Download as pdf or txt

You might also like

- Economía Europea - MartaDocument27 pagesEconomía Europea - MartaDaniel Gamarra PeñalverNo ratings yet

- Revisiting The EU Fiscal FrameworkDocument11 pagesRevisiting The EU Fiscal FrameworkRNo ratings yet

- Fixing The Euro ZoneDocument11 pagesFixing The Euro ZoneAlexandra DarmanNo ratings yet

- Euro Stability EurobondsDocument9 pagesEuro Stability EurobondsFrancisco RabyNo ratings yet

- Analysing Government Debt Sustainability in The Euro Area: ArticlesDocument15 pagesAnalysing Government Debt Sustainability in The Euro Area: ArticlesinexpugnabilNo ratings yet

- Occ Asional Paper Series: The Benefits of Fiscal Consolidation in Uncharted WatersDocument37 pagesOcc Asional Paper Series: The Benefits of Fiscal Consolidation in Uncharted WatersSofia Escária100% (1)

- Europe Under StressDocument4 pagesEurope Under StressurbanovNo ratings yet

- F 2807 SuerfDocument11 pagesF 2807 SuerfTBP_Think_TankNo ratings yet

- PC 2014 14 PDFDocument11 pagesPC 2014 14 PDFBruegelNo ratings yet

- The ECB During The Sovereign Debt Crisis Since 2009Document20 pagesThe ECB During The Sovereign Debt Crisis Since 2009nthNo ratings yet

- Monitoring Macro Economic Imbalances in Europe Proposal For A Refined Analytical FrameworkDocument16 pagesMonitoring Macro Economic Imbalances in Europe Proposal For A Refined Analytical FrameworkBruegelNo ratings yet

- Global Economic CrisisDocument3 pagesGlobal Economic CrisisShota NishnianidzeNo ratings yet

- International Business Management QBDocument12 pagesInternational Business Management QBAnonymous qAegy6GNo ratings yet

- Fiscal ConsolidationEUMarch182013Document42 pagesFiscal ConsolidationEUMarch182013nex1sNo ratings yet

- Unconventional Monetary Policy Measures - A Comparison of The Ecb, FedDocument38 pagesUnconventional Monetary Policy Measures - A Comparison of The Ecb, FedDaniel LiparaNo ratings yet

- Adair Turner: Leverage, Maturity Transformation and Financial Stability: Challenges Beyond Basel IiiDocument23 pagesAdair Turner: Leverage, Maturity Transformation and Financial Stability: Challenges Beyond Basel IiicreditplumberNo ratings yet

- Group - 9 Presents To You : Members: Ektaa Neeti Sainidhish Seweeka SoumiDocument25 pagesGroup - 9 Presents To You : Members: Ektaa Neeti Sainidhish Seweeka SoumiEktaa SipaniNo ratings yet

- Roland Berger EURECA Project 20110927Document7 pagesRoland Berger EURECA Project 20110927linkiestaNo ratings yet

- BCG Back To MesopotamiaDocument15 pagesBCG Back To MesopotamiaZerohedgeNo ratings yet

- An Action Plan For The European LeadersDocument10 pagesAn Action Plan For The European LeadersBruegelNo ratings yet

- Towards A Common European Monetary Union Risk Free Rate: Sergio Mayordomo Juan Ignacio Peña Eduardo S. SchwartzDocument56 pagesTowards A Common European Monetary Union Risk Free Rate: Sergio Mayordomo Juan Ignacio Peña Eduardo S. SchwartzsolajeroNo ratings yet

- Session 3,4,5 - Slides - Credit Institutions Under European Banking LawDocument82 pagesSession 3,4,5 - Slides - Credit Institutions Under European Banking LawThịnh NguyễnNo ratings yet

- 2021 09 06 ZEW - Fiscal DominanceDocument22 pages2021 09 06 ZEW - Fiscal DominanceXavier StraussNo ratings yet

- CCCCCCCCCCCCCCCC C C CCCC CCCC C CC CCCCCCCCCCCCCCCC C CCC C CCCCCCCCCCCCCCCCCCCCCCCCCCCCC CC CDocument9 pagesCCCCCCCCCCCCCCCC C C CCCC CCCC C CC CCCCCCCCCCCCCCCC C CCC C CCCCCCCCCCCCCCCCCCCCCCCCCCCCC CC CAmbika AchantaNo ratings yet

