Download as doc, pdf, or txt

You might also like

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- Archbishop Reyes Ave, Cebu City, Cebu, 6000Document5 pagesArchbishop Reyes Ave, Cebu City, Cebu, 6000Ralf Arthur Silverio100% (1)

- ChargebackDocument14 pagesChargebackShweta Sandhu0% (1)

- Ans Mini Case 2 - A171 - LecturerDocument14 pagesAns Mini Case 2 - A171 - LecturerXue Yin Lew100% (1)

- Professional Examination IiDocument55 pagesProfessional Examination IiFuchoin ReikoNo ratings yet

- LH 9 - Final Accounts ProblemsDocument29 pagesLH 9 - Final Accounts ProblemsHarshavardhanNo ratings yet

- Caribbean Holding LTD Is A Manufacturer of Cricket Balls CALCULATION QUESTIONDocument3 pagesCaribbean Holding LTD Is A Manufacturer of Cricket Balls CALCULATION QUESTIONJoiAntoineNo ratings yet

- p7sgp 2011 Dec QDocument10 pagesp7sgp 2011 Dec QamNo ratings yet

- Budget Template - With Sample ContentsDocument78 pagesBudget Template - With Sample ContentsAlvin FadulNo ratings yet

- Business Taxation: (Malawi)Document8 pagesBusiness Taxation: (Malawi)angaNo ratings yet

- Jun 2019 QDocument9 pagesJun 2019 Qsiti dalinaNo ratings yet

- Adam's Learning Centre, Lahore: Company AccountsDocument6 pagesAdam's Learning Centre, Lahore: Company AccountsMasood Ahmad AadamNo ratings yet

- Mba ZC415 Ec-3r First Sem 2022-2023Document4 pagesMba ZC415 Ec-3r First Sem 2022-2023Ravi KaviNo ratings yet

- Examination Paper: Ba Accounting & Finance Level Five Financial Accounting 5AG006 (RESIT)Document8 pagesExamination Paper: Ba Accounting & Finance Level Five Financial Accounting 5AG006 (RESIT)Boago PhatshwaneNo ratings yet

- Exercise 6 25Document8 pagesExercise 6 25junjunNo ratings yet

- 2-3mwi 2004 Dec ADocument13 pages2-3mwi 2004 Dec Aanga100% (1)

- Business Taxation: (Malawi)Document11 pagesBusiness Taxation: (Malawi)angaNo ratings yet

- M14 Pilot PaperDocument24 pagesM14 Pilot PaperKA LAI SoNo ratings yet

- Cap II Group I RTP Dec2023Document84 pagesCap II Group I RTP Dec2023pratyushmudbhari340No ratings yet

- First Semester M.B.A. Degree Examination, March 2020 Course - 3: Accounting For ManagersDocument7 pagesFirst Semester M.B.A. Degree Examination, March 2020 Course - 3: Accounting For ManagersChaithanya ChaithuNo ratings yet

- Mirri TaxDocument10 pagesMirri TaxMandanda LovemoreNo ratings yet

- Compreh Problems - AAA - SolutionDocument28 pagesCompreh Problems - AAA - SolutionNicola NaberNo ratings yet

- Problem Exercises AnswerDocument6 pagesProblem Exercises AnswersaphirejunelNo ratings yet

- CH 2 Reconciliation StatementDocument4 pagesCH 2 Reconciliation StatementHarshil ParekhNo ratings yet

- Business Taxation: (Malawi)Document10 pagesBusiness Taxation: (Malawi)angaNo ratings yet

- Befa Grand Test 2022Document2 pagesBefa Grand Test 2022cyberdrip1No ratings yet

- CCP102Document13 pagesCCP102api-3849444No ratings yet

- Final Accouts Unsolved QuestionsDocument27 pagesFinal Accouts Unsolved Questionsmayank shridharNo ratings yet

- P6 Princiiples of Taxation QJ17Document12 pagesP6 Princiiples of Taxation QJ17angaNo ratings yet

