Download as xlsx, pdf, or txt

You might also like

- Ecosystem-Led Growth: A Blueprint for Sales and Marketing Success Using the Power of PartnershipsFrom EverandEcosystem-Led Growth: A Blueprint for Sales and Marketing Success Using the Power of PartnershipsNo ratings yet

- Lady M DCF TemplateDocument4 pagesLady M DCF Templatednesudhudh100% (1)

- Is Excel Participant - Simplified v2Document9 pagesIs Excel Participant - Simplified v2Yash JasaparaNo ratings yet

- Buku Business Finance PiersonDocument785 pagesBuku Business Finance PiersonMaya Ulfa100% (1)

- Coca Cola - Portfolio ProjectDocument15 pagesCoca Cola - Portfolio Projectapi-249694223No ratings yet

- NYSF Walmart Templatev2Document49 pagesNYSF Walmart Templatev2Avinash Ganesan100% (1)

- FIN 3512 Fall 2019 Quiz #1 9.18.2019 To UploadDocument3 pagesFIN 3512 Fall 2019 Quiz #1 9.18.2019 To UploadgNo ratings yet

- 107 10 DCF Sanity Check AfterDocument6 pages107 10 DCF Sanity Check AfterDavid ChikhladzeNo ratings yet

- Seminar 3 N1591 - MCK Chap 8 QuestionsDocument4 pagesSeminar 3 N1591 - MCK Chap 8 QuestionsMandeep SNo ratings yet

- Xiv: Velocityshares Daily Inverse Vix Short-Term Etn: Note Information Issuer InformationDocument2 pagesXiv: Velocityshares Daily Inverse Vix Short-Term Etn: Note Information Issuer InformationglassguyNo ratings yet

- Is Excel Participant - Simplified v2Document10 pagesIs Excel Participant - Simplified v2Aaron Pool0% (2)

- Apple & RIM Merger Model and LBO ModelDocument50 pagesApple & RIM Merger Model and LBO ModelDarshana MathurNo ratings yet

- PE Exit AnalysisDocument5 pagesPE Exit AnalysisgNo ratings yet

- Facebook Working - Students - UnsolvedDocument10 pagesFacebook Working - Students - UnsolvedK Rohith ReddyNo ratings yet

- Tutorial On How To Use The DCF Model. Good Luck!: DateDocument9 pagesTutorial On How To Use The DCF Model. Good Luck!: DateTanya SinghNo ratings yet

- Sample DCF Valuation TemplateDocument2 pagesSample DCF Valuation TemplateTharun RaoNo ratings yet

- Sample DCF Valuation TemplateDocument2 pagesSample DCF Valuation TemplateTharun RaoNo ratings yet

- Sample DCF Valuation TemplateDocument2 pagesSample DCF Valuation TemplateTharun RaoNo ratings yet

- Valuation - PepsiDocument24 pagesValuation - PepsiLegends MomentsNo ratings yet

- Genzyme DCF PDFDocument5 pagesGenzyme DCF PDFAbinashNo ratings yet

- Discounted Cash Flow-Model For ValuationDocument9 pagesDiscounted Cash Flow-Model For ValuationPCM StresconNo ratings yet

- IS Excel Participant - Simplified v2Document9 pagesIS Excel Participant - Simplified v2Art Euphoria100% (1)

- Purchases / Average Payables Revenue / Average Total AssetsDocument7 pagesPurchases / Average Payables Revenue / Average Total AssetstannuNo ratings yet

- Valuation - CocacolaDocument14 pagesValuation - CocacolaLegends MomentsNo ratings yet

- Mayes 8e CH11 SolutionsDocument22 pagesMayes 8e CH11 SolutionsRamez AhmedNo ratings yet

- Amazon ValuationDocument22 pagesAmazon ValuationDr Sakshi SharmaNo ratings yet

- Is Excel Participant - Simplified v2Document9 pagesIs Excel Participant - Simplified v2dikshapatil6789No ratings yet

- Stock Valuation Spreadsheet TemplateDocument5 pagesStock Valuation Spreadsheet TemplatebgmanNo ratings yet

- Is Excel Participant Samarth - Simplified v2Document9 pagesIs Excel Participant Samarth - Simplified v2samarth halliNo ratings yet

- IS Excel Participant - Simplified v2Document9 pagesIS Excel Participant - Simplified v2animecommunity04No ratings yet

