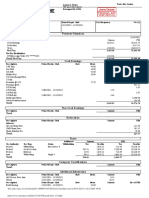

American Credit Acceptance Receivables Trust 2021-1 American Credit Acceptance Receivables Trust 2021-1

American Credit Acceptance Receivables Trust 2021-1 American Credit Acceptance Receivables Trust 2021-1

You might also like

- BIR Rulings On Change of Useful LifeDocument6 pagesBIR Rulings On Change of Useful LifeCarlota Nicolas VillaromanNo ratings yet

- FWB June 2021 Financials by LlamaDocument7 pagesFWB June 2021 Financials by LlamaShreyas HariharanNo ratings yet

- Revolut Stay and Spend LetterDocument2 pagesRevolut Stay and Spend LetterJonathan KeaneNo ratings yet

- RatingsDirect PresalePlanetFitnessMasterIssuerLLCSeries20181 39312924 Jul-23-2019Document18 pagesRatingsDirect PresalePlanetFitnessMasterIssuerLLCSeries20181 39312924 Jul-23-2019ougyajNo ratings yet

- Lead Schedule Fixed AssetDocument9 pagesLead Schedule Fixed Assetkelvin hervangga18No ratings yet

- CH.2 InterestDocument41 pagesCH.2 InterestJenalyn MacarilayNo ratings yet

- Carmax S&PDocument15 pagesCarmax S&Ptrust2386No ratings yet

- Honda Auto Receivables 2021-3 Owner Trust Honda Auto Receivables 2021-3 Owner TrustDocument15 pagesHonda Auto Receivables 2021-3 Owner Trust Honda Auto Receivables 2021-3 Owner Trustsprite2lNo ratings yet

- Sabey Data Center Issuer LLC (Series 2022-1) Sabey Data Center Issuer LLC (Series 2022-1)Document20 pagesSabey Data Center Issuer LLC (Series 2022-1) Sabey Data Center Issuer LLC (Series 2022-1)kouroumaNo ratings yet

- 2023-01-01 00-00-00-StatementDocument4 pages2023-01-01 00-00-00-StatementCarolina MartinsNo ratings yet

- INC.0012 Monthly Disbursments AURADocument23 pagesINC.0012 Monthly Disbursments AURAedwilsonjafarxNo ratings yet

- Estim 20951-00 2024-03-31 Ffalchi 11 653219 BatchuserDocument8 pagesEstim 20951-00 2024-03-31 Ffalchi 11 653219 Batchuserpelleriti2694No ratings yet

- Jockey Club Ti-I College F.4 Business, Accounting and Financial Studies Second Term Examination (2020-2021)Document5 pagesJockey Club Ti-I College F.4 Business, Accounting and Financial Studies Second Term Examination (2020-2021)ouo So方No ratings yet

- Fundcard: Edelweiss Low Duration Fund - Direct PlanDocument4 pagesFundcard: Edelweiss Low Duration Fund - Direct PlanYogi173No ratings yet

- ValueResearchFundcard FranklinIndiaUltraShortBondFund SuperInstitutionalPlan DirectPlan 2017oct11Document4 pagesValueResearchFundcard FranklinIndiaUltraShortBondFund SuperInstitutionalPlan DirectPlan 2017oct11jamsheer.aaNo ratings yet

- Stelco National BankDocument5 pagesStelco National BankForexliveNo ratings yet

- BppuDocument2 pagesBppuni made safitriNo ratings yet

- MDS Abril 2022Document2 pagesMDS Abril 2022edwilsonjafarxNo ratings yet

- Legg Mason Value Fund - Dec 2022 PDFDocument2 pagesLegg Mason Value Fund - Dec 2022 PDFJeanmarNo ratings yet

- M.P. ResultDocument1 pageM.P. Resultgautamji8151No ratings yet

- Press Release New Sapna Granite Industries: Details of Instruments/facilities in Annexure-1Document3 pagesPress Release New Sapna Granite Industries: Details of Instruments/facilities in Annexure-1Ravi BabuNo ratings yet

- Bhaivav Laxmi Ma Galla Bhandar7677Document14 pagesBhaivav Laxmi Ma Galla Bhandar7677Ravi KarnaNo ratings yet

- US Flow of Funds 07sept2022Document39 pagesUS Flow of Funds 07sept2022scribbugNo ratings yet

- MDS Out 2022Document2 pagesMDS Out 2022edwilsonjafarxNo ratings yet

- Compak Suggested AnswersDocument8 pagesCompak Suggested Answersknprop134No ratings yet

- Saob 2022 With RecordsDocument2 pagesSaob 2022 With RecordsJustin DonesNo ratings yet