- 2020 1 Accounting in Organisations and Society Assignment-3Document7 pages2020 1 Accounting in Organisations and Society Assignment-3Abs PangaderNo ratings yet

- Incomplete Records MTQDocument5 pagesIncomplete Records MTQqas4476pubNo ratings yet

- Amended - Final - Unit 5 - AAB-Accounting Principles - A2Document6 pagesAmended - Final - Unit 5 - AAB-Accounting Principles - A2Quang MinhNo ratings yet

- WorksheetDocument37 pagesWorksheetKim FloresNo ratings yet

- Handout 1 Adjusting Entries Adjusted Trial Balance Financial Statements Answer KeyDocument3 pagesHandout 1 Adjusting Entries Adjusted Trial Balance Financial Statements Answer KeyKris Dela CruzNo ratings yet

- Dec2019 PDFDocument12 pagesDec2019 PDFArief HilmanNo ratings yet

- Audit Practice & Assurance Services: Professional 2 Examination - August 2017Document19 pagesAudit Practice & Assurance Services: Professional 2 Examination - August 2017Vitalis MbuyaNo ratings yet

- Advanced TaxationDocument6 pagesAdvanced TaxationGIVEN N SIPANJENo ratings yet

- Taxation: Maicsa - Icsa International Qualifying Scheme (Iqs)Document25 pagesTaxation: Maicsa - Icsa International Qualifying Scheme (Iqs)diviananaslinNo ratings yet

- Taxation Solution 2018 SeptemberDocument9 pagesTaxation Solution 2018 SeptemberIffah NasuhaaNo ratings yet

- Level Four Code 3 Answer-1Document7 pagesLevel Four Code 3 Answer-1EdomNo ratings yet

- CHPTR 7 Worksheet DemoDocument1 pageCHPTR 7 Worksheet DemoParamorfsNo ratings yet

- AccountingDocument5 pagesAccountingAndrea Joy PekNo ratings yet

- Answer For Exam Five Project One GivenDocument6 pagesAnswer For Exam Five Project One GivenGuddataa DheekkamaaNo ratings yet

- Ac1104 Week1illDocument12 pagesAc1104 Week1illmjxncwk7nbNo ratings yet

- Reconciliation Statement MathDocument6 pagesReconciliation Statement MathRajibNo ratings yet

- Quiz Lab AkmDocument20 pagesQuiz Lab AkmAdib PramanaNo ratings yet

- 66088bos53351inter p3Document34 pages66088bos53351inter p3Asfarin ShaikhNo ratings yet

- Practice QNSDocument2 pagesPractice QNSIan chisemaNo ratings yet

- Professional - May 2021Document173 pagesProfessional - May 2021Jason Baba KwagheNo ratings yet

- Past Year QuestionDocument6 pagesPast Year QuestionNurulHuda Auni Binti Ab RahmanNo ratings yet

- Tutorial 2: Swedish CompanyDocument5 pagesTutorial 2: Swedish Companyszh saNo ratings yet

- MSA 1 Winter 2018Document17 pagesMSA 1 Winter 2018Faisal Abbas MB-19-47No ratings yet

- Sunway T4 (TX4014) - Tax Computation (Business Income)Document4 pagesSunway T4 (TX4014) - Tax Computation (Business Income)Ee LynnNo ratings yet

- Ent Buss Chapter 5Document16 pagesEnt Buss Chapter 5Muhammad AtifNo ratings yet

- Compre Audit Cieloflawless Q PDFDocument3 pagesCompre Audit Cieloflawless Q PDFCarina Mae Valdez ValenciaNo ratings yet

- Ch.6-Tutorial 1Document3 pagesCh.6-Tutorial 1NURSABRINA BINTI ROSLI (BG)No ratings yet

- 1663923012kelani Cables PLC Annual Report 2021Document128 pages1663923012kelani Cables PLC Annual Report 2021Sasindu GimhanNo ratings yet

- Prelim Exam Part 2 SolutionsDocument4 pagesPrelim Exam Part 2 SolutionseaeNo ratings yet

