Download as pdf or txt

You might also like

- Performance Task No 2 - Group Work - Planning Concepts and Tools P1Document8 pagesPerformance Task No 2 - Group Work - Planning Concepts and Tools P1Corn SaladNo ratings yet

- Sources and Uses of Short Term and Long Term FundsDocument7 pagesSources and Uses of Short Term and Long Term FundsSyrill Cayetano0% (1)

- Chapter 1 An Overview of FinanceDocument6 pagesChapter 1 An Overview of FinanceSyrill CayetanoNo ratings yet

- Business Finance Week 4Document3 pagesBusiness Finance Week 4JayMoralesNo ratings yet

- LESSON 10 Business TransactionsDocument8 pagesLESSON 10 Business TransactionsUnamadable UnleomarableNo ratings yet

- Accounting 2 - 2nd ModuleDocument8 pagesAccounting 2 - 2nd ModuleJessalyn Sarmiento Tancio100% (1)

- Typical Account Titles UsedDocument3 pagesTypical Account Titles Usedwenna janeNo ratings yet

- Module 1 - Business Transaction and Their Analysis Part 1Document12 pagesModule 1 - Business Transaction and Their Analysis Part 11BSA5-ABM Espiritu, CharlesNo ratings yet

- Abm General and Special JournalDocument63 pagesAbm General and Special JournalEstelle Gammad33% (3)

- Case AnalysisDocument1 pageCase Analysismarissa casareno almuete0% (1)

- Fabm2 Q2 M4 - 4 CsefDocument20 pagesFabm2 Q2 M4 - 4 CsefZeus MalicdemNo ratings yet

- Financial Statement Analysis Part 2Document10 pagesFinancial Statement Analysis Part 2Kim Patrick VictoriaNo ratings yet

- Accounting Fundamentals: The Accounting Equation and The Double-Entry SystemDocument70 pagesAccounting Fundamentals: The Accounting Equation and The Double-Entry SystemAllana Mier100% (1)

- FABM REVIEWER 2nd QUARTERDocument5 pagesFABM REVIEWER 2nd QUARTERMikaella Adriana GoNo ratings yet

- Statement of Cash Flows (SCF)Document23 pagesStatement of Cash Flows (SCF)Florante De LeonNo ratings yet

- Fabm 2: LEARNING ACTIVITIES - Statement of Comprehensive Income (SCI)Document2 pagesFabm 2: LEARNING ACTIVITIES - Statement of Comprehensive Income (SCI)Cameron VelascoNo ratings yet

- Cash Flow StatementDocument10 pagesCash Flow StatementSheilaMarieAnnMagcalasNo ratings yet

- Fabm2 Module Week 1Document8 pagesFabm2 Module Week 1Mylene Santiago100% (1)

- FundamentalsofAccounting IDSDocument2 pagesFundamentalsofAccounting IDSYu Babylan33% (3)

- ACTIVITY. On February 1, 20A4, Mira Delamar Opened A Store That SellsDocument1 pageACTIVITY. On February 1, 20A4, Mira Delamar Opened A Store That SellsMiguel Lulab100% (1)

- Accounting Cycle of A Merchandising Business: Prepared By: Prof. Jonah C. PardilloDocument41 pagesAccounting Cycle of A Merchandising Business: Prepared By: Prof. Jonah C. PardilloRoxe XNo ratings yet

- Basic Accounting Module 4Document11 pagesBasic Accounting Module 4Kristine Lou BaddongNo ratings yet

- Assessment QuizDocument2 pagesAssessment QuizFrancis Raagas67% (3)

- Module 11 - Fabm 1 - Merchandising InventoryDocument20 pagesModule 11 - Fabm 1 - Merchandising Inventoryjosefh martin cruz100% (1)

- AccountantsDocument15 pagesAccountantsJenny EvangelistaNo ratings yet

- After Paul's Guitar Shop, Inc. Records Its and Posts Them To Ledger Accounts, It Prepares This Unadjusted Trial BalanceDocument7 pagesAfter Paul's Guitar Shop, Inc. Records Its and Posts Them To Ledger Accounts, It Prepares This Unadjusted Trial Balancekenshi ihsnekNo ratings yet

- Lesson 6 Accounting For Merchandising Business Part 2 ExercisesDocument9 pagesLesson 6 Accounting For Merchandising Business Part 2 ExercisesTalented Kim SunooNo ratings yet