- Nike PIB 2021Document222 pagesNike PIB 2021Emperor OverwatchNo ratings yet

- Impairment Revaluation and Intangibles Acctg 3 Intermediate Accounting IDocument47 pagesImpairment Revaluation and Intangibles Acctg 3 Intermediate Accounting IMarjorie PalmaNo ratings yet

- Companies GL 2021 MemoDocument4 pagesCompanies GL 2021 MemoJayden KaydrnNo ratings yet

- Activision Blizzard, Inc: Data OverviewDocument7 pagesActivision Blizzard, Inc: Data OverviewPratyush ShakyaNo ratings yet

- REO Outreach 2022-11-01 UIDocument29 pagesREO Outreach 2022-11-01 UIJonathan NainggolanNo ratings yet

- RoyalBankofCanadaTSXRY PublicCompanyDocument1 pageRoyalBankofCanadaTSXRY PublicCompanyGDoingThings YTNo ratings yet

- APOLLO Series 2017-1 TrustDocument16 pagesAPOLLO Series 2017-1 TrustQuant_GeekNo ratings yet

- COSCO - PH Cosco Capital Inc. Financial Statements - WSJDocument1 pageCOSCO - PH Cosco Capital Inc. Financial Statements - WSJjannahaaliyahdNo ratings yet

- ValueResearchFundcard BarodaPioneerShortTermBondFund DirectPlan 2017may16Document4 pagesValueResearchFundcard BarodaPioneerShortTermBondFund DirectPlan 2017may16Achint KumarNo ratings yet

- Crisil GR&A - Bank - Bank of America NADocument9 pagesCrisil GR&A - Bank - Bank of America NANguyễn Bùi Phương DungNo ratings yet

- Franklin Resources, Inc.: Stock Report - March 12, 2022 - NYSE Symbol: BEN - BEN Is in The S&P 500Document9 pagesFranklin Resources, Inc.: Stock Report - March 12, 2022 - NYSE Symbol: BEN - BEN Is in The S&P 500apdusp2No ratings yet

- Data On Central Government Debt For The Quarter Ended December 2021 (Q4)Document1 pageData On Central Government Debt For The Quarter Ended December 2021 (Q4)Dhanesk KANo ratings yet

- Cambio 1Document1 pageCambio 1JESUS CRISTOBAL RIVERANo ratings yet

- Payment ScheduleDocument1 pagePayment Schedulebilal hassanNo ratings yet

- DRL1 CRDocument3 pagesDRL1 CRpankaj_xaviersNo ratings yet

- Client: PT Jambi Prima Coal Closing Date: 31 Desember 2018Document7 pagesClient: PT Jambi Prima Coal Closing Date: 31 Desember 2018Umar MukhtarNo ratings yet

- Intermediate AccountingDocument10 pagesIntermediate AccountingJean AmisiNo ratings yet

- Color Star Technology CoDocument1 pageColor Star Technology Cochecho zgzNo ratings yet

- Security Level Portfolio As On January 14 2022 For 6 Schemes Being Wound UpDocument30 pagesSecurity Level Portfolio As On January 14 2022 For 6 Schemes Being Wound UpRashmi LNo ratings yet

- Kotak Standard Multicap Fund (G)Document4 pagesKotak Standard Multicap Fund (G)Rudhra MoorthyNo ratings yet

- WSP Basic LBO - VF 2Document12 pagesWSP Basic LBO - VF 2jason.sevin02No ratings yet

- Sample Index - Sureshot CA Topics & CA Related Static GK PDFDocument7 pagesSample Index - Sureshot CA Topics & CA Related Static GK PDFanukriti3sinhaNo ratings yet

- Den FY2021 Financial Report-15Document6 pagesDen FY2021 Financial Report-15PAVANKUMAR S BNo ratings yet

- LBBW Annual Report 2019 Aa1r3sby3g MDocument316 pagesLBBW Annual Report 2019 Aa1r3sby3g MNicole RichardsonNo ratings yet

- Venkateshwara Power Project LimitedDocument3 pagesVenkateshwara Power Project Limited04 Sourabh BaraleNo ratings yet

- NSB Tajamal1Document4 pagesNSB Tajamal1Muzammil HasnainNo ratings yet

- Gulshan Welfare Society Rampur: Bajodi Tola, Rampur City, Rampur CityDocument4 pagesGulshan Welfare Society Rampur: Bajodi Tola, Rampur City, Rampur Cityparam mandalNo ratings yet

- Research 0452 - 2022 - F - M - p22 - MsDocument23 pagesResearch 0452 - 2022 - F - M - p22 - MsV-academy MathsNo ratings yet

