Download as pdf or txt

You might also like

- AJO (ROSCA) Contribution AgreementDocument3 pagesAJO (ROSCA) Contribution Agreementejogheneta72% (18)

- Full Download Ebook Ebook PDF Macroeconomics Global Edition 13th Edition PDFDocument41 pagesFull Download Ebook Ebook PDF Macroeconomics Global Edition 13th Edition PDFcarol.martinez79496% (50)

- If Current Trends Continue, China May Emerge As The World's Largest Economy by 2020.Document4 pagesIf Current Trends Continue, China May Emerge As The World's Largest Economy by 2020.Zainorin Ali100% (15)

- Chapter 6 Option Pricing 2022 SDocument32 pagesChapter 6 Option Pricing 2022 SĐức Nam TrầnNo ratings yet

- Chapter 6 - Option Pricing - 2022 - SDocument32 pagesChapter 6 - Option Pricing - 2022 - SNgoc Anh LeNo ratings yet

- Option ValuationsDocument29 pagesOption ValuationsArham Kumar JainBD21064No ratings yet

- BinomialDocument22 pagesBinomialSonam Gupta SarafNo ratings yet

- Put-Call Parity: - Put Option Value Can Be Computed Using Put-Call Parity Fiduciary Call Protective PutDocument30 pagesPut-Call Parity: - Put Option Value Can Be Computed Using Put-Call Parity Fiduciary Call Protective PutARYA SHETHNo ratings yet

- Introduction To Binomial TreesDocument25 pagesIntroduction To Binomial Treesyty etytrfNo ratings yet

- Binomial TreesDocument25 pagesBinomial TreesJayash KaushalNo ratings yet

- Session 9Document29 pagesSession 9Ramesh PowarNo ratings yet

- 7 Introduction To Binomial TreesDocument25 pages7 Introduction To Binomial TreesDragosCavescuNo ratings yet

- Binomial: TreesDocument33 pagesBinomial: Treesbk channelNo ratings yet

- Session 4 Stock ValuationDocument17 pagesSession 4 Stock ValuationRoshanNo ratings yet

- MGMT 41150 - Chapter 13 - Binomial TreesDocument41 pagesMGMT 41150 - Chapter 13 - Binomial TreesLaxus DreyerNo ratings yet

- Investment Basics I: ObjectivesDocument14 pagesInvestment Basics I: Objectivesno nameNo ratings yet

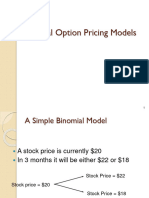

- A Simple Binomial Model: - A Stock Price Is Currently $20 - in Three Months It Will Be Either $22 or $18Document55 pagesA Simple Binomial Model: - A Stock Price Is Currently $20 - in Three Months It Will Be Either $22 or $18nasrullohNo ratings yet

- Binomial TreeDocument19 pagesBinomial Treenikhita1004No ratings yet

- Option Pricing Using Binomial TreesDocument19 pagesOption Pricing Using Binomial TreesDhaka SylhetNo ratings yet

- The Black-Scholes ModelDocument42 pagesThe Black-Scholes Modelnaviprasadthebond9532No ratings yet

- Investment Analysis & Portfolio ManagementDocument35 pagesInvestment Analysis & Portfolio ManagementMuhammad TalhaNo ratings yet

- Chapter Fifteen: Dividend Discount ModelsDocument33 pagesChapter Fifteen: Dividend Discount Modelsnarayanmenon007No ratings yet

- T10a Binomial Intro HoDocument8 pagesT10a Binomial Intro HoMd parvezsharifNo ratings yet

- ValuationDocument23 pagesValuationBisma KhalidNo ratings yet

- Inv - CH-4Document57 pagesInv - CH-4mickamhaaNo ratings yet

- Chapter 18 Equity Valuation Models Lecture Notes PDFDocument11 pagesChapter 18 Equity Valuation Models Lecture Notes PDFcourse shtsNo ratings yet