- Inventories With Lower Cost, Without Sacrificing Its QualityDocument4 pagesInventories With Lower Cost, Without Sacrificing Its QualityMark Lyndon YmataNo ratings yet

- Activity:: I. Define The Following TermsDocument3 pagesActivity:: I. Define The Following TermsAnonymousNo ratings yet

- Review of Journal Entries, T-Accounts, General Ledger, and Trial BalanceDocument25 pagesReview of Journal Entries, T-Accounts, General Ledger, and Trial BalanceVISITACION JAIRUS GWEN100% (1)

- 4 - BF - For STUDENTSDocument47 pages4 - BF - For STUDENTSPhill SamonteNo ratings yet

- Abm - 12 - Fabm2 - q1 - Clas2 - Prep of Sci - v8 - Rhea Ann NavillaDocument22 pagesAbm - 12 - Fabm2 - q1 - Clas2 - Prep of Sci - v8 - Rhea Ann NavillaKim Yessamin MadarcosNo ratings yet

- Budget and PlanningDocument9 pagesBudget and Planningyes1nthNo ratings yet

- Fundamentals of AccountingDocument83 pagesFundamentals of AccountingJaylien CruzzNo ratings yet

- Luyong - 4TH Q - Fabm1Document3 pagesLuyong - 4TH Q - Fabm1Jonavi LuyongNo ratings yet

- JKL Company Statement of Financial Position For The Year 2015 & 2016 JKL CompanyDocument2 pagesJKL Company Statement of Financial Position For The Year 2015 & 2016 JKL CompanyHazel Gumapon100% (2)

- Adjusting Entries Service BusinessDocument18 pagesAdjusting Entries Service BusinessrichelleNo ratings yet

- Chapter 9 Basic Reconcillation StatementDocument11 pagesChapter 9 Basic Reconcillation StatementRon louise Pereyra100% (1)

- AccountingDocument26 pagesAccountingRheen Clarin0% (1)

- Business Finance: Time Value of MoneyDocument15 pagesBusiness Finance: Time Value of MoneyAngelica Paras100% (1)

- Chapter 1 2 3Document14 pagesChapter 1 2 3Airon BendañaNo ratings yet

- Analysis of Common Business TransactionsDocument18 pagesAnalysis of Common Business TransactionsClarisse RosalNo ratings yet

- Chart of Accounts General Ledger General Ledger Page No. Page No. Assets IncomeDocument44 pagesChart of Accounts General Ledger General Ledger Page No. Page No. Assets IncomeJireh RiveraNo ratings yet

- Cash Balance Per Bank Versus Per BookDocument6 pagesCash Balance Per Bank Versus Per BookSyrill CayetanoNo ratings yet

- M4 Prac Exer. 2Document10 pagesM4 Prac Exer. 2Jasmine ActaNo ratings yet

- Business Finance: Mrs. Leah O. RualesDocument28 pagesBusiness Finance: Mrs. Leah O. RualesCleofe Sobiaco100% (1)

- Test Question For Exam Chapter 1 To 6Document4 pagesTest Question For Exam Chapter 1 To 6Cherryl ValmoresNo ratings yet

- Financial Planning Tools and Concepts pt.1: Learning ModuleDocument33 pagesFinancial Planning Tools and Concepts pt.1: Learning Moduledaphne ramosNo ratings yet

- Chapter 9 Financial Forecasting For Strategic GrowthDocument18 pagesChapter 9 Financial Forecasting For Strategic GrowthMa. Jhoan DailyNo ratings yet

- ABM PM 2nd QTR SLM Week12Document9 pagesABM PM 2nd QTR SLM Week12ganda dyosaNo ratings yet

- ACEFIAR Quiz No. 7Document2 pagesACEFIAR Quiz No. 7Marriel Fate CullanoNo ratings yet

- Accounting Concepts and PrinciplesDocument18 pagesAccounting Concepts and PrinciplesCharissa Jamis ChingwaNo ratings yet

- Dental Clinic AnswerDocument16 pagesDental Clinic AnswerMaria Licuanan100% (1)

- GHI Company Comparative Balance Sheet For The Year 2015 & 2016Document3 pagesGHI Company Comparative Balance Sheet For The Year 2015 & 2016Kl HumiwatNo ratings yet

- Senior High School Department: Quarter 3 - Module 8: Merchandising Concern (Part 1)Document9 pagesSenior High School Department: Quarter 3 - Module 8: Merchandising Concern (Part 1)Jaye RuantoNo ratings yet

