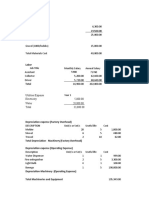

Expenses Cost/pc. 60 Pcs-Total Qty./Month Year 1: Acrylonitrile Butadiene Styrene)

Expenses Cost/pc. 60 Pcs-Total Qty./Month Year 1: Acrylonitrile Butadiene Styrene)

You might also like

- Standard Chart of Accounts For Manufacturing OperationsDocument31 pagesStandard Chart of Accounts For Manufacturing Operationswpentinio67% (15)

- Blitz CaseDocument13 pagesBlitz Caseankita_juhi111112646No ratings yet

- Corporate Income TaxDocument12 pagesCorporate Income TaxShiela Marie Sta Ana100% (1)

- Mayes 8e CH05 SolutionsDocument36 pagesMayes 8e CH05 SolutionsRamez AhmedNo ratings yet

- Practical Accounting 2: Angelito R. Punzalan, CPA, MBADocument33 pagesPractical Accounting 2: Angelito R. Punzalan, CPA, MBADaniella Mae Elip100% (1)

- Instructor: Võ H NG Đ C Group Members:: T Khánh LinhDocument20 pagesInstructor: Võ H NG Đ C Group Members:: T Khánh LinhMai Trần100% (1)

- Chapter 5 Financial Study (Part1) : A. Major AssumptionsDocument9 pagesChapter 5 Financial Study (Part1) : A. Major AssumptionsAnne XxNo ratings yet

- Chapter 5 FinallllllllllllDocument22 pagesChapter 5 Finallllllllllllsv7yyhdmkrNo ratings yet

- Financial StatementsDocument41 pagesFinancial StatementsJan Carla Cabusas CurimatmatNo ratings yet

- I. Financial AssumptionsDocument14 pagesI. Financial AssumptionsJaera shopaholicNo ratings yet

- Financial BreakevenDocument25 pagesFinancial Breakevenjoan villoNo ratings yet

- Financial Study - Garden of EdenDocument16 pagesFinancial Study - Garden of EdenEumar FabruadaNo ratings yet

- SomewhatDocument6 pagesSomewhatPauline VejanoNo ratings yet

- Unit 2Document79 pagesUnit 2Carlos Abadía MorenoNo ratings yet

- Ivd. Financial StatementDocument4 pagesIvd. Financial StatementDre AclonNo ratings yet

- The Financial Plan: Start-Up CapitalDocument7 pagesThe Financial Plan: Start-Up CapitalShany Mae PlaydaNo ratings yet

- Sabit FSDocument8 pagesSabit FSMilagrosa VillasNo ratings yet

- Capital Budgeting - Group AssignmentDocument15 pagesCapital Budgeting - Group AssignmentPhương Anh NguyễnNo ratings yet

- Pre-Cost 3,000,000.00 Pre-Operating ExpensesDocument10 pagesPre-Cost 3,000,000.00 Pre-Operating ExpensesJaselle TantogNo ratings yet

- Group 1 Chapter 5Document18 pagesGroup 1 Chapter 5Angelica GarciaNo ratings yet

- Powerol - Monthly MIS FormatDocument34 pagesPowerol - Monthly MIS Formatdharmender singhNo ratings yet

- A Feasibility Study On The Establishment of Housekeeping Recruitment AgencyDocument10 pagesA Feasibility Study On The Establishment of Housekeeping Recruitment AgencyMary Joy SumapidNo ratings yet

- Budget InformationDocument10 pagesBudget InformationIsabella BattiataNo ratings yet

- Juishat Financial Plan: College Park, Dipolog City Tel. No. (065) 212-8049 WebsiteDocument11 pagesJuishat Financial Plan: College Park, Dipolog City Tel. No. (065) 212-8049 WebsiteMeosjinNo ratings yet

- Nov. 6 DeadlineDocument11 pagesNov. 6 DeadlineAngelinee C.No ratings yet

- Financia ASPECT - FeedsDocument26 pagesFinancia ASPECT - FeedsEumar FabruadaNo ratings yet

- YeahDocument59 pagesYeahPrinceNo ratings yet

- New RevisedGREGORIO DULAY-BUSINESS-PLAN (Copy)Document11 pagesNew RevisedGREGORIO DULAY-BUSINESS-PLAN (Copy)Jnnfr DlyNo ratings yet

