Download as docx, pdf, or txt

You might also like

- Cfa Chapter 9 Problems: The Capital Asset Pricing ModelDocument7 pagesCfa Chapter 9 Problems: The Capital Asset Pricing ModelFagbola Oluwatobi Omolaja100% (1)

- Chapter 8 Risk and Return PresentationDocument29 pagesChapter 8 Risk and Return PresentationsarmadNo ratings yet

- Chapter 07Document34 pagesChapter 07Lea WehbeNo ratings yet

- Chap 7 End of Chap SolDocument13 pagesChap 7 End of Chap SolWan Chee100% (1)

- Summer Internship Project Working Capital Finance From BankDocument33 pagesSummer Internship Project Working Capital Finance From Bankpranjali shindeNo ratings yet

- The Year End Balance Sheet of Manor Inc Includes The FollowingDocument1 pageThe Year End Balance Sheet of Manor Inc Includes The FollowingAmit PandeyNo ratings yet

- D - Tutorial 7 (Solutions)Document10 pagesD - Tutorial 7 (Solutions)AlfieNo ratings yet

- Seminar QuestionsDocument35 pagesSeminar QuestionsDaniel SanchezNo ratings yet

- FINM2411 F S 1, 2020 Q 1 (2) : Inal Exam Solution Emester Uestion MarksDocument7 pagesFINM2411 F S 1, 2020 Q 1 (2) : Inal Exam Solution Emester Uestion MarksTullyNo ratings yet

- Assignment 5 AnswersDocument5 pagesAssignment 5 AnswersLionButtNo ratings yet

- FM 8th Edition Chapter 12 - Risk and ReturnDocument20 pagesFM 8th Edition Chapter 12 - Risk and ReturnKa Io ChaoNo ratings yet

- Tutorial 4Document10 pagesTutorial 4Yaonik HimmatramkaNo ratings yet

- CAPM Recap Exercises 2023 SolutionDocument15 pagesCAPM Recap Exercises 2023 SolutionMirela KafalievaNo ratings yet

- Chapter 9 - SolutionsDocument53 pagesChapter 9 - SolutionsLILYANo ratings yet

- PS 2Document6 pagesPS 2WristWork EntertainmentNo ratings yet

- Exercises Chapter 4 - Part II With SolutionsDocument6 pagesExercises Chapter 4 - Part II With SolutionsDiana AzevedoNo ratings yet

- Risk & Return: Risk of A Portfolio-Uncertainty Main View Two AspectsDocument36 pagesRisk & Return: Risk of A Portfolio-Uncertainty Main View Two AspectsAminul Islam AmuNo ratings yet

- Techniques For Portfolio MGT TUTORIAL QSNDocument2 pagesTechniques For Portfolio MGT TUTORIAL QSNkelvinyessa906No ratings yet

- Tarea 7 Finanzas CorpDocument12 pagesTarea 7 Finanzas Corpvuzo123No ratings yet

- #12 - Measuring Risk BETADocument2 pages#12 - Measuring Risk BETAMarieNo ratings yet

- R 30% Inflation Rate 15% R (1+R) - 1 (1+I)Document23 pagesR 30% Inflation Rate 15% R (1+R) - 1 (1+I)Adi SadiNo ratings yet

- FM Handout 2Document29 pagesFM Handout 2Rofiq VedcNo ratings yet

- All Your Answers Should Be On An Excel Sheet. Show Your Calculation Process.Document6 pagesAll Your Answers Should Be On An Excel Sheet. Show Your Calculation Process.Adi SadiNo ratings yet

- Jhones and Jhones, Where You're Employed. Meanwhile The Young Beneficiaries Were Very Eager To KnowDocument5 pagesJhones and Jhones, Where You're Employed. Meanwhile The Young Beneficiaries Were Very Eager To KnowUmairSadiqNo ratings yet