- Europe's Debt Crisis, Coordination Failure and International EffectsDocument49 pagesEurope's Debt Crisis, Coordination Failure and International EffectsAdrian SanduNo ratings yet

- Prof. Howard Davies PresentationDocument54 pagesProf. Howard Davies PresentationOkupacija VeiksmaiNo ratings yet

- Fiscal Free Riding of Peripheral Economies, Especially Represented by Greece, As It Is Hard To Control and Regulate National Financial InstitutionsDocument2 pagesFiscal Free Riding of Peripheral Economies, Especially Represented by Greece, As It Is Hard To Control and Regulate National Financial InstitutionsKrati AgarwalNo ratings yet

- Project Objectives and Scope: ObjectiveDocument77 pagesProject Objectives and Scope: Objectivesupriya patekarNo ratings yet

- Too Big To FailDocument3 pagesToo Big To FailРинат ДавлеевNo ratings yet

- Case Study of NextGenerationEU Report - EditedDocument9 pagesCase Study of NextGenerationEU Report - EditedFelix OdhiamboNo ratings yet

- The EU Stress Test and Sovereign Debt Exposures - by Blundell-Wignall and Slovik, Aug. 2010Document13 pagesThe EU Stress Test and Sovereign Debt Exposures - by Blundell-Wignall and Slovik, Aug. 2010FloridaHossNo ratings yet

- A Thesis Submitted For The Degree of PHD at The University of WarwickDocument163 pagesA Thesis Submitted For The Degree of PHD at The University of Warwickhamza kamalNo ratings yet

- The Role of Financial RegulationDocument15 pagesThe Role of Financial RegulationTanu GautamNo ratings yet

- Greek Debt CrisisDocument12 pagesGreek Debt Crisisjimmy_bhavanaNo ratings yet

- The Impact of The COVID-19 Pandemic On Credit Institutions and The Importance of Effective Bank Crisis Management RegimesDocument37 pagesThe Impact of The COVID-19 Pandemic On Credit Institutions and The Importance of Effective Bank Crisis Management RegimesRoberto TuestaNo ratings yet

- HE Uropean Entral Bank in THE Crisis: S E L HDocument7 pagesHE Uropean Entral Bank in THE Crisis: S E L HyszowenNo ratings yet

- DP 2011-31Document37 pagesDP 2011-31Ranulfo SobrinhoNo ratings yet

- Caiani - SFC MulticountryDocument32 pagesCaiani - SFC MulticountryorivilNo ratings yet

- Module 2 Contemporary WorldDocument4 pagesModule 2 Contemporary WorldCedric JulianNo ratings yet

- The Four Fallacies of Contemporary Austerity Policies: The Lost Keynesian LegacyDocument30 pagesThe Four Fallacies of Contemporary Austerity Policies: The Lost Keynesian LegacyEstebanAmayaNo ratings yet

- Project SyndicateDocument2 pagesProject SyndicatecorradopasseraNo ratings yet

- COVID-19 Debt Relief: Department of Economics and Finance, University of Rome Tor VergataDocument19 pagesCOVID-19 Debt Relief: Department of Economics and Finance, University of Rome Tor VergatastefgerosaNo ratings yet

- Banking in Crisis: How strategic trends will change the banking business of the futureFrom EverandBanking in Crisis: How strategic trends will change the banking business of the futureNo ratings yet

- 2018 02 Anuarioeuro 2017 para Cuando Una Banca PaneuropeaDocument21 pages2018 02 Anuarioeuro 2017 para Cuando Una Banca PaneuropeaSantiagoGarcíaNo ratings yet

- The Name Is Bond. Euro BondDocument12 pagesThe Name Is Bond. Euro BondfarhanadvaniNo ratings yet

- The Creation of Euro Area Financial Safety Nets: HighlightsDocument27 pagesThe Creation of Euro Area Financial Safety Nets: HighlightsBruegelNo ratings yet