- Group 8Document27 pagesGroup 8Anna ChristineNo ratings yet

- Chapter 6 PDFDocument23 pagesChapter 6 PDFreyNo ratings yet

- SuleeDocument8 pagesSuleefuadzeyniNo ratings yet

- 11.bergerac SystemsDocument12 pages11.bergerac SystemsAviralNo ratings yet

- Simdora Manufacturing Private LTD: Project Report OnDocument14 pagesSimdora Manufacturing Private LTD: Project Report OnShivam DashottarNo ratings yet

- Red Chilli WorkingsDocument10 pagesRed Chilli WorkingsImran UmarNo ratings yet

- Financial Study LunaDocument9 pagesFinancial Study LunaNia LunaNo ratings yet

- Tài Methyl-Acetate-Plant-DesignDocument18 pagesTài Methyl-Acetate-Plant-DesignLe Anh QuânNo ratings yet

- Bsbfim601 Manage Finances Prepare BudgetsDocument9 pagesBsbfim601 Manage Finances Prepare BudgetsAli Butt100% (4)

- Nhựa Tiền Phong - Lê Tôn Bảo Huy 20213141Document12 pagesNhựa Tiền Phong - Lê Tôn Bảo Huy 20213141Huy Lê Tôn BảoNo ratings yet

- NSDC Project ReportDocument53 pagesNSDC Project ReportAbirMukherjee67% (3)

- Final Project FMGT 80Document12 pagesFinal Project FMGT 80Alma UriasNo ratings yet

- Income Statement Account Year 1 Year 2 Year 3 Year 4 Year 5Document1 pageIncome Statement Account Year 1 Year 2 Year 3 Year 4 Year 5Anonymous OWNHEhtDNo ratings yet

- Day 1 To Day 4Document186 pagesDay 1 To Day 4Sameer PadhyNo ratings yet

- Feasib Financials Part 1 DocsDocument27 pagesFeasib Financials Part 1 DocsThea SalvadorNo ratings yet

- Cost Accounting Questions Chapter 5Document7 pagesCost Accounting Questions Chapter 5Owais Khan KhattakNo ratings yet

- 5 Year Financial PlanDocument25 pages5 Year Financial Plananwar kadiNo ratings yet

- Bergerac XLS ENGDocument12 pagesBergerac XLS ENGTelmo Barros0% (1)

- Practice Questions For Final W Brick FinancialsDocument7 pagesPractice Questions For Final W Brick FinancialsJoana SilvaNo ratings yet

- V. Financial Feasibility StudyDocument14 pagesV. Financial Feasibility StudyEumar FabruadaNo ratings yet

- 5-Year Financial Plan - Manufacturing 1Document8 pages5-Year Financial Plan - Manufacturing 1tulalit008No ratings yet

- Ampalaya Ice CreamDocument12 pagesAmpalaya Ice CreamEdhel Bryan Corsiga SuicoNo ratings yet

- Final Chapter 6 Financial PlanDocument26 pagesFinal Chapter 6 Financial Planangelo felizardoNo ratings yet

- FY 2012 Audited Financial StatementsDocument0 pagesFY 2012 Audited Financial StatementsmontalvoartsNo ratings yet

- T&T Plastic Industries Balance Sheet For 2019 and 2020Document2 pagesT&T Plastic Industries Balance Sheet For 2019 and 2020Omar BadaamNo ratings yet

- CR AssignmentDocument16 pagesCR AssignmentWaleed KhalidNo ratings yet

- S.N. Particulars Amount (RS.) : Cost of ProjectDocument27 pagesS.N. Particulars Amount (RS.) : Cost of ProjectSuman yadavNo ratings yet

- Services & Offers and Financial ProjectionDocument13 pagesServices & Offers and Financial ProjectionMark Leonil FunaNo ratings yet

- Financial Analysis Template (NPV, IRR & PP)Document11 pagesFinancial Analysis Template (NPV, IRR & PP)charlainecebrian22No ratings yet

- Project 3 Develop and Use A Personal Budget and Saving PlanDocument7 pagesProject 3 Develop and Use A Personal Budget and Saving PlanKen Lati100% (1)