- Essentials of Investments 10th Edition Bodie Solutions Manual DownloadDocument14 pagesEssentials of Investments 10th Edition Bodie Solutions Manual DownloadJennifer Walker100% (21)

- There Are 20 Questions in This Part. Please Choose ONE Answer For Each Question. Each Question Is Worth 0.2 PointsDocument8 pagesThere Are 20 Questions in This Part. Please Choose ONE Answer For Each Question. Each Question Is Worth 0.2 PointsThảo Như Trần NgọcNo ratings yet

- Lectures 5 & 7 - Hard Exercises - Attempt ReviewDocument11 pagesLectures 5 & 7 - Hard Exercises - Attempt ReviewHeidi DaoNo ratings yet

- Chapter 7 Risk, Return, and The Capital Asset Pricing Model: AWS Cloud Security RisksDocument18 pagesChapter 7 Risk, Return, and The Capital Asset Pricing Model: AWS Cloud Security RisksPauline Tracy BatilesNo ratings yet

- CH 9Document14 pagesCH 9joshua arnettNo ratings yet

- Risk and Return Hand OutDocument4 pagesRisk and Return Hand OutAsad ur rahmanNo ratings yet

- Fin33 2nd NewDocument2 pagesFin33 2nd NewRonieOlarteNo ratings yet

- CAPM by Yurii V HavryliukDocument28 pagesCAPM by Yurii V HavryliukyuriihavryliukNo ratings yet

- Module - 4 Problem On Portfolio Risk & Return-IIDocument4 pagesModule - 4 Problem On Portfolio Risk & Return-IIgaurav supadeNo ratings yet

- Tutorial Risk & ReturnDocument3 pagesTutorial Risk & Returnna1504.workNo ratings yet

- Solution 1Document5 pagesSolution 1frq qqrNo ratings yet

- Ch24 ShowDocument46 pagesCh24 ShowMahmoud AbdullahNo ratings yet

- 13 Portofolio Risk and Return Part IIDocument6 pages13 Portofolio Risk and Return Part IIAditya NugrohoNo ratings yet

- Assigment 1& 2Document5 pagesAssigment 1& 2Mohd Arif Bin BasirNo ratings yet

- FIN 223 - Tutorials Answers Week 6Document15 pagesFIN 223 - Tutorials Answers Week 6Ann JoyNo ratings yet

- Topic 4Document26 pagesTopic 420070304 Nguyễn Thị PhươngNo ratings yet

- CML Vs SMLDocument9 pagesCML Vs SMLJoanna JacksonNo ratings yet

- Chap009 Test Bank (1) SolutionDocument16 pagesChap009 Test Bank (1) Solutionbaskarbaju1No ratings yet

- Capital Asset Pricing Model (CAPM)Document25 pagesCapital Asset Pricing Model (CAPM)ktkalai selviNo ratings yet

- Tybbi, Sapm 1Document1 pageTybbi, Sapm 1PraWin KharateNo ratings yet

- BCH 503 SM05Document14 pagesBCH 503 SM05sugandh bajajNo ratings yet

- MBA 4 Sem I M Unit IV Probs On Portfolio TheoryDocument5 pagesMBA 4 Sem I M Unit IV Probs On Portfolio TheoryMoheed UddinNo ratings yet

- Tutorial 9 & 10-Qs-2Document2 pagesTutorial 9 & 10-Qs-2YunesshwaaryNo ratings yet

- Risk and ReturnDocument3 pagesRisk and ReturnPiyush RathiNo ratings yet

- Investment and Portfolio AnalysisDocument24 pagesInvestment and Portfolio Analysis‘Alya Qistina Mohd ZaimNo ratings yet

- Q CH 9Document7 pagesQ CH 9Jhon F SinagaNo ratings yet

- Chapter 7-Risk, Return, and The Capital Asset Pricing ModelDocument18 pagesChapter 7-Risk, Return, and The Capital Asset Pricing Modelbaha146100% (1)

