Chap Ter V Performance of Selected Growth Schemes

Chap Ter V Performance of Selected Growth Schemes

You might also like

- Investment Analysis and Portfolio Management Reilly 10th Edition Solutions ManualDocument11 pagesInvestment Analysis and Portfolio Management Reilly 10th Edition Solutions ManualMonicaAcostagzqkx100% (77)

- Ameritrade Case PDFDocument6 pagesAmeritrade Case PDFAnish Anish100% (1)

- Capital Budgeting With Illustration and TheoryDocument145 pagesCapital Budgeting With Illustration and Theorymmuneebsda50% (2)

- Class NotesDocument16 pagesClass NotesAnika Tabassum RodelaNo ratings yet

- Portfolio Management Tutorial 4 & Chapter 4 CalculationDocument39 pagesPortfolio Management Tutorial 4 & Chapter 4 CalculationchziNo ratings yet

- BKM Chapter 7Document43 pagesBKM Chapter 7Isha0% (1)

- 3210AFE Week 4Document43 pages3210AFE Week 4Jason WestNo ratings yet

- ICMEM PresentationDocument17 pagesICMEM Presentationirfanhilmanisme93No ratings yet

- Welcome TO Project SeminorDocument18 pagesWelcome TO Project SeminorRamNo ratings yet

- Capital Market IndicesDocument50 pagesCapital Market IndicesLina AlamiNo ratings yet

- Span MethodologyDocument26 pagesSpan MethodologyMarco PoloNo ratings yet

- 1 - Session - 7 PRM 44Document18 pages1 - Session - 7 PRM 44riteshNo ratings yet

- EFM - MSESPM - Lec 5 - Risk and Return - Chapt4 - 2020Document21 pagesEFM - MSESPM - Lec 5 - Risk and Return - Chapt4 - 2020RabinNo ratings yet

- AnswersDocument7 pagesAnswersasus.mediahubNo ratings yet

- Portfolio Management Handout 2 - QuestionsDocument6 pagesPortfolio Management Handout 2 - QuestionsPriyankaNo ratings yet

- 5SOGS FM LECTURE 5 Risk and Return 1Document31 pages5SOGS FM LECTURE 5 Risk and Return 1Right Karl-Maccoy HattohNo ratings yet

- FM Ch5 Risk & ReturnDocument75 pagesFM Ch5 Risk & Returntemesgen yohannesNo ratings yet

- In The Next Three Chapters, We Will Examine Different Aspects of Capital Market Theory, IncludingDocument62 pagesIn The Next Three Chapters, We Will Examine Different Aspects of Capital Market Theory, IncludingnidamahNo ratings yet

- Risk and Rates of Returns (FM PPT) by VikasDocument48 pagesRisk and Rates of Returns (FM PPT) by VikasVikas Dubey100% (1)

- Đ Bích Trâm 1632300129 HW Week 4Document8 pagesĐ Bích Trâm 1632300129 HW Week 4GuruBaluLeoKingNo ratings yet

- QADM Project On EventDocument6 pagesQADM Project On Eventpearlhadeedyahoo.comNo ratings yet

- CF 21 RRDocument20 pagesCF 21 RRSoumya KhatuaNo ratings yet

- Portfolio Management PDFDocument27 pagesPortfolio Management PDFdwkr giriNo ratings yet

- Gnanamani College of Technology: Reg - NoDocument3 pagesGnanamani College of Technology: Reg - NoSabha PathyNo ratings yet

- Product Construct MayDocument8 pagesProduct Construct MaynnsriniNo ratings yet

- Bennett Atuobi Amoafo ABS0422071 - Strategic Finance IssuesDocument12 pagesBennett Atuobi Amoafo ABS0422071 - Strategic Finance Issuesben atNo ratings yet

- MFRS 8 Operating SegmentDocument2 pagesMFRS 8 Operating SegmentSree Mathi Suntheri100% (1)

- ValueResearchFundcard ICICIPrudentialGrowthInstI 2011mar14Document6 pagesValueResearchFundcard ICICIPrudentialGrowthInstI 2011mar14Ravindra MisalNo ratings yet

- Chapter 24: Portfolio Performance Evaluation: Problem SetsDocument13 pagesChapter 24: Portfolio Performance Evaluation: Problem SetsminibodNo ratings yet

