Download as xls, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5820)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Quiz - Quiz 2 Partnership Dissolution and Liquidation AnswersDocument15 pagesQuiz - Quiz 2 Partnership Dissolution and Liquidation AnswersKent Zirkai CidroNo ratings yet

- Problem #3Document16 pagesProblem #3hehehehehloo42% (12)

- Obligation Drill 2Document2 pagesObligation Drill 2Maurren SalidoNo ratings yet

- Tabunggao, Shane Josa Marie M. AC23 Exercises On Cash Flow Statement Analysis Theories: Investing FinancingDocument3 pagesTabunggao, Shane Josa Marie M. AC23 Exercises On Cash Flow Statement Analysis Theories: Investing FinancingShane TabunggaoNo ratings yet

- United Bank Limited Aiou Internship ReportDocument104 pagesUnited Bank Limited Aiou Internship ReportHamza100% (3)

- Kotak Mahindra Bank Performance AnalysisDocument18 pagesKotak Mahindra Bank Performance AnalysisSurbhî GuptaNo ratings yet

- Marketing Channels For ServicesDocument24 pagesMarketing Channels For ServicesSurbhî GuptaNo ratings yet

- Electronic Marketing ChannelsDocument25 pagesElectronic Marketing ChannelsSurbhî GuptaNo ratings yet

- Samarth Mehrotra - BOCADocument23 pagesSamarth Mehrotra - BOCASurbhî GuptaNo ratings yet

- Boca Vinay pgfc1948 Icici BankDocument12 pagesBoca Vinay pgfc1948 Icici BankSurbhî GuptaNo ratings yet

- B.O.C.A Assignment - Vishal Singh - pgsf1951 - Performance AnalysisDocument14 pagesB.O.C.A Assignment - Vishal Singh - pgsf1951 - Performance AnalysisSurbhî GuptaNo ratings yet

- Shreeya Verma (PGSF1952)Document15 pagesShreeya Verma (PGSF1952)Surbhî GuptaNo ratings yet

- Bank Performance Analysis-INDUSIND BANK: Particulars Mar-16Document26 pagesBank Performance Analysis-INDUSIND BANK: Particulars Mar-16Surbhî GuptaNo ratings yet

- Shreya Jain - PGFC1935 - Performance AnalysisDocument13 pagesShreya Jain - PGFC1935 - Performance AnalysisSurbhî GuptaNo ratings yet

- YES Bank Performance AnalysisDocument11 pagesYES Bank Performance AnalysisSurbhî GuptaNo ratings yet

- Bank of India Performance Analysis: Total AssetsDocument6 pagesBank of India Performance Analysis: Total AssetsSurbhî GuptaNo ratings yet

- Performance Analysis - CbiDocument19 pagesPerformance Analysis - CbiSurbhî GuptaNo ratings yet

- Shashank Malik - PGFB1944 - BOCA GR2 - Study Group 4 - Central Bank of IndiaDocument13 pagesShashank Malik - PGFB1944 - BOCA GR2 - Study Group 4 - Central Bank of IndiaSurbhî GuptaNo ratings yet

- Axis Bank Ltd. Performance AnalysisDocument13 pagesAxis Bank Ltd. Performance AnalysisSurbhî GuptaNo ratings yet

- Bank Performance Analysis - Sahil Badaya PGFB1942Document10 pagesBank Performance Analysis - Sahil Badaya PGFB1942Surbhî GuptaNo ratings yet

- Nitesh Khandelwal (PGFC1921) - BOCA (Central Bank of India)Document12 pagesNitesh Khandelwal (PGFC1921) - BOCA (Central Bank of India)Surbhî GuptaNo ratings yet

- Satyam PGSF1937 BOCA BOI BADocument15 pagesSatyam PGSF1937 BOCA BOI BASurbhî GuptaNo ratings yet

- Bank Performance AnalysisDocument10 pagesBank Performance AnalysisSurbhî GuptaNo ratings yet

- Kotak Mahindra Bank Ltd. Performance Analysis For The Period 2016-2020Document15 pagesKotak Mahindra Bank Ltd. Performance Analysis For The Period 2016-2020Surbhî GuptaNo ratings yet

- Reshma Chauhan - PGFC1927 (BOCA)Document9 pagesReshma Chauhan - PGFC1927 (BOCA)Surbhî GuptaNo ratings yet

- Bank Performance Analysis With Risk RatiosDocument8 pagesBank Performance Analysis With Risk RatiosSurbhî GuptaNo ratings yet

- Rashi AggarwalDocument17 pagesRashi AggarwalSurbhî GuptaNo ratings yet

- Priya Bansal pgfc1924Document8 pagesPriya Bansal pgfc1924Surbhî GuptaNo ratings yet

- Bank Performance AnalysisDocument4 pagesBank Performance AnalysisSurbhî GuptaNo ratings yet

- Axis Bank Ltd. Performance AnalysisDocument11 pagesAxis Bank Ltd. Performance AnalysisSurbhî GuptaNo ratings yet