- Slides 5Document41 pagesSlides 5Gonçalo AlmeidaNo ratings yet

- Outline: Page 2 of 22Document61 pagesOutline: Page 2 of 22L SNo ratings yet

- Valuation of Bond & EquityDocument30 pagesValuation of Bond & EquityngbopNo ratings yet

- Valuation of EquityDocument40 pagesValuation of EquityPRIYA KUMARINo ratings yet

- FIN2004 - 2704 Week 8 SlidesDocument64 pagesFIN2004 - 2704 Week 8 SlidesNguyen DzungNo ratings yet

- Network Design Uncertain EnvDocument44 pagesNetwork Design Uncertain EnvNiranjan ThirNo ratings yet

- Risks Associated With Debt Capital Markets: B.B.Chakrabarti Professor of FinanceDocument39 pagesRisks Associated With Debt Capital Markets: B.B.Chakrabarti Professor of Financec26btnjhj4No ratings yet

- Associate Professor. Mohamed El AshhabDocument12 pagesAssociate Professor. Mohamed El AshhabmidoNo ratings yet

- Equity Valuation ModelsDocument37 pagesEquity Valuation Modelskarthik chamarthyNo ratings yet

- Chap007 OnlineDocument14 pagesChap007 OnlinelittlekittentomboyNo ratings yet

- Depreciation and Financial AccountingDocument77 pagesDepreciation and Financial AccountingnuvanNo ratings yet

- BU7300 Week 3 Cost of EquityDocument25 pagesBU7300 Week 3 Cost of EquityKawther Moh'dNo ratings yet

- Valuation of Bonds and Shares BD CH 8,9Document42 pagesValuation of Bonds and Shares BD CH 8,9Hien ThuNo ratings yet

- IMT-Chapter 2Document33 pagesIMT-Chapter 2kapoorraghav7777No ratings yet

- 0 20200519134342understanding of Loans and Bonds Part 2 PDFDocument19 pages0 20200519134342understanding of Loans and Bonds Part 2 PDFWalter WhiteNo ratings yet

- Ch. 10 Common Stock Valuation Fundamental Analysis: / (1+k) + D / (1+k) / (1+k) +..Document4 pagesCh. 10 Common Stock Valuation Fundamental Analysis: / (1+k) + D / (1+k) / (1+k) +..JoselinoPareraNo ratings yet

- MIT15 401F08 Review Mid PDFDocument38 pagesMIT15 401F08 Review Mid PDFGasimovskyNo ratings yet

- Interest Rates and Bond Valuation: Eric J. Mclaughlin, PH.DDocument60 pagesInterest Rates and Bond Valuation: Eric J. Mclaughlin, PH.DMinh TrangNo ratings yet

- Ch. 10 Common Stock Valuation Fundamental Analysis: / (1+k) + D / (1+k) / (1+k) +..Document4 pagesCh. 10 Common Stock Valuation Fundamental Analysis: / (1+k) + D / (1+k) / (1+k) +..Darshan RavalNo ratings yet

- Equity ValuationDocument36 pagesEquity ValuationANo ratings yet

- Chapter 07Document56 pagesChapter 07蔡彤旻No ratings yet

- Ratio Analysis: DR S.S.LimayeDocument14 pagesRatio Analysis: DR S.S.Limayeharry321No ratings yet

- Lecture 7 BondsDocument47 pagesLecture 7 BondsHuế HoàngNo ratings yet

- FRM Lecture 9 2020 2021 HandoutDocument39 pagesFRM Lecture 9 2020 2021 HandoutDaanNo ratings yet

- Valuing Options in Practice: DerivativesDocument6 pagesValuing Options in Practice: DerivativesLuis MiguelNo ratings yet

- Valuation ModelsDocument47 pagesValuation ModelsSenthilkumar VNo ratings yet

- Chapter II Choice Involving RiskDocument29 pagesChapter II Choice Involving Riskselomonbrhane17171No ratings yet

- Equity Valuation: Learning ObjectivesDocument25 pagesEquity Valuation: Learning Objectivesswastik guptaNo ratings yet