- Winton - Omega Ratio PDFDocument20 pagesWinton - Omega Ratio PDFajusalNo ratings yet

- Risk AnalysisDocument56 pagesRisk AnalysissukiratvirkNo ratings yet

- Appendix To "Volatility-Managed Portfolio: Does It Really Work?"Document13 pagesAppendix To "Volatility-Managed Portfolio: Does It Really Work?"MohammadNo ratings yet

- Evaluation of StockDocument48 pagesEvaluation of StockMd Zainuddin IbrahimNo ratings yet

- Chap 5-Pages-45-46,63-119Document59 pagesChap 5-Pages-45-46,63-119RITZ BROWN100% (1)

- CH 07Document52 pagesCH 07SaMi QuReSHiNo ratings yet

- 07 Introduction To Portfolio MGTDocument52 pages07 Introduction To Portfolio MGTwempy susantoNo ratings yet

- Slide Idriss Tsafack CIREQDocument50 pagesSlide Idriss Tsafack CIREQNielNo ratings yet

- Risk & Return: Risk of A Portfolio-Uncertainty Main ViewDocument47 pagesRisk & Return: Risk of A Portfolio-Uncertainty Main ViewKazi FahimNo ratings yet

- Cba Prez 31 Jan 2021Document24 pagesCba Prez 31 Jan 2021Archisman RoyNo ratings yet

- Value at Risk Studies of Industrial Security Portfolio by Naman SwaroopDocument30 pagesValue at Risk Studies of Industrial Security Portfolio by Naman SwaroopnamanNo ratings yet

- Value RiskDocument29 pagesValue RiskNishantNo ratings yet

- Assignment 01-Fin421Document11 pagesAssignment 01-Fin421i CrYNo ratings yet

- Eicher MotorsDocument5 pagesEicher MotorsrohitNo ratings yet

- Risk & Return: WFF 2013 Financial Management Faculty of Finance & Banking Universiti Utara MalaysiaDocument48 pagesRisk & Return: WFF 2013 Financial Management Faculty of Finance & Banking Universiti Utara MalaysiaSharanya RamasamyNo ratings yet

- Single Index ModelDocument11 pagesSingle Index Modelmohamed AthnaanNo ratings yet

- CAPM - Do You Want Fries With That?Document26 pagesCAPM - Do You Want Fries With That?logreturnNo ratings yet

- Portfolio Assignment 3Document3 pagesPortfolio Assignment 3Rashedul IslamNo ratings yet

- SAPM Assignment-Ayush GoyalDocument10 pagesSAPM Assignment-Ayush Goyalkartikay GulaniNo ratings yet

- Rate of Return One ProjectDocument18 pagesRate of Return One ProjectMalek Marry Anne100% (1)

- Risk and Return LectureDocument73 pagesRisk and Return LectureAJ100% (4)

- Group 3Document24 pagesGroup 3Tanya RaghavNo ratings yet

- ExpguideDocument31 pagesExpguidecarminatNo ratings yet

- Bolton SlidesDocument21 pagesBolton SlidesWilce ProtaNo ratings yet

- CA Final SFM - New Scheme - Dawn 2022 - Portfolio ManagementDocument35 pagesCA Final SFM - New Scheme - Dawn 2022 - Portfolio Managementideasthat worthNo ratings yet

- Is Chapter 7Document21 pagesIs Chapter 7elmsaw6No ratings yet

- Mr. Madoff 'S Amazing Returns: An Analysis of The Split-Strike Conversion StrategyDocument30 pagesMr. Madoff 'S Amazing Returns: An Analysis of The Split-Strike Conversion StrategyDieter SostNo ratings yet

- Sreejith's FMDocument5 pagesSreejith's FMsrinij chilamanthulaNo ratings yet

- Capital Asset Pricing and Arbitrage Pricing Theory: Bodie, Kane, and Marcus 9 EditionDocument36 pagesCapital Asset Pricing and Arbitrage Pricing Theory: Bodie, Kane, and Marcus 9 EditionGeorgina AlpertNo ratings yet

- Financial Risk Measurement and Management: Volatility Forecast: GARCH EstimationDocument5 pagesFinancial Risk Measurement and Management: Volatility Forecast: GARCH EstimationPratik JainNo ratings yet