- IS Excel Participant - Simplified v2Document9 pagesIS Excel Participant - Simplified v2tinothing01No ratings yet

- DCF LuluDocument44 pagesDCF LuluPrash KhadkaNo ratings yet

- Fatima FertilizersDocument18 pagesFatima FertilizersBarira AkhtarNo ratings yet

- Nike Inc - Cost of Capital - Syndicate 10Document16 pagesNike Inc - Cost of Capital - Syndicate 10Anthony KwoNo ratings yet

- Financial Model TemplateDocument30 pagesFinancial Model Templateudoshi_1No ratings yet

- 07 12 Sensitivity Tables AfterDocument30 pages07 12 Sensitivity Tables Aftermerag76668No ratings yet

- 04 06 Public Comps Valuation Multiples AfterDocument19 pages04 06 Public Comps Valuation Multiples AfterShanto Arif Uz ZamanNo ratings yet

- Valuation - NVIDIADocument27 pagesValuation - NVIDIALegends MomentsNo ratings yet

- 1/29/2010 2009 360 Apple Inc. 2010 $1,000 $192.06 1000 30% 900,678Document18 pages1/29/2010 2009 360 Apple Inc. 2010 $1,000 $192.06 1000 30% 900,678X.r. GeNo ratings yet

- TIF D&I Solution v24.0Document13 pagesTIF D&I Solution v24.0GDoingThings YTNo ratings yet

- Common Size Income StatementDocument7 pagesCommon Size Income StatementUSD 654No ratings yet

- Valuation of Tata Power, Based On Prof. Aswath Damodaran: DCF Base Year 1 2 3 AssumptionsDocument6 pagesValuation of Tata Power, Based On Prof. Aswath Damodaran: DCF Base Year 1 2 3 Assumptionspriyal batraNo ratings yet

- Análisis Equipo Nutresa Lina - Caso HanssenDocument24 pagesAnálisis Equipo Nutresa Lina - Caso HanssenSARA ZAPATA CANONo ratings yet

- Exxon Mobil Corporation NYSE XOM FinancialsDocument117 pagesExxon Mobil Corporation NYSE XOM Financialsdpr7033No ratings yet

- Manaal - Commercial Banking W J.P MorganDocument9 pagesManaal - Commercial Banking W J.P Morganmanaal.murtaza1No ratings yet

- Uv0052 Xls EngDocument12 pagesUv0052 Xls Engpriyanshu14No ratings yet

- Valuation+ +excel+ +students+Document4 pagesValuation+ +excel+ +students+snigdha.sanaboinaNo ratings yet

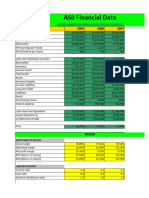

- ASII Financial Data: Items 2009 2008 2007Document10 pagesASII Financial Data: Items 2009 2008 2007AdrianNo ratings yet

- ASII Financial Data: Items 2009 2008 2007Document10 pagesASII Financial Data: Items 2009 2008 2007Gilang AnggoroNo ratings yet

- ASII Financial Data: Items 2009 2008 2007Document10 pagesASII Financial Data: Items 2009 2008 2007Arif SupriyadiNo ratings yet

- ASII Financial Data: Items 2009 2008 2007Document10 pagesASII Financial Data: Items 2009 2008 2007yrperdanaNo ratings yet

- Rasio Sheet v1.0Document10 pagesRasio Sheet v1.0David Syah putraNo ratings yet

- Rasio Sheet v1.0Document10 pagesRasio Sheet v1.0Akhi DanuNo ratings yet

- Lady M ValuationDocument3 pagesLady M Valuationsairaj bhatkarNo ratings yet

- Ratio Analysis TemplateDocument6 pagesRatio Analysis TemplateGapar FitriNo ratings yet

- Análisis Equipo Nutresa Lina - Caso Hanssen V2Document27 pagesAnálisis Equipo Nutresa Lina - Caso Hanssen V2SARA ZAPATA CANONo ratings yet

- Análisis Equipo Nutresa Lina - Caso Hanssen VFinalDocument28 pagesAnálisis Equipo Nutresa Lina - Caso Hanssen VFinalSARA ZAPATA CANONo ratings yet

- ModelDocument103 pagesModelMatheus Augusto Campos PiresNo ratings yet

- Eastboro Machine Tools - Class (Version 1)Document12 pagesEastboro Machine Tools - Class (Version 1)Shriniwas Nehete100% (1)

