Download as pdf or txt

You might also like

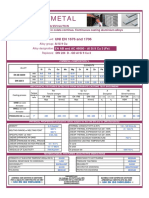

- Raffmetal: UNI EN 1676 and 1706Document2 pagesRaffmetal: UNI EN 1676 and 1706satheeskumar VikramasingarajNo ratings yet

- Lycoming TIO-541 Overhaul Manual PDFDocument80 pagesLycoming TIO-541 Overhaul Manual PDFsplynNo ratings yet

- BMS-0000356 - Part Number Definition - Rev04Document2 pagesBMS-0000356 - Part Number Definition - Rev04Cristian NarroNo ratings yet

- Configuration MOP Aircel ICRDocument7 pagesConfiguration MOP Aircel ICRKaran ParmarNo ratings yet

- GYRT OnlyDocument5 pagesGYRT OnlygirmabelayNo ratings yet

- Tata AIA Life Insurance Sampoorna Raksha Supreme TC 110N160V02Document54 pagesTata AIA Life Insurance Sampoorna Raksha Supreme TC 110N160V02Aman GuptaNo ratings yet

- Exide Life Freedom Plan (U24) (Uin 114l046v01)Document27 pagesExide Life Freedom Plan (U24) (Uin 114l046v01)Sachin KuttaNo ratings yet

- Tata AIA Life Insurance Sampoorna Raksha Supreme (UIN 110N160V03) TandCDocument32 pagesTata AIA Life Insurance Sampoorna Raksha Supreme (UIN 110N160V03) TandCPradeep KshatriyaNo ratings yet

- Exide Life Powering Life Limited Payment Endowment Plan (Elr) (Uin 114n010v01)Document7 pagesExide Life Powering Life Limited Payment Endowment Plan (Elr) (Uin 114n010v01)Navpreet Singh RandhawaNo ratings yet

- Standard Policy Provisions: 1. DefinitionsDocument4 pagesStandard Policy Provisions: 1. DefinitionsskvskvskvskvNo ratings yet

- Standard Policy Provisions: 1. DefinitionsDocument4 pagesStandard Policy Provisions: 1. DefinitionsskvskvskvskvNo ratings yet

- Reliance Child PlanDocument44 pagesReliance Child PlanNilesh PatilNo ratings yet

- Policy Document - LIC S Fortune PlusDocument12 pagesPolicy Document - LIC S Fortune Plussharma65367No ratings yet

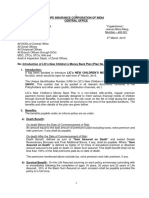

- LICs New Group Gratuity Cash Accumulation Plan (UIN 512N281V01)Document11 pagesLICs New Group Gratuity Cash Accumulation Plan (UIN 512N281V01)Hari GopalaNo ratings yet

- Bharti AXA Life Serv Suraksha V2Document4 pagesBharti AXA Life Serv Suraksha V2A Gophal ReddiNo ratings yet

- Futuregeneralipearlsguarantee 133n047v01Document18 pagesFuturegeneralipearlsguarantee 133n047v01Dinesh nawaleNo ratings yet

- Benefits On DeathDocument16 pagesBenefits On DeathnaitikNo ratings yet

- T&C GCLI Final 138N017V01Document9 pagesT&C GCLI Final 138N017V01raviNo ratings yet

- Annexure 1 To Circular 254Document13 pagesAnnexure 1 To Circular 254rahul4u88No ratings yet

- Directors and Officers Liability Insurance PolicyDocument18 pagesDirectors and Officers Liability Insurance PolicyŠäñjïv KrNo ratings yet

- Ko Tak Term PlanDocument8 pagesKo Tak Term Plansarvesh.bhartiNo ratings yet

- Exide Life InsuranceDocument26 pagesExide Life InsuranceMaheshNo ratings yet

- Part E 6. Part F: Tata AIA Life Insurance Sampoorna Raksha Supreme (UIN: 110N160V02) - IRDA of India Regn No. 110Document3 pagesPart E 6. Part F: Tata AIA Life Insurance Sampoorna Raksha Supreme (UIN: 110N160V02) - IRDA of India Regn No. 110Akshay PatilNo ratings yet

- Preferred Term Plan: Financial Protection For Your Loved Ones. AssuredDocument7 pagesPreferred Term Plan: Financial Protection For Your Loved Ones. AssuredpankajzapNo ratings yet

