam222No ratings yet

- (LGT) 20210316 - DRU - Sector RotationDocument3 pages(LGT) 20210316 - DRU - Sector RotationRuehYinn YapNo ratings yet

- 2008-10-08 TARP - Capital InfusionDocument6 pages2008-10-08 TARP - Capital InfusionJoshua RosnerNo ratings yet

- FINAL Joy Global Presentation For Investors 00793403xA26CA FinalDocument9 pagesFINAL Joy Global Presentation For Investors 00793403xA26CA FinalEdson MirandaNo ratings yet

- Background On: Insurance AccountingDocument5 pagesBackground On: Insurance AccountingSheena Doria de VeraNo ratings yet

- U.S. Mortgage Finance Reform Efforts and The Potential Credit ImplicationsDocument8 pagesU.S. Mortgage Finance Reform Efforts and The Potential Credit Implicationsapi-227433089No ratings yet

- Government SubsidiesDocument6 pagesGovernment Subsidiessamy7541No ratings yet

- Financial Supplement Q2 2011Document30 pagesFinancial Supplement Q2 2011Patricia bNo ratings yet

- Note 21. Fiduciary Activities: Thrift Savings PlanDocument2 pagesNote 21. Fiduciary Activities: Thrift Savings PlanLokiNo ratings yet

- Notes To The Financial Statements9Document1 pageNotes To The Financial Statements9LokiNo ratings yet

- Sensitive/Pre-Decisional: Department of The Treasury WASHINGTON, D.C. 20220Document8 pagesSensitive/Pre-Decisional: Department of The Treasury WASHINGTON, D.C. 20220api-261468864No ratings yet

- Accounting For Borrowing Cost and Government GrantDocument4 pagesAccounting For Borrowing Cost and Government GrantMaureen Derial PantaNo ratings yet

- Fair Valuation of Residential Whole Loans: Jay Guo, PH.D Interactive Data Corporation May 2011Document4 pagesFair Valuation of Residential Whole Loans: Jay Guo, PH.D Interactive Data Corporation May 2011bigposerNo ratings yet

- Accounting For Govt GrantsDocument20 pagesAccounting For Govt GrantsSaisanthosh Kumar SharmaNo ratings yet

- Muni Rally May Continue, But Must Navigate Policy RisksDocument3 pagesMuni Rally May Continue, But Must Navigate Policy RisksPutnam InvestmentsNo ratings yet

- Government Securities MarketDocument47 pagesGovernment Securities MarketArjit AgrawalNo ratings yet

- Investment and Financing Constrainst:: 1 CommentsDocument6 pagesInvestment and Financing Constrainst:: 1 CommentsCristina TessariNo ratings yet

- Moody's On ChinaDocument9 pagesMoody's On ChinaTim MooreNo ratings yet

- GT Capital: Up To P12B Bond IssueDocument457 pagesGT Capital: Up To P12B Bond IssueBusinessWorldNo ratings yet

- The Impact of COVID-19 On Alternative Assets: Investment ImplicationsDocument6 pagesThe Impact of COVID-19 On Alternative Assets: Investment ImplicationsAndres Torres0% (1)

- Unit 3 NFPDocument15 pagesUnit 3 NFPAbdii DhufeeraNo ratings yet

- Global Financial Crisis ReportDocument11 pagesGlobal Financial Crisis ReportRONNY WINGANo ratings yet

- International Accounting Standard 20 Accounting For Government Grants and Disclosure of Government AssistanceDocument7 pagesInternational Accounting Standard 20 Accounting For Government Grants and Disclosure of Government AssistanceParisNo ratings yet

- The $5 Trillion Question: What Should We Do With Fannie Mae and Freddie Mac?Document6 pagesThe $5 Trillion Question: What Should We Do With Fannie Mae and Freddie Mac?Lani RosalesNo ratings yet

- Housing Finance 0Document67 pagesHousing Finance 0AdminAliNo ratings yet

- RRMS Market Insights: Editor's NoteDocument5 pagesRRMS Market Insights: Editor's NoteRobert PardesNo ratings yet

- Policyholder Information Statement On Shenandoah Life Insurance Co.Document42 pagesPolicyholder Information Statement On Shenandoah Life Insurance Co.The Roanoke Times100% (1)

- Rating Action Moodys Downgrades Surinames Rating To Caa3 Maintains Negative Outlook 07jul20Document6 pagesRating Action Moodys Downgrades Surinames Rating To Caa3 Maintains Negative Outlook 07jul20Suriname MirrorNo ratings yet