- FINS1612 Tutorial 4 - Investors in The Share MarketDocument10 pagesFINS1612 Tutorial 4 - Investors in The Share MarketRuben CollinsNo ratings yet

- List of the Most Important Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Key Financial RatiosFrom EverandList of the Most Important Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Key Financial RatiosNo ratings yet

- GulfDocument17 pagesGulfmastermind_2848154No ratings yet

- Accounting 315 - Quiz Business CombinationDocument3 pagesAccounting 315 - Quiz Business CombinationJoshua HongNo ratings yet

- Summer Training Project Report ON Working Capital Management of Shreyans Industries Limited (Unit:Shreyans Papers)Document73 pagesSummer Training Project Report ON Working Capital Management of Shreyans Industries Limited (Unit:Shreyans Papers)Anu TayalNo ratings yet

- CH 12Document48 pagesCH 12Nguyen Ngoc Minh Chau (K15 HL)No ratings yet

- Annexure To Trading & Demat Account Opening Form: Power of Attorney (This Document Is Voluntary)Document3 pagesAnnexure To Trading & Demat Account Opening Form: Power of Attorney (This Document Is Voluntary)Consultant NowFoundationNo ratings yet

- Annual ReportDocument180 pagesAnnual ReportParehjuiNo ratings yet

- Noakhali Gold Foods Limited: Project CostDocument19 pagesNoakhali Gold Foods Limited: Project Costaktaruzzaman bethuNo ratings yet

- The Altman Z ScoreDocument2 pagesThe Altman Z ScoreNidhi PopliNo ratings yet

- Unit 1 - Describing A CompanyDocument14 pagesUnit 1 - Describing A CompanyKouame AdjepoleNo ratings yet

- Iim Sirmaur Iim SirmaurDocument4 pagesIim Sirmaur Iim SirmaurAjay SutharNo ratings yet

- Akindele Ayoola Alfred: Customer StatementDocument16 pagesAkindele Ayoola Alfred: Customer StatementAyoola Alfred AkindeleNo ratings yet

- Case StudyDocument7 pagesCase StudyAli RazaNo ratings yet

- Application Summary FormDocument3 pagesApplication Summary FormnatalieNo ratings yet

- Blank IM DraftDocument37 pagesBlank IM DraftSachinNo ratings yet

- Study of Cash Flow ManagementDocument14 pagesStudy of Cash Flow Managementsujjish0% (2)

- XII Accounts Test With SolutionDocument12 pagesXII Accounts Test With SolutionKritika Mahalwal100% (1)

- Fix Asset OTBI Report RequestDocument1 pageFix Asset OTBI Report RequestmuhammaditzazyousafNo ratings yet

- Income Taxation SyllabusDocument6 pagesIncome Taxation SyllabusAbegail Joy CabalfinNo ratings yet

- Ratio and Fs AnalysisDocument74 pagesRatio and Fs AnalysisRubie Corpuz SimanganNo ratings yet

- Log ValidasiDocument6 pagesLog ValidasiHermanNo ratings yet

- Price and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsDocument19 pagesPrice and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsSyed Ameer Ali ShahNo ratings yet

- FIN201 Assignment Cisco Ratio AnalysisDocument23 pagesFIN201 Assignment Cisco Ratio AnalysisDark RushNo ratings yet

- at 1 October 2002 Jim Had Fixed Assets As FollowsDocument3 pagesat 1 October 2002 Jim Had Fixed Assets As FollowsHussain ShahNo ratings yet

- Chapter 13 Akun Keuangan TugasDocument2 pagesChapter 13 Akun Keuangan Tugassegeri kec0% (1)

- Homework On Presentation of Financial Statements (Ias 1)Document4 pagesHomework On Presentation of Financial Statements (Ias 1)Jazehl Joy ValdezNo ratings yet

- Soa Mftecvlons00000520xxxx 18042023 1681800203755Document8 pagesSoa Mftecvlons00000520xxxx 18042023 1681800203755mohan MudhirajNo ratings yet

- ACC 503 FinalDocument14 pagesACC 503 FinalFarid UddinNo ratings yet

- Corporate Finance Chapter 4Document15 pagesCorporate Finance Chapter 4Razan EidNo ratings yet

