Download as xls, pdf, or txt

You might also like

- A) Stock Performance of Ahold and Tesco Between Jan-2008 and Dec-2011Document4 pagesA) Stock Performance of Ahold and Tesco Between Jan-2008 and Dec-2011MANAV ROY100% (3)

- Case Study Colgate PalmoliveDocument6 pagesCase Study Colgate PalmoliveSWATHI KRISHNA M R100% (1)

- Schaum's Outline of Basic Business Mathematics, 2edFrom EverandSchaum's Outline of Basic Business Mathematics, 2edRating: 5 out of 5 stars5/5 (2)

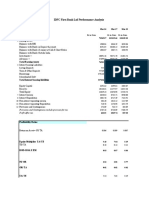

- IDFC First Bank LTD Performance Analysis: Total AssetsDocument9 pagesIDFC First Bank LTD Performance Analysis: Total AssetsSurbhî GuptaNo ratings yet

- Provisions and Contingencies Include Provision For TaxDocument6 pagesProvisions and Contingencies Include Provision For TaxSurbhî GuptaNo ratings yet

- Assignment On Ratio AnalysisDocument6 pagesAssignment On Ratio AnalysisSurbhî GuptaNo ratings yet

- Bank Performance Analysis With Risk RatiosDocument8 pagesBank Performance Analysis With Risk RatiosSurbhî GuptaNo ratings yet

- Bank Performance Analysis - Sahil Badaya PGFB1942Document10 pagesBank Performance Analysis - Sahil Badaya PGFB1942Surbhî GuptaNo ratings yet

- Bank Performance Analysis-INDUSIND BANK: Particulars Mar-16Document26 pagesBank Performance Analysis-INDUSIND BANK: Particulars Mar-16Surbhî GuptaNo ratings yet

- Ajanta Pharma LTD.: LiquidityDocument4 pagesAjanta Pharma LTD.: LiquidityDeepak DashNo ratings yet

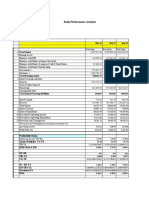

- Bank Performance AnalysisDocument4 pagesBank Performance AnalysisSurbhî GuptaNo ratings yet

- Atest Quarterly/Halfyearly As On (Months) : %OI %OI %OIDocument4 pagesAtest Quarterly/Halfyearly As On (Months) : %OI %OI %OIManas AnandNo ratings yet

- Reshma Chauhan - PGFC1927 (BOCA)Document9 pagesReshma Chauhan - PGFC1927 (BOCA)Surbhî GuptaNo ratings yet

- Boca Yes Bank PGFC 1904Document16 pagesBoca Yes Bank PGFC 1904Surbhî GuptaNo ratings yet

- Mar-19 Mar-18 Mar-17: Fixed Assets 1718.63 1317.69 1006.11Document17 pagesMar-19 Mar-18 Mar-17: Fixed Assets 1718.63 1317.69 1006.11PoorvaNo ratings yet

- Satyam PGSF1937 BOCA BOI BADocument15 pagesSatyam PGSF1937 BOCA BOI BASurbhî GuptaNo ratings yet

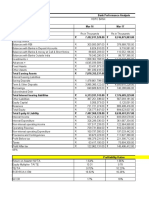

- Equities and Liabilities Shareholder'S Funds Mar-20 Mar-19 Total Share Capital 3,277.66 2,760.03Document11 pagesEquities and Liabilities Shareholder'S Funds Mar-20 Mar-19 Total Share Capital 3,277.66 2,760.03Surbhî GuptaNo ratings yet

- Shreya Jain - PGFC1935 - Performance AnalysisDocument13 pagesShreya Jain - PGFC1935 - Performance AnalysisSurbhî GuptaNo ratings yet

- Company Finance Profit & Loss Consolidated (Rs in CRS.)Document4 pagesCompany Finance Profit & Loss Consolidated (Rs in CRS.)rohanNo ratings yet

- Income Latest: Financials (Standalone)Document3 pagesIncome Latest: Financials (Standalone)Vishwavijay ThakurNo ratings yet