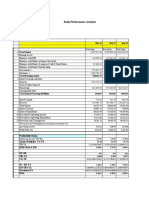

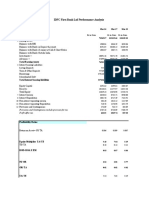

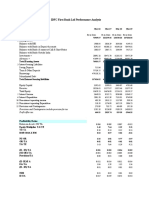

- IDFC First Bank LTD Performance Analysis: Total AssetsDocument9 pagesIDFC First Bank LTD Performance Analysis: Total AssetsSurbhî GuptaNo ratings yet

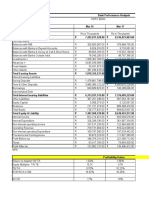

- IDFC First Bank LTD Performance Analysis: Total AssetsDocument6 pagesIDFC First Bank LTD Performance Analysis: Total AssetsSurbhî GuptaNo ratings yet

- Equities and Liabilities Shareholder'S Funds Mar-20 Mar-19 Total Share Capital 3,277.66 2,760.03Document11 pagesEquities and Liabilities Shareholder'S Funds Mar-20 Mar-19 Total Share Capital 3,277.66 2,760.03Surbhî GuptaNo ratings yet

- Provisions and Contingencies Include Provision For TaxDocument6 pagesProvisions and Contingencies Include Provision For TaxSurbhî GuptaNo ratings yet

- Assignment pgfc1913Document9 pagesAssignment pgfc1913Surbhî GuptaNo ratings yet

- Concept of Tax Planning and Specific Management Decisions: CHANIKA GOEL (1886532) RITIKA SACHDEVA (1886586)Document34 pagesConcept of Tax Planning and Specific Management Decisions: CHANIKA GOEL (1886532) RITIKA SACHDEVA (1886586)parvati anilkumarNo ratings yet

- Module 2 Time Value of MoneyDocument42 pagesModule 2 Time Value of MoneyNani MadhavNo ratings yet

- Chapter 01-The Business of Banking: Name: Clas S: DateDocument12 pagesChapter 01-The Business of Banking: Name: Clas S: DateLê Đặng Minh ThảoNo ratings yet

- Assignment-1: Interpretation of The Financial Statements For Jones Corporation and Smith CorporationDocument8 pagesAssignment-1: Interpretation of The Financial Statements For Jones Corporation and Smith CorporationfatemaNo ratings yet

- Teodoro M. Luansing College of Rosario: Senior High School DepartmentDocument9 pagesTeodoro M. Luansing College of Rosario: Senior High School DepartmentSamantha Alice LysanderNo ratings yet

- AC21 - Financial Liabilities - PracticalDocument4 pagesAC21 - Financial Liabilities - PracticalLouise GabrielNo ratings yet

- Finals Quiz 2Document9 pagesFinals Quiz 2Shane TorrieNo ratings yet

- 4MA43E6BFC5Document27 pages4MA43E6BFC5Devishka ShahNo ratings yet

- Transaction & Tabular AnalysisDocument18 pagesTransaction & Tabular AnalysisMahmudul Hassan RohidNo ratings yet

- Trident The U S Based Company Discussed in This Chapter Has Concluded Another LargeDocument1 pageTrident The U S Based Company Discussed in This Chapter Has Concluded Another Largetrilocksp SinghNo ratings yet

- AFFIDAVIT OF John Henry Doe RE CREDITORDocument6 pagesAFFIDAVIT OF John Henry Doe RE CREDITORlauren100% (5)

- Chapter 5-Capital StructureDocument31 pagesChapter 5-Capital StructureNguyen Ha PhuongNo ratings yet

- IELTS Essay 6Document1 pageIELTS Essay 6Mohamed FawzyNo ratings yet

- Public Notice FORECLOSUREDocument4 pagesPublic Notice FORECLOSUREInta DižāNo ratings yet

- Accounting For Specialized Institution Set 2 Scheme of ValuationDocument19 pagesAccounting For Specialized Institution Set 2 Scheme of ValuationTitus Clement100% (1)

- Bhagi Rathi Pandey: Page 1 of 3Document3 pagesBhagi Rathi Pandey: Page 1 of 3Bhagirathi PandeyNo ratings yet

- Introduction To The Scope of Syllabus and Paper Format.: ISC 2021 Accounts ProjectDocument20 pagesIntroduction To The Scope of Syllabus and Paper Format.: ISC 2021 Accounts ProjectMariamNo ratings yet

- Credit Transactions (JAPRL Development Corp vs. Security Bank Corporation)Document2 pagesCredit Transactions (JAPRL Development Corp vs. Security Bank Corporation)Maestro LazaroNo ratings yet

- A. RecognitionDocument9 pagesA. RecognitionMark Paul RamosNo ratings yet

- Auditing ExamDocument5 pagesAuditing ExamMoniqueNo ratings yet

- A Study On Comparative Analysis of Financial StatementDocument13 pagesA Study On Comparative Analysis of Financial StatementMehakNo ratings yet

- Oblicon 2 17 2024Document4 pagesOblicon 2 17 2024Justin BidanNo ratings yet

- Proceedings Carei2019 PDFDocument320 pagesProceedings Carei2019 PDFНаталія Юріївна ТодороваNo ratings yet

- Tandon CommitteeDocument17 pagesTandon CommitteeGayathri TNo ratings yet

- What Is Unearned Revenue?Document3 pagesWhat Is Unearned Revenue?JNo ratings yet