Download as xlsx, pdf, or txt

You might also like

- Merritt's BakeryDocument1 pageMerritt's BakeryNardine Farag0% (1)

- En 12604 (2000) (E)Document7 pagesEn 12604 (2000) (E)Carlos LanzillottoNo ratings yet

- Petron Corp - Financial Analysis From 2014 - 2018Document4 pagesPetron Corp - Financial Analysis From 2014 - 2018Neil Nadua100% (1)

- VLCT TutorialDocument29 pagesVLCT TutorialAbhishek ChughNo ratings yet

- URC Business ReviewDocument75 pagesURC Business Reviewanon_728683458No ratings yet

- Afsr Projet (Shell) Final - 20p00053Document48 pagesAfsr Projet (Shell) Final - 20p00053Halimah SheikhNo ratings yet

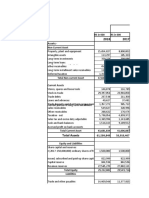

- Assets: Balance SheetDocument4 pagesAssets: Balance SheetAsadvirkNo ratings yet

- Research For OBUDocument14 pagesResearch For OBUM Burhan SafiNo ratings yet

- Con Solo Dated Financial Statement AsperUS GAAP 2009 10Document8 pagesCon Solo Dated Financial Statement AsperUS GAAP 2009 10Nitin VatsNo ratings yet

- The Group AssetsDocument46 pagesThe Group Assetsit4728No ratings yet

- Balance Sheet: 2016 2017 2018 Assets Non-Current AssetsDocument6 pagesBalance Sheet: 2016 2017 2018 Assets Non-Current AssetsAhsan KamranNo ratings yet

- Excel File SuzukiDocument18 pagesExcel File SuzukiMahnoor AfzalNo ratings yet

- Balance Sheet of Maple Leaf: AssetsDocument12 pagesBalance Sheet of Maple Leaf: Assets01290101002675No ratings yet

- 1321 Behroz TariqDocument11 pages1321 Behroz TariqBehroz Tariq 1321No ratings yet

- HOndaDocument8 pagesHOndaRizwan Sikandar 6149-FMS/BBA/F20No ratings yet

- Buxly Paint: Balance SheetDocument33 pagesBuxly Paint: Balance SheetJarhan AzeemNo ratings yet

- Balance Sheet: AssetsDocument19 pagesBalance Sheet: Assetssumeer shafiqNo ratings yet

- Renata LimitedDocument18 pagesRenata LimitedSaqeef RayhanNo ratings yet

- FSP LinaDocument43 pagesFSP LinaAlina Binte EjazNo ratings yet

- Gul Ahmed Quiz 2 QuesDocument5 pagesGul Ahmed Quiz 2 QuesTehreem SirajNo ratings yet

- MPCLDocument4 pagesMPCLRizwan Sikandar 6149-FMS/BBA/F20No ratings yet

- Ayala Corporation Statement of Financial Position 2019 2018 in Millions Audited Audited AsssetsDocument11 pagesAyala Corporation Statement of Financial Position 2019 2018 in Millions Audited Audited AsssetsAlgen SabaytonNo ratings yet

- Greetings Everyone: To My PresentationDocument15 pagesGreetings Everyone: To My PresentationZakaria ShuvoNo ratings yet

- AssetsDocument3 pagesAssetsyasrab abbasNo ratings yet

- FM Unit 2 Tutorial - Finanacial Statement Analysis Revised 2019Document4 pagesFM Unit 2 Tutorial - Finanacial Statement Analysis Revised 2019Tanice WhyteNo ratings yet

- Aisha Steel Annual Report 2015Document33 pagesAisha Steel Annual Report 2015qamber18No ratings yet

- Crescent Textile Mills LTD AnalysisDocument23 pagesCrescent Textile Mills LTD AnalysisMuhammad Noman MehboobNo ratings yet

- BERISO, Ella's Financial Status Analysis 2022Document8 pagesBERISO, Ella's Financial Status Analysis 2022kasandra dawn BerisoNo ratings yet

- Rafhan Maize Products Company LTDDocument10 pagesRafhan Maize Products Company LTDALI SHER HaidriNo ratings yet

- Globe Vertical AnalysisDocument22 pagesGlobe Vertical AnalysisArriana RefugioNo ratings yet

- DG Khan Cement Financial StatementsDocument8 pagesDG Khan Cement Financial StatementsAsad BumbiaNo ratings yet

- Income Statement: in ThousandsDocument29 pagesIncome Statement: in ThousandsDaviti LabadzeNo ratings yet