- Modi Rubber LimitedDocument10 pagesModi Rubber LimitedRohit BhatNo ratings yet

- YES Bank Performance AnalysisDocument11 pagesYES Bank Performance AnalysisSurbhî GuptaNo ratings yet

- Bank Performance AnalysisDocument10 pagesBank Performance AnalysisSurbhî GuptaNo ratings yet

- Ratio Analysis of Maruti Suzuki and M&MDocument5 pagesRatio Analysis of Maruti Suzuki and M&MkritiNo ratings yet

- Balance Sheet (2009-2003) of TCS (US Format)Document15 pagesBalance Sheet (2009-2003) of TCS (US Format)Girish RamachandraNo ratings yet

- DSP Merrill Lynch LTD Industry:Securities/Commodities Trading ServicesDocument8 pagesDSP Merrill Lynch LTD Industry:Securities/Commodities Trading Servicesapi-3699305No ratings yet

- Apollo Hospitals Enterprise LimitedDocument4 pagesApollo Hospitals Enterprise Limitedpaigesh1No ratings yet

- Balance Sheet: StandaloneDocument9 pagesBalance Sheet: StandaloneKabita BuragohainNo ratings yet

- Data For Dabur IndiaDocument4 pagesData For Dabur IndiaKarma MaharjanNo ratings yet

- Juhayna Food Industries: in Millions of EGP (Except For Per Share Items)Document11 pagesJuhayna Food Industries: in Millions of EGP (Except For Per Share Items)Shokry AminNo ratings yet

- Bank of India Performance Analysis: Total AssetsDocument6 pagesBank of India Performance Analysis: Total AssetsSurbhî GuptaNo ratings yet

- Dr. Sen's FFDocument16 pagesDr. Sen's FFnikhilluniaNo ratings yet

- BF Projects Ratio Analysis: Name Angshuman ChatterjeeDocument31 pagesBF Projects Ratio Analysis: Name Angshuman ChatterjeeAngshuman ChatterjeeNo ratings yet

- Standalone Financial Results, Limited Review Report For December 31, 2016 (Result)Document3 pagesStandalone Financial Results, Limited Review Report For December 31, 2016 (Result)Shyam SunderNo ratings yet

- VERTICAL LIABILITIES 1Document4 pagesVERTICAL LIABILITIES 1NL CastañaresNo ratings yet

- Cairns India Private LimitedDocument25 pagesCairns India Private LimitedSuruchi GoyalNo ratings yet

- Managerial Balance Sheet: Liabilities 2005-06 2006-07 2007-08 2008-09 2009-10Document10 pagesManagerial Balance Sheet: Liabilities 2005-06 2006-07 2007-08 2008-09 2009-10kirati_dalal2000No ratings yet

- (All Non-Ratios in Millions)Document13 pages(All Non-Ratios in Millions)Aninda DuttaNo ratings yet

- AccountDocument1 pageAccountjigopen219No ratings yet

- PVR LTD (PVRL IN) - StandardizedDocument18 pagesPVR LTD (PVRL IN) - StandardizedSrinidhi SrinathNo ratings yet

- Annexure: FINANCE - BALANCE SHEET - Bharti Airtel LTD (Curr: Rs in CR.)Document26 pagesAnnexure: FINANCE - BALANCE SHEET - Bharti Airtel LTD (Curr: Rs in CR.)Daman Deep Singh ArnejaNo ratings yet

- DLF Announces Annual Results For FY10: HistoryDocument7 pagesDLF Announces Annual Results For FY10: HistoryShalinee SinghNo ratings yet

- Financials SaharaDocument19 pagesFinancials SaharaJitendra NikhareNo ratings yet

- Arvind - Profit & Loss Account - Textiles - Denim - Profit & Loss Account of Arvind - BSE - 500101, NSE - ARVINDDocument2 pagesArvind - Profit & Loss Account - Textiles - Denim - Profit & Loss Account of Arvind - BSE - 500101, NSE - ARVINDAjay CharlesNo ratings yet

- Dalmia Cement (Bharat) LTDDocument8 pagesDalmia Cement (Bharat) LTDRemonNo ratings yet

