Download as xls, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5820)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- AgriPinay Simple Business PlanDocument6 pagesAgriPinay Simple Business PlanKristy Dela PeñaNo ratings yet

- Fini 619 Internship Report On Iqbal Rice MillsDocument43 pagesFini 619 Internship Report On Iqbal Rice MillsRohit Singh100% (1)

- A Review of The Theoretical and Empirical Basis of Financial Ratio AnalysisDocument36 pagesA Review of The Theoretical and Empirical Basis of Financial Ratio AnalysisMohammed Ali Askar100% (4)

- Kotak Mahindra Bank Performance AnalysisDocument18 pagesKotak Mahindra Bank Performance AnalysisSurbhî GuptaNo ratings yet

- Marketing Channels For ServicesDocument24 pagesMarketing Channels For ServicesSurbhî GuptaNo ratings yet

- Electronic Marketing ChannelsDocument25 pagesElectronic Marketing ChannelsSurbhî GuptaNo ratings yet

- Samarth Mehrotra - BOCADocument23 pagesSamarth Mehrotra - BOCASurbhî GuptaNo ratings yet

- Boca Vinay pgfc1948 Icici BankDocument12 pagesBoca Vinay pgfc1948 Icici BankSurbhî GuptaNo ratings yet

- B.O.C.A Assignment - Vishal Singh - pgsf1951 - Performance AnalysisDocument14 pagesB.O.C.A Assignment - Vishal Singh - pgsf1951 - Performance AnalysisSurbhî GuptaNo ratings yet

- Shreeya Verma (PGSF1952)Document15 pagesShreeya Verma (PGSF1952)Surbhî GuptaNo ratings yet

- Bank Performance Analysis-INDUSIND BANK: Particulars Mar-16Document26 pagesBank Performance Analysis-INDUSIND BANK: Particulars Mar-16Surbhî GuptaNo ratings yet

- Shreya Jain - PGFC1935 - Performance AnalysisDocument13 pagesShreya Jain - PGFC1935 - Performance AnalysisSurbhî GuptaNo ratings yet

- YES Bank Performance AnalysisDocument11 pagesYES Bank Performance AnalysisSurbhî GuptaNo ratings yet

- Bank of India Performance Analysis: Total AssetsDocument6 pagesBank of India Performance Analysis: Total AssetsSurbhî GuptaNo ratings yet

- Performance Analysis - CbiDocument19 pagesPerformance Analysis - CbiSurbhî GuptaNo ratings yet

- Shashank Malik - PGFB1944 - BOCA GR2 - Study Group 4 - Central Bank of IndiaDocument13 pagesShashank Malik - PGFB1944 - BOCA GR2 - Study Group 4 - Central Bank of IndiaSurbhî GuptaNo ratings yet

- Axis Bank Ltd. Performance AnalysisDocument13 pagesAxis Bank Ltd. Performance AnalysisSurbhî GuptaNo ratings yet

- Bank Performance Analysis - Sahil Badaya PGFB1942Document10 pagesBank Performance Analysis - Sahil Badaya PGFB1942Surbhî GuptaNo ratings yet

- Nitesh Khandelwal (PGFC1921) - BOCA (Central Bank of India)Document12 pagesNitesh Khandelwal (PGFC1921) - BOCA (Central Bank of India)Surbhî GuptaNo ratings yet

- Satyam PGSF1937 BOCA BOI BADocument15 pagesSatyam PGSF1937 BOCA BOI BASurbhî GuptaNo ratings yet

- Bank Performance AnalysisDocument10 pagesBank Performance AnalysisSurbhî GuptaNo ratings yet

- Kotak Mahindra Bank Ltd. Performance Analysis For The Period 2016-2020Document15 pagesKotak Mahindra Bank Ltd. Performance Analysis For The Period 2016-2020Surbhî GuptaNo ratings yet

- Reshma Chauhan - PGFC1927 (BOCA)Document9 pagesReshma Chauhan - PGFC1927 (BOCA)Surbhî GuptaNo ratings yet

- Bank Performance Analysis With Risk RatiosDocument8 pagesBank Performance Analysis With Risk RatiosSurbhî GuptaNo ratings yet

- Rashi AggarwalDocument17 pagesRashi AggarwalSurbhî GuptaNo ratings yet

- Priya Bansal pgfc1924Document8 pagesPriya Bansal pgfc1924Surbhî GuptaNo ratings yet

- Bank Performance AnalysisDocument4 pagesBank Performance AnalysisSurbhî GuptaNo ratings yet

- Axis Bank Ltd. Performance AnalysisDocument11 pagesAxis Bank Ltd. Performance AnalysisSurbhî GuptaNo ratings yet

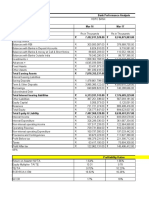

- IDFC First Bank LTD Performance Analysis: Total AssetsDocument9 pagesIDFC First Bank LTD Performance Analysis: Total AssetsSurbhî GuptaNo ratings yet

