Download as docx, pdf, or txt

You might also like

- FINAN 6220 - Target Case Study AnswersDocument2 pagesFINAN 6220 - Target Case Study AnswerschandanaNo ratings yet

- Delhi Metro Case StudyDocument26 pagesDelhi Metro Case StudyAnsari Faizullah100% (1)

- Case Study Mumbai Harbour LinkDocument4 pagesCase Study Mumbai Harbour LinkSagar Patel100% (1)

- Public Private Partnerships: Presented by Jerry Fay, PEDocument29 pagesPublic Private Partnerships: Presented by Jerry Fay, PEPrav Srivastava100% (1)

- Delhi Gurgaon Expressway (Bot)Document6 pagesDelhi Gurgaon Expressway (Bot)Avinash KommireddiNo ratings yet

- What Hedge Funds Really Do - An Introduction To Portfolio Management PDFDocument104 pagesWhat Hedge Funds Really Do - An Introduction To Portfolio Management PDFRutav shahNo ratings yet

- Case Study Hyderabad Metro: K Avinash 18MCT0028Document5 pagesCase Study Hyderabad Metro: K Avinash 18MCT0028AvinashNo ratings yet

- A Case Study On Hyderabad Metro Rail Project: Masters of TechnologyDocument13 pagesA Case Study On Hyderabad Metro Rail Project: Masters of TechnologyAvinash Kommireddi100% (1)

- PM Mumbai Metro PPPDocument30 pagesPM Mumbai Metro PPPNafeesur Rahman KhanNo ratings yet

- PDF Hyd MetroDocument13 pagesPDF Hyd MetroChakuliNo ratings yet

- Vaibhav: Erm Project Hyderabad Metro RailDocument25 pagesVaibhav: Erm Project Hyderabad Metro RailNikhil SachdevaNo ratings yet

- Ey Public Private Partnership The Next ContinuumDocument32 pagesEy Public Private Partnership The Next ContinuumPulokesh GhoshNo ratings yet

- Yuthish Prabakar R - Module EDocument3 pagesYuthish Prabakar R - Module EYuthish Prabakar RNo ratings yet

- Model Concession AgreementDocument32 pagesModel Concession AgreementManish R. PatelNo ratings yet

- Development Projects at The Year 2012 L&TDocument13 pagesDevelopment Projects at The Year 2012 L&TDurai Tamil GamerNo ratings yet

- Rajasthan Mega Highways ProjectDocument45 pagesRajasthan Mega Highways ProjectRohit RameshNo ratings yet

- Risks in A PPP Project:: Development RiskDocument21 pagesRisks in A PPP Project:: Development RiskKaran AggarwalNo ratings yet

- Financing ModuleDocument79 pagesFinancing ModuleVivek Kumar YadavNo ratings yet

- Hydro Power Projects: Recent Trends in Bidding: Presented by Rajiv Malhotra COODocument37 pagesHydro Power Projects: Recent Trends in Bidding: Presented by Rajiv Malhotra COOarvindNo ratings yet

- Presentation to Chairman NHADocument48 pagesPresentation to Chairman NHAmohammadtalhaijazNo ratings yet

- Chapter 12Document29 pagesChapter 12BS Nanjunda SwamyNo ratings yet

- Risk Assesment of Mumbai MetroDocument62 pagesRisk Assesment of Mumbai MetroshikshasNo ratings yet

- Mumbai MetroDocument23 pagesMumbai MetroTarun AnandNo ratings yet

- Infrastructure Finance News March 30 2015 April 05 2015Document3 pagesInfrastructure Finance News March 30 2015 April 05 2015YaIpha NaOremNo ratings yet

- EDFC - Through PPP ModeDocument44 pagesEDFC - Through PPP ModeMd. Shiraz JinnathNo ratings yet

- Class 5 - Transportation InfrastructureDocument21 pagesClass 5 - Transportation InfrastructureSmr OnlyNo ratings yet

- Need For Metro: Project DescriptionDocument3 pagesNeed For Metro: Project DescriptionPrashanth Babu.K100% (1)

- GMR Investor PresentationDocument45 pagesGMR Investor PresentationmanboombaamNo ratings yet

- RInfra Investor Presentation December 10Document46 pagesRInfra Investor Presentation December 10Omar 'Metric' JaleelNo ratings yet

- Hydro Power Projects: Recent Trends in Bidding: Presented by Rajiv Malhotra COODocument37 pagesHydro Power Projects: Recent Trends in Bidding: Presented by Rajiv Malhotra COODheeraj SehgalNo ratings yet