- 18 - Nacchhater - Tata MotorsDocument17 pages18 - Nacchhater - Tata Motorsrajat_singlaNo ratings yet

- FM Cce2Document7 pagesFM Cce2shrutiNo ratings yet

- Assignment pgfc1913Document9 pagesAssignment pgfc1913Surbhî GuptaNo ratings yet

- Godwari IspatDocument251 pagesGodwari IspatHarsh 'Bumma' BhammerNo ratings yet

- Comparison - Ratios - Tyre - DistributionDocument15 pagesComparison - Ratios - Tyre - DistributionParehjuiNo ratings yet

- Chapter 6Document1 pageChapter 6premaahokNo ratings yet

- Profit and Loss Account of Akzo NobelDocument15 pagesProfit and Loss Account of Akzo NobelKaizad DadrewallaNo ratings yet

- Priya Bansal pgfc1924Document8 pagesPriya Bansal pgfc1924Surbhî GuptaNo ratings yet

- The Income Statement Items For CIBDocument2 pagesThe Income Statement Items For CIBKhalid Al SanabaniNo ratings yet

- India Cements Limited: Latest Quarterly/Halfyearly Detailed Quarterly As On (Months) 31-Dec-200931-Dec-2008Document6 pagesIndia Cements Limited: Latest Quarterly/Halfyearly Detailed Quarterly As On (Months) 31-Dec-200931-Dec-2008amitkr91No ratings yet

- TVS Motors Credit Risk AnalysisDocument21 pagesTVS Motors Credit Risk AnalysisBharat ChaudharyNo ratings yet

- Accounts Term PaperDocument508 pagesAccounts Term Paperrohit_indiaNo ratings yet

- Accounting For ManagementDocument26 pagesAccounting For Managementdheivayani kNo ratings yet

- ATC Valuation - Solution Along With All The ExhibitsDocument20 pagesATC Valuation - Solution Along With All The ExhibitsAbiNo ratings yet

- Rdy Mad e Pmegp 10 LacsDocument13 pagesRdy Mad e Pmegp 10 LacssyedNo ratings yet

- Securities Operations: A Guide to Trade and Position ManagementFrom EverandSecurities Operations: A Guide to Trade and Position ManagementRating: 4 out of 5 stars4/5 (3)

- Electronic Marketing ChannelsDocument25 pagesElectronic Marketing ChannelsSurbhî GuptaNo ratings yet

- Marketing Channels For ServicesDocument24 pagesMarketing Channels For ServicesSurbhî GuptaNo ratings yet

- Shashank Malik - PGFB1944 - BOCA GR2 - Study Group 4 - Central Bank of IndiaDocument13 pagesShashank Malik - PGFB1944 - BOCA GR2 - Study Group 4 - Central Bank of IndiaSurbhî GuptaNo ratings yet

- Shreya Jain - PGFC1935 - Performance AnalysisDocument13 pagesShreya Jain - PGFC1935 - Performance AnalysisSurbhî GuptaNo ratings yet

- Bank Performance Analysis-INDUSIND BANK: Particulars Mar-16Document26 pagesBank Performance Analysis-INDUSIND BANK: Particulars Mar-16Surbhî GuptaNo ratings yet

- Bank of India Performance Analysis: Total AssetsDocument6 pagesBank of India Performance Analysis: Total AssetsSurbhî GuptaNo ratings yet

- B.O.C.A Assignment - Vishal Singh - pgsf1951 - Performance AnalysisDocument14 pagesB.O.C.A Assignment - Vishal Singh - pgsf1951 - Performance AnalysisSurbhî GuptaNo ratings yet

- Kotak Mahindra Bank Performance AnalysisDocument18 pagesKotak Mahindra Bank Performance AnalysisSurbhî GuptaNo ratings yet

- Boca Vinay pgfc1948 Icici BankDocument12 pagesBoca Vinay pgfc1948 Icici BankSurbhî GuptaNo ratings yet

- Shreeya Verma (PGSF1952)Document15 pagesShreeya Verma (PGSF1952)Surbhî GuptaNo ratings yet