- Case 2Document3 pagesCase 2Naveen AttigeriNo ratings yet

Download as pdf or txt

You might also like

- Investment Analysis and Portfolio Management Reilly 10th Edition Solutions ManualDocument11 pagesInvestment Analysis and Portfolio Management Reilly 10th Edition Solutions ManualMonicaAcostagzqkx100% (77)

- Ameritrade Case PDFDocument6 pagesAmeritrade Case PDFAnish Anish100% (1)

- Capital Budgeting With Illustration and TheoryDocument145 pagesCapital Budgeting With Illustration and Theorymmuneebsda50% (2)

- Class NotesDocument16 pagesClass NotesAnika Tabassum RodelaNo ratings yet

- Portfolio Management Tutorial 4 & Chapter 4 CalculationDocument39 pagesPortfolio Management Tutorial 4 & Chapter 4 CalculationchziNo ratings yet

- BKM Chapter 7Document43 pagesBKM Chapter 7Isha0% (1)

- 3210AFE Week 4Document43 pages3210AFE Week 4Jason WestNo ratings yet

- ICMEM PresentationDocument17 pagesICMEM Presentationirfanhilmanisme93No ratings yet

- Welcome TO Project SeminorDocument18 pagesWelcome TO Project SeminorRamNo ratings yet

- Capital Market IndicesDocument50 pagesCapital Market IndicesLina AlamiNo ratings yet

- Span MethodologyDocument26 pagesSpan MethodologyMarco PoloNo ratings yet

- 1 - Session - 7 PRM 44Document18 pages1 - Session - 7 PRM 44riteshNo ratings yet

- EFM - MSESPM - Lec 5 - Risk and Return - Chapt4 - 2020Document21 pagesEFM - MSESPM - Lec 5 - Risk and Return - Chapt4 - 2020RabinNo ratings yet

- AnswersDocument7 pagesAnswersasus.mediahubNo ratings yet

- Portfolio Management Handout 2 - QuestionsDocument6 pagesPortfolio Management Handout 2 - QuestionsPriyankaNo ratings yet

- 5SOGS FM LECTURE 5 Risk and Return 1Document31 pages5SOGS FM LECTURE 5 Risk and Return 1Right Karl-Maccoy HattohNo ratings yet

- FM Ch5 Risk & ReturnDocument75 pagesFM Ch5 Risk & Returntemesgen yohannesNo ratings yet

- In The Next Three Chapters, We Will Examine Different Aspects of Capital Market Theory, IncludingDocument62 pagesIn The Next Three Chapters, We Will Examine Different Aspects of Capital Market Theory, IncludingnidamahNo ratings yet

- Risk and Rates of Returns (FM PPT) by VikasDocument48 pagesRisk and Rates of Returns (FM PPT) by VikasVikas Dubey100% (1)

- Đ Bích Trâm 1632300129 HW Week 4Document8 pagesĐ Bích Trâm 1632300129 HW Week 4GuruBaluLeoKingNo ratings yet

- QADM Project On EventDocument6 pagesQADM Project On Eventpearlhadeedyahoo.comNo ratings yet

- CF 21 RRDocument20 pagesCF 21 RRSoumya KhatuaNo ratings yet

- Portfolio Management PDFDocument27 pagesPortfolio Management PDFdwkr giriNo ratings yet

- Gnanamani College of Technology: Reg - NoDocument3 pagesGnanamani College of Technology: Reg - NoSabha PathyNo ratings yet

- Product Construct MayDocument8 pagesProduct Construct MaynnsriniNo ratings yet

- Bennett Atuobi Amoafo ABS0422071 - Strategic Finance IssuesDocument12 pagesBennett Atuobi Amoafo ABS0422071 - Strategic Finance Issuesben atNo ratings yet

- MFRS 8 Operating SegmentDocument2 pagesMFRS 8 Operating SegmentSree Mathi Suntheri100% (1)

- ValueResearchFundcard ICICIPrudentialGrowthInstI 2011mar14Document6 pagesValueResearchFundcard ICICIPrudentialGrowthInstI 2011mar14Ravindra MisalNo ratings yet

- Chapter 24: Portfolio Performance Evaluation: Problem SetsDocument13 pagesChapter 24: Portfolio Performance Evaluation: Problem SetsminibodNo ratings yet

- Winton - Omega Ratio PDFDocument20 pagesWinton - Omega Ratio PDFajusalNo ratings yet