- Corp Fin 3Document25 pagesCorp Fin 3Nguyễn GiangNo ratings yet

- 4 Bond and StockDocument32 pages4 Bond and Stockmahwish111No ratings yet

- Chapter 8 Stock ValuationDocument35 pagesChapter 8 Stock ValuationHamza KhalidNo ratings yet

- Chapter 6 Set 1 Dividend Discount ModelsDocument14 pagesChapter 6 Set 1 Dividend Discount ModelsNick HaldenNo ratings yet

- Module 4: Option PricingDocument62 pagesModule 4: Option PricingAbinash BiswalNo ratings yet

- Financial Management Lecture 3 Valuation of SecuritiesDocument30 pagesFinancial Management Lecture 3 Valuation of SecuritiesTesfaye ejetaNo ratings yet

- Bond Prices and Yields: Figuring Out The Assured ReturnsDocument36 pagesBond Prices and Yields: Figuring Out The Assured ReturnsvaibhavNo ratings yet

- asset-v1-IMF+FMAx+1T2017+type@asset+block@FMAx M1 CLEAN NewDocument42 pagesasset-v1-IMF+FMAx+1T2017+type@asset+block@FMAx M1 CLEAN NewBURUNDI1No ratings yet

- Capital Asset Investment: Strategy, Tactics and ToolsFrom EverandCapital Asset Investment: Strategy, Tactics and ToolsRating: 1 out of 5 stars1/5 (1)

- 14 - VC NegotiationDocument10 pages14 - VC Negotiationmiku hrshNo ratings yet

- 08 - Nurturing Green (C)Document14 pages08 - Nurturing Green (C)miku hrshNo ratings yet

- Private Equity and Venture Capital: Atul KediaDocument12 pagesPrivate Equity and Venture Capital: Atul Kediamiku hrshNo ratings yet

- S1 - Introduction To DerivativesDocument12 pagesS1 - Introduction To Derivativesmiku hrshNo ratings yet

- Heston Model: Sankarshan Basu Professor of Finance Indian Institute of Management BangaloreDocument3 pagesHeston Model: Sankarshan Basu Professor of Finance Indian Institute of Management Bangaloremiku hrshNo ratings yet

- Private Equity and Venture Capital: Atul KediaDocument11 pagesPrivate Equity and Venture Capital: Atul Kediamiku hrshNo ratings yet

- 07 - VC Financing Co Creation and ExpansionDocument13 pages07 - VC Financing Co Creation and Expansionmiku hrshNo ratings yet

- S2. The Mechanics of The Futures MarketDocument13 pagesS2. The Mechanics of The Futures Marketmiku hrshNo ratings yet

- Investments, 8 Edition: Risk Aversion and Capital Allocation To Risky AssetsDocument33 pagesInvestments, 8 Edition: Risk Aversion and Capital Allocation To Risky Assetsmiku hrshNo ratings yet

- Security Analysis and Portfolio Management: Session-1Document26 pagesSecurity Analysis and Portfolio Management: Session-1miku hrshNo ratings yet

- Credit DerivativesDocument10 pagesCredit Derivativesmiku hrshNo ratings yet

- The Greek Letters: Option Portfolio Value and GreeksDocument16 pagesThe Greek Letters: Option Portfolio Value and Greeksmiku hrshNo ratings yet

- Credit Derivatives - AdditionalDocument13 pagesCredit Derivatives - Additionalmiku hrshNo ratings yet

- Black Scholes ModelDocument10 pagesBlack Scholes Modelmiku hrshNo ratings yet

- Swaptions: European Swap OptionsDocument4 pagesSwaptions: European Swap Optionsmiku hrshNo ratings yet

- What Are Exotic Options?Document9 pagesWhat Are Exotic Options?miku hrshNo ratings yet

- Karnataka Engineering Company Limited (KECL)Document13 pagesKarnataka Engineering Company Limited (KECL)miku hrshNo ratings yet