- Ko Tak Preferred Term PlanDocument7 pagesKo Tak Preferred Term PlanvtanmaynNo ratings yet

- CAB Rider ContractDocument5 pagesCAB Rider ContractpravinNo ratings yet

- ULK ManulifeDocument31 pagesULK ManulifeLong NguyenNo ratings yet

- TnCs Term TakafulPlus PlanDocument6 pagesTnCs Term TakafulPlus Planzairafrajpoot042No ratings yet

- Scan 0005Document1 pageScan 0005Manish KulkarniNo ratings yet

- Healthcare Policy WordingDocument6 pagesHealthcare Policy WordingSalman AbbasNo ratings yet

- Coi PmjjbyDocument4 pagesCoi Pmjjbyashok1259No ratings yet

- Kotak Endowment PlanDocument2 pagesKotak Endowment PlanMichael GreenNo ratings yet

- Sahara NidhiDocument4 pagesSahara NidhiAyush DubeyNo ratings yet

- Life Stay Smart Plan BrochureDocument2 pagesLife Stay Smart Plan BrochureBadi SudhakaranNo ratings yet

- Bharti AXA Life Premier Protect Home ShieldDocument20 pagesBharti AXA Life Premier Protect Home ShieldAsepNo ratings yet

- Fortune Guarantee Pension Policy Document1Document34 pagesFortune Guarantee Pension Policy Document1karamatNo ratings yet

- Privileges and Conditions & Policy Options, Nomination and AssignmentsDocument14 pagesPrivileges and Conditions & Policy Options, Nomination and AssignmentsMajharul Islam BillalNo ratings yet

- Loan Secure Sales Policy DocumentDocument15 pagesLoan Secure Sales Policy Documentakshayguin1997No ratings yet

- ICICI Pru Guaranteed Pension Plan Flexi Annexure V Benefit Enhancer 24june2022Document8 pagesICICI Pru Guaranteed Pension Plan Flexi Annexure V Benefit Enhancer 24june2022Prashant A UNo ratings yet

- Assurance PlanDocument1 pageAssurance Planswetaagarwal2706No ratings yet

- Tata AIA Life Guaranteed Return Insurance Plan (UIN 20110N152V10) TandCDocument106 pagesTata AIA Life Guaranteed Return Insurance Plan (UIN 20110N152V10) TandCsaurabh chaudhariNo ratings yet

- Modified Sales Brochure - New Pension Plus - 25 10 22 - WebsiteDocument25 pagesModified Sales Brochure - New Pension Plus - 25 10 22 - WebsitedeepsdesaiNo ratings yet

- Jubilee Policywordinghealth PersonalcareDocument6 pagesJubilee Policywordinghealth PersonalcareZaheer AhmadNo ratings yet

- PolicyDocument48 pagesPolicyPushpendra KushwahaNo ratings yet

- Lifestyle Care Policy WordingDocument13 pagesLifestyle Care Policy WordingShiza RaheelNo ratings yet

- 831 J Sangam IntroDocument6 pages831 J Sangam IntroJames WilliamsNo ratings yet

- Sample Policy Document - LIC S New Critical Illness Benefit Rider - UIN - 512A212V02Document7 pagesSample Policy Document - LIC S New Critical Illness Benefit Rider - UIN - 512A212V02mikewolf220No ratings yet

- Key Features Document - Aviva I LifeDocument4 pagesKey Features Document - Aviva I LifeSonisx SintuNo ratings yet

- Logo-Policy-document-LIC-s-Bima-Jyoti-dt-24122021 5Document1 pageLogo-Policy-document-LIC-s-Bima-Jyoti-dt-24122021 5Cyril PilligrinNo ratings yet

- Jeevan Vaibhav (PlafgyrthgfDocument4 pagesJeevan Vaibhav (Plafgyrthgfdeepak202002tNo ratings yet

- Life InsuranceDocument23 pagesLife InsuranceSruthi RavindranNo ratings yet

- Preferred Term Plan: Faidey Ka InsuranceDocument7 pagesPreferred Term Plan: Faidey Ka InsurancePratik JainNo ratings yet

- What Is Life Insurance PolicyDocument7 pagesWhat Is Life Insurance Policyzahid LarrNo ratings yet

