Download as xls, pdf, or txt

You might also like

- Bir Tax 2022Document79 pagesBir Tax 2022DENNIS RAMIREZNo ratings yet

- Bir Tax Deadlines 2015Document2 pagesBir Tax Deadlines 2015Mary Grace BanezNo ratings yet

- 2020 Kempal Bir Loa DocsDocument5 pages2020 Kempal Bir Loa DocsPajarillo Kathy AnnNo ratings yet

- Bir Sales 20221220Document38 pagesBir Sales 20221220Thomas Daniel CuarteroNo ratings yet

- Monthly Report - Current and Past Due Loans 2021Document2 pagesMonthly Report - Current and Past Due Loans 2021Mark Kevin IIINo ratings yet

- Payroll-Register - SEPTEMBER 1-15, 2021Document1 pagePayroll-Register - SEPTEMBER 1-15, 2021Ransey Ace AndalloNo ratings yet

- Bir 2023 SalesDocument128 pagesBir 2023 SalesMark Christian BentijabaNo ratings yet

- Alphalist of Employees Q1-2021 FINALDocument84 pagesAlphalist of Employees Q1-2021 FINALvivian deocampoNo ratings yet

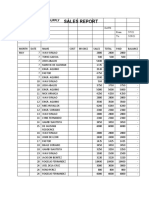

- Sales Report: Hcs Construction SupplyDocument3 pagesSales Report: Hcs Construction SupplyAzzia Morante LopezNo ratings yet

- Construction Materials Price Lists As of April 2017 Item Price Concrete WorksDocument16 pagesConstruction Materials Price Lists As of April 2017 Item Price Concrete WorksJohnRichieLTanNo ratings yet

- Tax ComputationDocument4 pagesTax Computationrfso16No ratings yet

- Billing Spread Sheet Form For Non - STP ProjectsDocument22 pagesBilling Spread Sheet Form For Non - STP ProjectsJay Mel Allan MarinduqueNo ratings yet

- Inventory Bir FinalDocument172 pagesInventory Bir FinalKim Espart CastilloNo ratings yet

- Visa Japan App LetterDocument1 pageVisa Japan App LettervegachanNo ratings yet

- 267731702final PDFDocument5 pages267731702final PDFelmarcomonal100% (1)

- Bir Form 1600 - Schedule Ii Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of April, 2019Document5 pagesBir Form 1600 - Schedule Ii Alphabetical List of Payees From Whom Taxes Were Withheld For The Month of April, 2019Pau Line EscosioNo ratings yet

- SalamatDocument132 pagesSalamatCaila Chin DinoyNo ratings yet

- RMC 11-2018 PDFDocument1 pageRMC 11-2018 PDFMichael James Madrid MalinginNo ratings yet

- Amendatory PPDocument109 pagesAmendatory PPMatet Escolano SamonteNo ratings yet

- Certificate of Compensation Payment/Tax Withheld: Rivera St. San Francisco, Red-V, Ibabang Dupay, Lucena CityDocument2 pagesCertificate of Compensation Payment/Tax Withheld: Rivera St. San Francisco, Red-V, Ibabang Dupay, Lucena CityACYATAN & CO., CPAs 2020No ratings yet

- BIR-CASH-RECEIPTS-JOURNAL ExcelDocument11 pagesBIR-CASH-RECEIPTS-JOURNAL ExcelGlaiza SantosNo ratings yet

- Tax Profile: Last Audit by RO PANSARDocument54 pagesTax Profile: Last Audit by RO PANSARHakimmala MacudNo ratings yet

- T1 Adjustments Letter 2020 05 11 23 24 21 808Document2 pagesT1 Adjustments Letter 2020 05 11 23 24 21 808Marina KiklevskaNo ratings yet

- Sworn Application For Tax Clearance For Bidding Purposes - EdrDocument2 pagesSworn Application For Tax Clearance For Bidding Purposes - Edranabua0% (1)

- Bir Form 1701 Summary Alphalist of Withholding Taxes (Sawt) For The Month of December, 2018Document5 pagesBir Form 1701 Summary Alphalist of Withholding Taxes (Sawt) For The Month of December, 2018lemor xalicaNo ratings yet

- 1601EDocument7 pages1601EEnrique Membrere SupsupNo ratings yet

- Journal Entry Voucher: National Housing Authority AgencyDocument22 pagesJournal Entry Voucher: National Housing Authority AgencyJENNIFER SIALANANo ratings yet