- Final ModuleDocument3 pagesFinal ModuleAnnabelle MancoNo ratings yet

- Fabm2 Module 2Document21 pagesFabm2 Module 2Rea Mariz Jordan50% (2)

- Journal Entry DiscussionDocument8 pagesJournal Entry DiscussionAyesha Eunice SalvaleonNo ratings yet

- LORENZOPABLOMARKETINGPLAN2021Document13 pagesLORENZOPABLOMARKETINGPLAN2021France Delos SantosNo ratings yet

- Abm Fabm2 q2w2 Abcdwith AnswerkeyDocument10 pagesAbm Fabm2 q2w2 Abcdwith AnswerkeyElla Marie LagosNo ratings yet

- Fabm 2Document170 pagesFabm 2Asti GumacaNo ratings yet

- Chapter 6 Service Culture and Its Importance in BPODocument15 pagesChapter 6 Service Culture and Its Importance in BPOSyrill CayetanoNo ratings yet

- BPO Business ModelsDocument3 pagesBPO Business ModelsSyrill CayetanoNo ratings yet

- Chapter 5 Strategies For Successful OutsourcingDocument11 pagesChapter 5 Strategies For Successful OutsourcingSyrill CayetanoNo ratings yet

- Chapter 7 Building A Service-Oriented Culture Within An OrganizationDocument18 pagesChapter 7 Building A Service-Oriented Culture Within An OrganizationSyrill CayetanoNo ratings yet

- Chapter 4 Managing Outsourcing RelationshipsDocument12 pagesChapter 4 Managing Outsourcing RelationshipsSyrill CayetanoNo ratings yet

- IT To Basic Process Operation Efficiency ManagementDocument6 pagesIT To Basic Process Operation Efficiency ManagementSyrill CayetanoNo ratings yet

- Chapter 1 Overview of Business Process Outsourcing (BPO)Document17 pagesChapter 1 Overview of Business Process Outsourcing (BPO)Syrill CayetanoNo ratings yet

- Chapter 8 Measuring and Improving Service QualityDocument12 pagesChapter 8 Measuring and Improving Service QualitySyrill CayetanoNo ratings yet

- Role of Securities and Exchange Commission at The Philippine Stock ExchangeDocument7 pagesRole of Securities and Exchange Commission at The Philippine Stock ExchangeSyrill CayetanoNo ratings yet

- Chapter 5 Financial AnalysisDocument7 pagesChapter 5 Financial AnalysisSyrill Cayetano100% (1)

- Philippines Stock ExchangeDocument4 pagesPhilippines Stock ExchangeSyrill CayetanoNo ratings yet

- Chapter 7 Importance of Money and Capital MarketsDocument9 pagesChapter 7 Importance of Money and Capital MarketsSyrill CayetanoNo ratings yet

- Chapter 5 Financial AnalysisDocument7 pagesChapter 5 Financial AnalysisSyrill Cayetano100% (1)

- Unit 15 Pre-Test Marketing and Test MarketingDocument10 pagesUnit 15 Pre-Test Marketing and Test MarketingSyrill CayetanoNo ratings yet

- Introduction To Business Finance: Chapter 1 An Overview of FinanceDocument3 pagesIntroduction To Business Finance: Chapter 1 An Overview of FinanceSyrill CayetanoNo ratings yet

- Chapter 1: Product Management - Introduction To Product Management UnitDocument2 pagesChapter 1: Product Management - Introduction To Product Management UnitSyrill CayetanoNo ratings yet

- Unit 8 Branding DecisionsDocument4 pagesUnit 8 Branding DecisionsSyrill CayetanoNo ratings yet

- Unit 9 Positioning DecisionsDocument4 pagesUnit 9 Positioning DecisionsSyrill CayetanoNo ratings yet

- Unit 14 Concept Development and TestingDocument8 pagesUnit 14 Concept Development and TestingSyrill CayetanoNo ratings yet

- Unit 12 Organising For New Product DevelopmentDocument10 pagesUnit 12 Organising For New Product DevelopmentSyrill CayetanoNo ratings yet

- Ssignment RiefDocument6 pagesSsignment RiefShah MuradNo ratings yet

- Highly Confidential Quiz Bowl QuestionsDocument3 pagesHighly Confidential Quiz Bowl QuestionsCy WallNo ratings yet