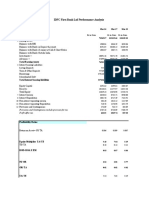

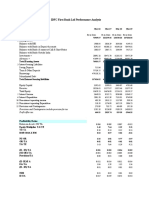

- IDFC First Bank LTD Performance Analysis: Total AssetsDocument6 pagesIDFC First Bank LTD Performance Analysis: Total AssetsSurbhî GuptaNo ratings yet

- Equities and Liabilities Shareholder'S Funds Mar-20 Mar-19 Total Share Capital 3,277.66 2,760.03Document11 pagesEquities and Liabilities Shareholder'S Funds Mar-20 Mar-19 Total Share Capital 3,277.66 2,760.03Surbhî GuptaNo ratings yet

- Provisions and Contingencies Include Provision For TaxDocument6 pagesProvisions and Contingencies Include Provision For TaxSurbhî GuptaNo ratings yet

- Assignment pgfc1913Document9 pagesAssignment pgfc1913Surbhî GuptaNo ratings yet

- Chapter-17 Bank Management - Lending To Business Firms and Pricing Business LoansDocument41 pagesChapter-17 Bank Management - Lending To Business Firms and Pricing Business Loanslmmh50% (2)

- PEC 1-Mohith .PPTX 123Document21 pagesPEC 1-Mohith .PPTX 123shekartacNo ratings yet

- MGT8200 - Chapter 3Document9 pagesMGT8200 - Chapter 3Si WongNo ratings yet

- Inari Amertron Berhad (0166)Document27 pagesInari Amertron Berhad (0166)Cindy TohNo ratings yet

- Q4 G11-ABM - L03 Analysis & Interpretation of Financial Statements PDFDocument50 pagesQ4 G11-ABM - L03 Analysis & Interpretation of Financial Statements PDFFatricia MedinaNo ratings yet

- Accounting Textbook Solutions - 43Document19 pagesAccounting Textbook Solutions - 43acc-expertNo ratings yet

- Thesis of BBS 4 Year - OriginalDocument42 pagesThesis of BBS 4 Year - Originalशुन्य बिशालNo ratings yet

- Review of Financial Statement Preparation Analysis and InterpretationDocument77 pagesReview of Financial Statement Preparation Analysis and InterpretationGray JavierNo ratings yet

- FINANCIAL ANALYSIS HDFC BankDocument112 pagesFINANCIAL ANALYSIS HDFC BankShivam SharmaNo ratings yet

- SS 11Document31 pagesSS 11Christopher MendozaNo ratings yet

- The Impact of Stock Market Listing On The Financial Performance of Companies Within The Rwanda Stock Exchange (RSE)Document20 pagesThe Impact of Stock Market Listing On The Financial Performance of Companies Within The Rwanda Stock Exchange (RSE)KIU PUBLICATION AND EXTENSIONNo ratings yet

- Chapter 4 Strategic ManagementDocument61 pagesChapter 4 Strategic ManagementHafsa KhanNo ratings yet

- This Study Resource Was: PROBLEM 1-8: Financial Statement Ratio AnalysisDocument4 pagesThis Study Resource Was: PROBLEM 1-8: Financial Statement Ratio AnalysisAbda IrsyaV3No ratings yet

- AccountDocument16 pagesAccountMohamad AlifNo ratings yet

- 2014 PGN Annual ReportDocument496 pages2014 PGN Annual ReportAndiAndaKacongNo ratings yet

- Publication 1 Seid MDocument9 pagesPublication 1 Seid Mseid100% (1)

- Starbucks Coffee Company Financial Analysis: Final Project Amanda N. Martin MBA 503: Financial Reporting and Analysis Dr. Uzell Freeman Southern New Hampshire University March 25, 2017Document18 pagesStarbucks Coffee Company Financial Analysis: Final Project Amanda N. Martin MBA 503: Financial Reporting and Analysis Dr. Uzell Freeman Southern New Hampshire University March 25, 2017Dennis KorirNo ratings yet

- Financial Reporting Week 4Document9 pagesFinancial Reporting Week 4islam hamdyNo ratings yet

- Salalah Mills Performance 1Document15 pagesSalalah Mills Performance 1پاکیزہ مسکانNo ratings yet

- Unit 4 Handouts - Bank Risk ManagementDocument5 pagesUnit 4 Handouts - Bank Risk ManagementmohamedNo ratings yet

- Strategic Management CH 4Document37 pagesStrategic Management CH 4karim kobeissiNo ratings yet

- Ib BM IaDocument19 pagesIb BM IaanirudhNo ratings yet

- Sonali BankDocument45 pagesSonali BankMohiuddin MuhinNo ratings yet

- Financial Statements and Ratio AnalysisDocument2 pagesFinancial Statements and Ratio AnalysisRyan MiguelNo ratings yet

- FM - 200 MCQDocument41 pagesFM - 200 MCQmangesh75% (12)

- Fabm2 q1 Mod5 Part-1-AnalysisDocument21 pagesFabm2 q1 Mod5 Part-1-AnalysisAmber Dela Cruz100% (2)

- Ratio Analysis FormulaDocument14 pagesRatio Analysis FormulaEmranul Islam ShovonNo ratings yet