- Zacks Small-Cap Research: Corecivic, IncDocument8 pagesZacks Small-Cap Research: Corecivic, IncKarim LahrichiNo ratings yet

- Chapter 17 In-Class Problems SolutionDocument6 pagesChapter 17 In-Class Problems Solutionliuxuhan3No ratings yet

- Paystub 2021 12 19 PDFDocument2 pagesPaystub 2021 12 19 PDFLuis MartinezNo ratings yet

- Barings Global Senior Secured Bond FundDocument4 pagesBarings Global Senior Secured Bond FundFrancis MejiaNo ratings yet

- Day 1 - Excel - Eff VsDocument4 pagesDay 1 - Excel - Eff Vsapi-661736044No ratings yet

- Af KulotDocument2 pagesAf Kulotshane bentaib ambiaNo ratings yet

- Question Bank Memo 2022 Second SemesterDocument59 pagesQuestion Bank Memo 2022 Second SemesterWorship NtshuxekaniNo ratings yet

- Virtual Private Lesson Opportuni2es Flutes: Name Contact Notes Stephanie Gillespie Jacqui Reaves Lawson Charles PageDocument5 pagesVirtual Private Lesson Opportuni2es Flutes: Name Contact Notes Stephanie Gillespie Jacqui Reaves Lawson Charles Pagegalter6No ratings yet

- Forage Production and Utilization: Office HoursDocument6 pagesForage Production and Utilization: Office Hoursgalter6No ratings yet

- Economics 4784: Economic Development: Class PoliciesDocument8 pagesEconomics 4784: Economic Development: Class Policiesgalter6No ratings yet

- History 1302 - U.S. History - 1865 To The Present Angelo State University 2021 Spring Semester Section 060, CRN# 22721Document2 pagesHistory 1302 - U.S. History - 1865 To The Present Angelo State University 2021 Spring Semester Section 060, CRN# 22721galter6No ratings yet

- Avatar Bulletin November 2020 TrainingDocument1 pageAvatar Bulletin November 2020 Traininggalter6No ratings yet

- Set-Up A Weekly Schedule Organize Around Each ClassDocument2 pagesSet-Up A Weekly Schedule Organize Around Each Classgalter6No ratings yet

- Working Western Rail Amateur DocumentDocument1 pageWorking Western Rail Amateur Documentgalter6No ratings yet

- KinasovuDocument2 pagesKinasovugalter6No ratings yet

- Use Classes Order 1987 - Quick Reference Guide: Planning Jungle LimitedDocument11 pagesUse Classes Order 1987 - Quick Reference Guide: Planning Jungle Limitedgalter6No ratings yet

- FUJITSU Notebook LIFEBOOK U759: Data SheetDocument8 pagesFUJITSU Notebook LIFEBOOK U759: Data Sheetgalter6No ratings yet

- Economics 330 D1 Section 2 Macroeconomic TheoryDocument6 pagesEconomics 330 D1 Section 2 Macroeconomic Theorygalter6No ratings yet

- Objective:: Inglés Junior Class - 3° EM 2. I Didn't Want To Leave September 4-11, 2020 18Document3 pagesObjective:: Inglés Junior Class - 3° EM 2. I Didn't Want To Leave September 4-11, 2020 18galter6No ratings yet

- (R3) 15:05 ASCOT, 7f: Champagne PiaffDocument3 pages(R3) 15:05 ASCOT, 7f: Champagne Piaffgalter6No ratings yet

- Monthly Return of Equity Issuer On Movements in Securities: (State Currency) (State Currency)Document11 pagesMonthly Return of Equity Issuer On Movements in Securities: (State Currency) (State Currency)galter6No ratings yet

- Distributed Computing COMP 4001 (September 2, 2020) : 1 Delivery MethodDocument5 pagesDistributed Computing COMP 4001 (September 2, 2020) : 1 Delivery Methodgalter6No ratings yet

- Notetaking Systems & Styles: Style of Notes, Always Spend at Least 5 Minutes Reviewing Them Before Packing Up Your BagsDocument2 pagesNotetaking Systems & Styles: Style of Notes, Always Spend at Least 5 Minutes Reviewing Them Before Packing Up Your Bagsgalter6No ratings yet

- Principles of Computer Networks Comp 3203 (September 2, 2020)Document5 pagesPrinciples of Computer Networks Comp 3203 (September 2, 2020)galter6No ratings yet

- Homework Basics: Getting OrganizedDocument2 pagesHomework Basics: Getting Organizedgalter6No ratings yet

- Taking Useful Class Notes: Academic Learning Centre 201 Tier 480-1481Document22 pagesTaking Useful Class Notes: Academic Learning Centre 201 Tier 480-1481galter6No ratings yet