- FM11 CH 04 Mini-Case Old6Document19 pagesFM11 CH 04 Mini-Case Old6AGNo ratings yet

- SAPMDocument10 pagesSAPMadisontakke_31792263No ratings yet

- Section 03Document27 pagesSection 03HarshNo ratings yet

- Tutorial Risk & ReturnDocument3 pagesTutorial Risk & ReturnNhi Hoang100% (1)

- Lecture 9 - Risk and Return 2 - StuDocument24 pagesLecture 9 - Risk and Return 2 - StuJaydeNo ratings yet

- Chapter 3 FMDocument23 pagesChapter 3 FMeferemNo ratings yet

- IACFMAS-ASSIGN MarjDocument4 pagesIACFMAS-ASSIGN MarjMarjorie PagsinuhinNo ratings yet

- Beyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkFrom EverandBeyond Earnings: Applying the HOLT CFROI and Economic Profit FrameworkNo ratings yet

- Summer Internship ProjectDocument9 pagesSummer Internship Projectpranjali shindeNo ratings yet

- Swayam Siddhi College of Management and Research: Strategic Business Unit (SBU) Mms Sem 3Document9 pagesSwayam Siddhi College of Management and Research: Strategic Business Unit (SBU) Mms Sem 3pranjali shindeNo ratings yet

- Process Characteristics: Variety FlowDocument38 pagesProcess Characteristics: Variety Flowpranjali shindeNo ratings yet

- FR - Sebi Issue of Capital & Disclosure RequirementsDocument16 pagesFR - Sebi Issue of Capital & Disclosure Requirementspranjali shindeNo ratings yet

- Working Capital Finance For BankDocument10 pagesWorking Capital Finance For Bankpranjali shindeNo ratings yet

- Debtors Financing-Factoring: Swayam Siddhi College of MGMT & ResearchDocument15 pagesDebtors Financing-Factoring: Swayam Siddhi College of MGMT & Researchpranjali shindeNo ratings yet

- Offer From Firm ADocument11 pagesOffer From Firm Apranjali shindeNo ratings yet

- FR - IntroductionDocument11 pagesFR - Introductionpranjali shindeNo ratings yet

- Inventory ManagementDocument33 pagesInventory Managementpranjali shindeNo ratings yet

- Material Requirement Planning PPTDocument19 pagesMaterial Requirement Planning PPTpranjali shindeNo ratings yet

- New Doc 2019-10-31 14.29.54Document39 pagesNew Doc 2019-10-31 14.29.54pranjali shindeNo ratings yet

- Facility Location: Operations ManagementDocument41 pagesFacility Location: Operations Managementpranjali shindeNo ratings yet

- Scanned With CamscannerDocument16 pagesScanned With Camscannerpranjali shindeNo ratings yet

- OMScheduling PPTDocument38 pagesOMScheduling PPTpranjali shindeNo ratings yet

- Quality2 SixSigmaControlChartsDocument40 pagesQuality2 SixSigmaControlChartspranjali shindeNo ratings yet

- Definitions of IT: Types of Information SystemDocument31 pagesDefinitions of IT: Types of Information Systempranjali shindeNo ratings yet

- Deferred Tax and Business Combinations: IFRS 3/IAS 12Document15 pagesDeferred Tax and Business Combinations: IFRS 3/IAS 12direhitNo ratings yet

- UGBA103 Final Fall 2016Document5 pagesUGBA103 Final Fall 2016Billy bobNo ratings yet

- HTTP Hubcap - Clemson.edu Kleinr 402 CHAPTER25Document68 pagesHTTP Hubcap - Clemson.edu Kleinr 402 CHAPTER25Jaesoon ParkNo ratings yet

- YPF Repsol CaseDocument30 pagesYPF Repsol CaseVijoyShankarRoyNo ratings yet

- The John Molson School of Business MBA 607 Final Exam June 2013 (100 MARKS)Document10 pagesThe John Molson School of Business MBA 607 Final Exam June 2013 (100 MARKS)aicellNo ratings yet