- Attachment AccountingDocument6 pagesAttachment Accountingtaylor swiftyyyNo ratings yet

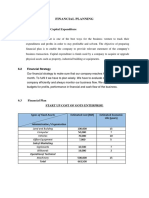

- Financial Planning: 6.1 Start-Up Cost and Capital ExpenditureDocument4 pagesFinancial Planning: 6.1 Start-Up Cost and Capital ExpenditurearefeenaNo ratings yet

- Business Income TutorialDocument5 pagesBusiness Income TutorialzulfikriNo ratings yet

- Advanced Accounting 2eDocument3 pagesAdvanced Accounting 2eHarusiNo ratings yet

- Ingredients" Viewed at 4 September 2013.Document1 pageIngredients" Viewed at 4 September 2013.leerenjyeNo ratings yet

- Diploma in Business Management: Semester Final ExaminationDocument4 pagesDiploma in Business Management: Semester Final ExaminationleerenjyeNo ratings yet

- There Offeror Is The Person Who Makes An Offer andDocument2 pagesThere Offeror Is The Person Who Makes An Offer andleerenjyeNo ratings yet

- Diploma in Business Management:: Business Law Exam Date: 15 / 07 / 2011 Exam Time: 8:30 - 11:30a.mDocument3 pagesDiploma in Business Management:: Business Law Exam Date: 15 / 07 / 2011 Exam Time: 8:30 - 11:30a.mleerenjyeNo ratings yet

- Recommendations: - Ethical Conduct of Coca-Cola Is Important For Social Norms, Employee Conduct, and Public RelationsDocument4 pagesRecommendations: - Ethical Conduct of Coca-Cola Is Important For Social Norms, Employee Conduct, and Public RelationsleerenjyeNo ratings yet

- Business Ethics SlideDocument20 pagesBusiness Ethics SlideleerenjyeNo ratings yet

- Ethical Conduct of Coca-Cola: - Community Projects and Partnerships Aligned With Our CRS ObjectivesDocument12 pagesEthical Conduct of Coca-Cola: - Community Projects and Partnerships Aligned With Our CRS ObjectivesleerenjyeNo ratings yet

- CIR V British Salmson Aero Engines LTDDocument1 pageCIR V British Salmson Aero Engines LTDleerenjyeNo ratings yet

- Business Ethics SlideDocument21 pagesBusiness Ethics SlideleerenjyeNo ratings yet

- ExampleDocument1 pageExampleleerenjyeNo ratings yet

- CIR V British Salmson Aero Engines LTDDocument1 pageCIR V British Salmson Aero Engines LTDleerenjyeNo ratings yet

- Compensation Is TaxableDocument1 pageCompensation Is TaxableleerenjyeNo ratings yet

- Difference Between Trading and Capital IncomeDocument1 pageDifference Between Trading and Capital IncomeleerenjyeNo ratings yet

- Business Maths. AssignmentDocument4 pagesBusiness Maths. AssignmentleerenjyeNo ratings yet

- Labor Cost AccountingDocument6 pagesLabor Cost AccountingleerenjyeNo ratings yet

- Taking Off Sheet T D S Description T D S Description: Perimeter 38.30 +38.30 +1.40+1.40 79.40Document5 pagesTaking Off Sheet T D S Description T D S Description: Perimeter 38.30 +38.30 +1.40+1.40 79.40leerenjyeNo ratings yet

- QS Practices 1 (Assignment) - Interview QuestionsDocument6 pagesQS Practices 1 (Assignment) - Interview QuestionsleerenjyeNo ratings yet

- Company Law Chapter 10Document11 pagesCompany Law Chapter 10leerenjyeNo ratings yet

- Notice For Credit Card Holders On RBI's COVID-19 Relief: Page 1 of 4Document4 pagesNotice For Credit Card Holders On RBI's COVID-19 Relief: Page 1 of 4cr4satyajitNo ratings yet

- OFI-GST - Functional Tax Computation For O2C - Phase1Document56 pagesOFI-GST - Functional Tax Computation For O2C - Phase1Rana7540100% (3)