- Irb Ar 2012-13Document148 pagesIrb Ar 2012-13Shikhin GargNo ratings yet

- World Bank PresentationDocument38 pagesWorld Bank Presentationsunnydargan91No ratings yet

- How To Improve PPP Projects in IndiaDocument3 pagesHow To Improve PPP Projects in IndiaHimanshu KashyapNo ratings yet

- Public-Private Partnership (PPP) in Airport Infrastructure: Ministry of Civil AviationDocument21 pagesPublic-Private Partnership (PPP) in Airport Infrastructure: Ministry of Civil AviationruhimeggiNo ratings yet

- 23 Gujarat PPP BhattacharyaDocument24 pages23 Gujarat PPP BhattacharyaSwapneel VaijanapurkarNo ratings yet

- Yuthish Prabakar R - Module FDocument3 pagesYuthish Prabakar R - Module FYuthish Prabakar RNo ratings yet

- Group 4 - Delhi - Gurgaon.Document17 pagesGroup 4 - Delhi - Gurgaon.Ketan ShahNo ratings yet

- Ipf - HMRDocument24 pagesIpf - HMRJimit SalotNo ratings yet

- Vadodara Halol Toll Road ProjectDocument19 pagesVadodara Halol Toll Road Projectsushant_agrawal_2No ratings yet

- SAPL - TIIC 1crDocument28 pagesSAPL - TIIC 1crMathura PackingNo ratings yet

- Upholding Sanctity of Contracts - Case Study of Hyderabad Metro Rail ProjectDocument22 pagesUpholding Sanctity of Contracts - Case Study of Hyderabad Metro Rail Projectankur guptaNo ratings yet

- Gairung - Kathmandu RailwayDocument11 pagesGairung - Kathmandu Railwaysahil sahNo ratings yet

- Crisil Opinion Ham in A JamDocument7 pagesCrisil Opinion Ham in A JamMohit BhatiaNo ratings yet

- Public Private PartnershipDocument25 pagesPublic Private PartnershipDr Sarbesh Mishra100% (1)

- Hybrid Annuity Model in Road Infrastructure ProjectsDocument12 pagesHybrid Annuity Model in Road Infrastructure ProjectsIJRASETPublicationsNo ratings yet

- Mumbai Metro Rail Project: Group - 8Document30 pagesMumbai Metro Rail Project: Group - 8akash srivastavaNo ratings yet

- D.M.R.C. Winter Training SCADADocument77 pagesD.M.R.C. Winter Training SCADASarthakBhatia100% (1)

- Case Study - ExpresswayDocument8 pagesCase Study - ExpresswayVNo ratings yet

- Study On Recruitment and Selection ProcessDocument122 pagesStudy On Recruitment and Selection ProcessSmartydr100% (1)

- Executive Summary: 1. BackgroundDocument9 pagesExecutive Summary: 1. BackgroundVenkatakrishnan IyerNo ratings yet

- Ip StudyDocument37 pagesIp StudyDHANA LAKSHMINo ratings yet

- A. Dept of Economic Affairs, Ministry of Finance, Govt of IndiaDocument5 pagesA. Dept of Economic Affairs, Ministry of Finance, Govt of IndiaaparajitatNo ratings yet

- GnanaselvamAyyappasamy (15 0)Document4 pagesGnanaselvamAyyappasamy (15 0)Mohanram PandiNo ratings yet

- IRB Invit FundDocument6 pagesIRB Invit FundPavanNo ratings yet

- Delhi Metro Case Study PDFDocument15 pagesDelhi Metro Case Study PDFAvinash Ajit SinghNo ratings yet

- Project Report: "Consumer Behaviour of Airtel"Document95 pagesProject Report: "Consumer Behaviour of Airtel"Sudhakar KarkeraNo ratings yet

- GMR Infrastructure Ltd. Announces Stake Sale in Transmission Projects To Adani Transmission Ltd. (Company Update)Document3 pagesGMR Infrastructure Ltd. Announces Stake Sale in Transmission Projects To Adani Transmission Ltd. (Company Update)Shyam SunderNo ratings yet

- Submitted To:-Submitted By: - Prof. A.B. Raju Rashika Gupta (M00111) Bhanu Pratap (Moo151) Shaiva Shah (M00153)Document25 pagesSubmitted To:-Submitted By: - Prof. A.B. Raju Rashika Gupta (M00111) Bhanu Pratap (Moo151) Shaiva Shah (M00153)Rashika GuptaNo ratings yet