- Risk AnalysisDocument56 pagesRisk AnalysissukiratvirkNo ratings yet

- Appendix To "Volatility-Managed Portfolio: Does It Really Work?"Document13 pagesAppendix To "Volatility-Managed Portfolio: Does It Really Work?"MohammadNo ratings yet

- Evaluation of StockDocument48 pagesEvaluation of StockMd Zainuddin IbrahimNo ratings yet

- Chap 5-Pages-45-46,63-119Document59 pagesChap 5-Pages-45-46,63-119RITZ BROWN100% (1)

- CH 07Document52 pagesCH 07SaMi QuReSHiNo ratings yet

- 07 Introduction To Portfolio MGTDocument52 pages07 Introduction To Portfolio MGTwempy susantoNo ratings yet

- Slide Idriss Tsafack CIREQDocument50 pagesSlide Idriss Tsafack CIREQNielNo ratings yet

- Risk & Return: Risk of A Portfolio-Uncertainty Main ViewDocument47 pagesRisk & Return: Risk of A Portfolio-Uncertainty Main ViewKazi FahimNo ratings yet

- Cba Prez 31 Jan 2021Document24 pagesCba Prez 31 Jan 2021Archisman RoyNo ratings yet

- Value at Risk Studies of Industrial Security Portfolio by Naman SwaroopDocument30 pagesValue at Risk Studies of Industrial Security Portfolio by Naman SwaroopnamanNo ratings yet

- Value RiskDocument29 pagesValue RiskNishantNo ratings yet

- Assignment 01-Fin421Document11 pagesAssignment 01-Fin421i CrYNo ratings yet

- Eicher MotorsDocument5 pagesEicher MotorsrohitNo ratings yet

- Risk & Return: WFF 2013 Financial Management Faculty of Finance & Banking Universiti Utara MalaysiaDocument48 pagesRisk & Return: WFF 2013 Financial Management Faculty of Finance & Banking Universiti Utara MalaysiaSharanya RamasamyNo ratings yet

- Single Index ModelDocument11 pagesSingle Index Modelmohamed AthnaanNo ratings yet

- CAPM - Do You Want Fries With That?Document26 pagesCAPM - Do You Want Fries With That?logreturnNo ratings yet

- Portfolio Assignment 3Document3 pagesPortfolio Assignment 3Rashedul IslamNo ratings yet

- SAPM Assignment-Ayush GoyalDocument10 pagesSAPM Assignment-Ayush Goyalkartikay GulaniNo ratings yet

- Rate of Return One ProjectDocument18 pagesRate of Return One ProjectMalek Marry Anne100% (1)

- Risk and Return LectureDocument73 pagesRisk and Return LectureAJ100% (4)

- Group 3Document24 pagesGroup 3Tanya RaghavNo ratings yet

- ExpguideDocument31 pagesExpguidecarminatNo ratings yet

- Bolton SlidesDocument21 pagesBolton SlidesWilce ProtaNo ratings yet

- CA Final SFM - New Scheme - Dawn 2022 - Portfolio ManagementDocument35 pagesCA Final SFM - New Scheme - Dawn 2022 - Portfolio Managementideasthat worthNo ratings yet

- Is Chapter 7Document21 pagesIs Chapter 7elmsaw6No ratings yet

- Mr. Madoff 'S Amazing Returns: An Analysis of The Split-Strike Conversion StrategyDocument30 pagesMr. Madoff 'S Amazing Returns: An Analysis of The Split-Strike Conversion StrategyDieter SostNo ratings yet

- Sreejith's FMDocument5 pagesSreejith's FMsrinij chilamanthulaNo ratings yet

- Capital Asset Pricing and Arbitrage Pricing Theory: Bodie, Kane, and Marcus 9 EditionDocument36 pagesCapital Asset Pricing and Arbitrage Pricing Theory: Bodie, Kane, and Marcus 9 EditionGeorgina AlpertNo ratings yet

- Financial Risk Measurement and Management: Volatility Forecast: GARCH EstimationDocument5 pagesFinancial Risk Measurement and Management: Volatility Forecast: GARCH EstimationPratik JainNo ratings yet

- FINS1612 Tutorial 4 - Investors in The Share MarketDocument10 pagesFINS1612 Tutorial 4 - Investors in The Share MarketRuben CollinsNo ratings yet

