Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5824)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- 50 SQL Query Questions You Should Practice For Interview PDFDocument15 pages50 SQL Query Questions You Should Practice For Interview PDFSangeeta Upadhyay67% (3)

- Manual API Testing Using Postman For Beginners PDFDocument8 pagesManual API Testing Using Postman For Beginners PDFSangeeta UpadhyayNo ratings yet

- Manual API Testing Using Postman For Beginners PDFDocument8 pagesManual API Testing Using Postman For Beginners PDFSangeeta UpadhyayNo ratings yet

- Admin 201 Certified Administrator NotesDocument69 pagesAdmin 201 Certified Administrator NotesSangeeta Upadhyay100% (2)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- What Is Software Testing - Definition, Types, Methods, ApproachesDocument17 pagesWhat Is Software Testing - Definition, Types, Methods, ApproachesSangeeta UpadhyayNo ratings yet

- Propaganda Rubric: Criteria Score 10 Score 8 Score 7 Score 6 Audiences and PurposeDocument1 pagePropaganda Rubric: Criteria Score 10 Score 8 Score 7 Score 6 Audiences and PurposePeter Allen Gomez100% (2)

- Hoshin Kanri Case StudyDocument3 pagesHoshin Kanri Case Studyogan97No ratings yet

- Mil STD 3034 PDFDocument64 pagesMil STD 3034 PDFJose D SalinasNo ratings yet

- Best Online Software Testing Training Course PDFDocument8 pagesBest Online Software Testing Training Course PDFSangeeta UpadhyayNo ratings yet

- Software Testing Interview Questions & AnswersDocument29 pagesSoftware Testing Interview Questions & AnswersSangeeta UpadhyayNo ratings yet

- Business Analysis Tutorial PDFDocument13 pagesBusiness Analysis Tutorial PDFSangeeta Upadhyay100% (1)

- Data Entry JobsDocument3 pagesData Entry JobsSangeeta UpadhyayNo ratings yet

- STLCDocument4 pagesSTLCSangeeta UpadhyayNo ratings yet

- STLCDocument4 pagesSTLCSangeeta UpadhyayNo ratings yet

- Software Development Life Cycle - SDLC - Software Testing MaterialDocument14 pagesSoftware Development Life Cycle - SDLC - Software Testing MaterialSangeeta UpadhyayNo ratings yet

- Technical ProfileDocument5 pagesTechnical ProfileSangeeta UpadhyayNo ratings yet

- Edit in PDFDocument1 pageEdit in PDFSangeeta UpadhyayNo ratings yet

- Crystal Report Viewer 1Document1 pageCrystal Report Viewer 1Sangeeta UpadhyayNo ratings yet

- Vacancy: Madhya Pradesh Agency For Promotion of Information Technology (MAP - IT)Document9 pagesVacancy: Madhya Pradesh Agency For Promotion of Information Technology (MAP - IT)Sangeeta UpadhyayNo ratings yet

- McaDocument4 pagesMcaSangeeta UpadhyayNo ratings yet

- Xiaomi. v281481691Document4 pagesXiaomi. v281481691Sangeeta UpadhyayNo ratings yet

- What's A Database System?Document5 pagesWhat's A Database System?Sangeeta UpadhyayNo ratings yet

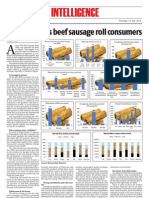

- Meet Nigeria's Beef Sausage Roll ConsumersDocument1 pageMeet Nigeria's Beef Sausage Roll ConsumersObodo EjiroNo ratings yet

- Segmenting The B2B Market-NotesDocument3 pagesSegmenting The B2B Market-NotesSamuel GeorgeNo ratings yet

- Demographic Factors Effect On InvestmentDocument12 pagesDemographic Factors Effect On InvestmentshobhikatyagiNo ratings yet

- 22 Immutable Laws of MarketingDocument2 pages22 Immutable Laws of MarketingDr. Wael El-Said100% (1)

- DISBURSEMENT REQUEST FORM - V4.1revisedDocument2 pagesDISBURSEMENT REQUEST FORM - V4.1revisedAnshul RastogiNo ratings yet

- Configuration TO Asset Accounting (Fi) : WelcomeDocument36 pagesConfiguration TO Asset Accounting (Fi) : Welcomevishal_160184No ratings yet

- CVPDocument20 pagesCVPDen Potxsz100% (1)

- TEMPLATE - PR Status ReportDocument8 pagesTEMPLATE - PR Status ReportVironica ValentineNo ratings yet

- University of Mumbai: Submitted ToDocument65 pagesUniversity of Mumbai: Submitted TomaheshNo ratings yet

- Project Synopsis Mba HR Stress Management in Bpo SectorDocument10 pagesProject Synopsis Mba HR Stress Management in Bpo Sectorsarla0% (1)

- Dimitri Iordan Planning For GrowthDocument34 pagesDimitri Iordan Planning For GrowthSoumyadeep BoseNo ratings yet

- Advertisement Vs Sales PromotionDocument29 pagesAdvertisement Vs Sales PromotionPoorna VenkatNo ratings yet

- Architects Code of EthicsDocument9 pagesArchitects Code of EthicsMark Gella Delfin100% (1)

- Pranab Das: Career ObjectiveDocument3 pagesPranab Das: Career ObjectiveMonirul IslamNo ratings yet

- Behind The SwooshDocument12 pagesBehind The Swooshapi-311844649No ratings yet

- USC LAW 408 - Compiled by JGF Sales Judge AdvientoDocument35 pagesUSC LAW 408 - Compiled by JGF Sales Judge Advientoalyza burdeosNo ratings yet

- UXUI Innovation HandbookDocument182 pagesUXUI Innovation Handbooki91171618No ratings yet

- 2015 Cambodia Ngo LawDocument10 pages2015 Cambodia Ngo LawAaron LincolnNo ratings yet

- Mentoring at SunDocument107 pagesMentoring at SunDeepshikha BhowmickNo ratings yet

- TLE W1 HaydecasisonDocument15 pagesTLE W1 Haydecasisonrhodora d. tamayoNo ratings yet

- LT E-BillDocument3 pagesLT E-Billsandeep khairnarNo ratings yet

- HRM Assignment: Training and Development Function of HPCLDocument11 pagesHRM Assignment: Training and Development Function of HPCLHarmanjit Singh DhillonNo ratings yet

- Grand Jury Report On Internal Audit DivisionDocument7 pagesGrand Jury Report On Internal Audit DivisionThe Press-Enterprise / pressenterprise.comNo ratings yet

- Para Jumble T2 Quiz 11 PDFDocument9 pagesPara Jumble T2 Quiz 11 PDFhimanshuNo ratings yet

- PECs Important TraitsDocument21 pagesPECs Important TraitsKyle Sean Shei ZeujnaraNo ratings yet

- Universidad Nacional de Colombia Intensive English Ii - Statement of Purpose VALENTINA RONCANCIO NIÑO C.C:1026.598.972 Europa Universitat ViadrinaDocument1 pageUniversidad Nacional de Colombia Intensive English Ii - Statement of Purpose VALENTINA RONCANCIO NIÑO C.C:1026.598.972 Europa Universitat ViadrinaValentina RoncancioNo ratings yet

- Investopedia. Using - The Greeks - To Undersand OptionsDocument5 pagesInvestopedia. Using - The Greeks - To Undersand OptionsEnrique BustillosNo ratings yet