- Revised ModelDocument27 pagesRevised ModelAnonymous 0CbF7xaNo ratings yet

- Company's Current StatusDocument36 pagesCompany's Current StatusSergio OlarteNo ratings yet

- I. Income StatementDocument27 pagesI. Income StatementNidhi KaushikNo ratings yet

- Masonite Corp DCF Analysis FinalDocument5 pagesMasonite Corp DCF Analysis FinaladiNo ratings yet

- Bond Basics: Yield, Price and Other Confusion - InvestopediaDocument7 pagesBond Basics: Yield, Price and Other Confusion - InvestopediaLouis ForestNo ratings yet

- Credit Transactions Case DoctrinesDocument20 pagesCredit Transactions Case DoctrinesMerGonzagaNo ratings yet

- Summer Training Project: Company: HSBC Invest Direct and HSBC Bank Advisor: Mrs. Shilpa JainDocument56 pagesSummer Training Project: Company: HSBC Invest Direct and HSBC Bank Advisor: Mrs. Shilpa JainGaurav KambojNo ratings yet

- SIP Pause Cancellation FormDocument1 pageSIP Pause Cancellation Formdatadisk10No ratings yet

- Capital Budgeting ExamplesDocument8 pagesCapital Budgeting Examplesaldamati2010No ratings yet

- Toys 25 Report 2018 Website VersionDocument9 pagesToys 25 Report 2018 Website VersionIgnatius M. Ivan HartonoNo ratings yet

- Session 8: Post Class Tests: Cyprus S&P 500 2Document3 pagesSession 8: Post Class Tests: Cyprus S&P 500 2Anshik BansalNo ratings yet

- Internal Assessment Test 2 Entrepreneurship Development Bu 3 Semester Section A Mcqs 20 30 Secs Each 20 MarksDocument28 pagesInternal Assessment Test 2 Entrepreneurship Development Bu 3 Semester Section A Mcqs 20 30 Secs Each 20 MarksRam Krishna KrishNo ratings yet

- Finalchapter 22Document7 pagesFinalchapter 22Jud Rossette ArcebesNo ratings yet

- Mata Kuliah Buku Mba IkaDocument2 pagesMata Kuliah Buku Mba IkaHabibah Asma'ul HusnaNo ratings yet

- Gold An Investment RationaleDocument83 pagesGold An Investment Rationaleप्रशांत कौशिक60% (5)

- Acquisition Leveraged Finance (한성원)Document18 pagesAcquisition Leveraged Finance (한성원)Claire Jingyi Li100% (5)

- Presentation On General Insurance CompaniesDocument43 pagesPresentation On General Insurance Companiesskenkan50% (6)

- Financial InnovationDocument19 pagesFinancial InnovationSiva ShankarNo ratings yet

- Liquidity RatioDocument24 pagesLiquidity RatioSarthakNo ratings yet

- Adjudication Order in The Matter of Anil Monga and OthersDocument12 pagesAdjudication Order in The Matter of Anil Monga and OthersShyam SunderNo ratings yet

- Re BPS EpsDocument4 pagesRe BPS EpsAngela MartiresNo ratings yet

- AcctgDocument11 pagesAcctgsarahbee100% (2)

- Joint Venture Accounting PDFDocument10 pagesJoint Venture Accounting PDFHena Kausar100% (2)

- VALUATION by Reynaldo NogralesDocument29 pagesVALUATION by Reynaldo NogralesresiajhiNo ratings yet

- Dayag Chapter 4Document17 pagesDayag Chapter 4Clifford Angel Matias71% (7)

- SSRN Id2939649 PDFDocument74 pagesSSRN Id2939649 PDFRaúl NàndiNo ratings yet

- Fins1613 NotesDocument22 pagesFins1613 Notesasyunmwewert100% (1)

- Introduction To Financial Systems and Banking Regulations: Institute of Bankers PakistanDocument3 pagesIntroduction To Financial Systems and Banking Regulations: Institute of Bankers PakistanUmar AwanNo ratings yet

- Technical AnalysisDocument3 pagesTechnical AnalysiscutemuskanNo ratings yet

- Far450 Fac450Document8 pagesFar450 Fac450aielNo ratings yet

- Mba Projects in Hyderabad@ 9908701362Document12 pagesMba Projects in Hyderabad@ 9908701362Balakrishna ChakaliNo ratings yet