- How To Upload Class NotesDocument1 pageHow To Upload Class Notesgalter6No ratings yet

- Hindu Law NotesDocument5 pagesHindu Law Notesgalter6No ratings yet

- Class Notes: NameDocument2 pagesClass Notes: Namegalter6No ratings yet

- Class Notes: Oral Presentations Class Notes Taken by The StudentDocument2 pagesClass Notes: Oral Presentations Class Notes Taken by The Studentgalter6No ratings yet

- Censusc 93Document4 pagesCensusc 93galter6No ratings yet

- GL Owners - JTDocument50 pagesGL Owners - JTSuneet GaggarNo ratings yet

- Talent ManagementDocument9 pagesTalent ManagementMehwish QayyumNo ratings yet

- SMES Insolvency - A.G. Martinez 2022Document65 pagesSMES Insolvency - A.G. Martinez 2022Vilija MogenyteNo ratings yet

- Segment Reporting PDFDocument4 pagesSegment Reporting PDFAnn Salazar100% (1)

- National Pension SchemeDocument18 pagesNational Pension SchemeNaveen NNo ratings yet

- Oil Demand and Chemicals FeedstocksDocument21 pagesOil Demand and Chemicals FeedstocksAswin KondapallyNo ratings yet

- Gujarat Technological UniversityDocument2 pagesGujarat Technological UniversityIsha KhannaNo ratings yet

- MBA FPX5008 - Assessment2 1Document11 pagesMBA FPX5008 - Assessment2 1AA TsolScholarNo ratings yet

- Lamya Yusuf Jhumur BUS498.37 Internship Report Summer2021..Document29 pagesLamya Yusuf Jhumur BUS498.37 Internship Report Summer2021..Nazia ElhamNo ratings yet

- Competitor AnalysisDocument4 pagesCompetitor AnalysisKhadija TahirNo ratings yet

- SAMPLE TRAVEL PLAN (Kyla)Document4 pagesSAMPLE TRAVEL PLAN (Kyla)Ralph IlardeNo ratings yet

- Certificate of Compliance: Rm1605, Block A, Haisong Building, Tairan 9th RD., Futian District, Shenzhen, ChinaDocument2 pagesCertificate of Compliance: Rm1605, Block A, Haisong Building, Tairan 9th RD., Futian District, Shenzhen, ChinaAleXis - AleXisNo ratings yet

- P Company Acquires 80Document5 pagesP Company Acquires 80hus wodgyNo ratings yet

- Batul Zaheer PatelDocument44 pagesBatul Zaheer PatelbatulNo ratings yet

- PWC Virtual Case Experience Corporate Tax - Model Work Task 1 - Tax Provision Calculation 2021Document6 pagesPWC Virtual Case Experience Corporate Tax - Model Work Task 1 - Tax Provision Calculation 2021arifansari2299No ratings yet

- Benchmarking Infrastructure DevelopmentDocument184 pagesBenchmarking Infrastructure DevelopmentSebghatullah KarimiNo ratings yet

- Ausgrid AMB259996MRE1 NSW CZ5Document3 pagesAusgrid AMB259996MRE1 NSW CZ5BaltNo ratings yet

- 10 BSC Strategy Focus OrganizationDocument20 pages10 BSC Strategy Focus OrganizationindahNo ratings yet

- 03-Keynote Paper R.S SidhuDocument25 pages03-Keynote Paper R.S SidhuRajkumarNo ratings yet

- Name: Jenylou Dapiton Semi Finals TopicDocument3 pagesName: Jenylou Dapiton Semi Finals TopicJenylou Maputol DapitonNo ratings yet

- Meaning of AccountingDocument1 pageMeaning of AccountingVinod GandhiNo ratings yet

- Composition Scheme Sec. 10: Ques-1 What Is Composition Levy Under GST?Document12 pagesComposition Scheme Sec. 10: Ques-1 What Is Composition Levy Under GST?Tapan BarikNo ratings yet

- Revision Notes For Class 12 Macro Economics Chapter 1 - Free PDF DownloadDocument15 pagesRevision Notes For Class 12 Macro Economics Chapter 1 - Free PDF DownloadVibhuti BatraNo ratings yet

- Case 1Document10 pagesCase 1Shawn VerzalesNo ratings yet

- MECO 111-Principles of Microeconomics-Syed Zahid AliDocument3 pagesMECO 111-Principles of Microeconomics-Syed Zahid AliAbdul Wasay SiddiquiNo ratings yet

- Sustainable Transformation of Yemen's Energy SystemDocument41 pagesSustainable Transformation of Yemen's Energy Systemfath badiNo ratings yet