- Satyam PGSF1937 BOCA BOI BADocument15 pagesSatyam PGSF1937 BOCA BOI BASurbhî GuptaNo ratings yet

- Bank Performance Analysis - Sahil Badaya PGFB1942Document10 pagesBank Performance Analysis - Sahil Badaya PGFB1942Surbhî GuptaNo ratings yet

- Reshma Chauhan - PGFC1927 (BOCA)Document9 pagesReshma Chauhan - PGFC1927 (BOCA)Surbhî GuptaNo ratings yet

- Samarth Mehrotra - BOCADocument23 pagesSamarth Mehrotra - BOCASurbhî GuptaNo ratings yet

- Axis Bank Ltd. Performance AnalysisDocument13 pagesAxis Bank Ltd. Performance AnalysisSurbhî GuptaNo ratings yet

- Priya Bansal pgfc1924Document8 pagesPriya Bansal pgfc1924Surbhî GuptaNo ratings yet

- Performance Analysis - CbiDocument19 pagesPerformance Analysis - CbiSurbhî GuptaNo ratings yet

- Nitesh Khandelwal (PGFC1921) - BOCA (Central Bank of India)Document12 pagesNitesh Khandelwal (PGFC1921) - BOCA (Central Bank of India)Surbhî GuptaNo ratings yet

- YES Bank Performance AnalysisDocument11 pagesYES Bank Performance AnalysisSurbhî GuptaNo ratings yet

- Rashi AggarwalDocument17 pagesRashi AggarwalSurbhî GuptaNo ratings yet

- Assignment pgfc1913Document9 pagesAssignment pgfc1913Surbhî GuptaNo ratings yet

- Bank Performance Analysis With Risk RatiosDocument8 pagesBank Performance Analysis With Risk RatiosSurbhî GuptaNo ratings yet

- Kotak Mahindra Bank Ltd. Performance Analysis For The Period 2016-2020Document15 pagesKotak Mahindra Bank Ltd. Performance Analysis For The Period 2016-2020Surbhî GuptaNo ratings yet

- Axis Bank Ltd. Performance AnalysisDocument11 pagesAxis Bank Ltd. Performance AnalysisSurbhî GuptaNo ratings yet

- Bank Performance AnalysisDocument10 pagesBank Performance AnalysisSurbhî GuptaNo ratings yet

- Equities and Liabilities Shareholder'S Funds Mar-20 Mar-19 Total Share Capital 3,277.66 2,760.03Document11 pagesEquities and Liabilities Shareholder'S Funds Mar-20 Mar-19 Total Share Capital 3,277.66 2,760.03Surbhî GuptaNo ratings yet

- Bank Performance AnalysisDocument4 pagesBank Performance AnalysisSurbhî GuptaNo ratings yet

- IDFC First Bank LTD Performance Analysis: Total AssetsDocument9 pagesIDFC First Bank LTD Performance Analysis: Total AssetsSurbhî GuptaNo ratings yet

- Provisions and Contingencies Include Provision For TaxDocument6 pagesProvisions and Contingencies Include Provision For TaxSurbhî GuptaNo ratings yet

- Performance Analysis of ICICI BankDocument7 pagesPerformance Analysis of ICICI BankSurbhî GuptaNo ratings yet

- Cost & Management Accounting (CMA) : SyllabusDocument7 pagesCost & Management Accounting (CMA) : SyllabusMandish AjmeriNo ratings yet

- French M&A and Restructuring ForumDocument24 pagesFrench M&A and Restructuring ForumRemark, The Mergermarket GroupNo ratings yet

- Sales Management: Meaning, Definition, Nature, Scope, Objectives, FunctionsDocument43 pagesSales Management: Meaning, Definition, Nature, Scope, Objectives, Functionsnamita sharmaNo ratings yet

- Atlas Copco 140 YearsDocument136 pagesAtlas Copco 140 YearsJulliana SilvaNo ratings yet

- Barrons 08 11 2021Document67 pagesBarrons 08 11 2021Netko BezimenNo ratings yet