- Final GMR UpdatedDocument20 pagesFinal GMR UpdatedSudhir SinghNo ratings yet

- The Delhi Metro ProjectDocument13 pagesThe Delhi Metro ProjectVikas SainiNo ratings yet

- GMR Corporate Presentation PPT - LatestDocument29 pagesGMR Corporate Presentation PPT - Latestsamrob17No ratings yet

- Creative Management: Shilpi Kumari Roll-120102 Section-BDocument4 pagesCreative Management: Shilpi Kumari Roll-120102 Section-BTanu SinghNo ratings yet

- The Project BackgroundDocument6 pagesThe Project BackgroundTanu SinghNo ratings yet

- Chandragupt Institute of Management Patna PGDM:2019-2021 BatchDocument1 pageChandragupt Institute of Management Patna PGDM:2019-2021 BatchTanu SinghNo ratings yet

- Https WWW - Finlatics.com Pdfs Certificates 16328 CertificateDocument1 pageHttps WWW - Finlatics.com Pdfs Certificates 16328 CertificateTanu SinghNo ratings yet

- Group Discussion Group No Applicant ID Candidate NameDocument8 pagesGroup Discussion Group No Applicant ID Candidate NameTanu SinghNo ratings yet

- Senior Profile Merged - 190920 - 16Document1 pageSenior Profile Merged - 190920 - 16Tanu SinghNo ratings yet

- Chandrayaan-2 Mission: India's Mission To MoonDocument12 pagesChandrayaan-2 Mission: India's Mission To MoonTanu SinghNo ratings yet

- Porter'S Five Forces (Banking and Finance)Document2 pagesPorter'S Five Forces (Banking and Finance)Tanu SinghNo ratings yet

- Chandrayaan-2 Mission: India's Mission To MoonDocument12 pagesChandrayaan-2 Mission: India's Mission To MoonTanu SinghNo ratings yet

- J1103015962 PDFDocument4 pagesJ1103015962 PDFTanu SinghNo ratings yet

- Career Objective: TH THDocument1 pageCareer Objective: TH THTanu SinghNo ratings yet

- It For Managers: Analysis of MotorolaDocument13 pagesIt For Managers: Analysis of MotorolaTanu SinghNo ratings yet

- Career Objective Academic Credentials: TH THDocument1 pageCareer Objective Academic Credentials: TH THTanu SinghNo ratings yet

- Research Insight: 1: A Research Report of Telecom Sector ON Bharti Airtel LimitedDocument16 pagesResearch Insight: 1: A Research Report of Telecom Sector ON Bharti Airtel LimitedTanu SinghNo ratings yet

- Make in India Initiative: A Key For Sustainable Growth: December 2017Document9 pagesMake in India Initiative: A Key For Sustainable Growth: December 2017Tanu SinghNo ratings yet

- Sector Project 1: Telcom: Bargaining Power of Buyers - Generally The Two Types of Buyer in Telecom Industry IncludesDocument2 pagesSector Project 1: Telcom: Bargaining Power of Buyers - Generally The Two Types of Buyer in Telecom Industry IncludesTanu SinghNo ratings yet

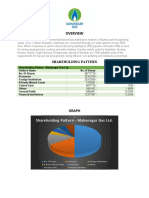

- Shareholding Patt Ern - Mahanagar Gas LTDDocument4 pagesShareholding Patt Ern - Mahanagar Gas LTDTanu SinghNo ratings yet

- Research Insight: 2: A Research Report of Telecom Sector ON Tata Communications LimitedDocument9 pagesResearch Insight: 2: A Research Report of Telecom Sector ON Tata Communications LimitedTanu SinghNo ratings yet

- Eshghi Kamran Finalsubmission2018december PHDDocument295 pagesEshghi Kamran Finalsubmission2018december PHDTanu SinghNo ratings yet

- Consumers Product Preference & Perceived RiskDocument2 pagesConsumers Product Preference & Perceived RiskTanu SinghNo ratings yet

- A Case Study On QTDocument8 pagesA Case Study On QTTanu SinghNo ratings yet

- TMTCP Team 45 DenmarkDocument16 pagesTMTCP Team 45 DenmarkTanu SinghNo ratings yet

- Consumers Product Preference & Perceived RiskDocument2 pagesConsumers Product Preference & Perceived RiskTanu SinghNo ratings yet