- Bonds Overview Pricing YieldDocument40 pagesBonds Overview Pricing YieldRajesh Chowdary Chintamaneni100% (1)

- A Tale of Two TradersDocument4 pagesA Tale of Two Tradersmayankjain24inNo ratings yet

- Stock Acquisition DOADocument9 pagesStock Acquisition DOAShekinah Grace SantuaNo ratings yet

- Costing and Pricing - 02 - Activity - 1Document1 pageCosting and Pricing - 02 - Activity - 1JERMAINE APRIL LAGURASNo ratings yet

- EntrepreneurshipDocument15 pagesEntrepreneurshipiNo ratings yet

- Go Rural FM AssignmentDocument31 pagesGo Rural FM AssignmentHumphrey OsaigbeNo ratings yet

- Blockbuster Video (BBI) : Postmortem: Ellen CarrDocument8 pagesBlockbuster Video (BBI) : Postmortem: Ellen Carrmweng407No ratings yet

- Actividad7.4 A01323445Document9 pagesActividad7.4 A01323445Estefanía ZavalaNo ratings yet

- Syllabus Sem 4Document3 pagesSyllabus Sem 4Anjali Gidwani67% (3)

- BBA in Financial Markets-Joint Programme by NSE Academy and GITAM, VisakhapatnamDocument1 pageBBA in Financial Markets-Joint Programme by NSE Academy and GITAM, VisakhapatnamsajidNo ratings yet

- Applied Corporate FinanceDocument88 pagesApplied Corporate Financedu_ha_1No ratings yet

- Summer Intern Project Submitted By: Manindra Konda IIM Calcutta (PGP 2014 - 2016)Document23 pagesSummer Intern Project Submitted By: Manindra Konda IIM Calcutta (PGP 2014 - 2016)manindra1kondaNo ratings yet

- Tax Evasion Through SharesDocument5 pagesTax Evasion Through SharesPrashant Thakur100% (1)

- Banking & Wealth Management BootcampDocument6 pagesBanking & Wealth Management BootcampVidita MehtaNo ratings yet

- Karnataka Board Class 12 Accountancy Question & Answer Paper March 2012Document14 pagesKarnataka Board Class 12 Accountancy Question & Answer Paper March 2012arunmuniswamy2522No ratings yet

- GRC Job Order Costing ModuleDocument14 pagesGRC Job Order Costing ModuleKirk EscanillaNo ratings yet

- TM1 Slides 202324Document49 pagesTM1 Slides 202324serepasfNo ratings yet

- The Playing Field - Graham Duncan - MediumDocument11 pagesThe Playing Field - Graham Duncan - MediumPradeep RaghunathanNo ratings yet

- Indian School Muscat: Page - 1 - of 7Document7 pagesIndian School Muscat: Page - 1 - of 7Devansh AsawaNo ratings yet

- ACCTG + PRELIM Activity With Key Answers (Lesson 1.1-1.4)Document7 pagesACCTG + PRELIM Activity With Key Answers (Lesson 1.1-1.4)NEIL OBINARIONo ratings yet

- Equity Share and Its TypesDocument4 pagesEquity Share and Its TypeslakshmibabymaniNo ratings yet

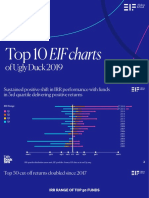

- EIF Ugly DuckDocument11 pagesEIF Ugly DuckJoao DuarteNo ratings yet

- Financial ManagementDocument171 pagesFinancial ManagementNasr MohammedNo ratings yet

- Balance Sheet Equation Assets Liabilities + Stockholders' EquityDocument7 pagesBalance Sheet Equation Assets Liabilities + Stockholders' EquityAsma RizviNo ratings yet