- Annex C-1 - Summary of System DescriptionDocument4 pagesAnnex C-1 - Summary of System DescriptionChristian Albert HerreraNo ratings yet

- Authority To PrintDocument5 pagesAuthority To PrintKyungsoo PenguinNo ratings yet

- 1702Q SGC - 2nd QTR 2019 FOR EMAILDocument31 pages1702Q SGC - 2nd QTR 2019 FOR EMAILJaylou BobisNo ratings yet

- Table of ContentsDocument1 pageTable of ContentsMacLaw MacOfficeNo ratings yet

- 01 January 2023 LRDocument42 pages01 January 2023 LRMAY-ANN ZONIONo ratings yet

- Certification: Issued This 8th Day of January, 2021. City of Manila, PhilippinesDocument1 pageCertification: Issued This 8th Day of January, 2021. City of Manila, PhilippinesRubie Anne SaducosNo ratings yet

- Sarahs Gen Journal TemplateDocument5 pagesSarahs Gen Journal TemplateLoey ParkNo ratings yet

- Cda Red FR 003 Rev7 CaprDocument32 pagesCda Red FR 003 Rev7 CaprRaina Phia PantaleonNo ratings yet

- Pbcom V CirDocument9 pagesPbcom V CirAbby ParwaniNo ratings yet

- 2307 New Template Ni PauDocument37 pages2307 New Template Ni Pau175pauNo ratings yet

- Iti Acceptance ListDocument29 pagesIti Acceptance Listapi-24129274967% (3)

- RMC 72-2004 PDFDocument9 pagesRMC 72-2004 PDFBobby LockNo ratings yet

- Vat July 2015Document83 pagesVat July 2015Anonymous TFqbYJNo ratings yet

- TaxDocument6 pagesTaxChristian GonzalesNo ratings yet

- PDFDocument8 pagesPDFLeah MoscareNo ratings yet

- Energy Cost & Consumption History: Billing Date Billing Period Total Bill Amount (PHP) VATDocument2 pagesEnergy Cost & Consumption History: Billing Date Billing Period Total Bill Amount (PHP) VATDoroty CastroNo ratings yet

- BIR AUGUST 2022 Sales PurchasesDocument13 pagesBIR AUGUST 2022 Sales PurchasesReyes Accounting Law OfficeNo ratings yet

- Efps Letter 009Document1 pageEfps Letter 009ElsieJhadeWandasAmandoNo ratings yet

- New Eilc Company ProfileDocument5 pagesNew Eilc Company ProfileCliffe D. GonzalesNo ratings yet

- Expanded Withholding Tax SeminarDocument20 pagesExpanded Withholding Tax SeminarkirkoNo ratings yet

- Letter To PAG IBIGDocument1 pageLetter To PAG IBIGRomy Angel CabreraNo ratings yet

- BIR Returns SummaryDocument7 pagesBIR Returns SummarySanta Dela Cruz NaluzNo ratings yet

- Eoyt 2020Document1 pageEoyt 2020Izza Joy MartinezNo ratings yet

- Etps LandbankDocument1 pageEtps LandbankMARY ROSE BERNADASNo ratings yet

- 2019 01 Jan Relief Purchases Template-FGSDocument35 pages2019 01 Jan Relief Purchases Template-FGSZydrick KunNo ratings yet

- Old Form 0605 PDFDocument2 pagesOld Form 0605 PDFeugene badere50% (2)

- Bir Registration RequirementsDocument47 pagesBir Registration RequirementsYus CeballosNo ratings yet

- Ending InventoryDocument70 pagesEnding InventoryThomas Daniel CuarteroNo ratings yet

- Annex C - TCVC (Individual)Document3 pagesAnnex C - TCVC (Individual)cbsacctg0920No ratings yet

- BIR FORM 2307 SampleDocument6 pagesBIR FORM 2307 SampleEasyHear Philippines by NuGen Hearing Devices, Inc.No ratings yet

- BIR Registration & Due Dates-1Document6 pagesBIR Registration & Due Dates-1jessicamarieogbinar37No ratings yet

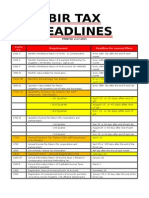

- BIR Tax Deadlines: Home About Us Services Clientele Contact UsDocument2 pagesBIR Tax Deadlines: Home About Us Services Clientele Contact UsNICKOL NAMOCNo ratings yet