- Taxation: MD Mashiur Rahaman Robin KPMG-RRHDocument12 pagesTaxation: MD Mashiur Rahaman Robin KPMG-RRHZidan ZaifNo ratings yet

- Financial MaamDocument7 pagesFinancial MaamFandinola BeverlyNo ratings yet

- Pawn Shop Revenues World Summary: Market Values & Financials by CountryFrom EverandPawn Shop Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Case Study 2Document4 pagesCase Study 2Sarwanti PurwandariNo ratings yet

- Sol. Man. - Chapter 4 Provisions, Cont. Liabs. & Cont. AssetsDocument9 pagesSol. Man. - Chapter 4 Provisions, Cont. Liabs. & Cont. AssetsEinez B. CarilloNo ratings yet

- Correction: Research and Development Should Be P5,000 Not P50,000Document43 pagesCorrection: Research and Development Should Be P5,000 Not P50,000Dieter LudwigNo ratings yet

- Income From Capital Gains - CS Executive Tax Laws MCQs - GST GunturDocument12 pagesIncome From Capital Gains - CS Executive Tax Laws MCQs - GST GunturDr A. K. SubramaniNo ratings yet

- Issue of SharesDocument24 pagesIssue of SharesManasNo ratings yet

- Public Listed IPO (TCS)Document6 pagesPublic Listed IPO (TCS)SatishNo ratings yet

- 5.3.2 Problems - Corporate LiquidationDocument16 pages5.3.2 Problems - Corporate LiquidationPaulina DocenaNo ratings yet

- Nature of CompanyDocument6 pagesNature of CompanyNaing AungNo ratings yet

- Hindenburg Report On Gautam Adani - Who Is Lying - Akash Banerjee & Manjul - EnglishDocument5 pagesHindenburg Report On Gautam Adani - Who Is Lying - Akash Banerjee & Manjul - EnglishShaik JilanNo ratings yet

- NCFM-Options Model PaperDocument15 pagesNCFM-Options Model Papergowtham2u2No ratings yet

- Ford Case Study (LT 11) - Jerry's Edit v2Document31 pagesFord Case Study (LT 11) - Jerry's Edit v2JerryJoshuaDiazNo ratings yet

- IpoDocument13 pagesIpoalan ruzarioNo ratings yet

- Nestle ExcelDocument2 pagesNestle ExcelWIly GurLsNo ratings yet

- Subramanyam Chapter07Document34 pagesSubramanyam Chapter07Saras Ina Pramesti100% (2)

- Rekha V.V.I. Commerce (Hons.) Part-3Document20 pagesRekha V.V.I. Commerce (Hons.) Part-3Ankur JhaNo ratings yet

- Open Book 30Document8 pagesOpen Book 30harshit bhattNo ratings yet

- 2020-07-03-CERA - NS-Ambit Capital PVT Lt-Cera Sanitaryware (BUY) Pain Is Inevitable!-89001883Document9 pages2020-07-03-CERA - NS-Ambit Capital PVT Lt-Cera Sanitaryware (BUY) Pain Is Inevitable!-89001883akanksha satijaNo ratings yet

- Currency Risk ManagementDocument14 pagesCurrency Risk ManagementAvayant Kumar SinghNo ratings yet

- Marasigan Medical Services - Ex 7Document4 pagesMarasigan Medical Services - Ex 7E.D.J100% (1)

- Solutions ManualDocument226 pagesSolutions Manualuzumakideva26No ratings yet

- 06 - Working Capital Management ProblemsDocument4 pages06 - Working Capital Management ProblemsMerr Fe PainaganNo ratings yet

- Chapter 3 (Tan&Lee) (Autosaved)Document67 pagesChapter 3 (Tan&Lee) (Autosaved)Dewi HazarNo ratings yet

- 3.6 ExercisesDocument8 pages3.6 ExercisesGeorgios MilitsisNo ratings yet

- Passenger Insurance: Your Ride With Rapido On 24 Apr 2022 at 06:07PM Is Now Insured!Document5 pagesPassenger Insurance: Your Ride With Rapido On 24 Apr 2022 at 06:07PM Is Now Insured!susmitha saiduNo ratings yet

- 2 Statement of Financial PositionDocument51 pages2 Statement of Financial PositionMarlon Ladesma100% (2)