- FirstBank Unaudited Half Year Results For Period Ending June 2010Document1 pageFirstBank Unaudited Half Year Results For Period Ending June 2010Kunle AdegboyeNo ratings yet

- Greenko - Investment - Company - Audited - Combined - Financial - Statements - FY 2018 - 19Document102 pagesGreenko - Investment - Company - Audited - Combined - Financial - Statements - FY 2018 - 19hNo ratings yet

- Vietnam Dairy Products Joint Stock Company Balance Sheet December 31, 2020Document24 pagesVietnam Dairy Products Joint Stock Company Balance Sheet December 31, 2020Như ThảoNo ratings yet

- Financial PlanDocument25 pagesFinancial PlanAyesha KanwalNo ratings yet

- Bursa Q3 2015 FinalDocument16 pagesBursa Q3 2015 FinalFakhrul Azman NawiNo ratings yet

- ABS-CBN Corporation and Subsidiaries Consolidated Statements of Financial Position (Amounts in Thousands)Document10 pagesABS-CBN Corporation and Subsidiaries Consolidated Statements of Financial Position (Amounts in Thousands)Mark Angelo BustosNo ratings yet

- Maple Leaf Cement Factory Limited.Document17 pagesMaple Leaf Cement Factory Limited.MubasharNo ratings yet

- Atlas Honda (2019 22)Document6 pagesAtlas Honda (2019 22)husnainbutt2025No ratings yet

- Balance Sheet: Glaxosmithkline Pakistan LimitedDocument15 pagesBalance Sheet: Glaxosmithkline Pakistan LimitedMuhammad SamiNo ratings yet

- Directors' Report: For The Period Ended 31 March 2018Document24 pagesDirectors' Report: For The Period Ended 31 March 2018Asma RehmanNo ratings yet

- HorizontalDocument4 pagesHorizontal30 Odicta, Justine AnneNo ratings yet

- Receivable Breakdown Type of Inventory Amount of Receivable Days Overdue RemarkDocument6 pagesReceivable Breakdown Type of Inventory Amount of Receivable Days Overdue RemarkYonatanNo ratings yet

- IbfDocument5 pagesIbfSader AzamNo ratings yet

- Philippine Seven Corporation and SubsidiariesDocument4 pagesPhilippine Seven Corporation and Subsidiariesgirlie ValdezNo ratings yet

- Greenko Investment Company - Financial Statements 2017-18Document93 pagesGreenko Investment Company - Financial Statements 2017-18DSddsNo ratings yet

- Consolidated Statement of Financial Position: Beximco Pharmaceuticals Limited and Its Subsidiaries As at June 30, 2019Document4 pagesConsolidated Statement of Financial Position: Beximco Pharmaceuticals Limited and Its Subsidiaries As at June 30, 2019palashndcNo ratings yet

- March 2021 Nine Month Orion PharmaDocument26 pagesMarch 2021 Nine Month Orion PharmaAfia Begum ChowdhuryNo ratings yet

- Finance NFL & MitchelsDocument10 pagesFinance NFL & Mitchelsrimshaanwar617No ratings yet

- Interim Financial Statements - English q2Document12 pagesInterim Financial Statements - English q2yanaNo ratings yet

- FinShiksha Maruti Suzuki UnsolvedDocument12 pagesFinShiksha Maruti Suzuki UnsolvedGANESH JAINNo ratings yet

- Quiz RatiosDocument4 pagesQuiz RatiosAmmar AsifNo ratings yet

- Scotiabank Peru Financial Statements - 2018Document80 pagesScotiabank Peru Financial Statements - 2018Juan CalfunNo ratings yet

- FSA ProjectDocument59 pagesFSA ProjectIslam AbdelshafyNo ratings yet

- Ain 20201025074Document8 pagesAin 20201025074HAMMADHRNo ratings yet

- Annexure 4116790Document31 pagesAnnexure 4116790ayesha ansariNo ratings yet

- IFRS FinalDocument69 pagesIFRS FinalHardik SharmaNo ratings yet

- Crescent Steel and Allied Products LTD.: Balance SheetDocument14 pagesCrescent Steel and Allied Products LTD.: Balance SheetAsadvirkNo ratings yet

- Term Peper Group G FIN201Document16 pagesTerm Peper Group G FIN201Fahim XubayerNo ratings yet

- Note 2019: Income StatementDocument19 pagesNote 2019: Income StatementSyeda Sarwish RizviNo ratings yet

- Hotel RoyalDocument28 pagesHotel RoyalFasasi Abdul Qodir AlabiNo ratings yet

- Securities Operations: A Guide to Trade and Position ManagementFrom EverandSecurities Operations: A Guide to Trade and Position ManagementRating: 4 out of 5 stars4/5 (3)