- Government SecuritiesDocument31 pagesGovernment Securitiesshranil-k-shah-7086100% (1)

- Budget of the U.S. Government: A New Foundation for American Greatness: Fiscal Year 2018From EverandBudget of the U.S. Government: A New Foundation for American Greatness: Fiscal Year 2018No ratings yet

- The effects of investment regulations on pension funds performance in BrazilFrom EverandThe effects of investment regulations on pension funds performance in BrazilNo ratings yet

- Scs 3Document8 pagesScs 3LokiNo ratings yet

- Food - The GuardianDocument7 pagesFood - The GuardianLoki100% (1)

- Culture - The GuardianDocument8 pagesCulture - The GuardianLokiNo ratings yet

- Language Learning With Free PodcastsDocument3 pagesLanguage Learning With Free PodcastsLokiNo ratings yet

- Unmatched Transactions and Balances: Restated Fiscal Year Fiscal Year 2019 2018Document1 pageUnmatched Transactions and Balances: Restated Fiscal Year Fiscal Year 2019 2018LokiNo ratings yet

- Notes To The Financial Statements27Document1 pageNotes To The Financial Statements27LokiNo ratings yet

- 2019 Country Reports On Human Rights Practices - United States Department of StateDocument10 pages2019 Country Reports On Human Rights Practices - United States Department of StateLokiNo ratings yet

- United States Government Other Information (Unaudited) For The Years Ended September 30, 2019, and 2018Document2 pagesUnited States Government Other Information (Unaudited) For The Years Ended September 30, 2019, and 2018LokiNo ratings yet

- Largest Income Tax Expenditures As of September 30, 2019Document2 pagesLargest Income Tax Expenditures As of September 30, 2019LokiNo ratings yet

- Tax Gap: Corporate Income Tax Liability For Tax Year 2016Document1 pageTax Gap: Corporate Income Tax Liability For Tax Year 2016LokiNo ratings yet

- Social Insurance: Social Security and MedicareDocument26 pagesSocial Insurance: Social Security and MedicareLokiNo ratings yet

- Sustainability of Fiscal PolicyDocument11 pagesSustainability of Fiscal PolicyLokiNo ratings yet

- Tax Assessments: Required Supplementary Information (Unaudited) 208Document1 pageTax Assessments: Required Supplementary Information (Unaudited) 208LokiNo ratings yet

- Note 25. Disclosure Entities and Related PartiesDocument5 pagesNote 25. Disclosure Entities and Related PartiesLokiNo ratings yet

- Note 21. Fiduciary Activities: Thrift Savings PlanDocument2 pagesNote 21. Fiduciary Activities: Thrift Savings PlanLokiNo ratings yet

- Deferred Maintenance and RepairsDocument1 pageDeferred Maintenance and RepairsLokiNo ratings yet

- Notes To The Financial Statements26 PDFDocument1 pageNotes To The Financial Statements26 PDFLokiNo ratings yet

- Note 23. Long-Term Fiscal ProjectionsDocument6 pagesNote 23. Long-Term Fiscal ProjectionsLokiNo ratings yet

- Note 24. Stewardship Land and Heritage Assets: 161 Notes To The Financial StatementsDocument1 pageNote 24. Stewardship Land and Heritage Assets: 161 Notes To The Financial StatementsLokiNo ratings yet

- Note 17. Collections and Refunds of Federal RevenueDocument3 pagesNote 17. Collections and Refunds of Federal RevenueLokiNo ratings yet

- Notes To The Financial Statements20Document6 pagesNotes To The Financial Statements20LokiNo ratings yet

- Note 22. Social Insurance: 137 Notes To The Financial StatementsDocument18 pagesNote 22. Social Insurance: 137 Notes To The Financial StatementsLokiNo ratings yet

- Notes To The Financial Statements18Document7 pagesNotes To The Financial Statements18LokiNo ratings yet

- Notes To The Financial Statements16Document2 pagesNotes To The Financial Statements16LokiNo ratings yet

- Note 19. Commitments: Long-Term Operating Leases As of September 30, 2019, and 2018Document3 pagesNote 19. Commitments: Long-Term Operating Leases As of September 30, 2019, and 2018LokiNo ratings yet

- Note 15. Insurance and Guarantee Program LiabilitiesDocument2 pagesNote 15. Insurance and Guarantee Program LiabilitiesLokiNo ratings yet

- Notes To The Financial Statements14Document1 pageNotes To The Financial Statements14LokiNo ratings yet