- SiloDocument3 pagesSiloBilly ChandraNo ratings yet

- Financial Statements and Analysis: N Learning GoalsDocument3 pagesFinancial Statements and Analysis: N Learning GoalsJoyce De LunaNo ratings yet

Download as docx, pdf, or txt

You might also like

- Standard Chart of Accounts For Manufacturing OperationsDocument31 pagesStandard Chart of Accounts For Manufacturing Operationswpentinio67% (15)

- Blitz CaseDocument13 pagesBlitz Caseankita_juhi111112646No ratings yet

- Corporate Income TaxDocument12 pagesCorporate Income TaxShiela Marie Sta Ana100% (1)

- Mayes 8e CH05 SolutionsDocument36 pagesMayes 8e CH05 SolutionsRamez AhmedNo ratings yet

- Practical Accounting 2: Angelito R. Punzalan, CPA, MBADocument33 pagesPractical Accounting 2: Angelito R. Punzalan, CPA, MBADaniella Mae Elip100% (1)

- Instructor: Võ H NG Đ C Group Members:: T Khánh LinhDocument20 pagesInstructor: Võ H NG Đ C Group Members:: T Khánh LinhMai Trần100% (1)

- Chapter 5 Financial Study (Part1) : A. Major AssumptionsDocument9 pagesChapter 5 Financial Study (Part1) : A. Major AssumptionsAnne XxNo ratings yet

- Chapter 5 FinallllllllllllDocument22 pagesChapter 5 Finallllllllllllsv7yyhdmkrNo ratings yet

- Financial StatementsDocument41 pagesFinancial StatementsJan Carla Cabusas CurimatmatNo ratings yet

- I. Financial AssumptionsDocument14 pagesI. Financial AssumptionsJaera shopaholicNo ratings yet

- Financial BreakevenDocument25 pagesFinancial Breakevenjoan villoNo ratings yet

- Financial Study - Garden of EdenDocument16 pagesFinancial Study - Garden of EdenEumar FabruadaNo ratings yet

- SomewhatDocument6 pagesSomewhatPauline VejanoNo ratings yet

- Unit 2Document79 pagesUnit 2Carlos Abadía MorenoNo ratings yet

- Ivd. Financial StatementDocument4 pagesIvd. Financial StatementDre AclonNo ratings yet

- The Financial Plan: Start-Up CapitalDocument7 pagesThe Financial Plan: Start-Up CapitalShany Mae PlaydaNo ratings yet

- Sabit FSDocument8 pagesSabit FSMilagrosa VillasNo ratings yet

- Capital Budgeting - Group AssignmentDocument15 pagesCapital Budgeting - Group AssignmentPhương Anh NguyễnNo ratings yet

- Pre-Cost 3,000,000.00 Pre-Operating ExpensesDocument10 pagesPre-Cost 3,000,000.00 Pre-Operating ExpensesJaselle TantogNo ratings yet

- Group 1 Chapter 5Document18 pagesGroup 1 Chapter 5Angelica GarciaNo ratings yet

- Powerol - Monthly MIS FormatDocument34 pagesPowerol - Monthly MIS Formatdharmender singhNo ratings yet

- A Feasibility Study On The Establishment of Housekeeping Recruitment AgencyDocument10 pagesA Feasibility Study On The Establishment of Housekeeping Recruitment AgencyMary Joy SumapidNo ratings yet

- Budget InformationDocument10 pagesBudget InformationIsabella BattiataNo ratings yet

- Juishat Financial Plan: College Park, Dipolog City Tel. No. (065) 212-8049 WebsiteDocument11 pagesJuishat Financial Plan: College Park, Dipolog City Tel. No. (065) 212-8049 WebsiteMeosjinNo ratings yet

- Nov. 6 DeadlineDocument11 pagesNov. 6 DeadlineAngelinee C.No ratings yet

- Financia ASPECT - FeedsDocument26 pagesFinancia ASPECT - FeedsEumar FabruadaNo ratings yet

- YeahDocument59 pagesYeahPrinceNo ratings yet

- New RevisedGREGORIO DULAY-BUSINESS-PLAN (Copy)Document11 pagesNew RevisedGREGORIO DULAY-BUSINESS-PLAN (Copy)Jnnfr DlyNo ratings yet