- Business Studies Exam Questions For Jss3 Second Term: Practice JAMB CBT 2022Document1 pageBusiness Studies Exam Questions For Jss3 Second Term: Practice JAMB CBT 2022Rachel Vlog100% (2)

Download as pdf or txt

You might also like

- BIR Rulings On Change of Useful LifeDocument6 pagesBIR Rulings On Change of Useful LifeCarlota Nicolas VillaromanNo ratings yet

- FWB June 2021 Financials by LlamaDocument7 pagesFWB June 2021 Financials by LlamaShreyas HariharanNo ratings yet

- Revolut Stay and Spend LetterDocument2 pagesRevolut Stay and Spend LetterJonathan KeaneNo ratings yet

- RatingsDirect PresalePlanetFitnessMasterIssuerLLCSeries20181 39312924 Jul-23-2019Document18 pagesRatingsDirect PresalePlanetFitnessMasterIssuerLLCSeries20181 39312924 Jul-23-2019ougyajNo ratings yet

- Lead Schedule Fixed AssetDocument9 pagesLead Schedule Fixed Assetkelvin hervangga18No ratings yet

- CH.2 InterestDocument41 pagesCH.2 InterestJenalyn MacarilayNo ratings yet

- Carmax S&PDocument15 pagesCarmax S&Ptrust2386No ratings yet

- Honda Auto Receivables 2021-3 Owner Trust Honda Auto Receivables 2021-3 Owner TrustDocument15 pagesHonda Auto Receivables 2021-3 Owner Trust Honda Auto Receivables 2021-3 Owner Trustsprite2lNo ratings yet

- Sabey Data Center Issuer LLC (Series 2022-1) Sabey Data Center Issuer LLC (Series 2022-1)Document20 pagesSabey Data Center Issuer LLC (Series 2022-1) Sabey Data Center Issuer LLC (Series 2022-1)kouroumaNo ratings yet

- 2023-01-01 00-00-00-StatementDocument4 pages2023-01-01 00-00-00-StatementCarolina MartinsNo ratings yet

- INC.0012 Monthly Disbursments AURADocument23 pagesINC.0012 Monthly Disbursments AURAedwilsonjafarxNo ratings yet

- Estim 20951-00 2024-03-31 Ffalchi 11 653219 BatchuserDocument8 pagesEstim 20951-00 2024-03-31 Ffalchi 11 653219 Batchuserpelleriti2694No ratings yet

- Jockey Club Ti-I College F.4 Business, Accounting and Financial Studies Second Term Examination (2020-2021)Document5 pagesJockey Club Ti-I College F.4 Business, Accounting and Financial Studies Second Term Examination (2020-2021)ouo So方No ratings yet

- Fundcard: Edelweiss Low Duration Fund - Direct PlanDocument4 pagesFundcard: Edelweiss Low Duration Fund - Direct PlanYogi173No ratings yet

- ValueResearchFundcard FranklinIndiaUltraShortBondFund SuperInstitutionalPlan DirectPlan 2017oct11Document4 pagesValueResearchFundcard FranklinIndiaUltraShortBondFund SuperInstitutionalPlan DirectPlan 2017oct11jamsheer.aaNo ratings yet

- Stelco National BankDocument5 pagesStelco National BankForexliveNo ratings yet

- BppuDocument2 pagesBppuni made safitriNo ratings yet

- MDS Abril 2022Document2 pagesMDS Abril 2022edwilsonjafarxNo ratings yet

- Legg Mason Value Fund - Dec 2022 PDFDocument2 pagesLegg Mason Value Fund - Dec 2022 PDFJeanmarNo ratings yet

- M.P. ResultDocument1 pageM.P. Resultgautamji8151No ratings yet

- Press Release New Sapna Granite Industries: Details of Instruments/facilities in Annexure-1Document3 pagesPress Release New Sapna Granite Industries: Details of Instruments/facilities in Annexure-1Ravi BabuNo ratings yet

- Bhaivav Laxmi Ma Galla Bhandar7677Document14 pagesBhaivav Laxmi Ma Galla Bhandar7677Ravi KarnaNo ratings yet

- US Flow of Funds 07sept2022Document39 pagesUS Flow of Funds 07sept2022scribbugNo ratings yet

- MDS Out 2022Document2 pagesMDS Out 2022edwilsonjafarxNo ratings yet

- Compak Suggested AnswersDocument8 pagesCompak Suggested Answersknprop134No ratings yet

- Saob 2022 With RecordsDocument2 pagesSaob 2022 With RecordsJustin DonesNo ratings yet

- Nike PIB 2021Document222 pagesNike PIB 2021Emperor OverwatchNo ratings yet

- Impairment Revaluation and Intangibles Acctg 3 Intermediate Accounting IDocument47 pagesImpairment Revaluation and Intangibles Acctg 3 Intermediate Accounting IMarjorie PalmaNo ratings yet