- Note 13. Environmental and Disposal LiabilitiesDocument2 pagesNote 13. Environmental and Disposal LiabilitiesLokiNo ratings yet

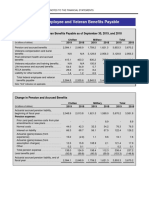

- Note 12. Federal Employee and Veteran Benefits PayableDocument10 pagesNote 12. Federal Employee and Veteran Benefits PayableLokiNo ratings yet

- Note 11. Federal Debt Securities Held by The Public and Accrued InterestDocument4 pagesNote 11. Federal Debt Securities Held by The Public and Accrued InterestLokiNo ratings yet

- Unit-Iii Fundamental AnalysisDocument36 pagesUnit-Iii Fundamental Analysisharesh KNo ratings yet

- Mba 4 Sem (Umang Rajput)Document20 pagesMba 4 Sem (Umang Rajput)Umang RajputNo ratings yet

- Black BookDocument43 pagesBlack Booknedexed404No ratings yet

- PercentDocument24 pagesPercentmidas66No ratings yet

- 2,3,4 Ir Uzd PDFDocument31 pages2,3,4 Ir Uzd PDFLeonid LeoNo ratings yet

- 03 04 Analysis Financial StatementDocument216 pages03 04 Analysis Financial StatementShanique Y. Harnett100% (1)

- Security Analysis & Portfolio Management - 1Document4 pagesSecurity Analysis & Portfolio Management - 1api-3745584No ratings yet

- DP 25537Document293 pagesDP 25537Antonio LopezNo ratings yet

- Capital MarketDocument14 pagesCapital MarketAnmol GuptaNo ratings yet

- Debre Markos Universty College of Post-Graduate Studies Department of Accounting and FinanceDocument14 pagesDebre Markos Universty College of Post-Graduate Studies Department of Accounting and FinanceMikias DegwaleNo ratings yet

- Phillip Nova 2H2023 Market OutlookDocument29 pagesPhillip Nova 2H2023 Market OutlookSteven TimNo ratings yet

- Chapter 7Document21 pagesChapter 7TACIPIT, Rowena Marie DizonNo ratings yet

- Chapter 1: The Investment Environment: Problem SetsDocument5 pagesChapter 1: The Investment Environment: Problem SetsGrant LiNo ratings yet

- Iaet and Tax-Exempt CorporationsDocument12 pagesIaet and Tax-Exempt Corporationsandrea ibanezNo ratings yet

- 9QDEHY - 2019 Tesla Inc Press Release Annual Report - JGVR0PDocument232 pages9QDEHY - 2019 Tesla Inc Press Release Annual Report - JGVR0PHarshNo ratings yet

- Lesson 7 Bull Call SpreadDocument14 pagesLesson 7 Bull Call Spreadadms100% (3)

- Certificate of Final Tax Withheld at Source: Faye and Sam General MerchandiseDocument4 pagesCertificate of Final Tax Withheld at Source: Faye and Sam General MerchandiseMay MayNo ratings yet

- Crescent Star Insurance LimitedDocument5 pagesCrescent Star Insurance LimitedlordraiNo ratings yet

- DuPont Public WP 2015 - 02.11.15Document78 pagesDuPont Public WP 2015 - 02.11.15marketfolly.comNo ratings yet

- Annual Report FinalDocument192 pagesAnnual Report Finalprashanthfeb90No ratings yet

- Bonus IssueDocument11 pagesBonus IssueRiya NitharwalNo ratings yet

- EFAMA AssetManagementReport2019Document15 pagesEFAMA AssetManagementReport2019CHUMBNo ratings yet

- Canadian Preferred Shares Yield TablesDocument29 pagesCanadian Preferred Shares Yield TablesrblaisNo ratings yet

- IDirect GladiatorStocks LIC March24Document9 pagesIDirect GladiatorStocks LIC March24ptus nayakNo ratings yet

- A Comparative Analysis On The Shareholder Value of Saint and Sin StocksDocument43 pagesA Comparative Analysis On The Shareholder Value of Saint and Sin StocksKarla Eunice Aquino ChanNo ratings yet

- Diglog07 15Document15 pagesDiglog07 15iftiniaziNo ratings yet

- Managerial Economics: Applications, Strategy, and Tactics, 10 EditionDocument18 pagesManagerial Economics: Applications, Strategy, and Tactics, 10 EditionMoshNo ratings yet

- CA IPCC New Accounts Question Paper Nov 2018 StudycafeDocument12 pagesCA IPCC New Accounts Question Paper Nov 2018 Studycafeshrey goelNo ratings yet