- SSM - pr210730 Aggregate Results 5a1c5fb6bd - enDocument29 pagesSSM - pr210730 Aggregate Results 5a1c5fb6bd - enHervé MUKADINo ratings yet

- SatelliteDocument2 pagesSatelliteperig_olyaNo ratings yet

- Public and Private Risk Sharing in The Euro AreDocument20 pagesPublic and Private Risk Sharing in The Euro AreRobin WongNo ratings yet

- Telsat Bruegel PC-22-101121Document23 pagesTelsat Bruegel PC-22-101121hewett2000No ratings yet

- Bank of England, Tha Role of Macroprudential PolicyDocument38 pagesBank of England, Tha Role of Macroprudential PolicyCliffordTorresNo ratings yet

- Policy BriefingDocument4 pagesPolicy BriefingNicolaiescu GheorgeNo ratings yet

- Euro Crisis Book.Document102 pagesEuro Crisis Book.morganistNo ratings yet

- Euro Zone CrisisccDocument2 pagesEuro Zone CrisisccSami Ahmed ZiaNo ratings yet

- Albertazzi Et Al 2018Document39 pagesAlbertazzi Et Al 2018lanfeustangeNo ratings yet

- International Banking and Finance ProjectDocument11 pagesInternational Banking and Finance ProjectKishalaya PalNo ratings yet

- EU Crisis and Its Effect S: Presented by Leon Emre Taha LukeDocument10 pagesEU Crisis and Its Effect S: Presented by Leon Emre Taha Lukeemre tunaNo ratings yet

- The Level and Composition of Public Sector Debt in Emerging Market CrisesDocument35 pagesThe Level and Composition of Public Sector Debt in Emerging Market CrisesTBP_Think_TankNo ratings yet

- The Financial Crisis and the Global South: A Development PerspectiveFrom EverandThe Financial Crisis and the Global South: A Development PerspectiveNo ratings yet

- China Economic Review: Chuanglian Chen, Shujie Yao, Peiwei Hu, Yuting LinDocument22 pagesChina Economic Review: Chuanglian Chen, Shujie Yao, Peiwei Hu, Yuting LinAlyss AlysikNo ratings yet

- 283583.Vlahinic-Dizdarevic Et - Al. Sarajevo 2006 PDFDocument15 pages283583.Vlahinic-Dizdarevic Et - Al. Sarajevo 2006 PDFAlyss AlysikNo ratings yet

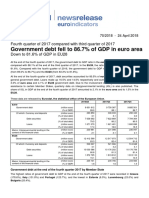

- Government Debt Fell To 86.7% of GDP in Euro Area: Fourth Quarter of 2017 Compared With Third Quarter of 2017Document4 pagesGovernment Debt Fell To 86.7% of GDP in Euro Area: Fourth Quarter of 2017 Compared With Third Quarter of 2017Alyss AlysikNo ratings yet

- The Analysis of Public Debt in Eu CountriesDocument9 pagesThe Analysis of Public Debt in Eu CountriesAlyss AlysikNo ratings yet

- Constancio-Contagion and The European Debt Crises PDFDocument13 pagesConstancio-Contagion and The European Debt Crises PDFAlyss AlysikNo ratings yet

- E Currie J J Dethier E Togo Institutional Arrangements For Public Debt Management April 2003 PDFDocument59 pagesE Currie J J Dethier E Togo Institutional Arrangements For Public Debt Management April 2003 PDFAlyss AlysikNo ratings yet

- Sovereign Debt: A Modern Greek Tragedy: Fernando M. Martin Christopher J. WallerDocument21 pagesSovereign Debt: A Modern Greek Tragedy: Fernando M. Martin Christopher J. WallerAlyss AlysikNo ratings yet

- Orhan Pamuk-Ma Numesc Rosu 1.0 10 2Document805 pagesOrhan Pamuk-Ma Numesc Rosu 1.0 10 2Alyss Alysik0% (3)

- CBSE Class 12 Accountancy Question Paper Solution SET 1 Series 2Document18 pagesCBSE Class 12 Accountancy Question Paper Solution SET 1 Series 2Mehul JindalNo ratings yet