- Plan 832 CircularDocument9 pagesPlan 832 CircularPankaj GoenkaNo ratings yet

- Sales Brochure LIC GCLIDocument5 pagesSales Brochure LIC GCLIRKNo ratings yet

- SuperannuationDocument12 pagesSuperannuationNetaji DasariNo ratings yet

- Akansha Investment Services: Home Products Services SMS Service FAQ Contact DetailsDocument6 pagesAkansha Investment Services: Home Products Services SMS Service FAQ Contact Detailssarup007No ratings yet

- Life Insurance Corporation of India PDFDocument6 pagesLife Insurance Corporation of India PDFAxe ExaNo ratings yet

- QBE ME Project Specific WordingDocument18 pagesQBE ME Project Specific WordingpranavyesNo ratings yet

- Am Sure Bonus BuilderDocument4 pagesAm Sure Bonus BuildersuganthiaravindNo ratings yet

- Ilife BrochureDocument1 pageIlife BrochureSudhakar GanjikuntaNo ratings yet

- Life, Accident and Health Insurance in the United StatesFrom EverandLife, Accident and Health Insurance in the United StatesRating: 5 out of 5 stars5/5 (1)

- Kuwait National Petroleum Company: Request For QuotationDocument6 pagesKuwait National Petroleum Company: Request For Quotationsatheeskumar VikramasingarajNo ratings yet

- Srila Prabhupada Offerings From Kanhaiyadesh DevoteesDocument57 pagesSrila Prabhupada Offerings From Kanhaiyadesh Devoteessatheeskumar VikramasingarajNo ratings yet

- Kural (Tiruvalluvar)Document168 pagesKural (Tiruvalluvar)satheeskumar VikramasingarajNo ratings yet

- D3.1 - Study On Small Cells and Dense Cellular Networks Regulatory Issues - FinalDocument101 pagesD3.1 - Study On Small Cells and Dense Cellular Networks Regulatory Issues - Finalsatheeskumar VikramasingarajNo ratings yet

- Kuwait National Petroleum Co. Commercial Department Invitation To BidDocument4 pagesKuwait National Petroleum Co. Commercial Department Invitation To Bidsatheeskumar Vikramasingaraj100% (1)

- Item No.1 - UPVCDuctsDocument1 pageItem No.1 - UPVCDuctssatheeskumar VikramasingarajNo ratings yet

- Momarasah Quota Tion Form ﺔــﯿﺘﯾﻮـﻜﻟا ﺔﯿﻨطﻮﻟا لوﺮــﺘﺒﻟا ﺔــﻛﺮــﺷDocument1 pageMomarasah Quota Tion Form ﺔــﯿﺘﯾﻮـﻜﻟا ﺔﯿﻨطﻮﻟا لوﺮــﺘﺒﻟا ﺔــﻛﺮــﺷsatheeskumar VikramasingarajNo ratings yet

- How To Write A Letter or Email That Works (PDFDrive)Document52 pagesHow To Write A Letter or Email That Works (PDFDrive)satheeskumar VikramasingarajNo ratings yet

- Pay Before You Pump Sign2-Pdf-En PDFDocument1 pagePay Before You Pump Sign2-Pdf-En PDFsatheeskumar VikramasingarajNo ratings yet

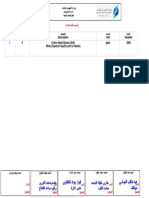

- Item Part No Description Unit Quantity 1 0 Cotton Hand Gloves (Soft) White) Superior Quality Soft On Hands) Pairs 2000Document1 pageItem Part No Description Unit Quantity 1 0 Cotton Hand Gloves (Soft) White) Superior Quality Soft On Hands) Pairs 2000satheeskumar VikramasingarajNo ratings yet

- Teleclaim PDFDocument1 pageTeleclaim PDFsatheeskumar VikramasingarajNo ratings yet

- Vendor Complaint Review Process PDF en PDFDocument3 pagesVendor Complaint Review Process PDF en PDFsatheeskumar VikramasingarajNo ratings yet

- Stuck by A NeedleDocument1 pageStuck by A Needlesatheeskumar VikramasingarajNo ratings yet

- Health Safety Associations PDF enDocument2 pagesHealth Safety Associations PDF ensatheeskumar VikramasingarajNo ratings yet

- Pay Before You Pump Sign2-Pdf-En PDFDocument1 pagePay Before You Pump Sign2-Pdf-En PDFsatheeskumar VikramasingarajNo ratings yet

- Hearing - Protection PDF en PDFDocument1 pageHearing - Protection PDF en PDFsatheeskumar VikramasingarajNo ratings yet