- List of the Most Important Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Key Financial RatiosFrom EverandList of the Most Important Financial Ratios: Formulas and Calculation Examples Defined for Different Types of Key Financial RatiosNo ratings yet

- GulfDocument17 pagesGulfmastermind_2848154No ratings yet

- Accounting 315 - Quiz Business CombinationDocument3 pagesAccounting 315 - Quiz Business CombinationJoshua HongNo ratings yet

- Summer Training Project Report ON Working Capital Management of Shreyans Industries Limited (Unit:Shreyans Papers)Document73 pagesSummer Training Project Report ON Working Capital Management of Shreyans Industries Limited (Unit:Shreyans Papers)Anu TayalNo ratings yet

- CH 12Document48 pagesCH 12Nguyen Ngoc Minh Chau (K15 HL)No ratings yet

- Annexure To Trading & Demat Account Opening Form: Power of Attorney (This Document Is Voluntary)Document3 pagesAnnexure To Trading & Demat Account Opening Form: Power of Attorney (This Document Is Voluntary)Consultant NowFoundationNo ratings yet

- Annual ReportDocument180 pagesAnnual ReportParehjuiNo ratings yet

- Noakhali Gold Foods Limited: Project CostDocument19 pagesNoakhali Gold Foods Limited: Project Costaktaruzzaman bethuNo ratings yet

- The Altman Z ScoreDocument2 pagesThe Altman Z ScoreNidhi PopliNo ratings yet

- Unit 1 - Describing A CompanyDocument14 pagesUnit 1 - Describing A CompanyKouame AdjepoleNo ratings yet

- Iim Sirmaur Iim SirmaurDocument4 pagesIim Sirmaur Iim SirmaurAjay SutharNo ratings yet

- Akindele Ayoola Alfred: Customer StatementDocument16 pagesAkindele Ayoola Alfred: Customer StatementAyoola Alfred AkindeleNo ratings yet

- Case StudyDocument7 pagesCase StudyAli RazaNo ratings yet

- Application Summary FormDocument3 pagesApplication Summary FormnatalieNo ratings yet

- Blank IM DraftDocument37 pagesBlank IM DraftSachinNo ratings yet

- Study of Cash Flow ManagementDocument14 pagesStudy of Cash Flow Managementsujjish0% (2)

- XII Accounts Test With SolutionDocument12 pagesXII Accounts Test With SolutionKritika Mahalwal100% (1)

- Fix Asset OTBI Report RequestDocument1 pageFix Asset OTBI Report RequestmuhammaditzazyousafNo ratings yet

- Income Taxation SyllabusDocument6 pagesIncome Taxation SyllabusAbegail Joy CabalfinNo ratings yet

- Ratio and Fs AnalysisDocument74 pagesRatio and Fs AnalysisRubie Corpuz SimanganNo ratings yet

- Log ValidasiDocument6 pagesLog ValidasiHermanNo ratings yet

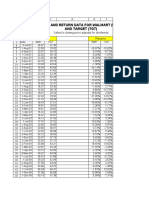

- Price and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsDocument19 pagesPrice and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsSyed Ameer Ali ShahNo ratings yet

- FIN201 Assignment Cisco Ratio AnalysisDocument23 pagesFIN201 Assignment Cisco Ratio AnalysisDark RushNo ratings yet

- at 1 October 2002 Jim Had Fixed Assets As FollowsDocument3 pagesat 1 October 2002 Jim Had Fixed Assets As FollowsHussain ShahNo ratings yet

- Chapter 13 Akun Keuangan TugasDocument2 pagesChapter 13 Akun Keuangan Tugassegeri kec0% (1)

- Homework On Presentation of Financial Statements (Ias 1)Document4 pagesHomework On Presentation of Financial Statements (Ias 1)Jazehl Joy ValdezNo ratings yet

- Soa Mftecvlons00000520xxxx 18042023 1681800203755Document8 pagesSoa Mftecvlons00000520xxxx 18042023 1681800203755mohan MudhirajNo ratings yet

- ACC 503 FinalDocument14 pagesACC 503 FinalFarid UddinNo ratings yet

- Corporate Finance Chapter 4Document15 pagesCorporate Finance Chapter 4Razan EidNo ratings yet

- Case 2Document3 pagesCase 2Naveen AttigeriNo ratings yet