- Companies GL 2021 MemoDocument4 pagesCompanies GL 2021 MemoJayden KaydrnNo ratings yet

- Activision Blizzard, Inc: Data OverviewDocument7 pagesActivision Blizzard, Inc: Data OverviewPratyush ShakyaNo ratings yet

- REO Outreach 2022-11-01 UIDocument29 pagesREO Outreach 2022-11-01 UIJonathan NainggolanNo ratings yet

- RoyalBankofCanadaTSXRY PublicCompanyDocument1 pageRoyalBankofCanadaTSXRY PublicCompanyGDoingThings YTNo ratings yet

- APOLLO Series 2017-1 TrustDocument16 pagesAPOLLO Series 2017-1 TrustQuant_GeekNo ratings yet

- COSCO - PH Cosco Capital Inc. Financial Statements - WSJDocument1 pageCOSCO - PH Cosco Capital Inc. Financial Statements - WSJjannahaaliyahdNo ratings yet

- ValueResearchFundcard BarodaPioneerShortTermBondFund DirectPlan 2017may16Document4 pagesValueResearchFundcard BarodaPioneerShortTermBondFund DirectPlan 2017may16Achint KumarNo ratings yet

- Crisil GR&A - Bank - Bank of America NADocument9 pagesCrisil GR&A - Bank - Bank of America NANguyễn Bùi Phương DungNo ratings yet

- Franklin Resources, Inc.: Stock Report - March 12, 2022 - NYSE Symbol: BEN - BEN Is in The S&P 500Document9 pagesFranklin Resources, Inc.: Stock Report - March 12, 2022 - NYSE Symbol: BEN - BEN Is in The S&P 500apdusp2No ratings yet

- Data On Central Government Debt For The Quarter Ended December 2021 (Q4)Document1 pageData On Central Government Debt For The Quarter Ended December 2021 (Q4)Dhanesk KANo ratings yet

- Cambio 1Document1 pageCambio 1JESUS CRISTOBAL RIVERANo ratings yet

- Payment ScheduleDocument1 pagePayment Schedulebilal hassanNo ratings yet

- DRL1 CRDocument3 pagesDRL1 CRpankaj_xaviersNo ratings yet

- Client: PT Jambi Prima Coal Closing Date: 31 Desember 2018Document7 pagesClient: PT Jambi Prima Coal Closing Date: 31 Desember 2018Umar MukhtarNo ratings yet

- Intermediate AccountingDocument10 pagesIntermediate AccountingJean AmisiNo ratings yet

- Color Star Technology CoDocument1 pageColor Star Technology Cochecho zgzNo ratings yet

- Security Level Portfolio As On January 14 2022 For 6 Schemes Being Wound UpDocument30 pagesSecurity Level Portfolio As On January 14 2022 For 6 Schemes Being Wound UpRashmi LNo ratings yet

- Kotak Standard Multicap Fund (G)Document4 pagesKotak Standard Multicap Fund (G)Rudhra MoorthyNo ratings yet

- WSP Basic LBO - VF 2Document12 pagesWSP Basic LBO - VF 2jason.sevin02No ratings yet

- Sample Index - Sureshot CA Topics & CA Related Static GK PDFDocument7 pagesSample Index - Sureshot CA Topics & CA Related Static GK PDFanukriti3sinhaNo ratings yet

- Den FY2021 Financial Report-15Document6 pagesDen FY2021 Financial Report-15PAVANKUMAR S BNo ratings yet

- LBBW Annual Report 2019 Aa1r3sby3g MDocument316 pagesLBBW Annual Report 2019 Aa1r3sby3g MNicole RichardsonNo ratings yet

- Venkateshwara Power Project LimitedDocument3 pagesVenkateshwara Power Project Limited04 Sourabh BaraleNo ratings yet

- NSB Tajamal1Document4 pagesNSB Tajamal1Muzammil HasnainNo ratings yet

- Gulshan Welfare Society Rampur: Bajodi Tola, Rampur City, Rampur CityDocument4 pagesGulshan Welfare Society Rampur: Bajodi Tola, Rampur City, Rampur Cityparam mandalNo ratings yet

- Research 0452 - 2022 - F - M - p22 - MsDocument23 pagesResearch 0452 - 2022 - F - M - p22 - MsV-academy MathsNo ratings yet

- Zacks Small-Cap Research: Corecivic, IncDocument8 pagesZacks Small-Cap Research: Corecivic, IncKarim LahrichiNo ratings yet