- Bhagavat GIta Marathon - DM 2020 Price ListDocument2 pagesBhagavat GIta Marathon - DM 2020 Price Listsatheeskumar VikramasingarajNo ratings yet

- Ofa Statment Fitness PDF enDocument2 pagesOfa Statment Fitness PDF ensatheeskumar VikramasingarajNo ratings yet

- EE List - 07 Nov 2018Document143 pagesEE List - 07 Nov 2018Alex LeowNo ratings yet

- Martin GreeveDocument43 pagesMartin GreevemanuelNo ratings yet

- KPM ProposalDocument3 pagesKPM Proposalzen.livemeNo ratings yet

- Angola Mineral ResourcesDocument18 pagesAngola Mineral ResourcesOladipo Ojo100% (1)

- EIA ReportDocument11 pagesEIA ReportSid WorldNo ratings yet

- Emi01 2013Document14 pagesEmi01 2013Universal Music CanadaNo ratings yet

- Fluid Mechanics - ProblemsDocument4 pagesFluid Mechanics - ProblemsClement Chima50% (2)

- Quality Test Bank 2Document16 pagesQuality Test Bank 2Behbehlynn100% (4)

- 2X100V 500W Audio Amplifier SMPS Power Supply - Electronics Projects CircuitsDocument2 pages2X100V 500W Audio Amplifier SMPS Power Supply - Electronics Projects CircuitsK. RAJA SEKARNo ratings yet

- Review For The Second TestDocument7 pagesReview For The Second TestMati MoralesNo ratings yet

- Skidmore, Owings and Merrill (SOM) Studio Daniel Libeskind 2006 2014Document8 pagesSkidmore, Owings and Merrill (SOM) Studio Daniel Libeskind 2006 2014Ishita BhardwajNo ratings yet

- Loss of Containment Manual 2012 PDFDocument68 pagesLoss of Containment Manual 2012 PDFpetrolhead1No ratings yet

- ChargeTech PLUG Manual - 42K & 54KDocument6 pagesChargeTech PLUG Manual - 42K & 54KKian GonzagaNo ratings yet

- Piping & Instrumentation DiagramDocument15 pagesPiping & Instrumentation Diagramplanet123No ratings yet

- Comparative Analysis and Optimization of Active Power and Delay of 1-Bit Full Adder at 45 NM TechnologyDocument3 pagesComparative Analysis and Optimization of Active Power and Delay of 1-Bit Full Adder at 45 NM TechnologyNsrc Nano ScientifcNo ratings yet

- Manual Servico Home Theater Philips Hts2500 05Document36 pagesManual Servico Home Theater Philips Hts2500 05Karel Švihálek100% (1)

- Installation Guide C175-C172 All Models Appendix C 242 Rev BDocument52 pagesInstallation Guide C175-C172 All Models Appendix C 242 Rev BJonathan Miguel Gómez MogollónNo ratings yet

- NokShall MartDocument15 pagesNokShall MartMd. Fayazur RahmanNo ratings yet

- BoeingDocument7 pagesBoeingShraddha MalandkarNo ratings yet

- Solar Resource Mapping and PV Potential in MyanmarDocument8 pagesSolar Resource Mapping and PV Potential in Myanmarsalem BEN MOUSSA100% (1)

- Igcse: Definitions & Concepts of ElectricityDocument4 pagesIgcse: Definitions & Concepts of ElectricityMusdq ChowdhuryNo ratings yet

- Jodel D120A Maintenance ScheduleDocument4 pagesJodel D120A Maintenance ScheduleMark JuhrigNo ratings yet

- Final Paper - Ana Maria PumneaDocument2 pagesFinal Paper - Ana Maria PumneaAnna Pumnea0% (1)

- A320 Generator Control SystemDocument5 pagesA320 Generator Control Systemdo hai tran leNo ratings yet

- 9 Chapter 6 ConclusionDocument3 pages9 Chapter 6 ConclusionTejas YeoleNo ratings yet

- MQ SP P 5011 PDFDocument25 pagesMQ SP P 5011 PDFjaseelNo ratings yet

- P1 - CHAPTER 10 - KNOWLEDGE CHECK - Relevant Costs and Decision Making - IMASDocument19 pagesP1 - CHAPTER 10 - KNOWLEDGE CHECK - Relevant Costs and Decision Making - IMASYeon Baek100% (1)