- Value at RiskDocument17 pagesValue at Riskmiku hrshNo ratings yet

- Ps Asia Catalogue 6 (Jan 2021) (Free)Document120 pagesPs Asia Catalogue 6 (Jan 2021) (Free)Muhammad DanaNo ratings yet

- Lecture Note 3 Economic Welfare and Pricing in Competitive and Monopolistic StructuresDocument17 pagesLecture Note 3 Economic Welfare and Pricing in Competitive and Monopolistic Structuresveera reddyNo ratings yet

- In Union Budget 2023 Detailed Analysis NoexpDocument78 pagesIn Union Budget 2023 Detailed Analysis NoexppatrodeskNo ratings yet

- VHINSON - Intermediate Accounting 3 (2023 - 2024 Edition) - 103Document1 pageVHINSON - Intermediate Accounting 3 (2023 - 2024 Edition) - 103Alyssa Marie NacionNo ratings yet

- ACT 2100 Worksheet IVDocument7 pagesACT 2100 Worksheet IVAshmini PershadNo ratings yet

- Gov. Ige's BudgetDocument158 pagesGov. Ige's BudgetHNN100% (1)

- Accounting ProjectDocument25 pagesAccounting ProjectLidianny CastilloNo ratings yet

- Presentation For Partners ENGDocument20 pagesPresentation For Partners ENGinvestorsclinicleadsNo ratings yet

- trắc nghiệm thị trường tài chính tiếng anhDocument41 pagestrắc nghiệm thị trường tài chính tiếng anh05 Phạm Hồng Diệp12.11No ratings yet

- Winston - Children of Invention - OcredDocument13 pagesWinston - Children of Invention - OcredIrene IturraldeNo ratings yet

- Background For International Business and Trade Module 1Document9 pagesBackground For International Business and Trade Module 1Gilbert Ocampo100% (2)

- Life Annuities Evaluation Answer KeyDocument6 pagesLife Annuities Evaluation Answer KeyReign ManeseNo ratings yet

- Invoice 1144 Spectra Chembekasumbalesa SiteDocument1 pageInvoice 1144 Spectra Chembekasumbalesa SiteAmon KapelaNo ratings yet

- 10 Practice Problems Monopoly Price DiscrimDocument12 pages10 Practice Problems Monopoly Price Discrimphineas12345678910ferbNo ratings yet

- Cultural SymbolsDocument4 pagesCultural SymbolsMark BaquiranNo ratings yet

- 10.1007@978 3 030 35346 9Document405 pages10.1007@978 3 030 35346 9abiliovieiraNo ratings yet

- F9 FM ALL in One Technical ArticlesDocument191 pagesF9 FM ALL in One Technical ArticlesRejoice MpofuNo ratings yet

- Lecture Chapter 5Document32 pagesLecture Chapter 5Mai HiếuNo ratings yet

- As Built Layout-As Built LayoutDocument1 pageAs Built Layout-As Built LayoutMaster MunnaNo ratings yet

- Study - Id86824 - Coffee Market in VietnamDocument42 pagesStudy - Id86824 - Coffee Market in VietnamĐặng Thị Mỹ LệNo ratings yet

- Marico BSDocument2 pagesMarico BSAbhay Kumar SinghNo ratings yet

- State Bank of India (SBI) : Fortune Global 500Document14 pagesState Bank of India (SBI) : Fortune Global 500Varsha RayaluNo ratings yet

- Dho Health Science Updated 8th Edition Simmers Test BankDocument24 pagesDho Health Science Updated 8th Edition Simmers Test BankEmilyRamirezmgdq100% (48)

- Can Money Buy Happiness An Examination of Happiness EconomicsDocument4 pagesCan Money Buy Happiness An Examination of Happiness EconomicsLeon HaiderNo ratings yet

- Buy Back AssingmentDocument5 pagesBuy Back AssingmentDARK KING GamersNo ratings yet

- Bahan 4Document9 pagesBahan 4wahyudhyNo ratings yet

- Committee/Commission Head ObjectiveDocument5 pagesCommittee/Commission Head ObjectiveadmNo ratings yet