- Indian GST Reference ManualDocument594 pagesIndian GST Reference ManualY M Shah & Co100% (5)

- Chapter 2 Corporations IntDocument64 pagesChapter 2 Corporations IntRachel Sayson100% (1)

- Payment SlipDocument2 pagesPayment SlipAlphie PabloNo ratings yet

- 2023 02 16 17 54 04nov 22 - 600053Document6 pages2023 02 16 17 54 04nov 22 - 600053narendran kNo ratings yet

- TDS - and - TCS Rate Chart 2025Document5 pagesTDS - and - TCS Rate Chart 2025jsparakhNo ratings yet

- Tax Invoice: Scan To ReturnDocument1 pageTax Invoice: Scan To ReturnVIJAY SAININo ratings yet

- Definition of Terms: GROSS INCOME: Classification of Taxpayers, Compensation Income, and Business IncomeDocument13 pagesDefinition of Terms: GROSS INCOME: Classification of Taxpayers, Compensation Income, and Business IncomeSKEETER BRITNEY COSTANo ratings yet

- Synerquest-Public Training Schedule For Oct-Dec 2013 Ver14Document3 pagesSynerquest-Public Training Schedule For Oct-Dec 2013 Ver14Robin RubinaNo ratings yet

- Tax of Transfer of Real Property OwnershipDocument3 pagesTax of Transfer of Real Property OwnershipGerard DGNo ratings yet

- 13 Accenture, Inc. v. Commissioner of Internal RevenueDocument9 pages13 Accenture, Inc. v. Commissioner of Internal RevenueChristian Edward CoronadoNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)AK तकNo ratings yet

- Vietnam Tax Legal HandbookDocument52 pagesVietnam Tax Legal HandbookaNo ratings yet

- The Candidate Has To Report in Person As Per Schedule. Delayed Reporting Without Prior Approval From The Competent Authority Will Not Be Accepted For AdmissionDocument23 pagesThe Candidate Has To Report in Person As Per Schedule. Delayed Reporting Without Prior Approval From The Competent Authority Will Not Be Accepted For AdmissionshivamNo ratings yet

- Bengaluru City University: Exam Application FormDocument1 pageBengaluru City University: Exam Application FormMadhu KrishNo ratings yet

- Chapter 2 MCQs On House PropertyDocument24 pagesChapter 2 MCQs On House PropertyRam Iyer100% (1)

- The FollowingDocument2 pagesThe FollowingAnthony Angel TejaresNo ratings yet

- American Revolution Exit TicketDocument2 pagesAmerican Revolution Exit TicketMs. HorneNo ratings yet

- Chapter 4 For FilingDocument9 pagesChapter 4 For Filinglagurr100% (1)

- Citizen PTR Receipt (2023-2024)Document1 pageCitizen PTR Receipt (2023-2024)AnmolBansalNo ratings yet

- Deductions From Gross Income 2 1Document42 pagesDeductions From Gross Income 2 1Katherine EderosasNo ratings yet

- Premium Receipt: Harsha Patil Contact Number: 9611700115 Email ID: Pharsha1515@yahoo - Co.in Client DetailsDocument1 pagePremium Receipt: Harsha Patil Contact Number: 9611700115 Email ID: Pharsha1515@yahoo - Co.in Client DetailsHarshaNo ratings yet

- Í Jn5Sè Ryanârepolloâbesi Rya R Ç2F' 2lî Ryan Repollo BesidDocument3 pagesÍ Jn5Sè Ryanârepolloâbesi Rya R Ç2F' 2lî Ryan Repollo Besidraymund12345No ratings yet

- View StatementDocument2 pagesView StatementexohguilianaNo ratings yet

- How To Register For Maha Behes 2018Document2 pagesHow To Register For Maha Behes 2018reetikaNo ratings yet

- Tl11a 15eDocument1 pageTl11a 15esmian08No ratings yet

- Duty Free Philippines V BIRDocument2 pagesDuty Free Philippines V BIRTheodore0176No ratings yet