- 04 - COA SamplesDocument4 pages04 - COA SamplesJonalyn MalicdanNo ratings yet

- Chapter Five Decision Making and Relevant Information Information and The Decision ProcessDocument10 pagesChapter Five Decision Making and Relevant Information Information and The Decision ProcesskirosNo ratings yet

- Assignment 2 SolutionDocument3 pagesAssignment 2 SolutionarwaNo ratings yet

- Tax2 TRAIN 8.5x13Document64 pagesTax2 TRAIN 8.5x13Kim EstalNo ratings yet

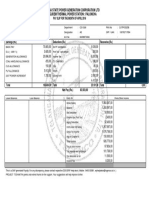

- Telangana State Power Generation Corporation LTD Kothagudem Thermal Power Station: PalonchaDocument1 pageTelangana State Power Generation Corporation LTD Kothagudem Thermal Power Station: PalonchaKANNE NITHINNo ratings yet

- Cost Accounting Hilton 14Document13 pagesCost Accounting Hilton 14Vin TenNo ratings yet

- Chapter 6 - Consolidated Financial Statements (Part 3)Document41 pagesChapter 6 - Consolidated Financial Statements (Part 3)Rena Jocelle NalzaroNo ratings yet

- FA2 Part 6Document3 pagesFA2 Part 6uzma qadirNo ratings yet

- Monthly Remittance Return of Income Taxes Withheld On CompensationDocument4 pagesMonthly Remittance Return of Income Taxes Withheld On CompensationHanabishi RekkaNo ratings yet

- Job Aid For Taxpayers - How To Fill Up 1702-MX Version 2013Document35 pagesJob Aid For Taxpayers - How To Fill Up 1702-MX Version 2013matthew02012010No ratings yet

- CTA Case Filinvest Devt Corp V CIRDocument5 pagesCTA Case Filinvest Devt Corp V CIRsaintkarriNo ratings yet

- Auditing Theory TEST BANKDocument23 pagesAuditing Theory TEST BANKGelyn CruzNo ratings yet

- Accounting 3 & 4 - 07 Fundamentals of Acctg 2Document10 pagesAccounting 3 & 4 - 07 Fundamentals of Acctg 2Kristine Salvador CayetanoNo ratings yet

- Accounts Receivable: Chartered Institute of Internal AuditorsDocument7 pagesAccounts Receivable: Chartered Institute of Internal AuditorsClarice GuintibanoNo ratings yet

- Theoretical Problems: Chapter Deductions Out Gross Total (Including of Income Tax)Document25 pagesTheoretical Problems: Chapter Deductions Out Gross Total (Including of Income Tax)chandrani4029No ratings yet

- Corporation Law Notes Under Atty Ladia RevisedDocument78 pagesCorporation Law Notes Under Atty Ladia Revisedcarlo_tabangcuraNo ratings yet

- Indian Capital Goods - HSBC Jan 2011Document298 pagesIndian Capital Goods - HSBC Jan 2011didwaniasNo ratings yet

- Annexure V Comparative ChartDocument4 pagesAnnexure V Comparative ChartRaju HalderNo ratings yet

- Golf Course ProposalDocument3 pagesGolf Course ProposalTara MeltonNo ratings yet

- Richard Fuld Punched in Face in Lehman Brothers GymDocument21 pagesRichard Fuld Punched in Face in Lehman Brothers GymAkash saxenaNo ratings yet

- Privatization of PIA 1Document16 pagesPrivatization of PIA 1Ayesha ParachaNo ratings yet

- Asst. Prof. Rishi Dev ALS AUMDocument9 pagesAsst. Prof. Rishi Dev ALS AUMjoy parimalaNo ratings yet

- Indirect-Tax - Sem VI PDFDocument73 pagesIndirect-Tax - Sem VI PDFMaheswar SethiNo ratings yet

- Chapter 11 v2Document14 pagesChapter 11 v2Sheilamae Sernadilla GregorioNo ratings yet

- BSBFIM601 Hints For Task 2Document32 pagesBSBFIM601 Hints For Task 2Mohammed MGNo ratings yet

- 078 Federal Income TaxDocument67 pages078 Federal Income Taxcitygirl518No ratings yet

- 16-1 Hospital Supply IncDocument4 pages16-1 Hospital Supply IncFrancisco Marvin100% (1)

- Income Tax, Tax RemDocument23 pagesIncome Tax, Tax RemAlyanna CabralNo ratings yet