- Chapter 17 In-Class Problems SolutionDocument6 pagesChapter 17 In-Class Problems Solutionliuxuhan3No ratings yet

- Paystub 2021 12 19 PDFDocument2 pagesPaystub 2021 12 19 PDFLuis MartinezNo ratings yet

- Barings Global Senior Secured Bond FundDocument4 pagesBarings Global Senior Secured Bond FundFrancis MejiaNo ratings yet

- Day 1 - Excel - Eff VsDocument4 pagesDay 1 - Excel - Eff Vsapi-661736044No ratings yet

- Af KulotDocument2 pagesAf Kulotshane bentaib ambiaNo ratings yet

- Question Bank Memo 2022 Second SemesterDocument59 pagesQuestion Bank Memo 2022 Second SemesterWorship NtshuxekaniNo ratings yet

- Virtual Private Lesson Opportuni2es Flutes: Name Contact Notes Stephanie Gillespie Jacqui Reaves Lawson Charles PageDocument5 pagesVirtual Private Lesson Opportuni2es Flutes: Name Contact Notes Stephanie Gillespie Jacqui Reaves Lawson Charles Pagegalter6No ratings yet

- Forage Production and Utilization: Office HoursDocument6 pagesForage Production and Utilization: Office Hoursgalter6No ratings yet

- Economics 4784: Economic Development: Class PoliciesDocument8 pagesEconomics 4784: Economic Development: Class Policiesgalter6No ratings yet

- History 1302 - U.S. History - 1865 To The Present Angelo State University 2021 Spring Semester Section 060, CRN# 22721Document2 pagesHistory 1302 - U.S. History - 1865 To The Present Angelo State University 2021 Spring Semester Section 060, CRN# 22721galter6No ratings yet

- Avatar Bulletin November 2020 TrainingDocument1 pageAvatar Bulletin November 2020 Traininggalter6No ratings yet

- Set-Up A Weekly Schedule Organize Around Each ClassDocument2 pagesSet-Up A Weekly Schedule Organize Around Each Classgalter6No ratings yet

- Working Western Rail Amateur DocumentDocument1 pageWorking Western Rail Amateur Documentgalter6No ratings yet

- KinasovuDocument2 pagesKinasovugalter6No ratings yet

- Use Classes Order 1987 - Quick Reference Guide: Planning Jungle LimitedDocument11 pagesUse Classes Order 1987 - Quick Reference Guide: Planning Jungle Limitedgalter6No ratings yet

- FUJITSU Notebook LIFEBOOK U759: Data SheetDocument8 pagesFUJITSU Notebook LIFEBOOK U759: Data Sheetgalter6No ratings yet

- Economics 330 D1 Section 2 Macroeconomic TheoryDocument6 pagesEconomics 330 D1 Section 2 Macroeconomic Theorygalter6No ratings yet

- Objective:: Inglés Junior Class - 3° EM 2. I Didn't Want To Leave September 4-11, 2020 18Document3 pagesObjective:: Inglés Junior Class - 3° EM 2. I Didn't Want To Leave September 4-11, 2020 18galter6No ratings yet

- (R3) 15:05 ASCOT, 7f: Champagne PiaffDocument3 pages(R3) 15:05 ASCOT, 7f: Champagne Piaffgalter6No ratings yet

- Monthly Return of Equity Issuer On Movements in Securities: (State Currency) (State Currency)Document11 pagesMonthly Return of Equity Issuer On Movements in Securities: (State Currency) (State Currency)galter6No ratings yet

- Distributed Computing COMP 4001 (September 2, 2020) : 1 Delivery MethodDocument5 pagesDistributed Computing COMP 4001 (September 2, 2020) : 1 Delivery Methodgalter6No ratings yet

- Notetaking Systems & Styles: Style of Notes, Always Spend at Least 5 Minutes Reviewing Them Before Packing Up Your BagsDocument2 pagesNotetaking Systems & Styles: Style of Notes, Always Spend at Least 5 Minutes Reviewing Them Before Packing Up Your Bagsgalter6No ratings yet

- Principles of Computer Networks Comp 3203 (September 2, 2020)Document5 pagesPrinciples of Computer Networks Comp 3203 (September 2, 2020)galter6No ratings yet

- Homework Basics: Getting OrganizedDocument2 pagesHomework Basics: Getting Organizedgalter6No ratings yet

- Taking Useful Class Notes: Academic Learning Centre 201 Tier 480-1481Document22 pagesTaking Useful Class Notes: Academic Learning Centre 201 Tier 480-1481galter6No ratings yet

- How To Upload Class NotesDocument1 pageHow To Upload Class Notesgalter6No ratings yet