- Leverage AnalsysisDocument5 pagesLeverage AnalsysisIfraNo ratings yet

- Costs: FinancingDocument6 pagesCosts: FinancingIfraNo ratings yet

- Public LTD Company: Joint Stock CompaniesDocument7 pagesPublic LTD Company: Joint Stock CompaniesIfraNo ratings yet

- Capital Budgeting: 2. Cost and Benefit AnalysisDocument12 pagesCapital Budgeting: 2. Cost and Benefit AnalysisIfraNo ratings yet

- Financial Analysis of Security Paper Limited (Ifra Arshad 2016-Ag-7558)Document9 pagesFinancial Analysis of Security Paper Limited (Ifra Arshad 2016-Ag-7558)IfraNo ratings yet

- Mar 31 2020 Mar 31 2020: Shogun-Method-Derek-Rake 1/5 Shogun-Method-Derek-Rake 1/5Document5 pagesMar 31 2020 Mar 31 2020: Shogun-Method-Derek-Rake 1/5 Shogun-Method-Derek-Rake 1/5Mwila TumbaNo ratings yet

- Snow Leopard Fact SheetDocument2 pagesSnow Leopard Fact SheetHammad_Asif_5099No ratings yet

- Rangkaian Doa RasulullahDocument22 pagesRangkaian Doa RasulullahPETUA PESONA UTTANUANo ratings yet

- Detailed Study of Maharshi Bharadwaja S Vymanika ShastraDocument44 pagesDetailed Study of Maharshi Bharadwaja S Vymanika ShastradwarakaNo ratings yet

- Machine Tools and Automation Machine Tools Operations Mod-3Document20 pagesMachine Tools and Automation Machine Tools Operations Mod-3code makerNo ratings yet

- Instant Water Heater InstructionsDocument16 pagesInstant Water Heater InstructionsJack OffgridNo ratings yet

- Ajp 1Document15 pagesAjp 1Yuva Neta Ashish PandeyNo ratings yet

- The Relationship Between Boron Content and Crack Properties in FCAW Weld MetalDocument6 pagesThe Relationship Between Boron Content and Crack Properties in FCAW Weld MetalVizay KumarNo ratings yet

- 5-Interfacing IO Devices - Student VersionDocument43 pages5-Interfacing IO Devices - Student Versionapi-372116475% (4)

- 5 TH Sem Advanced Accounting PPT - 2.pdf382Document21 pages5 TH Sem Advanced Accounting PPT - 2.pdf382Azhar Ali100% (3)

- Mikel Hoffman Field Observation Report Visit 4 5-6-14Document3 pagesMikel Hoffman Field Observation Report Visit 4 5-6-14api-243298110No ratings yet

- 9i How To Setup Oracle Streams Replication. (Doc ID 224255.1)Document9 pages9i How To Setup Oracle Streams Replication. (Doc ID 224255.1)Nick SantosNo ratings yet

- Nominal Interest Rates vs. Real Interest Rates: DeflationDocument8 pagesNominal Interest Rates vs. Real Interest Rates: DeflationKr PrajapatNo ratings yet

- Oil and Gas IndustryDocument6 pagesOil and Gas IndustryLuqman HadiNo ratings yet

- Rigid Pavement DesignDocument81 pagesRigid Pavement DesignKaustubh Kulkarni100% (1)

- 7227 Lrdi3Document4 pages7227 Lrdi3Gang BhasinNo ratings yet

- ICT3Document16 pagesICT3franceloiseNo ratings yet

- Indesign TutotialDocument6 pagesIndesign TutotialDaniel VillanuevaNo ratings yet

- Banda Caminadora l9Document72 pagesBanda Caminadora l9Yahir LópezNo ratings yet

- Question 926614Document7 pagesQuestion 926614davulurusurekhaNo ratings yet

- Savings PlansDocument39 pagesSavings Plansfrsantos123No ratings yet

- PULP - Oral Histo PDFDocument5 pagesPULP - Oral Histo PDFMaanNo ratings yet

- Chips in A Crisis: EditorialDocument1 pageChips in A Crisis: EditorialAnnisa SilvianaNo ratings yet

- CPU - Organisation - Sir NotesDocument8 pagesCPU - Organisation - Sir Notes69Sutanu MukherjeeNo ratings yet

- SYNC2000-3000-4000 Software UserManual Rev4.5Document187 pagesSYNC2000-3000-4000 Software UserManual Rev4.5BharathiNo ratings yet

- III 1 Electrification 1 28Document30 pagesIII 1 Electrification 1 28Kevin LampaanNo ratings yet