- Group 8Document27 pagesGroup 8Anna ChristineNo ratings yet

- Chapter 6 PDFDocument23 pagesChapter 6 PDFreyNo ratings yet

- SuleeDocument8 pagesSuleefuadzeyniNo ratings yet

- 11.bergerac SystemsDocument12 pages11.bergerac SystemsAviralNo ratings yet

- Simdora Manufacturing Private LTD: Project Report OnDocument14 pagesSimdora Manufacturing Private LTD: Project Report OnShivam DashottarNo ratings yet

- Red Chilli WorkingsDocument10 pagesRed Chilli WorkingsImran UmarNo ratings yet

- Financial Study LunaDocument9 pagesFinancial Study LunaNia LunaNo ratings yet

- Tài Methyl-Acetate-Plant-DesignDocument18 pagesTài Methyl-Acetate-Plant-DesignLe Anh QuânNo ratings yet

- Bsbfim601 Manage Finances Prepare BudgetsDocument9 pagesBsbfim601 Manage Finances Prepare BudgetsAli Butt100% (4)

- Nhựa Tiền Phong - Lê Tôn Bảo Huy 20213141Document12 pagesNhựa Tiền Phong - Lê Tôn Bảo Huy 20213141Huy Lê Tôn BảoNo ratings yet

- NSDC Project ReportDocument53 pagesNSDC Project ReportAbirMukherjee67% (3)

- Final Project FMGT 80Document12 pagesFinal Project FMGT 80Alma UriasNo ratings yet

- Income Statement Account Year 1 Year 2 Year 3 Year 4 Year 5Document1 pageIncome Statement Account Year 1 Year 2 Year 3 Year 4 Year 5Anonymous OWNHEhtDNo ratings yet

- Day 1 To Day 4Document186 pagesDay 1 To Day 4Sameer PadhyNo ratings yet

- Feasib Financials Part 1 DocsDocument27 pagesFeasib Financials Part 1 DocsThea SalvadorNo ratings yet

- Cost Accounting Questions Chapter 5Document7 pagesCost Accounting Questions Chapter 5Owais Khan KhattakNo ratings yet

- 5 Year Financial PlanDocument25 pages5 Year Financial Plananwar kadiNo ratings yet

- Bergerac XLS ENGDocument12 pagesBergerac XLS ENGTelmo Barros0% (1)

- Practice Questions For Final W Brick FinancialsDocument7 pagesPractice Questions For Final W Brick FinancialsJoana SilvaNo ratings yet

- V. Financial Feasibility StudyDocument14 pagesV. Financial Feasibility StudyEumar FabruadaNo ratings yet

- 5-Year Financial Plan - Manufacturing 1Document8 pages5-Year Financial Plan - Manufacturing 1tulalit008No ratings yet

- Ampalaya Ice CreamDocument12 pagesAmpalaya Ice CreamEdhel Bryan Corsiga SuicoNo ratings yet

- Final Chapter 6 Financial PlanDocument26 pagesFinal Chapter 6 Financial Planangelo felizardoNo ratings yet

- FY 2012 Audited Financial StatementsDocument0 pagesFY 2012 Audited Financial StatementsmontalvoartsNo ratings yet

- T&T Plastic Industries Balance Sheet For 2019 and 2020Document2 pagesT&T Plastic Industries Balance Sheet For 2019 and 2020Omar BadaamNo ratings yet

- CR AssignmentDocument16 pagesCR AssignmentWaleed KhalidNo ratings yet

- S.N. Particulars Amount (RS.) : Cost of ProjectDocument27 pagesS.N. Particulars Amount (RS.) : Cost of ProjectSuman yadavNo ratings yet

- Services & Offers and Financial ProjectionDocument13 pagesServices & Offers and Financial ProjectionMark Leonil FunaNo ratings yet

- Financial Analysis Template (NPV, IRR & PP)Document11 pagesFinancial Analysis Template (NPV, IRR & PP)charlainecebrian22No ratings yet

- Project 3 Develop and Use A Personal Budget and Saving PlanDocument7 pagesProject 3 Develop and Use A Personal Budget and Saving PlanKen Lati100% (1)

- Taxation: MD Mashiur Rahaman Robin KPMG-RRHDocument12 pagesTaxation: MD Mashiur Rahaman Robin KPMG-RRHZidan ZaifNo ratings yet