- Hindu Law NotesDocument5 pagesHindu Law Notesgalter6No ratings yet

- Class Notes: NameDocument2 pagesClass Notes: Namegalter6No ratings yet

- Class Notes: Oral Presentations Class Notes Taken by The StudentDocument2 pagesClass Notes: Oral Presentations Class Notes Taken by The Studentgalter6No ratings yet

- Censusc 93Document4 pagesCensusc 93galter6No ratings yet

- GL Owners - JTDocument50 pagesGL Owners - JTSuneet GaggarNo ratings yet

- Talent ManagementDocument9 pagesTalent ManagementMehwish QayyumNo ratings yet

- SMES Insolvency - A.G. Martinez 2022Document65 pagesSMES Insolvency - A.G. Martinez 2022Vilija MogenyteNo ratings yet

- Segment Reporting PDFDocument4 pagesSegment Reporting PDFAnn Salazar100% (1)

- National Pension SchemeDocument18 pagesNational Pension SchemeNaveen NNo ratings yet

- Oil Demand and Chemicals FeedstocksDocument21 pagesOil Demand and Chemicals FeedstocksAswin KondapallyNo ratings yet

- Gujarat Technological UniversityDocument2 pagesGujarat Technological UniversityIsha KhannaNo ratings yet

- MBA FPX5008 - Assessment2 1Document11 pagesMBA FPX5008 - Assessment2 1AA TsolScholarNo ratings yet

- Lamya Yusuf Jhumur BUS498.37 Internship Report Summer2021..Document29 pagesLamya Yusuf Jhumur BUS498.37 Internship Report Summer2021..Nazia ElhamNo ratings yet

- Competitor AnalysisDocument4 pagesCompetitor AnalysisKhadija TahirNo ratings yet

- SAMPLE TRAVEL PLAN (Kyla)Document4 pagesSAMPLE TRAVEL PLAN (Kyla)Ralph IlardeNo ratings yet

- Certificate of Compliance: Rm1605, Block A, Haisong Building, Tairan 9th RD., Futian District, Shenzhen, ChinaDocument2 pagesCertificate of Compliance: Rm1605, Block A, Haisong Building, Tairan 9th RD., Futian District, Shenzhen, ChinaAleXis - AleXisNo ratings yet

- P Company Acquires 80Document5 pagesP Company Acquires 80hus wodgyNo ratings yet

- Batul Zaheer PatelDocument44 pagesBatul Zaheer PatelbatulNo ratings yet

- PWC Virtual Case Experience Corporate Tax - Model Work Task 1 - Tax Provision Calculation 2021Document6 pagesPWC Virtual Case Experience Corporate Tax - Model Work Task 1 - Tax Provision Calculation 2021arifansari2299No ratings yet

- Benchmarking Infrastructure DevelopmentDocument184 pagesBenchmarking Infrastructure DevelopmentSebghatullah KarimiNo ratings yet

- Ausgrid AMB259996MRE1 NSW CZ5Document3 pagesAusgrid AMB259996MRE1 NSW CZ5BaltNo ratings yet

- 10 BSC Strategy Focus OrganizationDocument20 pages10 BSC Strategy Focus OrganizationindahNo ratings yet

- 03-Keynote Paper R.S SidhuDocument25 pages03-Keynote Paper R.S SidhuRajkumarNo ratings yet

- Name: Jenylou Dapiton Semi Finals TopicDocument3 pagesName: Jenylou Dapiton Semi Finals TopicJenylou Maputol DapitonNo ratings yet

- Meaning of AccountingDocument1 pageMeaning of AccountingVinod GandhiNo ratings yet

- Composition Scheme Sec. 10: Ques-1 What Is Composition Levy Under GST?Document12 pagesComposition Scheme Sec. 10: Ques-1 What Is Composition Levy Under GST?Tapan BarikNo ratings yet

- Revision Notes For Class 12 Macro Economics Chapter 1 - Free PDF DownloadDocument15 pagesRevision Notes For Class 12 Macro Economics Chapter 1 - Free PDF DownloadVibhuti BatraNo ratings yet

- Case 1Document10 pagesCase 1Shawn VerzalesNo ratings yet

- MECO 111-Principles of Microeconomics-Syed Zahid AliDocument3 pagesMECO 111-Principles of Microeconomics-Syed Zahid AliAbdul Wasay SiddiquiNo ratings yet

- Sustainable Transformation of Yemen's Energy SystemDocument41 pagesSustainable Transformation of Yemen's Energy Systemfath badiNo ratings yet

- Business Studies Exam Questions For Jss3 Second Term: Practice JAMB CBT 2022Document1 pageBusiness Studies Exam Questions For Jss3 Second Term: Practice JAMB CBT 2022Rachel Vlog100% (2)