- Understanding The Dynamics of Bull and Bear Markets Types Strategies and Practical Applications F 20231004071047L052Document10 pagesUnderstanding The Dynamics of Bull and Bear Markets Types Strategies and Practical Applications F 20231004071047L052Aani RashNo ratings yet

- 1 NVCDocument27 pages1 NVCAnida AhmadNo ratings yet

- Gary Smith, Margaret Smith - The Power of Modern Value Investing - Beyond Indexing, Algos, and Alpha-Palgrave Macmillan (2024)Document195 pagesGary Smith, Margaret Smith - The Power of Modern Value Investing - Beyond Indexing, Algos, and Alpha-Palgrave Macmillan (2024)Jyotishman SahaNo ratings yet

- CE On Shareholders' EquityDocument2 pagesCE On Shareholders' EquityCharles TuazonNo ratings yet

- Finance BIS MCQs & TF Ch7Document4 pagesFinance BIS MCQs & TF Ch7Souliman MuhammadNo ratings yet

- ACST2001: Financial ModellingDocument42 pagesACST2001: Financial ModellingNam Nam NamNo ratings yet

- List of Hedge Funds From OdpDocument5 pagesList of Hedge Funds From OdpChris AbbottNo ratings yet

- Financial Aspects IntroductionDocument5 pagesFinancial Aspects IntroductionSef Getizo Cado67% (3)

- Index Watch:: EPIC Research ReportDocument8 pagesIndex Watch:: EPIC Research Reportapi-211507971No ratings yet

- CFA Level II 3 Topics - High Yield List of QuestionsDocument4 pagesCFA Level II 3 Topics - High Yield List of QuestionsCatalinNo ratings yet

- Ammann Tracking Error Variance Decomposition FinalDocument37 pagesAmmann Tracking Error Variance Decomposition Finalswinki3No ratings yet

- INVESTMENT ANALYSIS & PORTFOLIO MANAGEMENT 17th Dec, 2020 PDFDocument4 pagesINVESTMENT ANALYSIS & PORTFOLIO MANAGEMENT 17th Dec, 2020 PDFVidushi ThapliyalNo ratings yet

- 23.03.27 SW the-PutCall-ratio-As-A-contrarian-market-timing-Indicator (2022, Fabian Scheler, PCR As A Contrarian Indicator)Document4 pages23.03.27 SW the-PutCall-ratio-As-A-contrarian-market-timing-Indicator (2022, Fabian Scheler, PCR As A Contrarian Indicator)Rolf ScheiderNo ratings yet

- Capital Structure Case Study - QDocument2 pagesCapital Structure Case Study - Qrosario correiaNo ratings yet

- Final Publish Paper ABDocument15 pagesFinal Publish Paper ABJayesh AdakmolNo ratings yet

- KRDTop100SFM PDFDocument215 pagesKRDTop100SFM PDFNag Sai NarahariNo ratings yet

- MSCI ESG Research - Bruno RauisDocument15 pagesMSCI ESG Research - Bruno RauisValerio ScaccoNo ratings yet

- Accounting Assignment DraftDocument4 pagesAccounting Assignment DraftMargeNo ratings yet

- BIS Structured FinanceDocument63 pagesBIS Structured Financeandrealuzzi0No ratings yet

- Ar 2010Document272 pagesAr 2010Shehani ThilakshikaNo ratings yet

- Interm1 Quiz Module 12 & 13Document4 pagesInterm1 Quiz Module 12 & 13finn mertensNo ratings yet

- Lessons Learned From Commodities CorporationDocument3 pagesLessons Learned From Commodities CorporationLonewolf99No ratings yet

- Group 1Document13 pagesGroup 1Siddharth Singh TomarNo ratings yet

- Priyanka Jha CLLG ProjectDocument80 pagesPriyanka Jha CLLG Projectpriyanka jhaNo ratings yet

- Beginning Balances of Ivan & FrederickDocument13 pagesBeginning Balances of Ivan & FrederickRaluca ToneNo ratings yet

- Equity and Social Justice: Madame C.J. Walker AND Reginald LewisDocument10 pagesEquity and Social Justice: Madame C.J. Walker AND Reginald LewisHaovangDonglien KipgenNo ratings yet

- EverFi Planning Fort Your Future NOTESDocument17 pagesEverFi Planning Fort Your Future NOTESYamileth Nino MoranNo ratings yet

- Foreign Direct Investment in IndiaDocument30 pagesForeign Direct Investment in Indiadevesh bhattNo ratings yet