- BIR Tax DeadlinesDocument2 pagesBIR Tax Deadlinesimports.fcfilesNo ratings yet

- S183R1 02Document16 pagesS183R1 02Yahia Luay DarweeshNo ratings yet

- Government Procurement Reform ActDocument191 pagesGovernment Procurement Reform ActAlyssa SiychaNo ratings yet

- Cement July 2021Document25 pagesCement July 2021dhinesh dNo ratings yet

- Tilenga - Tas-Wsc Res KampalaDocument2 pagesTilenga - Tas-Wsc Res KampalaDario BitettiNo ratings yet

- Franklin V Behar - Platon DeclarationDocument6 pagesFranklin V Behar - Platon DeclarationTHROnlineNo ratings yet

- Consolidation Worksheets: NSS Exploring Economics 3 (3 Edition)Document17 pagesConsolidation Worksheets: NSS Exploring Economics 3 (3 Edition)Rachel LeeNo ratings yet

- Auditing and Its Objective in NepalDocument10 pagesAuditing and Its Objective in NepalNyimaSherpaNo ratings yet

- Final Arbitration AwardDocument15 pagesFinal Arbitration AwardSitus TurtleNo ratings yet

- Quote For - DMIAGRP For Projector & Accessories August 2020Document1 pageQuote For - DMIAGRP For Projector & Accessories August 2020raviezsoftNo ratings yet

- Advanced English Transitions (Hereby.... )Document2 pagesAdvanced English Transitions (Hereby.... )Gabriel BorgesNo ratings yet

- Requirements For BMBE ApplicationDocument1 pageRequirements For BMBE ApplicationJulius Espiga ElmedorialNo ratings yet

- Blue Bell BSNL Urban Greens - 99acresDocument2 pagesBlue Bell BSNL Urban Greens - 99acresRaghu Mohan AlamandaNo ratings yet

- 2022 05 18 10 41Document169 pages2022 05 18 10 41BUSHRA ABDUL KALIQNo ratings yet

- 2023 06 11 18 02 55 Statement - 1699273975024Document9 pages2023 06 11 18 02 55 Statement - 1699273975024Anandhu SNo ratings yet

- Handbook of Decentralised Governance and Development in India (D. Rajasekhar, (Ed.) ) (Z-Library)Document361 pagesHandbook of Decentralised Governance and Development in India (D. Rajasekhar, (Ed.) ) (Z-Library)Lubna RizviNo ratings yet

- Globalization in The 1990sDocument8 pagesGlobalization in The 1990sBhanu MehraNo ratings yet

- Cgia Compendium 2021 EditionDocument348 pagesCgia Compendium 2021 EditionCG LTJG GUERRERO PRECIOUS LEANELLIE UNo ratings yet

- StatementDocument15 pagesStatementVishal BawaneNo ratings yet

- Amazon InvoiceDocument1 pageAmazon InvoiceJaideep SinghNo ratings yet

- A To Z Pmy Sum 9 SeptDocument1 pageA To Z Pmy Sum 9 SeptPravendra SinghNo ratings yet

- SALESDocument4 pagesSALESbandam sai krishnaNo ratings yet

- Commissioner v. Algue, G.R. No. L-28896, 1988Document2 pagesCommissioner v. Algue, G.R. No. L-28896, 1988Jeffrey Medina100% (1)

- Application DetailsDocument3 pagesApplication Detailsshreyshaw21No ratings yet

- Affidavit of Land Holding. Heirs of Titiwa.8.29.2022Document1 pageAffidavit of Land Holding. Heirs of Titiwa.8.29.2022black stalkerNo ratings yet

- Why The Sangguniang Kabataan Needs An OverhaulDocument6 pagesWhy The Sangguniang Kabataan Needs An OverhaulArolf PatacsilNo ratings yet

- LL. B. V Term Paper - LB - 5034 - Intellectual Property Law - IIDocument6 pagesLL. B. V Term Paper - LB - 5034 - Intellectual Property Law - IIPulkitNo ratings yet

- OS21998315 PremiumPaymentCertificateDocument1 pageOS21998315 PremiumPaymentCertificateSoumyaranjan SwainNo ratings yet

- Barclays Colombia Outlook June 2023Document16 pagesBarclays Colombia Outlook June 2023La Silla VacíaNo ratings yet

- Form PDF 338116400010723Document9 pagesForm PDF 338116400010723R c GuptaNo ratings yet

- Brigada Eskwela Pworkplan: Francisco Oringo Sr. Elementary SchoolDocument3 pagesBrigada Eskwela Pworkplan: Francisco Oringo Sr. Elementary SchoolPrecilla HalagoNo ratings yet