- ICAEW - Chapter 6 - Control Accounts Errors and Suspense AccountsDocument21 pagesICAEW - Chapter 6 - Control Accounts Errors and Suspense Accountsvothituongnhi7703No ratings yet

- Example 1: SolutionDocument7 pagesExample 1: SolutionalemayehuNo ratings yet

- College of Agribusiness Management GBPUAT, Pantnagar: Topic:The Law of AdvertisingDocument10 pagesCollege of Agribusiness Management GBPUAT, Pantnagar: Topic:The Law of AdvertisingGaurav YadavNo ratings yet

- Course Syllabus: L&S 126 Strategy Formulation First Semester SY 2012 - 2013 Instructors & ScheduleDocument5 pagesCourse Syllabus: L&S 126 Strategy Formulation First Semester SY 2012 - 2013 Instructors & ScheduleJullie Kaye Frias DiamanteNo ratings yet

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument48 pagesDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing Balancemistergray1485No ratings yet

- Quality Management and Reliability (Mn5554) : DR Qingping YangDocument11 pagesQuality Management and Reliability (Mn5554) : DR Qingping YangMuhammad Gunadi RahmadiNo ratings yet

- NMIMS - Session 2 - Transfer Pricing and APA - An OverviewDocument51 pagesNMIMS - Session 2 - Transfer Pricing and APA - An OverviewYash SharmaNo ratings yet

- Professional Certificate in Esg and Social Responsibility - Ausimm PDFDocument1 pageProfessional Certificate in Esg and Social Responsibility - Ausimm PDFAam MuhsramNo ratings yet

- Idea and OpportunityDocument11 pagesIdea and OpportunityAdil BeshayiNo ratings yet

- Assignment 1 Agbu 350 Agribusiness FinanceDocument2 pagesAssignment 1 Agbu 350 Agribusiness FinancePenelopeSFennellNo ratings yet

- Midterm ReviewerDocument9 pagesMidterm ReviewerLesley IdentityNo ratings yet

- Strategic Cost Management Learning Activities Direction: Read and Encircle The Letter Which Corresponds To The Correct AnswerDocument5 pagesStrategic Cost Management Learning Activities Direction: Read and Encircle The Letter Which Corresponds To The Correct AnswerJoan Elieza SernalNo ratings yet

- Export Run at 2023-02-16 04 - 09 - 56Document75 pagesExport Run at 2023-02-16 04 - 09 - 56GeorgeNo ratings yet

- Chapter 7Document25 pagesChapter 7shraddhapagalNo ratings yet

- Mahendra & MahendraDocument111 pagesMahendra & MahendrasiddiqrehanNo ratings yet

- 1Document23 pages1Hanggara CahyadiNo ratings yet

- Wilmar SR 2016 FinalDocument82 pagesWilmar SR 2016 FinalJoseph LeoNo ratings yet

- Corporate Social Responsibility: Installation of Water Purifiers When Mumbai Was SubmergedDocument21 pagesCorporate Social Responsibility: Installation of Water Purifiers When Mumbai Was SubmergedChetan ZopeNo ratings yet

- BSAIS-InAc 213 Information Sheet 1Document11 pagesBSAIS-InAc 213 Information Sheet 1Reena BoliverNo ratings yet

- Mahindra Aerostructure PVT LTD (Maspl)Document37 pagesMahindra Aerostructure PVT LTD (Maspl)Uday Gowda100% (1)

- Ok DECAL, WIRING SCHEMATIC (Xe), SD, LVM, PORO, REMOTE ALARMDocument4 pagesOk DECAL, WIRING SCHEMATIC (Xe), SD, LVM, PORO, REMOTE ALARMMarcos LunaNo ratings yet

- Quiz Submissions - Week 3 - Quiz #3 - TLMT313 D001 Fall 2022 - APEIDocument4 pagesQuiz Submissions - Week 3 - Quiz #3 - TLMT313 D001 Fall 2022 - APEIAmanda LemanskiaNo ratings yet

- Business ScruplesDocument1 pageBusiness ScruplesLizeDecotelliHübnerNo ratings yet

- SOP of Stability Study - 2Document3 pagesSOP of Stability Study - 2YousifNo ratings yet