- Homework 7 Problems and SolutionsDocument17 pagesHomework 7 Problems and Solutionswasif ahmedNo ratings yet

- Chapter 03, Math SolutionDocument8 pagesChapter 03, Math SolutionSaith UmairNo ratings yet

- Summer Internship Project: (A Project With NNEELL'S INVEST)Document45 pagesSummer Internship Project: (A Project With NNEELL'S INVEST)Aditi BagadeNo ratings yet

- Businessfinance12 q3 Mod1.1 Introduction To Financial ManagementDocument20 pagesBusinessfinance12 q3 Mod1.1 Introduction To Financial ManagementAsset Dy93% (14)

- Amtb Eft Format SpaDocument7 pagesAmtb Eft Format SpaDavid GómezNo ratings yet

- C 1Document20 pagesC 1Long AnhNo ratings yet

- Important : Allama Iqbal Open University Islamabad Allama Iqbal Open University IslamabadDocument1 pageImportant : Allama Iqbal Open University Islamabad Allama Iqbal Open University IslamabadAfzAal GraphicNo ratings yet

- Mcom Part2 FinalDocument45 pagesMcom Part2 FinalRahul SosaNo ratings yet

- Bond ValuationDocument35 pagesBond ValuationVijay SinghNo ratings yet

- Chapter 17 Other Percentage TaxesDocument7 pagesChapter 17 Other Percentage TaxesJaycee CabigaoNo ratings yet

- Câu hỏi review lý thuyết tiền tệDocument4 pagesCâu hỏi review lý thuyết tiền tệKim TiếnNo ratings yet

- 03 Literature ReviewDocument13 pages03 Literature ReviewAmitesh KumarNo ratings yet

- Financial Sectors-Deepika Bhati FIMTDocument21 pagesFinancial Sectors-Deepika Bhati FIMTNITISH BHATINo ratings yet

- Trading Volatility2 Capturing The VRMDocument9 pagesTrading Volatility2 Capturing The VRMlibra11No ratings yet

- Deutsche BrauereiDocument22 pagesDeutsche Brauereiusergurl0% (2)

- Asc 2017-12 PDFDocument405 pagesAsc 2017-12 PDFBabymetal LoNo ratings yet

- Syllabus For F.Y.BBI Course:Banking Insurance Semester: IDocument16 pagesSyllabus For F.Y.BBI Course:Banking Insurance Semester: IMukeshNo ratings yet

- Account Statement 280619 180719Document3 pagesAccount Statement 280619 180719Naresh SeerviNo ratings yet

- Account Transactions (Accrual)Document4 pagesAccount Transactions (Accrual)qy9482qrk8No ratings yet

- Statement of Axis Account No:919010012738847 For The Period (From: 08-09-2020 To: 07-09-2021)Document2 pagesStatement of Axis Account No:919010012738847 For The Period (From: 08-09-2020 To: 07-09-2021)Sayan SarkarNo ratings yet

- ECONOMICS Passing PackageDocument10 pagesECONOMICS Passing PackageNikitha Jyothi Kumar100% (7)

- Chandak Insurance Services: Magic Mix Illustration For Mr. - (Age 25)Document5 pagesChandak Insurance Services: Magic Mix Illustration For Mr. - (Age 25)Mohit DhakaNo ratings yet

- GDP - Class NotesDocument42 pagesGDP - Class NotesPeris WanjikuNo ratings yet

- Agriculture PoliciesDocument1 pageAgriculture PoliciesDebjit ChatterjeeNo ratings yet

- Problems Chapter Hybrid Financing 04032024 124444pmDocument41 pagesProblems Chapter Hybrid Financing 04032024 124444pmumarjamil032No ratings yet

- Blowing The Lid On World History and The Hidden PowersDocument129 pagesBlowing The Lid On World History and The Hidden PowersSeoirse DionysosNo ratings yet

- Cheque IntDocument6 pagesCheque Intneo_yasserNo ratings yet

- Op Transaction History 03!09!2023Document2 pagesOp Transaction History 03!09!2023Kuljinder SinghNo ratings yet

- Corporate Finace 1 PDFDocument4 pagesCorporate Finace 1 PDFwafflesNo ratings yet