- Financial MaamDocument7 pagesFinancial MaamFandinola BeverlyNo ratings yet

- Pawn Shop Revenues World Summary: Market Values & Financials by CountryFrom EverandPawn Shop Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Miscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryFrom EverandMiscellaneous Intermediation Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Case Study 2Document4 pagesCase Study 2Sarwanti PurwandariNo ratings yet

- Sol. Man. - Chapter 4 Provisions, Cont. Liabs. & Cont. AssetsDocument9 pagesSol. Man. - Chapter 4 Provisions, Cont. Liabs. & Cont. AssetsEinez B. CarilloNo ratings yet

- Correction: Research and Development Should Be P5,000 Not P50,000Document43 pagesCorrection: Research and Development Should Be P5,000 Not P50,000Dieter LudwigNo ratings yet

- Income From Capital Gains - CS Executive Tax Laws MCQs - GST GunturDocument12 pagesIncome From Capital Gains - CS Executive Tax Laws MCQs - GST GunturDr A. K. SubramaniNo ratings yet

- Issue of SharesDocument24 pagesIssue of SharesManasNo ratings yet

- Public Listed IPO (TCS)Document6 pagesPublic Listed IPO (TCS)SatishNo ratings yet

- 5.3.2 Problems - Corporate LiquidationDocument16 pages5.3.2 Problems - Corporate LiquidationPaulina DocenaNo ratings yet

- Nature of CompanyDocument6 pagesNature of CompanyNaing AungNo ratings yet

- Hindenburg Report On Gautam Adani - Who Is Lying - Akash Banerjee & Manjul - EnglishDocument5 pagesHindenburg Report On Gautam Adani - Who Is Lying - Akash Banerjee & Manjul - EnglishShaik JilanNo ratings yet

- NCFM-Options Model PaperDocument15 pagesNCFM-Options Model Papergowtham2u2No ratings yet

- Ford Case Study (LT 11) - Jerry's Edit v2Document31 pagesFord Case Study (LT 11) - Jerry's Edit v2JerryJoshuaDiazNo ratings yet

- IpoDocument13 pagesIpoalan ruzarioNo ratings yet

- Nestle ExcelDocument2 pagesNestle ExcelWIly GurLsNo ratings yet

- Subramanyam Chapter07Document34 pagesSubramanyam Chapter07Saras Ina Pramesti100% (2)

- Rekha V.V.I. Commerce (Hons.) Part-3Document20 pagesRekha V.V.I. Commerce (Hons.) Part-3Ankur JhaNo ratings yet

- Open Book 30Document8 pagesOpen Book 30harshit bhattNo ratings yet

- 2020-07-03-CERA - NS-Ambit Capital PVT Lt-Cera Sanitaryware (BUY) Pain Is Inevitable!-89001883Document9 pages2020-07-03-CERA - NS-Ambit Capital PVT Lt-Cera Sanitaryware (BUY) Pain Is Inevitable!-89001883akanksha satijaNo ratings yet

- Currency Risk ManagementDocument14 pagesCurrency Risk ManagementAvayant Kumar SinghNo ratings yet

- Marasigan Medical Services - Ex 7Document4 pagesMarasigan Medical Services - Ex 7E.D.J100% (1)

- Solutions ManualDocument226 pagesSolutions Manualuzumakideva26No ratings yet

- 06 - Working Capital Management ProblemsDocument4 pages06 - Working Capital Management ProblemsMerr Fe PainaganNo ratings yet

- Chapter 3 (Tan&Lee) (Autosaved)Document67 pagesChapter 3 (Tan&Lee) (Autosaved)Dewi HazarNo ratings yet

- 3.6 ExercisesDocument8 pages3.6 ExercisesGeorgios MilitsisNo ratings yet

- Passenger Insurance: Your Ride With Rapido On 24 Apr 2022 at 06:07PM Is Now Insured!Document5 pagesPassenger Insurance: Your Ride With Rapido On 24 Apr 2022 at 06:07PM Is Now Insured!susmitha saiduNo ratings yet

- 2 Statement of Financial PositionDocument51 pages2 Statement of Financial PositionMarlon Ladesma100% (2)

- SiloDocument3 pagesSiloBilly ChandraNo ratings yet

- Financial Statements and Analysis: N Learning GoalsDocument3 pagesFinancial Statements and Analysis: N Learning GoalsJoyce De LunaNo ratings yet